Jeronimo Martins PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

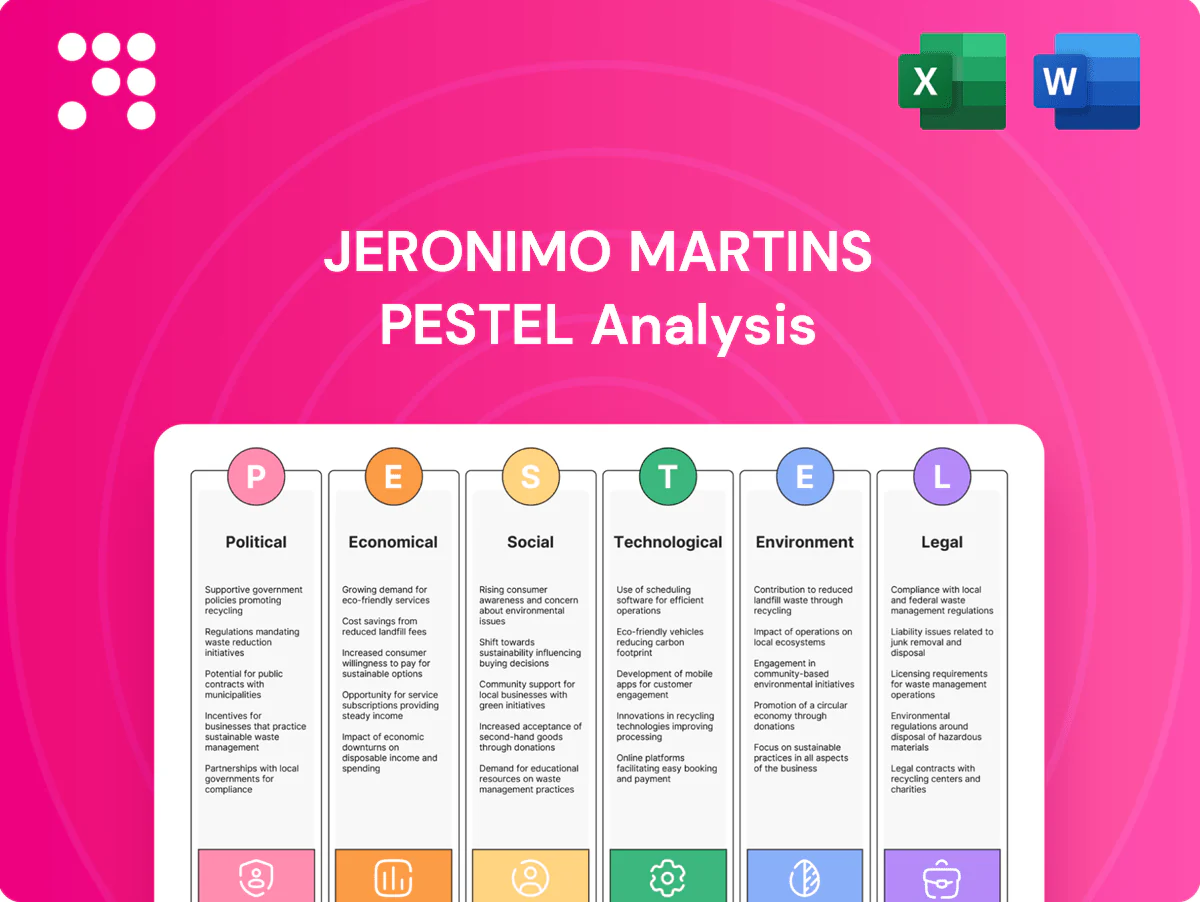

Gain strategic clarity with our concise PESTLE analysis of Jeronimo Martins—identifying political, economic, social, technological, legal and environmental forces shaping growth. Ideal for investors and planners seeking quick, actionable intel. Buy the full report for the complete, editable breakdown and instant download.

Political factors

EU and national retail policies

Operating mainly in Portugal (≈10.31m people) and Poland (≈38.1m) exposes Jerónimo Martins to EU competition, food-safety and trade rules while its Biedronka chain (over 3,000 stores) faces cross-border rivals and regulatory scrutiny. Policy shifts on retail zoning or trading hours can rapidly reshape store expansion plans and capex. CAP reforms (EU 2021–27 budget €386.6bn) influence suppliers’ costs and availability. Stable EU governance aids planning but raises compliance complexity and costs.

Poland’s regulatory direction

Poland is a core profit driver for Jeronimo Martins, where Biedronka runs over 3,000 stores. Existing Sunday trading restrictions (introduced 2018) and any loosening/tightening affect footfall and shift rostering. Poland's standard VAT is 23%, so rate changes directly impact shelf prices and margins. Political turnover can rapidly alter wage, tax and retail rules, raising operational risk.

Colombia’s policy and security climate

Colombia, Latin America's fourth-largest economy with about 51 million people (2025), offers growth but higher political and security variability that raises operational risk for Jeronimo Martins. Recent tax-reform debates, import-tariff adjustments and occasional FX controls can quickly shift cost structures and margins. Periodic public-order incidents disrupt logistics and store openings, while active government debates on nutrition policy and price controls could force assortment and pricing changes.

Trade and supply chain geopolitics

Global tensions can disrupt food imports, packaging and energy inputs, increasing volatility in Jerónimo Martins supply chains. Sanctions and transport bottlenecks raise lead times and procurement costs, pressuring margins. Diversifying sourcing reduces single-country exposure while customs changes force agile procurement and higher inventory buffers.

- Supply disruption

- Higher lead times/costs

- Sourcing diversification

- Agile procurement & buffers

Public health and food policy

Nutrition labeling, sugar taxes and alcohol rules keep evolving — Poland introduced a beverage sugar tax in 2021 — while the EU Farm to Fork target aims for 25% organic land by 2030, pushing demand for healthier private labels. Pandemic-era lessons keep preparedness expectations high; vaccine or health-certificate regimes in 2021–22 demonstrated potential to constrain labor availability.

- Poland sugar tax: implemented 2021

- EU Farm to Fork: 25% organic by 2030

- Pandemic preparedness increases compliance costs

- Health certificates can reduce workforce availability

EU policy, Poland VAT and trading-hour shifts raise costs; Colombia adds tax, security, FX risk

Operating in Portugal (≈10.31m) and Poland (≈38.1m) exposes Jerónimo Martins and Biedronka (>3,000 stores) to EU competition, trading-hour and zoning shifts that affect expansion and capex. EU CAP budget €386.6bn (2021–27) and Poland VAT 23% change supplier costs and margins. Colombia (≈51m, 2025) adds tax, security and FX risks. Global trade tensions raise import lead times and costs.

| Jurisdiction | Key political risks | Data |

|---|---|---|

| Portugal | EU rules, zoning | Pop ≈10.31m |

| Poland | Trading hours, VAT, sugar tax | Pop ≈38.1m; VAT 23%; sugar tax 2021; Biedronka >3,000 |

| Colombia | Tax, security, FX | Pop ≈51m (2025) |

What is included in the product

Explores how macro-environmental factors uniquely affect Jerónimo Martins across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, region-specific regulatory context and forward-looking insights to help executives and investors identify risks, opportunities and strategic responses.

A compact, visually segmented PESTLE summary for Jerónimo Martins that eases meeting prep and is editable for local market notes—drop-ready for slides, shareable across teams, and written in plain language to support risk discussions and client reports.

Economic factors

Inflation and consumer purchasing power

Food inflation compresses real incomes—Euro area food inflation eased to c.4% in 2024—pushing consumers toward private label, where Jerónimo Martins leverages c.30% penetration in key banners to protect volumes.

High price elasticity forces tight mix and promo management; rapid cost pass-through risks losing share, so JMT balances competitiveness and margin through targeted promotions and SKU rationalisation.

In deflationary windows, rapid price investment is required to defend share, as prolonged pass-through delays have historically led to volume erosion in FMCG markets.

Wage growth and labor markets

Minimum wage hikes — Portugal €820 (2024), Poland PLN 4,300 (2024) and Colombia COP 1,300,000 (2024) — lift Jeronimo Martins’ labor costs across core markets. Tight labor markets push higher retention spend and productivity levers; turnover in retail remains elevated post-pandemic. Investment in automation, self-checkouts and scheduling optimization helps offset wage pressure. Outcomes of collective bargaining in each country can materially shift cost trajectories.

FX volatility and translation risk

PLN and Colombian peso swings directly affect Jeronimo Martins’ cost of goods sold and translated reported earnings across its Poland and Colombia operations. Hedging programs reduce short-term volatility but cannot fully offset large macro shocks or abrupt commodity-price shifts. Reliance on imported commodities and packaging increases FX pass-through risk, while dynamic pricing and greater local sourcing help cushion margin impacts.

Commodity and energy costs

Food inputs, fertilizers and energy are primary drivers of Jeronimo Martins’ gross margin variability, especially in fresh categories exposed to seasonal supply; procurement scale and long-term supplier contracts in Poland and Portugal smooth purchase-price volatility. Energy-efficiency investments and on-site generation reduce cost swings and cut emissions, while weather shocks can abruptly spike fruit, vegetable and meat prices.

- procurement scale stabilizes costs

- long-term contracts reduce input volatility

- energy programs lower consumption and emissions

- weather shocks raise fresh-category prices

Consumer demand cycles

Cyclicality in EU consumption and Colombia’s divergent growth paths drive store traffic shifts for Jerónimo Martins, with weaker periods pushing shoppers toward Biedronka and Ara discount ranges while expansions lift premium private-label and fresh segments, improving mix; basket size and visit frequency fall in downturns and rebound in recoveries, requiring dynamic assortment and pricing to protect margins.

- trend: downturns boost discount/value tiers

- trend: expansions raise premium/private-label mix

- action: agile promo calendar tied to basket/frequency

EU policy, Poland VAT and trading-hour shifts raise costs; Colombia adds tax, security, FX risk

Food inflation ~4% in 2024 compresses real incomes, pushing consumers to private label where Jerónimo Martins holds c.30% penetration to protect volumes.

Minimum wages (Portugal €820, Poland PLN4,300, Colombia COP1,300,000 in 2024) raise labor costs; automation and scheduling offset pressure.

FX swings and commodity/energy volatility drive COGS and reported earnings; hedging and local sourcing mitigate but not eliminate risk.

| Metric | 2024/2025 |

|---|---|

| Food inflation (EU) | ~4% (2024) |

| Private-label penetration | ~30% |

| Min wages | PT €820 / PLN4,300 / COP1,300,000 (2024) |

Same Document Delivered

Jeronimo Martins PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Jeronimo Martins PESTLE Analysis contains complete political, economic, social, technological, legal and environmental assessments. No placeholders or teasers—what you see is the final file.

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our concise PESTLE analysis of Jeronimo Martins—identifying political, economic, social, technological, legal and environmental forces shaping growth. Ideal for investors and planners seeking quick, actionable intel. Buy the full report for the complete, editable breakdown and instant download.

Political factors

EU and national retail policies

Operating mainly in Portugal (≈10.31m people) and Poland (≈38.1m) exposes Jerónimo Martins to EU competition, food-safety and trade rules while its Biedronka chain (over 3,000 stores) faces cross-border rivals and regulatory scrutiny. Policy shifts on retail zoning or trading hours can rapidly reshape store expansion plans and capex. CAP reforms (EU 2021–27 budget €386.6bn) influence suppliers’ costs and availability. Stable EU governance aids planning but raises compliance complexity and costs.

Poland’s regulatory direction

Poland is a core profit driver for Jeronimo Martins, where Biedronka runs over 3,000 stores. Existing Sunday trading restrictions (introduced 2018) and any loosening/tightening affect footfall and shift rostering. Poland's standard VAT is 23%, so rate changes directly impact shelf prices and margins. Political turnover can rapidly alter wage, tax and retail rules, raising operational risk.

Colombia’s policy and security climate

Colombia, Latin America's fourth-largest economy with about 51 million people (2025), offers growth but higher political and security variability that raises operational risk for Jeronimo Martins. Recent tax-reform debates, import-tariff adjustments and occasional FX controls can quickly shift cost structures and margins. Periodic public-order incidents disrupt logistics and store openings, while active government debates on nutrition policy and price controls could force assortment and pricing changes.

Trade and supply chain geopolitics

Global tensions can disrupt food imports, packaging and energy inputs, increasing volatility in Jerónimo Martins supply chains. Sanctions and transport bottlenecks raise lead times and procurement costs, pressuring margins. Diversifying sourcing reduces single-country exposure while customs changes force agile procurement and higher inventory buffers.

- Supply disruption

- Higher lead times/costs

- Sourcing diversification

- Agile procurement & buffers

Public health and food policy

Nutrition labeling, sugar taxes and alcohol rules keep evolving — Poland introduced a beverage sugar tax in 2021 — while the EU Farm to Fork target aims for 25% organic land by 2030, pushing demand for healthier private labels. Pandemic-era lessons keep preparedness expectations high; vaccine or health-certificate regimes in 2021–22 demonstrated potential to constrain labor availability.

- Poland sugar tax: implemented 2021

- EU Farm to Fork: 25% organic by 2030

- Pandemic preparedness increases compliance costs

- Health certificates can reduce workforce availability

EU policy, Poland VAT and trading-hour shifts raise costs; Colombia adds tax, security, FX risk

Operating in Portugal (≈10.31m) and Poland (≈38.1m) exposes Jerónimo Martins and Biedronka (>3,000 stores) to EU competition, trading-hour and zoning shifts that affect expansion and capex. EU CAP budget €386.6bn (2021–27) and Poland VAT 23% change supplier costs and margins. Colombia (≈51m, 2025) adds tax, security and FX risks. Global trade tensions raise import lead times and costs.

| Jurisdiction | Key political risks | Data |

|---|---|---|

| Portugal | EU rules, zoning | Pop ≈10.31m |

| Poland | Trading hours, VAT, sugar tax | Pop ≈38.1m; VAT 23%; sugar tax 2021; Biedronka >3,000 |

| Colombia | Tax, security, FX | Pop ≈51m (2025) |

What is included in the product

Explores how macro-environmental factors uniquely affect Jerónimo Martins across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, region-specific regulatory context and forward-looking insights to help executives and investors identify risks, opportunities and strategic responses.

A compact, visually segmented PESTLE summary for Jerónimo Martins that eases meeting prep and is editable for local market notes—drop-ready for slides, shareable across teams, and written in plain language to support risk discussions and client reports.

Economic factors

Inflation and consumer purchasing power

Food inflation compresses real incomes—Euro area food inflation eased to c.4% in 2024—pushing consumers toward private label, where Jerónimo Martins leverages c.30% penetration in key banners to protect volumes.

High price elasticity forces tight mix and promo management; rapid cost pass-through risks losing share, so JMT balances competitiveness and margin through targeted promotions and SKU rationalisation.

In deflationary windows, rapid price investment is required to defend share, as prolonged pass-through delays have historically led to volume erosion in FMCG markets.

Wage growth and labor markets

Minimum wage hikes — Portugal €820 (2024), Poland PLN 4,300 (2024) and Colombia COP 1,300,000 (2024) — lift Jeronimo Martins’ labor costs across core markets. Tight labor markets push higher retention spend and productivity levers; turnover in retail remains elevated post-pandemic. Investment in automation, self-checkouts and scheduling optimization helps offset wage pressure. Outcomes of collective bargaining in each country can materially shift cost trajectories.

FX volatility and translation risk

PLN and Colombian peso swings directly affect Jeronimo Martins’ cost of goods sold and translated reported earnings across its Poland and Colombia operations. Hedging programs reduce short-term volatility but cannot fully offset large macro shocks or abrupt commodity-price shifts. Reliance on imported commodities and packaging increases FX pass-through risk, while dynamic pricing and greater local sourcing help cushion margin impacts.

Commodity and energy costs

Food inputs, fertilizers and energy are primary drivers of Jeronimo Martins’ gross margin variability, especially in fresh categories exposed to seasonal supply; procurement scale and long-term supplier contracts in Poland and Portugal smooth purchase-price volatility. Energy-efficiency investments and on-site generation reduce cost swings and cut emissions, while weather shocks can abruptly spike fruit, vegetable and meat prices.

- procurement scale stabilizes costs

- long-term contracts reduce input volatility

- energy programs lower consumption and emissions

- weather shocks raise fresh-category prices

Consumer demand cycles

Cyclicality in EU consumption and Colombia’s divergent growth paths drive store traffic shifts for Jerónimo Martins, with weaker periods pushing shoppers toward Biedronka and Ara discount ranges while expansions lift premium private-label and fresh segments, improving mix; basket size and visit frequency fall in downturns and rebound in recoveries, requiring dynamic assortment and pricing to protect margins.

- trend: downturns boost discount/value tiers

- trend: expansions raise premium/private-label mix

- action: agile promo calendar tied to basket/frequency

EU policy, Poland VAT and trading-hour shifts raise costs; Colombia adds tax, security, FX risk

Food inflation ~4% in 2024 compresses real incomes, pushing consumers to private label where Jerónimo Martins holds c.30% penetration to protect volumes.

Minimum wages (Portugal €820, Poland PLN4,300, Colombia COP1,300,000 in 2024) raise labor costs; automation and scheduling offset pressure.

FX swings and commodity/energy volatility drive COGS and reported earnings; hedging and local sourcing mitigate but not eliminate risk.

| Metric | 2024/2025 |

|---|---|

| Food inflation (EU) | ~4% (2024) |

| Private-label penetration | ~30% |

| Min wages | PT €820 / PLN4,300 / COP1,300,000 (2024) |

Same Document Delivered

Jeronimo Martins PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Jeronimo Martins PESTLE Analysis contains complete political, economic, social, technological, legal and environmental assessments. No placeholders or teasers—what you see is the final file.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our concise PESTLE analysis of Jeronimo Martins—identifying political, economic, social, technological, legal and environmental forces shaping growth. Ideal for investors and planners seeking quick, actionable intel. Buy the full report for the complete, editable breakdown and instant download.

Political factors

EU and national retail policies

Operating mainly in Portugal (≈10.31m people) and Poland (≈38.1m) exposes Jerónimo Martins to EU competition, food-safety and trade rules while its Biedronka chain (over 3,000 stores) faces cross-border rivals and regulatory scrutiny. Policy shifts on retail zoning or trading hours can rapidly reshape store expansion plans and capex. CAP reforms (EU 2021–27 budget €386.6bn) influence suppliers’ costs and availability. Stable EU governance aids planning but raises compliance complexity and costs.

Poland’s regulatory direction

Poland is a core profit driver for Jeronimo Martins, where Biedronka runs over 3,000 stores. Existing Sunday trading restrictions (introduced 2018) and any loosening/tightening affect footfall and shift rostering. Poland's standard VAT is 23%, so rate changes directly impact shelf prices and margins. Political turnover can rapidly alter wage, tax and retail rules, raising operational risk.

Colombia’s policy and security climate

Colombia, Latin America's fourth-largest economy with about 51 million people (2025), offers growth but higher political and security variability that raises operational risk for Jeronimo Martins. Recent tax-reform debates, import-tariff adjustments and occasional FX controls can quickly shift cost structures and margins. Periodic public-order incidents disrupt logistics and store openings, while active government debates on nutrition policy and price controls could force assortment and pricing changes.

Trade and supply chain geopolitics

Global tensions can disrupt food imports, packaging and energy inputs, increasing volatility in Jerónimo Martins supply chains. Sanctions and transport bottlenecks raise lead times and procurement costs, pressuring margins. Diversifying sourcing reduces single-country exposure while customs changes force agile procurement and higher inventory buffers.

- Supply disruption

- Higher lead times/costs

- Sourcing diversification

- Agile procurement & buffers

Public health and food policy

Nutrition labeling, sugar taxes and alcohol rules keep evolving — Poland introduced a beverage sugar tax in 2021 — while the EU Farm to Fork target aims for 25% organic land by 2030, pushing demand for healthier private labels. Pandemic-era lessons keep preparedness expectations high; vaccine or health-certificate regimes in 2021–22 demonstrated potential to constrain labor availability.

- Poland sugar tax: implemented 2021

- EU Farm to Fork: 25% organic by 2030

- Pandemic preparedness increases compliance costs

- Health certificates can reduce workforce availability

EU policy, Poland VAT and trading-hour shifts raise costs; Colombia adds tax, security, FX risk

Operating in Portugal (≈10.31m) and Poland (≈38.1m) exposes Jerónimo Martins and Biedronka (>3,000 stores) to EU competition, trading-hour and zoning shifts that affect expansion and capex. EU CAP budget €386.6bn (2021–27) and Poland VAT 23% change supplier costs and margins. Colombia (≈51m, 2025) adds tax, security and FX risks. Global trade tensions raise import lead times and costs.

| Jurisdiction | Key political risks | Data |

|---|---|---|

| Portugal | EU rules, zoning | Pop ≈10.31m |

| Poland | Trading hours, VAT, sugar tax | Pop ≈38.1m; VAT 23%; sugar tax 2021; Biedronka >3,000 |

| Colombia | Tax, security, FX | Pop ≈51m (2025) |

What is included in the product

Explores how macro-environmental factors uniquely affect Jerónimo Martins across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, region-specific regulatory context and forward-looking insights to help executives and investors identify risks, opportunities and strategic responses.

A compact, visually segmented PESTLE summary for Jerónimo Martins that eases meeting prep and is editable for local market notes—drop-ready for slides, shareable across teams, and written in plain language to support risk discussions and client reports.

Economic factors

Inflation and consumer purchasing power

Food inflation compresses real incomes—Euro area food inflation eased to c.4% in 2024—pushing consumers toward private label, where Jerónimo Martins leverages c.30% penetration in key banners to protect volumes.

High price elasticity forces tight mix and promo management; rapid cost pass-through risks losing share, so JMT balances competitiveness and margin through targeted promotions and SKU rationalisation.

In deflationary windows, rapid price investment is required to defend share, as prolonged pass-through delays have historically led to volume erosion in FMCG markets.

Wage growth and labor markets

Minimum wage hikes — Portugal €820 (2024), Poland PLN 4,300 (2024) and Colombia COP 1,300,000 (2024) — lift Jeronimo Martins’ labor costs across core markets. Tight labor markets push higher retention spend and productivity levers; turnover in retail remains elevated post-pandemic. Investment in automation, self-checkouts and scheduling optimization helps offset wage pressure. Outcomes of collective bargaining in each country can materially shift cost trajectories.

FX volatility and translation risk

PLN and Colombian peso swings directly affect Jeronimo Martins’ cost of goods sold and translated reported earnings across its Poland and Colombia operations. Hedging programs reduce short-term volatility but cannot fully offset large macro shocks or abrupt commodity-price shifts. Reliance on imported commodities and packaging increases FX pass-through risk, while dynamic pricing and greater local sourcing help cushion margin impacts.

Commodity and energy costs

Food inputs, fertilizers and energy are primary drivers of Jeronimo Martins’ gross margin variability, especially in fresh categories exposed to seasonal supply; procurement scale and long-term supplier contracts in Poland and Portugal smooth purchase-price volatility. Energy-efficiency investments and on-site generation reduce cost swings and cut emissions, while weather shocks can abruptly spike fruit, vegetable and meat prices.

- procurement scale stabilizes costs

- long-term contracts reduce input volatility

- energy programs lower consumption and emissions

- weather shocks raise fresh-category prices

Consumer demand cycles

Cyclicality in EU consumption and Colombia’s divergent growth paths drive store traffic shifts for Jerónimo Martins, with weaker periods pushing shoppers toward Biedronka and Ara discount ranges while expansions lift premium private-label and fresh segments, improving mix; basket size and visit frequency fall in downturns and rebound in recoveries, requiring dynamic assortment and pricing to protect margins.

- trend: downturns boost discount/value tiers

- trend: expansions raise premium/private-label mix

- action: agile promo calendar tied to basket/frequency

EU policy, Poland VAT and trading-hour shifts raise costs; Colombia adds tax, security, FX risk

Food inflation ~4% in 2024 compresses real incomes, pushing consumers to private label where Jerónimo Martins holds c.30% penetration to protect volumes.

Minimum wages (Portugal €820, Poland PLN4,300, Colombia COP1,300,000 in 2024) raise labor costs; automation and scheduling offset pressure.

FX swings and commodity/energy volatility drive COGS and reported earnings; hedging and local sourcing mitigate but not eliminate risk.

| Metric | 2024/2025 |

|---|---|

| Food inflation (EU) | ~4% (2024) |

| Private-label penetration | ~30% |

| Min wages | PT €820 / PLN4,300 / COP1,300,000 (2024) |

Same Document Delivered

Jeronimo Martins PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Jeronimo Martins PESTLE Analysis contains complete political, economic, social, technological, legal and environmental assessments. No placeholders or teasers—what you see is the final file.