JetBlue Porter's Five Forces Analysis

From Overview to Strategy Blueprint

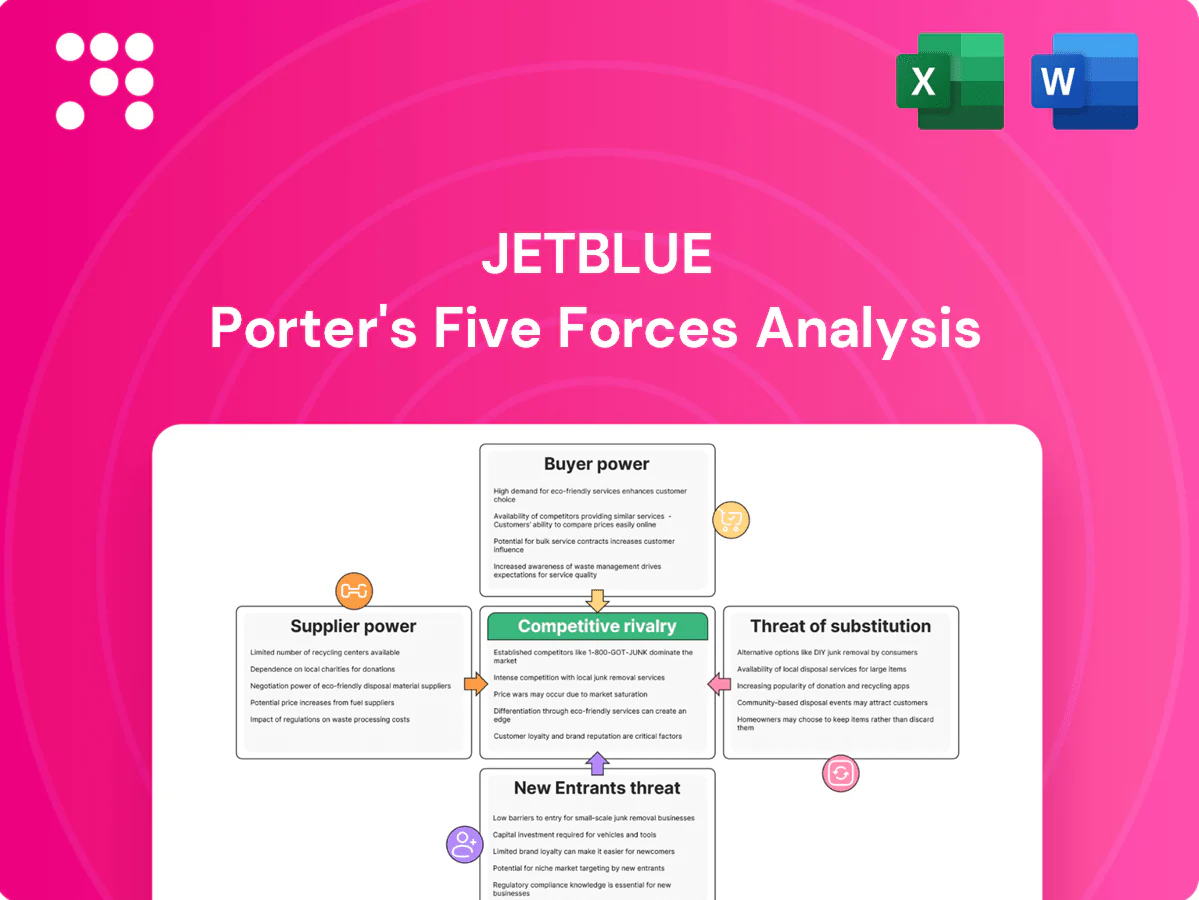

JetBlue faces intense rivalry from legacy carriers and low-cost rivals, moderate supplier power driven by aircraft and fuel costs, and evolving buyer leverage as customers demand low fares and loyalty perks. Regulatory and network barriers temper new entrants while substitutes like high-speed rail remain limited in the U.S. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore JetBlue’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated aircraft OEMs

JetBlue depends on a duopoly—Airbus and Boeing, which together supply roughly 98% of large commercial jets—giving suppliers strong leverage over pricing, delivery slots, and cabin configuration for JetBlue’s ~270-aircraft system (2024). Limited OEM alternatives constrain negotiation power and fleet flexibility, so production delays or quality issues ripple into capacity and unit-cost plans. Long lead times of 3–5+ years lock in capital commitments.

Engine and MRO dependence

Engine OEMs GE, Pratt & Whitney and Rolls‑Royce hold proprietary IP and parts control over most commercial engines, giving them aftermarket pricing power and influence over turnaround times; the global commercial MRO market was about $90 billion in 2023. Technical failures can ground aircraft and spike maintenance costs, and while contracts and warranties mitigate risk, they rarely eliminate OEM/MRO leverage; certified shop scarcity raises switching costs.

Jet fuel volatility and suppliers

Jet fuel is a volatile commodity and accounted for roughly 20–25% of airline operating costs in 2024, limiting JetBlue’s ability to pass sudden spikes to passengers without hurting demand. Supply is fragmented but airport-specific infrastructure bottlenecks can push local jet-fuel margins higher. Financial hedges only partially mitigate price exposure, and 2024-era environmental policies plus SAF priced roughly 3–5x Jet A are shifting long-term cost curves.

Airport access, slots, and gate control

Airport authorities and slot coordinators at congested hubs like LaGuardia and Reagan National (both FAA slot-controlled in 2024) hold scarce takeoff and landing rights, giving them leverage over carriers such as JetBlue; fees, gate availability, and curfew rules raise operating costs and constrain scheduling. Access limits can cap growth and force capacity tradeoffs, so airlines often exchange long-term commercial commitments for guaranteed slots and gates.

- FAA slot control: LaGuardia, Reagan National (2024)

- Negotiation lever: fees, gate leases, curfews

- Outcome: long-term commitments for capacity rights

Unionized labor and skilled crews

Airlines squeezed by supplier power: OEM duopoly, engine MRO control, fuel volatility, unions

JetBlue faces high supplier bargaining power: Airbus/Boeing duopoly (~98% large jets), engine OEMs with aftermarket control, volatile jet fuel (20–25% of ops in 2024) and strong unionized labor—each constrains pricing, delivery flexibility and capacity decisions.

| Supplier | Metric | 2024 |

|---|---|---|

| Airframe OEMs | Market share | ~98% |

| Engines/MRO | Global MRO | $90B |

| Fuel | Cost share | 20–25% |

| Labor | Pressure | High |

What is included in the product

Concise Porter's Five Forces analysis of JetBlue assessing competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and regulatory dynamics to highlight pressure points, strategic advantages, and emerging disruptions to its profitability.

A clear one-sheet Porter's Five Forces for JetBlue—perfect for quick strategic decisions and investor meetings. Swap in route-specific data, adjust force intensity for market shifts, and export charts into decks without macros.

Customers Bargaining Power

High price sensitivity

JetBlue’s customer mix skews toward leisure travelers who are highly price elastic, so even small fare differences drive switching to rivals. Promotional fares and ancillary bundles (seat, bags, Wi‑Fi) are pivotal to capture demand. Macroeconomic shifts rapidly alter willingness to pay — US CPI averaged about 3.4% in 2024 (BLS), pressuring discretionary travel budgets and price sensitivity.

Low switching costs

Low switching costs let travelers compare fares instantly via OTAs and metasearch, with these channels accounting for ≈50% of online flight bookings in recent industry reports (2023–24), eroding loyalty. Route-by-route alternatives intensify choice, while cancellation policies and credits influence decisions but seldom lock customers. Convenience and schedule frequently trump brand in purchase decisions.

Transparency via digital channels

Real-time fare visibility via OTAs and metasearch forces JetBlue to protect yields, compressing margins on competitive routes as fares fluctuate; dynamic pricing must balance higher load factors with reputation risk from sharp fare swings. Reviews and social media amplify service lapses—over 70% of travelers say online feedback influences choices. Ancillary clarity matters: ancillary revenue was over 10% of US airline revenue in 2024.

Loyalty and product differentiation

TrueBlue loyalty, seat comfort and in‑flight experience reduce buyer power by raising perceived value; JetBlue’s premium‑economy style products create micro‑segments but must justify typical fare deltas of about 20–40% to hold customers, and co‑brand cards add modest switching costs via bonus points and status perks.

- TrueBlue loyalty: customer retention

- Seat comfort/in‑flight: perceived value

- Premium economy: micro‑segmentation, 20–40% fare delta

- Co‑brand cards: modest switching costs

Corporate and group contracts

While JetBlue remains leisure-skewed, corporate and group contracts secure discounted fares and inventory access; concentrated accounts can command fare concessions and service guarantees, affecting yield management and distribution.

Renewals hinge on performance clauses and disruption handling; mixed-cabin (Mint/Even More Space) strategies can grow share without full price erosion.

- Corporate share: ~10–20% of airline revenue pools (industry range)

- Concentrated accounts leverage bulk discounts and service SLAs

- Performance clauses, disruption payouts key in renewals

- Mixed-cabin upsell preserves fares while expanding share

Leisure carrier facing buyer power; OTAs ≈50% bookings, yields squeezed

JetBlue faces high customer bargaining power: leisure-skewed, price-elastic demand with OTAs/metasearch ≈50% of bookings (2023–24) and US CPI ~3.4% in 2024 tightening budgets. Ancillary revenue >10% of US airline revenue (2024) and visible fares compress yields; loyalty programs and Mint/Even More Space raise switching costs modestly. Corporate accounts (~10–20% share) extract discounts and SLAs, influencing renewals.

| Metric | Value |

|---|---|

| OTAs/metasearch share | ≈50% (2023–24) |

| US CPI | ≈3.4% (2024, BLS) |

| Ancillary revenue | >10% (2024, US airlines) |

| Corporate revenue share | ≈10–20% |

Full Version Awaits

JetBlue Porter's Five Forces Analysis

This JetBlue Porter’s Five Forces Analysis preview is the exact, fully formatted document you’ll receive immediately after purchase. It contains the complete competitive assessment—threat of entrants, buyer and supplier power, substitutes, and rivalry—ready for download and use. No placeholders, samples, or edits required.

From Overview to Strategy Blueprint

JetBlue faces intense rivalry from legacy carriers and low-cost rivals, moderate supplier power driven by aircraft and fuel costs, and evolving buyer leverage as customers demand low fares and loyalty perks. Regulatory and network barriers temper new entrants while substitutes like high-speed rail remain limited in the U.S. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore JetBlue’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated aircraft OEMs

JetBlue depends on a duopoly—Airbus and Boeing, which together supply roughly 98% of large commercial jets—giving suppliers strong leverage over pricing, delivery slots, and cabin configuration for JetBlue’s ~270-aircraft system (2024). Limited OEM alternatives constrain negotiation power and fleet flexibility, so production delays or quality issues ripple into capacity and unit-cost plans. Long lead times of 3–5+ years lock in capital commitments.

Engine and MRO dependence

Engine OEMs GE, Pratt & Whitney and Rolls‑Royce hold proprietary IP and parts control over most commercial engines, giving them aftermarket pricing power and influence over turnaround times; the global commercial MRO market was about $90 billion in 2023. Technical failures can ground aircraft and spike maintenance costs, and while contracts and warranties mitigate risk, they rarely eliminate OEM/MRO leverage; certified shop scarcity raises switching costs.

Jet fuel volatility and suppliers

Jet fuel is a volatile commodity and accounted for roughly 20–25% of airline operating costs in 2024, limiting JetBlue’s ability to pass sudden spikes to passengers without hurting demand. Supply is fragmented but airport-specific infrastructure bottlenecks can push local jet-fuel margins higher. Financial hedges only partially mitigate price exposure, and 2024-era environmental policies plus SAF priced roughly 3–5x Jet A are shifting long-term cost curves.

Airport access, slots, and gate control

Airport authorities and slot coordinators at congested hubs like LaGuardia and Reagan National (both FAA slot-controlled in 2024) hold scarce takeoff and landing rights, giving them leverage over carriers such as JetBlue; fees, gate availability, and curfew rules raise operating costs and constrain scheduling. Access limits can cap growth and force capacity tradeoffs, so airlines often exchange long-term commercial commitments for guaranteed slots and gates.

- FAA slot control: LaGuardia, Reagan National (2024)

- Negotiation lever: fees, gate leases, curfews

- Outcome: long-term commitments for capacity rights

Unionized labor and skilled crews

Airlines squeezed by supplier power: OEM duopoly, engine MRO control, fuel volatility, unions

JetBlue faces high supplier bargaining power: Airbus/Boeing duopoly (~98% large jets), engine OEMs with aftermarket control, volatile jet fuel (20–25% of ops in 2024) and strong unionized labor—each constrains pricing, delivery flexibility and capacity decisions.

| Supplier | Metric | 2024 |

|---|---|---|

| Airframe OEMs | Market share | ~98% |

| Engines/MRO | Global MRO | $90B |

| Fuel | Cost share | 20–25% |

| Labor | Pressure | High |

What is included in the product

Concise Porter's Five Forces analysis of JetBlue assessing competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and regulatory dynamics to highlight pressure points, strategic advantages, and emerging disruptions to its profitability.

A clear one-sheet Porter's Five Forces for JetBlue—perfect for quick strategic decisions and investor meetings. Swap in route-specific data, adjust force intensity for market shifts, and export charts into decks without macros.

Customers Bargaining Power

High price sensitivity

JetBlue’s customer mix skews toward leisure travelers who are highly price elastic, so even small fare differences drive switching to rivals. Promotional fares and ancillary bundles (seat, bags, Wi‑Fi) are pivotal to capture demand. Macroeconomic shifts rapidly alter willingness to pay — US CPI averaged about 3.4% in 2024 (BLS), pressuring discretionary travel budgets and price sensitivity.

Low switching costs

Low switching costs let travelers compare fares instantly via OTAs and metasearch, with these channels accounting for ≈50% of online flight bookings in recent industry reports (2023–24), eroding loyalty. Route-by-route alternatives intensify choice, while cancellation policies and credits influence decisions but seldom lock customers. Convenience and schedule frequently trump brand in purchase decisions.

Transparency via digital channels

Real-time fare visibility via OTAs and metasearch forces JetBlue to protect yields, compressing margins on competitive routes as fares fluctuate; dynamic pricing must balance higher load factors with reputation risk from sharp fare swings. Reviews and social media amplify service lapses—over 70% of travelers say online feedback influences choices. Ancillary clarity matters: ancillary revenue was over 10% of US airline revenue in 2024.

Loyalty and product differentiation

TrueBlue loyalty, seat comfort and in‑flight experience reduce buyer power by raising perceived value; JetBlue’s premium‑economy style products create micro‑segments but must justify typical fare deltas of about 20–40% to hold customers, and co‑brand cards add modest switching costs via bonus points and status perks.

- TrueBlue loyalty: customer retention

- Seat comfort/in‑flight: perceived value

- Premium economy: micro‑segmentation, 20–40% fare delta

- Co‑brand cards: modest switching costs

Corporate and group contracts

While JetBlue remains leisure-skewed, corporate and group contracts secure discounted fares and inventory access; concentrated accounts can command fare concessions and service guarantees, affecting yield management and distribution.

Renewals hinge on performance clauses and disruption handling; mixed-cabin (Mint/Even More Space) strategies can grow share without full price erosion.

- Corporate share: ~10–20% of airline revenue pools (industry range)

- Concentrated accounts leverage bulk discounts and service SLAs

- Performance clauses, disruption payouts key in renewals

- Mixed-cabin upsell preserves fares while expanding share

Leisure carrier facing buyer power; OTAs ≈50% bookings, yields squeezed

JetBlue faces high customer bargaining power: leisure-skewed, price-elastic demand with OTAs/metasearch ≈50% of bookings (2023–24) and US CPI ~3.4% in 2024 tightening budgets. Ancillary revenue >10% of US airline revenue (2024) and visible fares compress yields; loyalty programs and Mint/Even More Space raise switching costs modestly. Corporate accounts (~10–20% share) extract discounts and SLAs, influencing renewals.

| Metric | Value |

|---|---|

| OTAs/metasearch share | ≈50% (2023–24) |

| US CPI | ≈3.4% (2024, BLS) |

| Ancillary revenue | >10% (2024, US airlines) |

| Corporate revenue share | ≈10–20% |

Full Version Awaits

JetBlue Porter's Five Forces Analysis

This JetBlue Porter’s Five Forces Analysis preview is the exact, fully formatted document you’ll receive immediately after purchase. It contains the complete competitive assessment—threat of entrants, buyer and supplier power, substitutes, and rivalry—ready for download and use. No placeholders, samples, or edits required.

Description

From Overview to Strategy Blueprint

JetBlue faces intense rivalry from legacy carriers and low-cost rivals, moderate supplier power driven by aircraft and fuel costs, and evolving buyer leverage as customers demand low fares and loyalty perks. Regulatory and network barriers temper new entrants while substitutes like high-speed rail remain limited in the U.S. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore JetBlue’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated aircraft OEMs

JetBlue depends on a duopoly—Airbus and Boeing, which together supply roughly 98% of large commercial jets—giving suppliers strong leverage over pricing, delivery slots, and cabin configuration for JetBlue’s ~270-aircraft system (2024). Limited OEM alternatives constrain negotiation power and fleet flexibility, so production delays or quality issues ripple into capacity and unit-cost plans. Long lead times of 3–5+ years lock in capital commitments.

Engine and MRO dependence

Engine OEMs GE, Pratt & Whitney and Rolls‑Royce hold proprietary IP and parts control over most commercial engines, giving them aftermarket pricing power and influence over turnaround times; the global commercial MRO market was about $90 billion in 2023. Technical failures can ground aircraft and spike maintenance costs, and while contracts and warranties mitigate risk, they rarely eliminate OEM/MRO leverage; certified shop scarcity raises switching costs.

Jet fuel volatility and suppliers

Jet fuel is a volatile commodity and accounted for roughly 20–25% of airline operating costs in 2024, limiting JetBlue’s ability to pass sudden spikes to passengers without hurting demand. Supply is fragmented but airport-specific infrastructure bottlenecks can push local jet-fuel margins higher. Financial hedges only partially mitigate price exposure, and 2024-era environmental policies plus SAF priced roughly 3–5x Jet A are shifting long-term cost curves.

Airport access, slots, and gate control

Airport authorities and slot coordinators at congested hubs like LaGuardia and Reagan National (both FAA slot-controlled in 2024) hold scarce takeoff and landing rights, giving them leverage over carriers such as JetBlue; fees, gate availability, and curfew rules raise operating costs and constrain scheduling. Access limits can cap growth and force capacity tradeoffs, so airlines often exchange long-term commercial commitments for guaranteed slots and gates.

- FAA slot control: LaGuardia, Reagan National (2024)

- Negotiation lever: fees, gate leases, curfews

- Outcome: long-term commitments for capacity rights

Unionized labor and skilled crews

Airlines squeezed by supplier power: OEM duopoly, engine MRO control, fuel volatility, unions

JetBlue faces high supplier bargaining power: Airbus/Boeing duopoly (~98% large jets), engine OEMs with aftermarket control, volatile jet fuel (20–25% of ops in 2024) and strong unionized labor—each constrains pricing, delivery flexibility and capacity decisions.

| Supplier | Metric | 2024 |

|---|---|---|

| Airframe OEMs | Market share | ~98% |

| Engines/MRO | Global MRO | $90B |

| Fuel | Cost share | 20–25% |

| Labor | Pressure | High |

What is included in the product

Concise Porter's Five Forces analysis of JetBlue assessing competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and regulatory dynamics to highlight pressure points, strategic advantages, and emerging disruptions to its profitability.

A clear one-sheet Porter's Five Forces for JetBlue—perfect for quick strategic decisions and investor meetings. Swap in route-specific data, adjust force intensity for market shifts, and export charts into decks without macros.

Customers Bargaining Power

High price sensitivity

JetBlue’s customer mix skews toward leisure travelers who are highly price elastic, so even small fare differences drive switching to rivals. Promotional fares and ancillary bundles (seat, bags, Wi‑Fi) are pivotal to capture demand. Macroeconomic shifts rapidly alter willingness to pay — US CPI averaged about 3.4% in 2024 (BLS), pressuring discretionary travel budgets and price sensitivity.

Low switching costs

Low switching costs let travelers compare fares instantly via OTAs and metasearch, with these channels accounting for ≈50% of online flight bookings in recent industry reports (2023–24), eroding loyalty. Route-by-route alternatives intensify choice, while cancellation policies and credits influence decisions but seldom lock customers. Convenience and schedule frequently trump brand in purchase decisions.

Transparency via digital channels

Real-time fare visibility via OTAs and metasearch forces JetBlue to protect yields, compressing margins on competitive routes as fares fluctuate; dynamic pricing must balance higher load factors with reputation risk from sharp fare swings. Reviews and social media amplify service lapses—over 70% of travelers say online feedback influences choices. Ancillary clarity matters: ancillary revenue was over 10% of US airline revenue in 2024.

Loyalty and product differentiation

TrueBlue loyalty, seat comfort and in‑flight experience reduce buyer power by raising perceived value; JetBlue’s premium‑economy style products create micro‑segments but must justify typical fare deltas of about 20–40% to hold customers, and co‑brand cards add modest switching costs via bonus points and status perks.

- TrueBlue loyalty: customer retention

- Seat comfort/in‑flight: perceived value

- Premium economy: micro‑segmentation, 20–40% fare delta

- Co‑brand cards: modest switching costs

Corporate and group contracts

While JetBlue remains leisure-skewed, corporate and group contracts secure discounted fares and inventory access; concentrated accounts can command fare concessions and service guarantees, affecting yield management and distribution.

Renewals hinge on performance clauses and disruption handling; mixed-cabin (Mint/Even More Space) strategies can grow share without full price erosion.

- Corporate share: ~10–20% of airline revenue pools (industry range)

- Concentrated accounts leverage bulk discounts and service SLAs

- Performance clauses, disruption payouts key in renewals

- Mixed-cabin upsell preserves fares while expanding share

Leisure carrier facing buyer power; OTAs ≈50% bookings, yields squeezed

JetBlue faces high customer bargaining power: leisure-skewed, price-elastic demand with OTAs/metasearch ≈50% of bookings (2023–24) and US CPI ~3.4% in 2024 tightening budgets. Ancillary revenue >10% of US airline revenue (2024) and visible fares compress yields; loyalty programs and Mint/Even More Space raise switching costs modestly. Corporate accounts (~10–20% share) extract discounts and SLAs, influencing renewals.

| Metric | Value |

|---|---|

| OTAs/metasearch share | ≈50% (2023–24) |

| US CPI | ≈3.4% (2024, BLS) |

| Ancillary revenue | >10% (2024, US airlines) |

| Corporate revenue share | ≈10–20% |

Full Version Awaits

JetBlue Porter's Five Forces Analysis

This JetBlue Porter’s Five Forces Analysis preview is the exact, fully formatted document you’ll receive immediately after purchase. It contains the complete competitive assessment—threat of entrants, buyer and supplier power, substitutes, and rivalry—ready for download and use. No placeholders, samples, or edits required.