Jindal Steel & Power Boston Consulting Group Matrix

Actionable Strategy Starts Here

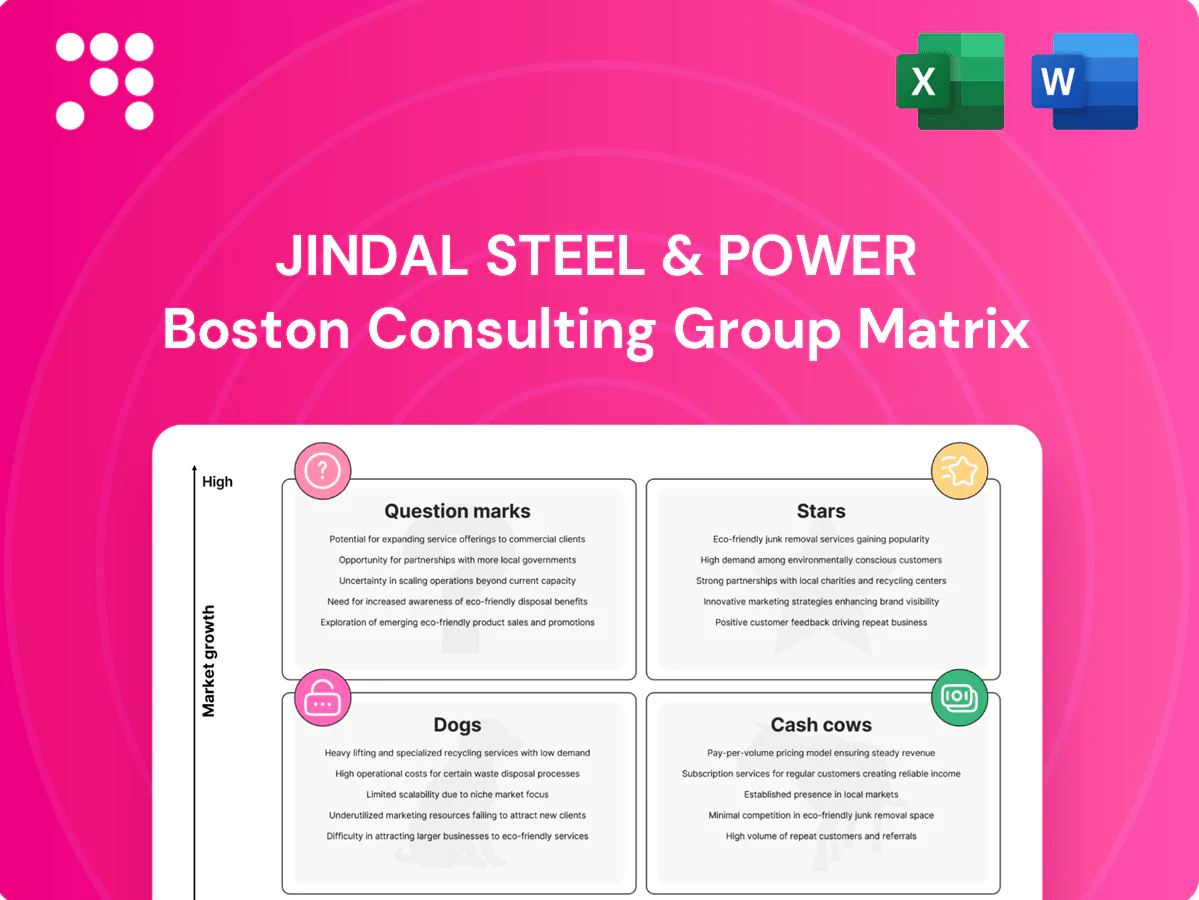

Quick snapshot: the Jindal Steel & Power BCG Matrix teases which business lines are scaling fast, which fund the engine, and which might be costing you growth—vital when steel markets pivot. This preview shows placement trends and competitive signals, but the full report gives quadrant-by-quadrant clarity, data-driven moves, and tactical next steps. Buy the complete BCG Matrix for a ready-to-use Word report plus an Excel summary you can present and act on immediately.

Stars

Indian rails leadership

High market share in a fast-growing rail capex cycle makes JSPL rails a classic Star, supported by Indian Railways capex of about Rs 2.4 lakh crore in FY24 and rising metro investments. JSPL is a key approved supplier to Indian Railways and multiple metro projects, with growing export traction to Southeast Asia and Africa. Growth eats cash—capacity expansion, quality upgrades and approvals require capital—but defending share will compound returns; keep investing until growth normalizes.

TMT rebars for infra boom

Nationwide housing, highways and urban buildouts—backed by the ₹111 lakh crore National Infrastructure Pipeline—keep long products like TMT rebars in sustained demand, positioning JSPL as a Star in BCG terms. JSPL’s distribution muscle and brand recall have captured incremental share in 2024’s hot market, though working capital and channel incentives remain sizable. Preserve price discipline while expanding reach in Tier-2/3 to protect margins.

Railway turnouts & head-hardened rails

Premium head-hardened rails and specialized turnouts are capturing the same 2024 growth wave with higher specs and margins, driven by heavier axle-load and speed upgrade programs across key markets. Early-mover technical approvals and OEM certifications have created a durable moat for Jindal Steel & Power, locking preferred-supplier status. Accelerating demand for higher axle loads and faster services makes doubling down on certifications and expanded after-sales support essential to convert orders into recurring revenue.

Value-added structurals

Value-added structurals are a Star for JSPL as large industrial and warehousing structural demand scales with India’s capex push (Union Budget 2024–25 capex allocation ₹11.1 lakh crore); JSPL’s engineering depth and project credentials win complex orders, but the segment remains growth-heavy and capex-hungry, requiring sustained investment and execution focus.

- High demand: India capex ₹11.1 lakh crore (2024–25)

- Competitive edge: engineering depth for complex orders

- Capital intensity: ongoing heavy capex requirement

- Strategy: deepen project partnerships with EPCs

Iron ore pellets (premium mix)

Iron ore pellets (premium mix) sit as a Star for JSPL: rising pellet demand driven by stricter BF/DRI efficiency standards and India’s position as the world’s second-largest steel producer make growth real.

JSPL’s integrated mining-to-pellet chain provides clear cost and quality leverage, but meeting large orders needs targeted logistics upgrades and plant debottlenecking capex.

Invest to sustain market share as the pellet segment expands regionally and demand shifts toward higher-grade, low-impurity feeds.

- Demand driver: BF/DRI efficiency standards

- Advantage: integrated mining-pellet value chain

- Requirement: logistics + debottlenecking spend

- Action: invest to defend/grow share

High rail capex crowns rails; exports, premium head-hardened rails lift margins

High share in fast-growing rail capex (Indian Railways capex ~Rs 2.4 lakh crore in FY24) makes JSPL rails a Star; exports to SE Asia/Africa and premium head-hardened rails boost margins. Long products (TMT) benefit from NIP ₹111 lakh crore and Budget capex ₹11.1 lakh crore (2024–25) — distribution gains but channel working capital is high. Pellets are a Star via integrated mining-to-pellet chain; logistics and debottlenecking capex required.

| Segment | 2024 Driver | JSPL edge | Capex need |

|---|---|---|---|

| Rails | Rail capex Rs 2.4L cr | Approved supplier, exports | Quality & approvals |

| TMT | NIP ₹111L cr | Distribution, brand | Working capital |

| Pellets | BF/DRI efficiency | Integrated chain | Logistics/debottleneck |

What is included in the product

BCG analysis of Jindal Steel & Power: Stars, Cash Cows, Question Marks, Dogs with investment, divestment guidance and trend context.

One-page BCG matrix mapping Jindal Steel & Power units to ease portfolio decisions and spotlight growth vs divestment needs.

Cash Cows

Captive iron ore mining

Captive iron-ore mining supplies over 70% of Jindal Steel & Power’s ore needs (FY2024), giving high internal consumption, stable volumes and predictable cash generation. Mature regulatory frameworks and established pits keep unit mining costs low, supporting healthy operating margins. The operations free cash funds growth elsewhere in the group; management prioritizes efficiency gains, lower stripping ratios and mine-life extensions rather than large discretionary capex.

Thermal power (captive)

Thermal power (captive) is locked to Jindal Steel & Power operations, delivering steady offtake and reliability premiums that supported the steel margin profile in 2024. Growth is modest but margins remain solid when fuel is vertically integrated, with the captive model reducing procurement volatility. Low promotional needs mean incremental cash comes from optimization and PLF gains. Maintaining availability and heat-rate discipline is key to sustaining cash generation.

Mature structural steel SKUs

Mature commodity-grade beams and channels deliver steady volume for Jindal Steel & Power, with market growth moderate at about 3% in 2024 and disciplined pricing supporting margins. Strong share in core regions (estimated 25–30%) makes these SKUs reliable cash generators with limited marketing spend. Focus remains on squeezing costs, improving yields and keeping plants at high utilisation to sustain free cash flow.

Domestic flat products (core grades)

Domestic flat products (core grades) — baseline coils and plates for general fabrication — deliver steady cash flows for JSPL, not high growth. JSPL’s integrated cost base, backed by captive raw materials and power, supports resilient spreads even in weak cycles. With low market growth, the focus is monetizing scale through mix optimization and securing long-term contracts to smooth volatility.

- mix optimization

- long-term contracts

- monetize scale

- stable margins from integration

Coal linkages for captive use

Secured coal linkages for captive use underpin JSPLs power and DRI feed, cutting input volatility and stabilizing costs; in 2024 captive coal flows (~2.5 mtpa) helped sustain reliable power for steel and power plants and improved cash conversion. This enabler delivers steady cash returns with limited growth potential but high utility; keep compliance and logistics tight and avoid capacity expansion solely to absorb extra coal.

- Low growth, high margin

- Stabilizes input costs ~reduces fuel volatility

- Enables steady cash generation

- Focus: compliance, logistics, no needless expansion

Captive ore >70% and secured coal (~2.5 mtpa) lock in low-cost, steady cash flow

Captive iron-ore supplies >70% of JSPL’s ore (FY2024), ensuring stable volumes and low unit cost. Captive thermal and secured coal (~2.5 mtpa) stabilize power/DRI inputs, preserving margins. Core beams/flat products (domestic growth ~3% in 2024) deliver steady cash with ~25–30% regional share. Focus remains on utilization, yield improvement and long-term contracts to sustain cash flow.

| Metric | 2024 |

|---|---|

| Captive ore supply | >70% |

| Captive coal | ~2.5 mtpa |

| Domestic product growth | ~3% |

| Regional share (beams) | 25–30% |

Delivered as Shown

Jindal Steel & Power BCG Matrix

The file you’re previewing is the exact Jindal Steel & Power BCG Matrix report you’ll receive after purchase. No watermarks, no placeholders—just the fully formatted, analysis-ready document. It’s built for clarity and strategic use, so you can edit, print, or present right away. Purchase unlocks the full file instantly and it will be delivered to your inbox—no surprises, no revisions needed.

Actionable Strategy Starts Here

Quick snapshot: the Jindal Steel & Power BCG Matrix teases which business lines are scaling fast, which fund the engine, and which might be costing you growth—vital when steel markets pivot. This preview shows placement trends and competitive signals, but the full report gives quadrant-by-quadrant clarity, data-driven moves, and tactical next steps. Buy the complete BCG Matrix for a ready-to-use Word report plus an Excel summary you can present and act on immediately.

Stars

Indian rails leadership

High market share in a fast-growing rail capex cycle makes JSPL rails a classic Star, supported by Indian Railways capex of about Rs 2.4 lakh crore in FY24 and rising metro investments. JSPL is a key approved supplier to Indian Railways and multiple metro projects, with growing export traction to Southeast Asia and Africa. Growth eats cash—capacity expansion, quality upgrades and approvals require capital—but defending share will compound returns; keep investing until growth normalizes.

TMT rebars for infra boom

Nationwide housing, highways and urban buildouts—backed by the ₹111 lakh crore National Infrastructure Pipeline—keep long products like TMT rebars in sustained demand, positioning JSPL as a Star in BCG terms. JSPL’s distribution muscle and brand recall have captured incremental share in 2024’s hot market, though working capital and channel incentives remain sizable. Preserve price discipline while expanding reach in Tier-2/3 to protect margins.

Railway turnouts & head-hardened rails

Premium head-hardened rails and specialized turnouts are capturing the same 2024 growth wave with higher specs and margins, driven by heavier axle-load and speed upgrade programs across key markets. Early-mover technical approvals and OEM certifications have created a durable moat for Jindal Steel & Power, locking preferred-supplier status. Accelerating demand for higher axle loads and faster services makes doubling down on certifications and expanded after-sales support essential to convert orders into recurring revenue.

Value-added structurals

Value-added structurals are a Star for JSPL as large industrial and warehousing structural demand scales with India’s capex push (Union Budget 2024–25 capex allocation ₹11.1 lakh crore); JSPL’s engineering depth and project credentials win complex orders, but the segment remains growth-heavy and capex-hungry, requiring sustained investment and execution focus.

- High demand: India capex ₹11.1 lakh crore (2024–25)

- Competitive edge: engineering depth for complex orders

- Capital intensity: ongoing heavy capex requirement

- Strategy: deepen project partnerships with EPCs

Iron ore pellets (premium mix)

Iron ore pellets (premium mix) sit as a Star for JSPL: rising pellet demand driven by stricter BF/DRI efficiency standards and India’s position as the world’s second-largest steel producer make growth real.

JSPL’s integrated mining-to-pellet chain provides clear cost and quality leverage, but meeting large orders needs targeted logistics upgrades and plant debottlenecking capex.

Invest to sustain market share as the pellet segment expands regionally and demand shifts toward higher-grade, low-impurity feeds.

- Demand driver: BF/DRI efficiency standards

- Advantage: integrated mining-pellet value chain

- Requirement: logistics + debottlenecking spend

- Action: invest to defend/grow share

High rail capex crowns rails; exports, premium head-hardened rails lift margins

High share in fast-growing rail capex (Indian Railways capex ~Rs 2.4 lakh crore in FY24) makes JSPL rails a Star; exports to SE Asia/Africa and premium head-hardened rails boost margins. Long products (TMT) benefit from NIP ₹111 lakh crore and Budget capex ₹11.1 lakh crore (2024–25) — distribution gains but channel working capital is high. Pellets are a Star via integrated mining-to-pellet chain; logistics and debottlenecking capex required.

| Segment | 2024 Driver | JSPL edge | Capex need |

|---|---|---|---|

| Rails | Rail capex Rs 2.4L cr | Approved supplier, exports | Quality & approvals |

| TMT | NIP ₹111L cr | Distribution, brand | Working capital |

| Pellets | BF/DRI efficiency | Integrated chain | Logistics/debottleneck |

What is included in the product

BCG analysis of Jindal Steel & Power: Stars, Cash Cows, Question Marks, Dogs with investment, divestment guidance and trend context.

One-page BCG matrix mapping Jindal Steel & Power units to ease portfolio decisions and spotlight growth vs divestment needs.

Cash Cows

Captive iron ore mining

Captive iron-ore mining supplies over 70% of Jindal Steel & Power’s ore needs (FY2024), giving high internal consumption, stable volumes and predictable cash generation. Mature regulatory frameworks and established pits keep unit mining costs low, supporting healthy operating margins. The operations free cash funds growth elsewhere in the group; management prioritizes efficiency gains, lower stripping ratios and mine-life extensions rather than large discretionary capex.

Thermal power (captive)

Thermal power (captive) is locked to Jindal Steel & Power operations, delivering steady offtake and reliability premiums that supported the steel margin profile in 2024. Growth is modest but margins remain solid when fuel is vertically integrated, with the captive model reducing procurement volatility. Low promotional needs mean incremental cash comes from optimization and PLF gains. Maintaining availability and heat-rate discipline is key to sustaining cash generation.

Mature structural steel SKUs

Mature commodity-grade beams and channels deliver steady volume for Jindal Steel & Power, with market growth moderate at about 3% in 2024 and disciplined pricing supporting margins. Strong share in core regions (estimated 25–30%) makes these SKUs reliable cash generators with limited marketing spend. Focus remains on squeezing costs, improving yields and keeping plants at high utilisation to sustain free cash flow.

Domestic flat products (core grades)

Domestic flat products (core grades) — baseline coils and plates for general fabrication — deliver steady cash flows for JSPL, not high growth. JSPL’s integrated cost base, backed by captive raw materials and power, supports resilient spreads even in weak cycles. With low market growth, the focus is monetizing scale through mix optimization and securing long-term contracts to smooth volatility.

- mix optimization

- long-term contracts

- monetize scale

- stable margins from integration

Coal linkages for captive use

Secured coal linkages for captive use underpin JSPLs power and DRI feed, cutting input volatility and stabilizing costs; in 2024 captive coal flows (~2.5 mtpa) helped sustain reliable power for steel and power plants and improved cash conversion. This enabler delivers steady cash returns with limited growth potential but high utility; keep compliance and logistics tight and avoid capacity expansion solely to absorb extra coal.

- Low growth, high margin

- Stabilizes input costs ~reduces fuel volatility

- Enables steady cash generation

- Focus: compliance, logistics, no needless expansion

Captive ore >70% and secured coal (~2.5 mtpa) lock in low-cost, steady cash flow

Captive iron-ore supplies >70% of JSPL’s ore (FY2024), ensuring stable volumes and low unit cost. Captive thermal and secured coal (~2.5 mtpa) stabilize power/DRI inputs, preserving margins. Core beams/flat products (domestic growth ~3% in 2024) deliver steady cash with ~25–30% regional share. Focus remains on utilization, yield improvement and long-term contracts to sustain cash flow.

| Metric | 2024 |

|---|---|

| Captive ore supply | >70% |

| Captive coal | ~2.5 mtpa |

| Domestic product growth | ~3% |

| Regional share (beams) | 25–30% |

Delivered as Shown

Jindal Steel & Power BCG Matrix

The file you’re previewing is the exact Jindal Steel & Power BCG Matrix report you’ll receive after purchase. No watermarks, no placeholders—just the fully formatted, analysis-ready document. It’s built for clarity and strategic use, so you can edit, print, or present right away. Purchase unlocks the full file instantly and it will be delivered to your inbox—no surprises, no revisions needed.

Original: $10.00

-65%$10.00

$3.50Description

Actionable Strategy Starts Here

Quick snapshot: the Jindal Steel & Power BCG Matrix teases which business lines are scaling fast, which fund the engine, and which might be costing you growth—vital when steel markets pivot. This preview shows placement trends and competitive signals, but the full report gives quadrant-by-quadrant clarity, data-driven moves, and tactical next steps. Buy the complete BCG Matrix for a ready-to-use Word report plus an Excel summary you can present and act on immediately.

Stars

Indian rails leadership

High market share in a fast-growing rail capex cycle makes JSPL rails a classic Star, supported by Indian Railways capex of about Rs 2.4 lakh crore in FY24 and rising metro investments. JSPL is a key approved supplier to Indian Railways and multiple metro projects, with growing export traction to Southeast Asia and Africa. Growth eats cash—capacity expansion, quality upgrades and approvals require capital—but defending share will compound returns; keep investing until growth normalizes.

TMT rebars for infra boom

Nationwide housing, highways and urban buildouts—backed by the ₹111 lakh crore National Infrastructure Pipeline—keep long products like TMT rebars in sustained demand, positioning JSPL as a Star in BCG terms. JSPL’s distribution muscle and brand recall have captured incremental share in 2024’s hot market, though working capital and channel incentives remain sizable. Preserve price discipline while expanding reach in Tier-2/3 to protect margins.

Railway turnouts & head-hardened rails

Premium head-hardened rails and specialized turnouts are capturing the same 2024 growth wave with higher specs and margins, driven by heavier axle-load and speed upgrade programs across key markets. Early-mover technical approvals and OEM certifications have created a durable moat for Jindal Steel & Power, locking preferred-supplier status. Accelerating demand for higher axle loads and faster services makes doubling down on certifications and expanded after-sales support essential to convert orders into recurring revenue.

Value-added structurals

Value-added structurals are a Star for JSPL as large industrial and warehousing structural demand scales with India’s capex push (Union Budget 2024–25 capex allocation ₹11.1 lakh crore); JSPL’s engineering depth and project credentials win complex orders, but the segment remains growth-heavy and capex-hungry, requiring sustained investment and execution focus.

- High demand: India capex ₹11.1 lakh crore (2024–25)

- Competitive edge: engineering depth for complex orders

- Capital intensity: ongoing heavy capex requirement

- Strategy: deepen project partnerships with EPCs

Iron ore pellets (premium mix)

Iron ore pellets (premium mix) sit as a Star for JSPL: rising pellet demand driven by stricter BF/DRI efficiency standards and India’s position as the world’s second-largest steel producer make growth real.

JSPL’s integrated mining-to-pellet chain provides clear cost and quality leverage, but meeting large orders needs targeted logistics upgrades and plant debottlenecking capex.

Invest to sustain market share as the pellet segment expands regionally and demand shifts toward higher-grade, low-impurity feeds.

- Demand driver: BF/DRI efficiency standards

- Advantage: integrated mining-pellet value chain

- Requirement: logistics + debottlenecking spend

- Action: invest to defend/grow share

High rail capex crowns rails; exports, premium head-hardened rails lift margins

High share in fast-growing rail capex (Indian Railways capex ~Rs 2.4 lakh crore in FY24) makes JSPL rails a Star; exports to SE Asia/Africa and premium head-hardened rails boost margins. Long products (TMT) benefit from NIP ₹111 lakh crore and Budget capex ₹11.1 lakh crore (2024–25) — distribution gains but channel working capital is high. Pellets are a Star via integrated mining-to-pellet chain; logistics and debottlenecking capex required.

| Segment | 2024 Driver | JSPL edge | Capex need |

|---|---|---|---|

| Rails | Rail capex Rs 2.4L cr | Approved supplier, exports | Quality & approvals |

| TMT | NIP ₹111L cr | Distribution, brand | Working capital |

| Pellets | BF/DRI efficiency | Integrated chain | Logistics/debottleneck |

What is included in the product

BCG analysis of Jindal Steel & Power: Stars, Cash Cows, Question Marks, Dogs with investment, divestment guidance and trend context.

One-page BCG matrix mapping Jindal Steel & Power units to ease portfolio decisions and spotlight growth vs divestment needs.

Cash Cows

Captive iron ore mining

Captive iron-ore mining supplies over 70% of Jindal Steel & Power’s ore needs (FY2024), giving high internal consumption, stable volumes and predictable cash generation. Mature regulatory frameworks and established pits keep unit mining costs low, supporting healthy operating margins. The operations free cash funds growth elsewhere in the group; management prioritizes efficiency gains, lower stripping ratios and mine-life extensions rather than large discretionary capex.

Thermal power (captive)

Thermal power (captive) is locked to Jindal Steel & Power operations, delivering steady offtake and reliability premiums that supported the steel margin profile in 2024. Growth is modest but margins remain solid when fuel is vertically integrated, with the captive model reducing procurement volatility. Low promotional needs mean incremental cash comes from optimization and PLF gains. Maintaining availability and heat-rate discipline is key to sustaining cash generation.

Mature structural steel SKUs

Mature commodity-grade beams and channels deliver steady volume for Jindal Steel & Power, with market growth moderate at about 3% in 2024 and disciplined pricing supporting margins. Strong share in core regions (estimated 25–30%) makes these SKUs reliable cash generators with limited marketing spend. Focus remains on squeezing costs, improving yields and keeping plants at high utilisation to sustain free cash flow.

Domestic flat products (core grades)

Domestic flat products (core grades) — baseline coils and plates for general fabrication — deliver steady cash flows for JSPL, not high growth. JSPL’s integrated cost base, backed by captive raw materials and power, supports resilient spreads even in weak cycles. With low market growth, the focus is monetizing scale through mix optimization and securing long-term contracts to smooth volatility.

- mix optimization

- long-term contracts

- monetize scale

- stable margins from integration

Coal linkages for captive use

Secured coal linkages for captive use underpin JSPLs power and DRI feed, cutting input volatility and stabilizing costs; in 2024 captive coal flows (~2.5 mtpa) helped sustain reliable power for steel and power plants and improved cash conversion. This enabler delivers steady cash returns with limited growth potential but high utility; keep compliance and logistics tight and avoid capacity expansion solely to absorb extra coal.

- Low growth, high margin

- Stabilizes input costs ~reduces fuel volatility

- Enables steady cash generation

- Focus: compliance, logistics, no needless expansion

Captive ore >70% and secured coal (~2.5 mtpa) lock in low-cost, steady cash flow

Captive iron-ore supplies >70% of JSPL’s ore (FY2024), ensuring stable volumes and low unit cost. Captive thermal and secured coal (~2.5 mtpa) stabilize power/DRI inputs, preserving margins. Core beams/flat products (domestic growth ~3% in 2024) deliver steady cash with ~25–30% regional share. Focus remains on utilization, yield improvement and long-term contracts to sustain cash flow.

| Metric | 2024 |

|---|---|

| Captive ore supply | >70% |

| Captive coal | ~2.5 mtpa |

| Domestic product growth | ~3% |

| Regional share (beams) | 25–30% |

Delivered as Shown

Jindal Steel & Power BCG Matrix

The file you’re previewing is the exact Jindal Steel & Power BCG Matrix report you’ll receive after purchase. No watermarks, no placeholders—just the fully formatted, analysis-ready document. It’s built for clarity and strategic use, so you can edit, print, or present right away. Purchase unlocks the full file instantly and it will be delivered to your inbox—no surprises, no revisions needed.