Jindal Steel & Power Porter's Five Forces Analysis

From Overview to Strategy Blueprint

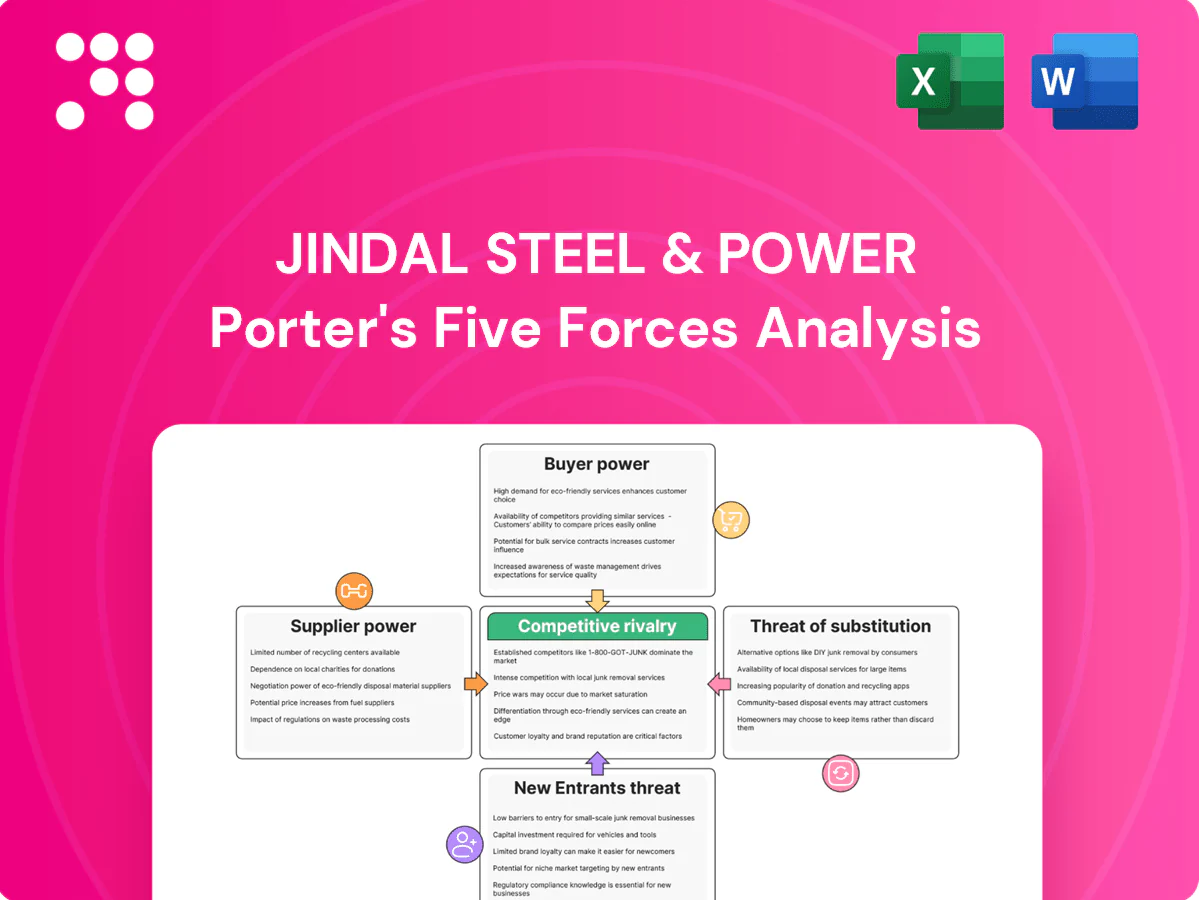

Jindal Steel & Power faces moderate supplier power due to raw-material integration, while high capital intensity and scale advantages keep the threat of new entrants low; buyer power is mixed as large infrastructure clients pressure margins but rising domestic demand cushions volume risk. Competitive rivalry is intense in commodities, yet product diversification lowers substitute threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Jindal Steel & Power’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Backward integration dampens leverage

JSPL’s captive iron‑ore and thermal‑coal assets materially cut reliance on external miners, weakening supplier pricing power for core inputs; FY2024 disclosures highlight internal sourcing as a strategic buffer. Gaps persist for premium coking coal and specialty alloys, where global suppliers retain leverage. Suppliers therefore keep influence in areas where JSPL lacks full self‑sufficiency.

Concentrated sources for coking coal

Hard coking coal exports remain concentrated—Australia supplied about 60% of seaborne hard coking coal in 2024—raising switching costs and exposure to geopolitical and freight shocks; past 2021–22 price spikes showed suppliers can exert strong upward pressure in tight cycles. JSPL mitigates by long‑term contracts covering a majority of imports and coal‑blending to reduce feedstock cost volatility.

Energy and logistics as critical inputs

Power, fuel, rail rakes and port slots act as supplier-like constraints for JSPL, with congestion or policy shifts able to lift input costs and delay shipments; thermal coal imports and logistics slowdowns raised landed coal costs by double-digit percentages in 2023–24. JSPL’s captive power (~1,500 MW in 2024) and multi-modal logistics reduce dependence, yet peak-season bottlenecks still boost supplier leverage and transient cost spikes.

Specialty inputs and technology

Specialty inputs and automation systems for Jindal Steel & Power are supplied by a small set of certified vendors for alloying elements, refractories, electrodes and control systems, limiting substitution and raising supplier bargaining power; quality and certification requirements reinforce this niche leverage, while volume commitments and vendor development programs are used to mitigate risk.

- Concentration: few certified suppliers

- Constraints: strict QA/certification

- Leverage: niche supplier pricing power

- Mitigation: volume contracts & vendor development

Currency and freight pass-through

Imported coking coal and metallurgical inputs embed FX and ocean freight volatility; India imports around 80% of coking coal, so JSPL faces material exposure. Suppliers frequently insist on currency and freight pass-through clauses, which in buoyant markets tend to stick and lift input costs; in weaker markets JSPL negotiates rollbacks or shifts suppliers.

- FX exposure: imported c.80% of coking coal

- Supplier leverage: common pass-through clauses

- Market effect: pass-throughs raise costs when demand strong

- Mitigation: contract renegotiation, supplier diversification

Captive power ~1,500 MW cuts supplier power; coking coal imports ~80%

JSPL’s captive assets reduce supplier power for ore and thermal coal, but gaps in premium coking coal and specialty alloys sustain vendor leverage. Seaborne hard coking coal is concentrated—Australia ~60% share in 2024—while India imports ~80% of coking coal, raising switching costs and FX/freight exposure. Captive power (~1,500 MW in 2024) and long‑term contracts partially mitigate but do not eliminate supplier influence.

| Metric | 2024 figure |

|---|---|

| Captive power | ~1,500 MW |

| India coking coal imports | ~80% |

| Australia share seaborne HCC | ~60% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging threats specific to Jindal Steel & Power, with strategic commentary on pricing, profitability, market share risks, and protective dynamics for incumbency.

A clear, one-sheet Porter's Five Forces for Jindal Steel & Power—distills industry pressures (raw materials costs, energy constraints, buyer/supplier power, entry threats, substitutes) into a decision-ready snapshot for fast strategic moves.

Customers Bargaining Power

Commodity pricing heightens sensitivity

Commodity pricing heightens sensitivity as steel buyers, facing commoditized grades, react to even 1–2% price deltas that can reallocate volumes in spot markets. This dynamic raises buyer bargaining power in downcycles when margins compress and purchase switching increases. JSPL mitigates pressure through higher-margin value-added products and by emphasizing service reliability and delivery performance to retain contracts.

Large institutional buyers wield clout

Infrastructure EPCs, OEMs and Indian Railways place large, repeat orders, enabling tougher negotiations on price and payment terms; Indian Railways' capital outlay for 2024–25 was announced at 2.40 trillion rupees, underscoring procurement scale. Qualification norms and long-term supply contracts make winning and retaining them crucial, and JSPL’s rails and long-products portfolio is explicitly targeted at these high-volume accounts.

Switching costs vary by application

Standard longs and flats carry low switching costs, so buyers can shop suppliers easily, keeping buyer power high; by contrast certified rails, API-grade plates and high-spec coils require approvals that raise switching costs and weaken buyer leverage. In 2024 JSPL emphasized certifications, investing in API, EN and rail approvals to lock customers, with value-added certified products representing about 20% of steel sales that year.

Demand cyclicality shifts leverage

In downturns excess supply strengthens buyers and compresses spreads, while India produced about 125 MT of crude steel in FY2023-24, increasing buyer options; during capex upcycles and the government’s INR 10 lakh crore 2024–25 capex push leverage shifts back to mills. Contracting mix (spot vs contract) moderates power swings, and JSPL uses hedged contracts to stabilize realizations.

Service, delivery, and financing terms

Just-in-time delivery, flexible credit terms and robust after-sales support significantly shape buyer choices; JSPL’s emphasis on logistics and working-capital solutions reduces price as the primary lever. Superior distribution and financing tie-ups narrow effective buyer power by improving order reliability and cash-flow for customers. As of 2024 JSPL operates expanded steel capacity and strengthened sales logistics to support these services.

- Jindal advantage: logistics + financing = reduced buyer price leverage

Buyers dominate commoditized steel; mills push certified grades, logistics and hedges

Buyers wield high power on commoditized longs/flats, shifting volumes on 1–2% price moves; certified products (≈20% of JSPL 2024 steel sales) reduce switching. India crude steel ~125 MT in FY2023-24, excess supply strengthens buyers in downturns while INR 10 lakh crore 2024–25 capex shifts leverage to mills. JSPL counters with value-added grades, logistics, financing and hedged contracts to stabilize realizations.

| Metric | Value |

|---|---|

| India crude steel FY2023-24 | ~125 MT |

| 2024–25 Govt capex | INR 10 lakh crore |

| JSPL certified/value-added share 2024 | ~20% |

Full Version Awaits

Jindal Steel & Power Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Jindal Steel & Power Porter's Five Forces analysis evaluates supplier and buyer power, threat of new entrants and substitutes, and intensity of competitive rivalry specific to steel, power and mining segments. It highlights strategic implications and actionable risks and opportunities.

From Overview to Strategy Blueprint

Jindal Steel & Power faces moderate supplier power due to raw-material integration, while high capital intensity and scale advantages keep the threat of new entrants low; buyer power is mixed as large infrastructure clients pressure margins but rising domestic demand cushions volume risk. Competitive rivalry is intense in commodities, yet product diversification lowers substitute threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Jindal Steel & Power’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Backward integration dampens leverage

JSPL’s captive iron‑ore and thermal‑coal assets materially cut reliance on external miners, weakening supplier pricing power for core inputs; FY2024 disclosures highlight internal sourcing as a strategic buffer. Gaps persist for premium coking coal and specialty alloys, where global suppliers retain leverage. Suppliers therefore keep influence in areas where JSPL lacks full self‑sufficiency.

Concentrated sources for coking coal

Hard coking coal exports remain concentrated—Australia supplied about 60% of seaborne hard coking coal in 2024—raising switching costs and exposure to geopolitical and freight shocks; past 2021–22 price spikes showed suppliers can exert strong upward pressure in tight cycles. JSPL mitigates by long‑term contracts covering a majority of imports and coal‑blending to reduce feedstock cost volatility.

Energy and logistics as critical inputs

Power, fuel, rail rakes and port slots act as supplier-like constraints for JSPL, with congestion or policy shifts able to lift input costs and delay shipments; thermal coal imports and logistics slowdowns raised landed coal costs by double-digit percentages in 2023–24. JSPL’s captive power (~1,500 MW in 2024) and multi-modal logistics reduce dependence, yet peak-season bottlenecks still boost supplier leverage and transient cost spikes.

Specialty inputs and technology

Specialty inputs and automation systems for Jindal Steel & Power are supplied by a small set of certified vendors for alloying elements, refractories, electrodes and control systems, limiting substitution and raising supplier bargaining power; quality and certification requirements reinforce this niche leverage, while volume commitments and vendor development programs are used to mitigate risk.

- Concentration: few certified suppliers

- Constraints: strict QA/certification

- Leverage: niche supplier pricing power

- Mitigation: volume contracts & vendor development

Currency and freight pass-through

Imported coking coal and metallurgical inputs embed FX and ocean freight volatility; India imports around 80% of coking coal, so JSPL faces material exposure. Suppliers frequently insist on currency and freight pass-through clauses, which in buoyant markets tend to stick and lift input costs; in weaker markets JSPL negotiates rollbacks or shifts suppliers.

- FX exposure: imported c.80% of coking coal

- Supplier leverage: common pass-through clauses

- Market effect: pass-throughs raise costs when demand strong

- Mitigation: contract renegotiation, supplier diversification

Captive power ~1,500 MW cuts supplier power; coking coal imports ~80%

JSPL’s captive assets reduce supplier power for ore and thermal coal, but gaps in premium coking coal and specialty alloys sustain vendor leverage. Seaborne hard coking coal is concentrated—Australia ~60% share in 2024—while India imports ~80% of coking coal, raising switching costs and FX/freight exposure. Captive power (~1,500 MW in 2024) and long‑term contracts partially mitigate but do not eliminate supplier influence.

| Metric | 2024 figure |

|---|---|

| Captive power | ~1,500 MW |

| India coking coal imports | ~80% |

| Australia share seaborne HCC | ~60% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging threats specific to Jindal Steel & Power, with strategic commentary on pricing, profitability, market share risks, and protective dynamics for incumbency.

A clear, one-sheet Porter's Five Forces for Jindal Steel & Power—distills industry pressures (raw materials costs, energy constraints, buyer/supplier power, entry threats, substitutes) into a decision-ready snapshot for fast strategic moves.

Customers Bargaining Power

Commodity pricing heightens sensitivity

Commodity pricing heightens sensitivity as steel buyers, facing commoditized grades, react to even 1–2% price deltas that can reallocate volumes in spot markets. This dynamic raises buyer bargaining power in downcycles when margins compress and purchase switching increases. JSPL mitigates pressure through higher-margin value-added products and by emphasizing service reliability and delivery performance to retain contracts.

Large institutional buyers wield clout

Infrastructure EPCs, OEMs and Indian Railways place large, repeat orders, enabling tougher negotiations on price and payment terms; Indian Railways' capital outlay for 2024–25 was announced at 2.40 trillion rupees, underscoring procurement scale. Qualification norms and long-term supply contracts make winning and retaining them crucial, and JSPL’s rails and long-products portfolio is explicitly targeted at these high-volume accounts.

Switching costs vary by application

Standard longs and flats carry low switching costs, so buyers can shop suppliers easily, keeping buyer power high; by contrast certified rails, API-grade plates and high-spec coils require approvals that raise switching costs and weaken buyer leverage. In 2024 JSPL emphasized certifications, investing in API, EN and rail approvals to lock customers, with value-added certified products representing about 20% of steel sales that year.

Demand cyclicality shifts leverage

In downturns excess supply strengthens buyers and compresses spreads, while India produced about 125 MT of crude steel in FY2023-24, increasing buyer options; during capex upcycles and the government’s INR 10 lakh crore 2024–25 capex push leverage shifts back to mills. Contracting mix (spot vs contract) moderates power swings, and JSPL uses hedged contracts to stabilize realizations.

Service, delivery, and financing terms

Just-in-time delivery, flexible credit terms and robust after-sales support significantly shape buyer choices; JSPL’s emphasis on logistics and working-capital solutions reduces price as the primary lever. Superior distribution and financing tie-ups narrow effective buyer power by improving order reliability and cash-flow for customers. As of 2024 JSPL operates expanded steel capacity and strengthened sales logistics to support these services.

- Jindal advantage: logistics + financing = reduced buyer price leverage

Buyers dominate commoditized steel; mills push certified grades, logistics and hedges

Buyers wield high power on commoditized longs/flats, shifting volumes on 1–2% price moves; certified products (≈20% of JSPL 2024 steel sales) reduce switching. India crude steel ~125 MT in FY2023-24, excess supply strengthens buyers in downturns while INR 10 lakh crore 2024–25 capex shifts leverage to mills. JSPL counters with value-added grades, logistics, financing and hedged contracts to stabilize realizations.

| Metric | Value |

|---|---|

| India crude steel FY2023-24 | ~125 MT |

| 2024–25 Govt capex | INR 10 lakh crore |

| JSPL certified/value-added share 2024 | ~20% |

Full Version Awaits

Jindal Steel & Power Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Jindal Steel & Power Porter's Five Forces analysis evaluates supplier and buyer power, threat of new entrants and substitutes, and intensity of competitive rivalry specific to steel, power and mining segments. It highlights strategic implications and actionable risks and opportunities.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Jindal Steel & Power faces moderate supplier power due to raw-material integration, while high capital intensity and scale advantages keep the threat of new entrants low; buyer power is mixed as large infrastructure clients pressure margins but rising domestic demand cushions volume risk. Competitive rivalry is intense in commodities, yet product diversification lowers substitute threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Jindal Steel & Power’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Backward integration dampens leverage

JSPL’s captive iron‑ore and thermal‑coal assets materially cut reliance on external miners, weakening supplier pricing power for core inputs; FY2024 disclosures highlight internal sourcing as a strategic buffer. Gaps persist for premium coking coal and specialty alloys, where global suppliers retain leverage. Suppliers therefore keep influence in areas where JSPL lacks full self‑sufficiency.

Concentrated sources for coking coal

Hard coking coal exports remain concentrated—Australia supplied about 60% of seaborne hard coking coal in 2024—raising switching costs and exposure to geopolitical and freight shocks; past 2021–22 price spikes showed suppliers can exert strong upward pressure in tight cycles. JSPL mitigates by long‑term contracts covering a majority of imports and coal‑blending to reduce feedstock cost volatility.

Energy and logistics as critical inputs

Power, fuel, rail rakes and port slots act as supplier-like constraints for JSPL, with congestion or policy shifts able to lift input costs and delay shipments; thermal coal imports and logistics slowdowns raised landed coal costs by double-digit percentages in 2023–24. JSPL’s captive power (~1,500 MW in 2024) and multi-modal logistics reduce dependence, yet peak-season bottlenecks still boost supplier leverage and transient cost spikes.

Specialty inputs and technology

Specialty inputs and automation systems for Jindal Steel & Power are supplied by a small set of certified vendors for alloying elements, refractories, electrodes and control systems, limiting substitution and raising supplier bargaining power; quality and certification requirements reinforce this niche leverage, while volume commitments and vendor development programs are used to mitigate risk.

- Concentration: few certified suppliers

- Constraints: strict QA/certification

- Leverage: niche supplier pricing power

- Mitigation: volume contracts & vendor development

Currency and freight pass-through

Imported coking coal and metallurgical inputs embed FX and ocean freight volatility; India imports around 80% of coking coal, so JSPL faces material exposure. Suppliers frequently insist on currency and freight pass-through clauses, which in buoyant markets tend to stick and lift input costs; in weaker markets JSPL negotiates rollbacks or shifts suppliers.

- FX exposure: imported c.80% of coking coal

- Supplier leverage: common pass-through clauses

- Market effect: pass-throughs raise costs when demand strong

- Mitigation: contract renegotiation, supplier diversification

Captive power ~1,500 MW cuts supplier power; coking coal imports ~80%

JSPL’s captive assets reduce supplier power for ore and thermal coal, but gaps in premium coking coal and specialty alloys sustain vendor leverage. Seaborne hard coking coal is concentrated—Australia ~60% share in 2024—while India imports ~80% of coking coal, raising switching costs and FX/freight exposure. Captive power (~1,500 MW in 2024) and long‑term contracts partially mitigate but do not eliminate supplier influence.

| Metric | 2024 figure |

|---|---|

| Captive power | ~1,500 MW |

| India coking coal imports | ~80% |

| Australia share seaborne HCC | ~60% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging threats specific to Jindal Steel & Power, with strategic commentary on pricing, profitability, market share risks, and protective dynamics for incumbency.

A clear, one-sheet Porter's Five Forces for Jindal Steel & Power—distills industry pressures (raw materials costs, energy constraints, buyer/supplier power, entry threats, substitutes) into a decision-ready snapshot for fast strategic moves.

Customers Bargaining Power

Commodity pricing heightens sensitivity

Commodity pricing heightens sensitivity as steel buyers, facing commoditized grades, react to even 1–2% price deltas that can reallocate volumes in spot markets. This dynamic raises buyer bargaining power in downcycles when margins compress and purchase switching increases. JSPL mitigates pressure through higher-margin value-added products and by emphasizing service reliability and delivery performance to retain contracts.

Large institutional buyers wield clout

Infrastructure EPCs, OEMs and Indian Railways place large, repeat orders, enabling tougher negotiations on price and payment terms; Indian Railways' capital outlay for 2024–25 was announced at 2.40 trillion rupees, underscoring procurement scale. Qualification norms and long-term supply contracts make winning and retaining them crucial, and JSPL’s rails and long-products portfolio is explicitly targeted at these high-volume accounts.

Switching costs vary by application

Standard longs and flats carry low switching costs, so buyers can shop suppliers easily, keeping buyer power high; by contrast certified rails, API-grade plates and high-spec coils require approvals that raise switching costs and weaken buyer leverage. In 2024 JSPL emphasized certifications, investing in API, EN and rail approvals to lock customers, with value-added certified products representing about 20% of steel sales that year.

Demand cyclicality shifts leverage

In downturns excess supply strengthens buyers and compresses spreads, while India produced about 125 MT of crude steel in FY2023-24, increasing buyer options; during capex upcycles and the government’s INR 10 lakh crore 2024–25 capex push leverage shifts back to mills. Contracting mix (spot vs contract) moderates power swings, and JSPL uses hedged contracts to stabilize realizations.

Service, delivery, and financing terms

Just-in-time delivery, flexible credit terms and robust after-sales support significantly shape buyer choices; JSPL’s emphasis on logistics and working-capital solutions reduces price as the primary lever. Superior distribution and financing tie-ups narrow effective buyer power by improving order reliability and cash-flow for customers. As of 2024 JSPL operates expanded steel capacity and strengthened sales logistics to support these services.

- Jindal advantage: logistics + financing = reduced buyer price leverage

Buyers dominate commoditized steel; mills push certified grades, logistics and hedges

Buyers wield high power on commoditized longs/flats, shifting volumes on 1–2% price moves; certified products (≈20% of JSPL 2024 steel sales) reduce switching. India crude steel ~125 MT in FY2023-24, excess supply strengthens buyers in downturns while INR 10 lakh crore 2024–25 capex shifts leverage to mills. JSPL counters with value-added grades, logistics, financing and hedged contracts to stabilize realizations.

| Metric | Value |

|---|---|

| India crude steel FY2023-24 | ~125 MT |

| 2024–25 Govt capex | INR 10 lakh crore |

| JSPL certified/value-added share 2024 | ~20% |

Full Version Awaits

Jindal Steel & Power Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Jindal Steel & Power Porter's Five Forces analysis evaluates supplier and buyer power, threat of new entrants and substitutes, and intensity of competitive rivalry specific to steel, power and mining segments. It highlights strategic implications and actionable risks and opportunities.