JINS Holdings Porter's Five Forces Analysis

Don't Miss the Bigger Picture

JINS Holdings faces moderate supplier power, intense buyer choice, and growing digital-native substitutes that pressure margins, while brand differentiation and retail scale temper new entrant threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore JINS’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Concentrated lens and component sources

High-quality ophthalmic lenses, coatings and premium frame materials are sourced from a relatively concentrated set of global suppliers—major players such as EssilorLuxottica reported €24.3bn revenue in 2023—giving key vendors leverage on pricing and lead times. JINS can mitigate risk via dual-sourcing, private-label specifications, and long-term contracts with volume commitments to stabilize terms.

Switching costs in tooling and quality

Changing lens labs or frame OEMs requires retooling, QC alignment and re‑certification, creating switching frictions that concentrate supplier leverage on critical SKUs; lead-time and defect-rate impacts are amplified in a global eyewear market valued at about USD 166.8 billion in 2024 (Statista). Standardizing components and designs can materially lower swap costs and shorten qualification cycles. Building in‑house lens and minor frame capabilities cuts dependency and mitigates supplier power.

Commodity vs specialized inputs

Basic acetate, TR-90 and hinges are commoditized, widely available and price-competitive, supporting low supplier power for frames; the global eyewear market was about $200 billion in 2024, keeping input competition intense. Specialized lenses (high-index, photochromic, blue-light, progressive) and AR coatings are less substitutable, raising supplier leverage. Supplier power is notably higher for these premium optics than for commodity parts. Maintaining a balanced product mix dilutes exposure to specialized-supplier concentration.

Logistics and FX exposure

Global supply chains expose JINS to freight, customs and FX swings, with IMF 2024 global trade growth at about 2.6% increasing demand-side volatility and suppliers often passing through cost inflation, raising their effective bargaining power.

JINS mitigates via hedging and selective nearshoring to shorten lanes, while inventory buffers smooth procurement cycles and absorb short-term freight or FX shocks.

- Freight & customs exposure

- Supplier pass-through raises costs

- Hedging & nearshoring reduce volatility

- Inventory buffers stabilize supply

Potential vertical integration by vendors

Large upstream players such as EssilorLuxottica, a vertically integrated leader, can prioritize their own retail channels, subtly increasing supplier bargaining power against retailers like JINS.

JINS offsets this with brand-led demand, diversified sourcing, and collaborative product development to align incentives and reduce dependency; EssilorLuxottica reported group revenue ~€24.1bn in 2023.

- Supplier vertical integration: increases leverage

- JINS mitigation: brand demand + sourcing diversification

- Collaboration: co-development aligns incentives

Supplier concentration in premium lenses raises pricing risk; retailers hedge via dual-sourcing

High supplier concentration for premium lenses (EssilorLuxottica €24.3bn 2023) raises pricing and lead‑time leverage; JINS mitigates via dual‑sourcing, private‑label specs and long‑term contracts. Commodity frames remain competitive, but specialized optics (high‑index, photochromic, AR) increase supplier power. Supply‑chain shocks (IMF trade +2.6% 2024) drive hedging, nearshoring and inventory buffers.

| Metric | Value |

|---|---|

| Global eyewear market | USD 166.8bn (2024) |

| EssilorLuxottica revenue | €24.3bn (2023) |

| IMF global trade growth | 2.6% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for JINS Holdings, uncovering competitive intensity, buyer and supplier power, substitution threats, and entry barriers within eyewear retail and DTC channels. Provides strategic insights on disruptive trends, pricing leverage, and defensive positioning to inform investor and management decisions.

A clear, one-sheet Porter's Five Forces for JINS Holdings—customizable pressure levels with a radar visualization for instant strategic insight, ready to drop into pitch decks or dashboards without macros.

Customers Bargaining Power

High price sensitivity and transparency

Consumers compare prices across chains and online, with frequent promotions setting reference points; this heightens customer bargaining power and compresses margins for JINS, which operated over 600 stores in 2024. Clear value propositions and tiered pricing blunt discount pressure, while bundles and extended warranties boost perceived value and average transaction size.

Low switching costs

Shoppers can easily move among retailers for frames and lenses, with online eyewear's market share at about 18% globally in 2024, lowering barriers to switch. Digital prescriptions and virtual try-on tools accelerate defection by simplifying purchase paths. JINS' loyalty programs, fit and aftercare services and consistent omnichannel experience—across its ~330 stores and digital channels in 2024—help increase customer stickiness and reduce churn.

Wide assortment alternatives

From fast-fashion labels to premium boutiques buyers face abundant choice; online marketplaces list over 10,000 eyewear SKUs in 2024, broadening styles and price points. Marketplace promotions and price transparency raise price sensitivity, while JINS and peers protect margins with curated collections, exclusive collaborations and weekly refresh cycles that keep assortment relevance and repeat purchase rates high.

Service and convenience expectations

Customers now treat quick eye exams, same-day edging, and hassle-free returns as table stakes, shifting bargaining power to buyers; in 2024 JINS operated over 500 stores globally supporting in-store labs to meet demand. Investing in lab-capable stores and efficient logistics preserves margins and retention, while clear SLAs raise repeat purchase rates and reduce complaints.

- Customers: quick exams, same-day edging, easy returns

- JINS 2024: 500+ stores with in-store lab capability

- Mitigants: invest in labs, logistics, and clear SLAs

Influence of health benefits and regulations

Insurance and employer vision benefits shape channel choice and co-pay expectations; in Japan statutory health insurance generally excludes routine eyewear, steering buyers to retail chains like JINS, while globally 2.2 billion people have vision impairment (WHO), creating large insured and self-pay segments. Buyers leverage coverage to negotiate lower out-of-pocket costs; clear claims processing shortens dispute cycles and compliance boosts repeat purchases.

- coverage-direction

- co-pay-negotiation

- claims-transparency

- compliance-trust

Omnichannel eyewear: online 18% share, 500+ stores, 2.2bn vision needs

Customers shop price/promotions across channels; online eyewear ~18% global share in 2024 raising price sensitivity. JINS operated over 500 stores with in‑store labs in 2024 to secure service-led loyalty. Insurance/co-pay dynamics and 2.2bn people with vision impairment (WHO) create mixed insured/self-pay negotiating power.

| Metric | 2024 value | Impact |

|---|---|---|

| JINS stores (with labs) | 500+ | Service retention |

| Online eyewear share | ~18% | Price sensitivity |

| Eyewear SKUs on marketplaces | 10,000+ | Choice/elasticity |

| Vision impairment (WHO) | 2.2bn | Large market/coverage effects |

Same Document Delivered

JINS Holdings Porter's Five Forces Analysis

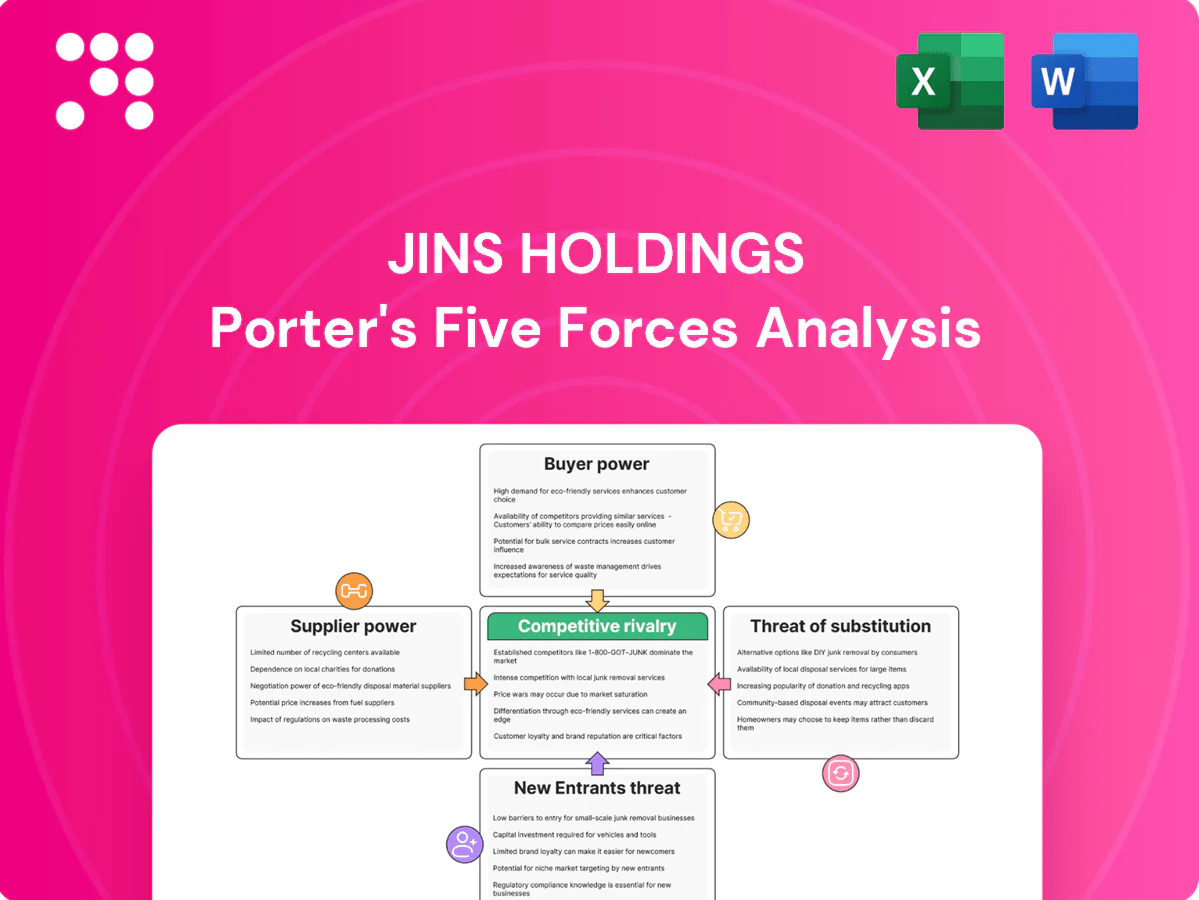

This preview shows the exact Porter's Five Forces analysis of JINS Holdings you'll receive—no surprises, no placeholders. The document assesses competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products with actionable insights. Once purchased, you'll get this fully formatted file instantly, ready to use.

Don't Miss the Bigger Picture

JINS Holdings faces moderate supplier power, intense buyer choice, and growing digital-native substitutes that pressure margins, while brand differentiation and retail scale temper new entrant threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore JINS’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Concentrated lens and component sources

High-quality ophthalmic lenses, coatings and premium frame materials are sourced from a relatively concentrated set of global suppliers—major players such as EssilorLuxottica reported €24.3bn revenue in 2023—giving key vendors leverage on pricing and lead times. JINS can mitigate risk via dual-sourcing, private-label specifications, and long-term contracts with volume commitments to stabilize terms.

Switching costs in tooling and quality

Changing lens labs or frame OEMs requires retooling, QC alignment and re‑certification, creating switching frictions that concentrate supplier leverage on critical SKUs; lead-time and defect-rate impacts are amplified in a global eyewear market valued at about USD 166.8 billion in 2024 (Statista). Standardizing components and designs can materially lower swap costs and shorten qualification cycles. Building in‑house lens and minor frame capabilities cuts dependency and mitigates supplier power.

Commodity vs specialized inputs

Basic acetate, TR-90 and hinges are commoditized, widely available and price-competitive, supporting low supplier power for frames; the global eyewear market was about $200 billion in 2024, keeping input competition intense. Specialized lenses (high-index, photochromic, blue-light, progressive) and AR coatings are less substitutable, raising supplier leverage. Supplier power is notably higher for these premium optics than for commodity parts. Maintaining a balanced product mix dilutes exposure to specialized-supplier concentration.

Logistics and FX exposure

Global supply chains expose JINS to freight, customs and FX swings, with IMF 2024 global trade growth at about 2.6% increasing demand-side volatility and suppliers often passing through cost inflation, raising their effective bargaining power.

JINS mitigates via hedging and selective nearshoring to shorten lanes, while inventory buffers smooth procurement cycles and absorb short-term freight or FX shocks.

- Freight & customs exposure

- Supplier pass-through raises costs

- Hedging & nearshoring reduce volatility

- Inventory buffers stabilize supply

Potential vertical integration by vendors

Large upstream players such as EssilorLuxottica, a vertically integrated leader, can prioritize their own retail channels, subtly increasing supplier bargaining power against retailers like JINS.

JINS offsets this with brand-led demand, diversified sourcing, and collaborative product development to align incentives and reduce dependency; EssilorLuxottica reported group revenue ~€24.1bn in 2023.

- Supplier vertical integration: increases leverage

- JINS mitigation: brand demand + sourcing diversification

- Collaboration: co-development aligns incentives

Supplier concentration in premium lenses raises pricing risk; retailers hedge via dual-sourcing

High supplier concentration for premium lenses (EssilorLuxottica €24.3bn 2023) raises pricing and lead‑time leverage; JINS mitigates via dual‑sourcing, private‑label specs and long‑term contracts. Commodity frames remain competitive, but specialized optics (high‑index, photochromic, AR) increase supplier power. Supply‑chain shocks (IMF trade +2.6% 2024) drive hedging, nearshoring and inventory buffers.

| Metric | Value |

|---|---|

| Global eyewear market | USD 166.8bn (2024) |

| EssilorLuxottica revenue | €24.3bn (2023) |

| IMF global trade growth | 2.6% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for JINS Holdings, uncovering competitive intensity, buyer and supplier power, substitution threats, and entry barriers within eyewear retail and DTC channels. Provides strategic insights on disruptive trends, pricing leverage, and defensive positioning to inform investor and management decisions.

A clear, one-sheet Porter's Five Forces for JINS Holdings—customizable pressure levels with a radar visualization for instant strategic insight, ready to drop into pitch decks or dashboards without macros.

Customers Bargaining Power

High price sensitivity and transparency

Consumers compare prices across chains and online, with frequent promotions setting reference points; this heightens customer bargaining power and compresses margins for JINS, which operated over 600 stores in 2024. Clear value propositions and tiered pricing blunt discount pressure, while bundles and extended warranties boost perceived value and average transaction size.

Low switching costs

Shoppers can easily move among retailers for frames and lenses, with online eyewear's market share at about 18% globally in 2024, lowering barriers to switch. Digital prescriptions and virtual try-on tools accelerate defection by simplifying purchase paths. JINS' loyalty programs, fit and aftercare services and consistent omnichannel experience—across its ~330 stores and digital channels in 2024—help increase customer stickiness and reduce churn.

Wide assortment alternatives

From fast-fashion labels to premium boutiques buyers face abundant choice; online marketplaces list over 10,000 eyewear SKUs in 2024, broadening styles and price points. Marketplace promotions and price transparency raise price sensitivity, while JINS and peers protect margins with curated collections, exclusive collaborations and weekly refresh cycles that keep assortment relevance and repeat purchase rates high.

Service and convenience expectations

Customers now treat quick eye exams, same-day edging, and hassle-free returns as table stakes, shifting bargaining power to buyers; in 2024 JINS operated over 500 stores globally supporting in-store labs to meet demand. Investing in lab-capable stores and efficient logistics preserves margins and retention, while clear SLAs raise repeat purchase rates and reduce complaints.

- Customers: quick exams, same-day edging, easy returns

- JINS 2024: 500+ stores with in-store lab capability

- Mitigants: invest in labs, logistics, and clear SLAs

Influence of health benefits and regulations

Insurance and employer vision benefits shape channel choice and co-pay expectations; in Japan statutory health insurance generally excludes routine eyewear, steering buyers to retail chains like JINS, while globally 2.2 billion people have vision impairment (WHO), creating large insured and self-pay segments. Buyers leverage coverage to negotiate lower out-of-pocket costs; clear claims processing shortens dispute cycles and compliance boosts repeat purchases.

- coverage-direction

- co-pay-negotiation

- claims-transparency

- compliance-trust

Omnichannel eyewear: online 18% share, 500+ stores, 2.2bn vision needs

Customers shop price/promotions across channels; online eyewear ~18% global share in 2024 raising price sensitivity. JINS operated over 500 stores with in‑store labs in 2024 to secure service-led loyalty. Insurance/co-pay dynamics and 2.2bn people with vision impairment (WHO) create mixed insured/self-pay negotiating power.

| Metric | 2024 value | Impact |

|---|---|---|

| JINS stores (with labs) | 500+ | Service retention |

| Online eyewear share | ~18% | Price sensitivity |

| Eyewear SKUs on marketplaces | 10,000+ | Choice/elasticity |

| Vision impairment (WHO) | 2.2bn | Large market/coverage effects |

Same Document Delivered

JINS Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of JINS Holdings you'll receive—no surprises, no placeholders. The document assesses competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products with actionable insights. Once purchased, you'll get this fully formatted file instantly, ready to use.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

JINS Holdings faces moderate supplier power, intense buyer choice, and growing digital-native substitutes that pressure margins, while brand differentiation and retail scale temper new entrant threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore JINS’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Concentrated lens and component sources

High-quality ophthalmic lenses, coatings and premium frame materials are sourced from a relatively concentrated set of global suppliers—major players such as EssilorLuxottica reported €24.3bn revenue in 2023—giving key vendors leverage on pricing and lead times. JINS can mitigate risk via dual-sourcing, private-label specifications, and long-term contracts with volume commitments to stabilize terms.

Switching costs in tooling and quality

Changing lens labs or frame OEMs requires retooling, QC alignment and re‑certification, creating switching frictions that concentrate supplier leverage on critical SKUs; lead-time and defect-rate impacts are amplified in a global eyewear market valued at about USD 166.8 billion in 2024 (Statista). Standardizing components and designs can materially lower swap costs and shorten qualification cycles. Building in‑house lens and minor frame capabilities cuts dependency and mitigates supplier power.

Commodity vs specialized inputs

Basic acetate, TR-90 and hinges are commoditized, widely available and price-competitive, supporting low supplier power for frames; the global eyewear market was about $200 billion in 2024, keeping input competition intense. Specialized lenses (high-index, photochromic, blue-light, progressive) and AR coatings are less substitutable, raising supplier leverage. Supplier power is notably higher for these premium optics than for commodity parts. Maintaining a balanced product mix dilutes exposure to specialized-supplier concentration.

Logistics and FX exposure

Global supply chains expose JINS to freight, customs and FX swings, with IMF 2024 global trade growth at about 2.6% increasing demand-side volatility and suppliers often passing through cost inflation, raising their effective bargaining power.

JINS mitigates via hedging and selective nearshoring to shorten lanes, while inventory buffers smooth procurement cycles and absorb short-term freight or FX shocks.

- Freight & customs exposure

- Supplier pass-through raises costs

- Hedging & nearshoring reduce volatility

- Inventory buffers stabilize supply

Potential vertical integration by vendors

Large upstream players such as EssilorLuxottica, a vertically integrated leader, can prioritize their own retail channels, subtly increasing supplier bargaining power against retailers like JINS.

JINS offsets this with brand-led demand, diversified sourcing, and collaborative product development to align incentives and reduce dependency; EssilorLuxottica reported group revenue ~€24.1bn in 2023.

- Supplier vertical integration: increases leverage

- JINS mitigation: brand demand + sourcing diversification

- Collaboration: co-development aligns incentives

Supplier concentration in premium lenses raises pricing risk; retailers hedge via dual-sourcing

High supplier concentration for premium lenses (EssilorLuxottica €24.3bn 2023) raises pricing and lead‑time leverage; JINS mitigates via dual‑sourcing, private‑label specs and long‑term contracts. Commodity frames remain competitive, but specialized optics (high‑index, photochromic, AR) increase supplier power. Supply‑chain shocks (IMF trade +2.6% 2024) drive hedging, nearshoring and inventory buffers.

| Metric | Value |

|---|---|

| Global eyewear market | USD 166.8bn (2024) |

| EssilorLuxottica revenue | €24.3bn (2023) |

| IMF global trade growth | 2.6% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for JINS Holdings, uncovering competitive intensity, buyer and supplier power, substitution threats, and entry barriers within eyewear retail and DTC channels. Provides strategic insights on disruptive trends, pricing leverage, and defensive positioning to inform investor and management decisions.

A clear, one-sheet Porter's Five Forces for JINS Holdings—customizable pressure levels with a radar visualization for instant strategic insight, ready to drop into pitch decks or dashboards without macros.

Customers Bargaining Power

High price sensitivity and transparency

Consumers compare prices across chains and online, with frequent promotions setting reference points; this heightens customer bargaining power and compresses margins for JINS, which operated over 600 stores in 2024. Clear value propositions and tiered pricing blunt discount pressure, while bundles and extended warranties boost perceived value and average transaction size.

Low switching costs

Shoppers can easily move among retailers for frames and lenses, with online eyewear's market share at about 18% globally in 2024, lowering barriers to switch. Digital prescriptions and virtual try-on tools accelerate defection by simplifying purchase paths. JINS' loyalty programs, fit and aftercare services and consistent omnichannel experience—across its ~330 stores and digital channels in 2024—help increase customer stickiness and reduce churn.

Wide assortment alternatives

From fast-fashion labels to premium boutiques buyers face abundant choice; online marketplaces list over 10,000 eyewear SKUs in 2024, broadening styles and price points. Marketplace promotions and price transparency raise price sensitivity, while JINS and peers protect margins with curated collections, exclusive collaborations and weekly refresh cycles that keep assortment relevance and repeat purchase rates high.

Service and convenience expectations

Customers now treat quick eye exams, same-day edging, and hassle-free returns as table stakes, shifting bargaining power to buyers; in 2024 JINS operated over 500 stores globally supporting in-store labs to meet demand. Investing in lab-capable stores and efficient logistics preserves margins and retention, while clear SLAs raise repeat purchase rates and reduce complaints.

- Customers: quick exams, same-day edging, easy returns

- JINS 2024: 500+ stores with in-store lab capability

- Mitigants: invest in labs, logistics, and clear SLAs

Influence of health benefits and regulations

Insurance and employer vision benefits shape channel choice and co-pay expectations; in Japan statutory health insurance generally excludes routine eyewear, steering buyers to retail chains like JINS, while globally 2.2 billion people have vision impairment (WHO), creating large insured and self-pay segments. Buyers leverage coverage to negotiate lower out-of-pocket costs; clear claims processing shortens dispute cycles and compliance boosts repeat purchases.

- coverage-direction

- co-pay-negotiation

- claims-transparency

- compliance-trust

Omnichannel eyewear: online 18% share, 500+ stores, 2.2bn vision needs

Customers shop price/promotions across channels; online eyewear ~18% global share in 2024 raising price sensitivity. JINS operated over 500 stores with in‑store labs in 2024 to secure service-led loyalty. Insurance/co-pay dynamics and 2.2bn people with vision impairment (WHO) create mixed insured/self-pay negotiating power.

| Metric | 2024 value | Impact |

|---|---|---|

| JINS stores (with labs) | 500+ | Service retention |

| Online eyewear share | ~18% | Price sensitivity |

| Eyewear SKUs on marketplaces | 10,000+ | Choice/elasticity |

| Vision impairment (WHO) | 2.2bn | Large market/coverage effects |

Same Document Delivered

JINS Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of JINS Holdings you'll receive—no surprises, no placeholders. The document assesses competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products with actionable insights. Once purchased, you'll get this fully formatted file instantly, ready to use.