JINS Holdings PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Quickly grasp how political, economic and technological shifts are reshaping JINS Holdings’ competitive edge and operational risks. This concise PESTLE snapshot highlights regulatory pressures, market trends, and innovation drivers you need to know. Purchase the full analysis for a complete, actionable breakdown and ready-to-use insights.

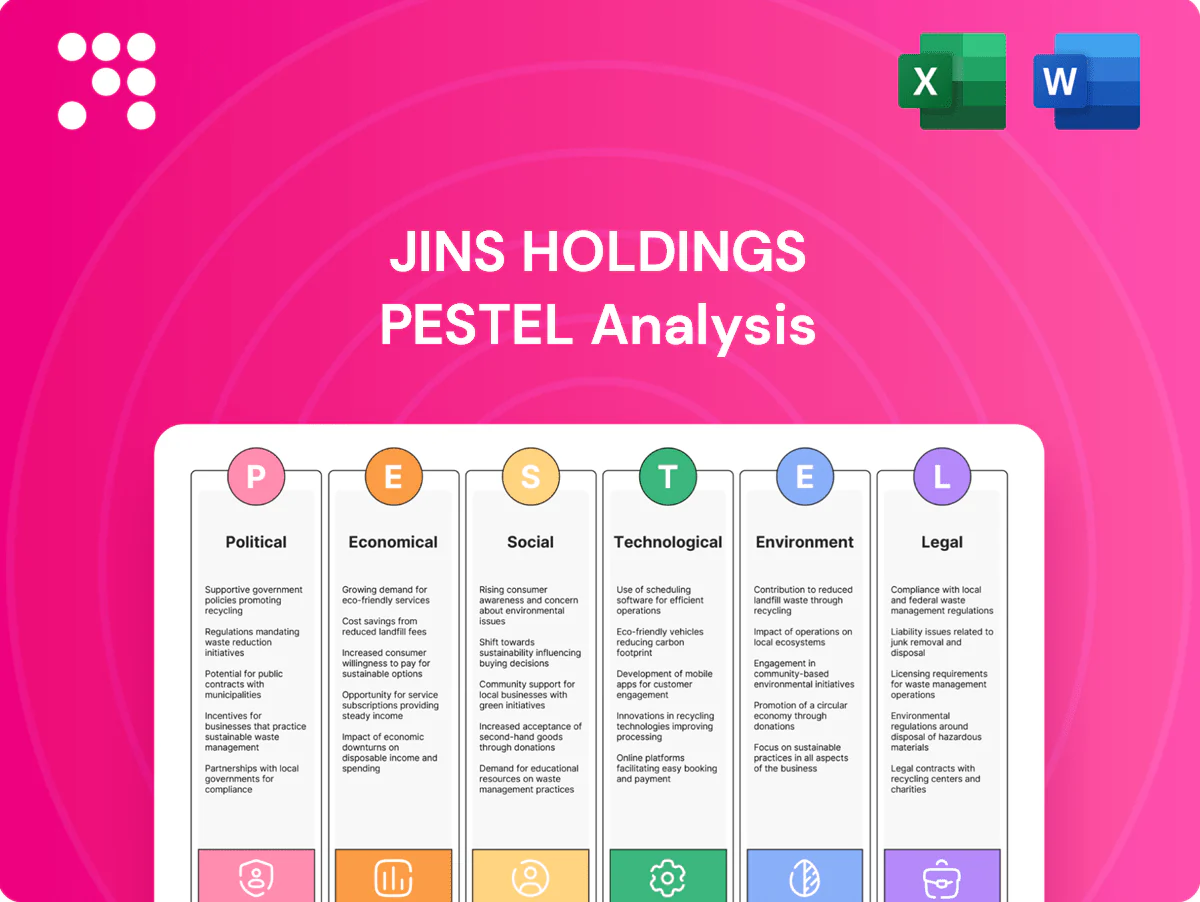

Political factors

Trade policy and tariffs on eyewear

Import duties on frames, lenses and raw materials directly lift landed costs and compress margins; Japan's average applied MFN tariff is about 2.7% (WTO, 2023), though specific lines can be higher under HS classifications. Changes in Japan’s FTAs (CPTPP, Japan-EU EPA) and rules-of-origin shift sourcing/assembly economics, while geopolitical frictions with China risk sudden tariff or non-tariff barriers. JINS must diversify suppliers and strengthen customs compliance to protect margins.

Government support for healthcare and vision

Public policy on eye health screenings and insurance shapes prescription demand; WHO reports 2.2 billion people have vision impairment, with 1 billion preventable, signaling large unmet need. School and workplace vision programs drive recurring purchases of basic frames. Subsidies or tax incentives for domestic manufacturing can materially alter JINS cost structures. JINS can align assortments to reimbursable products to capture volume.

Labor and immigration policies

Retail staffing in Japan and overseas depends on visa rules and wage regulations; Japan's unemployment was about 2.6% in 2024 and foreign workers exceeded 2 million in 2023, shaping available labor supply.

Tight labor markets and successive minimum wage hikes (notably in 2023–24) have lifted store operating costs, squeezing retail margins.

Policy shifts on part-time employment reduce scheduling flexibility, so JINS needs targeted labor-productivity tools and accelerated staff training to offset policy-driven cost pressure.

Urban development and retail zoning

Local zoning and permitting dictate JINS store openings and remodel timelines, often creating multi-month approval cycles that affect CAPEX scheduling. Transit-oriented development and higher urban density support mall and street footfall—UN estimates 2024 urban population at 4.48 billion, concentrating consumer traffic in transit hubs. Restrictions on signage and store formats limit brand visibility, so JINS should engage municipalities early to secure high-traffic sites.

- Engage municipalities early

- Prioritize transit-oriented sites

- Monitor signage/format restrictions

Currency and foreign investment stance

Japan’s monetary stance and periodic MOF FX interventions (notably in 2022–23) kept the yen weak — roughly 150–160 JPY per USD in 2024–25 — raising imported sourcing costs; policy signals on outbound FDI and bilateral frameworks influence how Japanese retailers like JINS expand overseas, while capital repatriation rules and tax treatment constrain cash deployment and dividends; JINS must actively hedge USD- and CNY-linked sourcing exposure.

- FX risk: hedge USD/CNY exposure

- Yen level: ~150–160 JPY/USD (2024–25)

- Policy: MOF interventions in 2022–23

- Impact: repatriation rules affect dividends/cash strategy

Tariffs, yen swings and labor tightness reshape vision care demand; hedge suppliers now

Import tariffs raise landed costs (Japan MFN tariff ~2.7% WTO 2023) and FTAs (CPTPP, Japan-EU EPA) shift sourcing economics; WHO cites 2.2bn with vision impairment (1bn preventable) boosting addressable demand. Labor tightness (unemp ~2.6% 2024; foreign workers >2m 2023) and yen ~150–160 JPY/USD (2024–25) raise operating and sourcing costs; hedge and diversify suppliers.

| Issue | Key data | Impact |

|---|---|---|

| Tariffs | MFN ~2.7% (WTO 2023) | Higher COGS |

| Demand | 2.2bn impaired; 1bn preventable | Reimbursable sales |

| FX | 150–160 JPY/USD (2024–25) | Cost volatility |

What is included in the product

Explores how macro-environmental factors—Political, Economic, Social, Technological, Environmental, and Legal—uniquely affect JINS Holdings (Japan/global eyewear & retail‑tech), combining data‑driven trends and regulatory context to help executives, investors, and consultants identify strategic risks, opportunities and forward‑looking scenarios.

A concise, visually segmented PESTLE summary for JINS Holdings that streamlines external risk assessment, is easily editable for regional context, and ready to drop into presentations or share across teams.

Economic factors

FX volatility and cost of goods

Yen volatility—USD/JPY averaging roughly 155–160 in 2024–mid‑2025—raises landed costs for imported frames, lenses and chemicals, compressing gross margins for retailers like JINS. Passing costs risks demand elasticity in value‑sensitive segments where price hikes can cut volumes. Strategic hedging, mixed‑currency sourcing and aligning tiered price points and promotional levers to FX scenarios can stabilize margins and preserve market share.

Consumer spending cycles

Macroeconomic slowdowns delay discretionary eyewear upgrades and accessories, and with the global eyewear market at about $148 billion in 2023 and a ~7% CAGR to 2030, JINS may see near-term trading-down as consumers prioritize essentials. Prescription sales remain more resilient but can shift to lower-price frames; recovery phases typically boost demand for higher-margin fashion and premium lenses. JINS can tier assortments and price points to capture varied budgets across cycles.

Inflation in materials and logistics

Acetate, titanium, specialty coatings and freight carry cyclical inflation risk, with global container freight rates remaining roughly 30% above 2019 levels in 2024, keeping landed costs elevated. Tightness in specialty resins has periodically pushed lens and frame input margins by several percentage points for manufacturers in 2024. Long-term supplier contracts and nearshoring reduce volatility, and JINS should optimize SKU complexity to cut material waste.

E-commerce growth and omnichannel mix

E-commerce growth (global e‑commerce sales US$5.7 trillion in 2022, projected US$8.1 trillion by 2026 per Statista) lowers per‑transaction fulfillment costs but raises returns and CX expectations; higher online returns and demand for seamless experiences push JINS to invest in frictionless checkout, fast delivery and dynamic pricing. Click‑and‑collect can lift store productivity and attachment rates while price transparency intensifies DTC competition.

- Lower fulfillment cost per order

- Higher return/CX expectations

- Click‑and‑collect boosts store sales

- Price transparency favors DTC

- Need: frictionless checkout, fast delivery, smart pricing

Interest rates and lease economics

Higher interest rates since the Bank of Japan moved away from negative rates in 2023 have elevated financing costs for store fit-outs and distribution-center capex, squeezing project IRRs for JINS. Landlords in prime urban hubs often resist rent concessions despite footfall risk, increasing fixed-cost exposure. Embedding lease flexibility and performance-linked clauses can protect cash flow; JINS should prioritize high-ROI store formats and smaller footprints to preserve returns.

- financing-costs: BOJ exit from negative rates (2023) raised borrowing pressure

- landlord-power: limited concessions in prime hubs—higher fixed rent risk

- lease-mitigation: flexibility and performance-linked clauses protect cash flow

- portfolio-focus: prioritize high-ROI formats and smaller footprints

Tariffs, yen swings and labor tightness reshape vision care demand; hedge suppliers now

Yen at ~155–160 (2024–mid‑2025) raises imported input costs; global eyewear market ~$148bn (2023) with ~7% CAGR to 2030 tempers volume upside. Container rates ~+30% vs 2019 (2024) and e‑commerce growth (US$5.7tn 2022 → US$8.1tn 2026) shift channel economics; BOJ exit from negative rates (2023) increases financing costs for store CAPEX.

| Metric | 2023–2025 |

|---|---|

| USD/JPY | ~155–160 |

| Eyewear market | $148bn (2023), ~7% CAGR |

| Freight vs 2019 | ~+30% (2024) |

| E‑commerce | $5.7tn (2022) → $8.1tn (2026) |

| BOJ policy | Exit NIRP (2023) |

Preview the Actual Deliverable

JINS Holdings PESTLE Analysis

The JINS Holdings PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessment specific to JINS. No placeholders or teasers—this is the final file you’ll download instantly after payment.

Your Shortcut to Market Insight Starts Here

Quickly grasp how political, economic and technological shifts are reshaping JINS Holdings’ competitive edge and operational risks. This concise PESTLE snapshot highlights regulatory pressures, market trends, and innovation drivers you need to know. Purchase the full analysis for a complete, actionable breakdown and ready-to-use insights.

Political factors

Trade policy and tariffs on eyewear

Import duties on frames, lenses and raw materials directly lift landed costs and compress margins; Japan's average applied MFN tariff is about 2.7% (WTO, 2023), though specific lines can be higher under HS classifications. Changes in Japan’s FTAs (CPTPP, Japan-EU EPA) and rules-of-origin shift sourcing/assembly economics, while geopolitical frictions with China risk sudden tariff or non-tariff barriers. JINS must diversify suppliers and strengthen customs compliance to protect margins.

Government support for healthcare and vision

Public policy on eye health screenings and insurance shapes prescription demand; WHO reports 2.2 billion people have vision impairment, with 1 billion preventable, signaling large unmet need. School and workplace vision programs drive recurring purchases of basic frames. Subsidies or tax incentives for domestic manufacturing can materially alter JINS cost structures. JINS can align assortments to reimbursable products to capture volume.

Labor and immigration policies

Retail staffing in Japan and overseas depends on visa rules and wage regulations; Japan's unemployment was about 2.6% in 2024 and foreign workers exceeded 2 million in 2023, shaping available labor supply.

Tight labor markets and successive minimum wage hikes (notably in 2023–24) have lifted store operating costs, squeezing retail margins.

Policy shifts on part-time employment reduce scheduling flexibility, so JINS needs targeted labor-productivity tools and accelerated staff training to offset policy-driven cost pressure.

Urban development and retail zoning

Local zoning and permitting dictate JINS store openings and remodel timelines, often creating multi-month approval cycles that affect CAPEX scheduling. Transit-oriented development and higher urban density support mall and street footfall—UN estimates 2024 urban population at 4.48 billion, concentrating consumer traffic in transit hubs. Restrictions on signage and store formats limit brand visibility, so JINS should engage municipalities early to secure high-traffic sites.

- Engage municipalities early

- Prioritize transit-oriented sites

- Monitor signage/format restrictions

Currency and foreign investment stance

Japan’s monetary stance and periodic MOF FX interventions (notably in 2022–23) kept the yen weak — roughly 150–160 JPY per USD in 2024–25 — raising imported sourcing costs; policy signals on outbound FDI and bilateral frameworks influence how Japanese retailers like JINS expand overseas, while capital repatriation rules and tax treatment constrain cash deployment and dividends; JINS must actively hedge USD- and CNY-linked sourcing exposure.

- FX risk: hedge USD/CNY exposure

- Yen level: ~150–160 JPY/USD (2024–25)

- Policy: MOF interventions in 2022–23

- Impact: repatriation rules affect dividends/cash strategy

Tariffs, yen swings and labor tightness reshape vision care demand; hedge suppliers now

Import tariffs raise landed costs (Japan MFN tariff ~2.7% WTO 2023) and FTAs (CPTPP, Japan-EU EPA) shift sourcing economics; WHO cites 2.2bn with vision impairment (1bn preventable) boosting addressable demand. Labor tightness (unemp ~2.6% 2024; foreign workers >2m 2023) and yen ~150–160 JPY/USD (2024–25) raise operating and sourcing costs; hedge and diversify suppliers.

| Issue | Key data | Impact |

|---|---|---|

| Tariffs | MFN ~2.7% (WTO 2023) | Higher COGS |

| Demand | 2.2bn impaired; 1bn preventable | Reimbursable sales |

| FX | 150–160 JPY/USD (2024–25) | Cost volatility |

What is included in the product

Explores how macro-environmental factors—Political, Economic, Social, Technological, Environmental, and Legal—uniquely affect JINS Holdings (Japan/global eyewear & retail‑tech), combining data‑driven trends and regulatory context to help executives, investors, and consultants identify strategic risks, opportunities and forward‑looking scenarios.

A concise, visually segmented PESTLE summary for JINS Holdings that streamlines external risk assessment, is easily editable for regional context, and ready to drop into presentations or share across teams.

Economic factors

FX volatility and cost of goods

Yen volatility—USD/JPY averaging roughly 155–160 in 2024–mid‑2025—raises landed costs for imported frames, lenses and chemicals, compressing gross margins for retailers like JINS. Passing costs risks demand elasticity in value‑sensitive segments where price hikes can cut volumes. Strategic hedging, mixed‑currency sourcing and aligning tiered price points and promotional levers to FX scenarios can stabilize margins and preserve market share.

Consumer spending cycles

Macroeconomic slowdowns delay discretionary eyewear upgrades and accessories, and with the global eyewear market at about $148 billion in 2023 and a ~7% CAGR to 2030, JINS may see near-term trading-down as consumers prioritize essentials. Prescription sales remain more resilient but can shift to lower-price frames; recovery phases typically boost demand for higher-margin fashion and premium lenses. JINS can tier assortments and price points to capture varied budgets across cycles.

Inflation in materials and logistics

Acetate, titanium, specialty coatings and freight carry cyclical inflation risk, with global container freight rates remaining roughly 30% above 2019 levels in 2024, keeping landed costs elevated. Tightness in specialty resins has periodically pushed lens and frame input margins by several percentage points for manufacturers in 2024. Long-term supplier contracts and nearshoring reduce volatility, and JINS should optimize SKU complexity to cut material waste.

E-commerce growth and omnichannel mix

E-commerce growth (global e‑commerce sales US$5.7 trillion in 2022, projected US$8.1 trillion by 2026 per Statista) lowers per‑transaction fulfillment costs but raises returns and CX expectations; higher online returns and demand for seamless experiences push JINS to invest in frictionless checkout, fast delivery and dynamic pricing. Click‑and‑collect can lift store productivity and attachment rates while price transparency intensifies DTC competition.

- Lower fulfillment cost per order

- Higher return/CX expectations

- Click‑and‑collect boosts store sales

- Price transparency favors DTC

- Need: frictionless checkout, fast delivery, smart pricing

Interest rates and lease economics

Higher interest rates since the Bank of Japan moved away from negative rates in 2023 have elevated financing costs for store fit-outs and distribution-center capex, squeezing project IRRs for JINS. Landlords in prime urban hubs often resist rent concessions despite footfall risk, increasing fixed-cost exposure. Embedding lease flexibility and performance-linked clauses can protect cash flow; JINS should prioritize high-ROI store formats and smaller footprints to preserve returns.

- financing-costs: BOJ exit from negative rates (2023) raised borrowing pressure

- landlord-power: limited concessions in prime hubs—higher fixed rent risk

- lease-mitigation: flexibility and performance-linked clauses protect cash flow

- portfolio-focus: prioritize high-ROI formats and smaller footprints

Tariffs, yen swings and labor tightness reshape vision care demand; hedge suppliers now

Yen at ~155–160 (2024–mid‑2025) raises imported input costs; global eyewear market ~$148bn (2023) with ~7% CAGR to 2030 tempers volume upside. Container rates ~+30% vs 2019 (2024) and e‑commerce growth (US$5.7tn 2022 → US$8.1tn 2026) shift channel economics; BOJ exit from negative rates (2023) increases financing costs for store CAPEX.

| Metric | 2023–2025 |

|---|---|

| USD/JPY | ~155–160 |

| Eyewear market | $148bn (2023), ~7% CAGR |

| Freight vs 2019 | ~+30% (2024) |

| E‑commerce | $5.7tn (2022) → $8.1tn (2026) |

| BOJ policy | Exit NIRP (2023) |

Preview the Actual Deliverable

JINS Holdings PESTLE Analysis

The JINS Holdings PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessment specific to JINS. No placeholders or teasers—this is the final file you’ll download instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Quickly grasp how political, economic and technological shifts are reshaping JINS Holdings’ competitive edge and operational risks. This concise PESTLE snapshot highlights regulatory pressures, market trends, and innovation drivers you need to know. Purchase the full analysis for a complete, actionable breakdown and ready-to-use insights.

Political factors

Trade policy and tariffs on eyewear

Import duties on frames, lenses and raw materials directly lift landed costs and compress margins; Japan's average applied MFN tariff is about 2.7% (WTO, 2023), though specific lines can be higher under HS classifications. Changes in Japan’s FTAs (CPTPP, Japan-EU EPA) and rules-of-origin shift sourcing/assembly economics, while geopolitical frictions with China risk sudden tariff or non-tariff barriers. JINS must diversify suppliers and strengthen customs compliance to protect margins.

Government support for healthcare and vision

Public policy on eye health screenings and insurance shapes prescription demand; WHO reports 2.2 billion people have vision impairment, with 1 billion preventable, signaling large unmet need. School and workplace vision programs drive recurring purchases of basic frames. Subsidies or tax incentives for domestic manufacturing can materially alter JINS cost structures. JINS can align assortments to reimbursable products to capture volume.

Labor and immigration policies

Retail staffing in Japan and overseas depends on visa rules and wage regulations; Japan's unemployment was about 2.6% in 2024 and foreign workers exceeded 2 million in 2023, shaping available labor supply.

Tight labor markets and successive minimum wage hikes (notably in 2023–24) have lifted store operating costs, squeezing retail margins.

Policy shifts on part-time employment reduce scheduling flexibility, so JINS needs targeted labor-productivity tools and accelerated staff training to offset policy-driven cost pressure.

Urban development and retail zoning

Local zoning and permitting dictate JINS store openings and remodel timelines, often creating multi-month approval cycles that affect CAPEX scheduling. Transit-oriented development and higher urban density support mall and street footfall—UN estimates 2024 urban population at 4.48 billion, concentrating consumer traffic in transit hubs. Restrictions on signage and store formats limit brand visibility, so JINS should engage municipalities early to secure high-traffic sites.

- Engage municipalities early

- Prioritize transit-oriented sites

- Monitor signage/format restrictions

Currency and foreign investment stance

Japan’s monetary stance and periodic MOF FX interventions (notably in 2022–23) kept the yen weak — roughly 150–160 JPY per USD in 2024–25 — raising imported sourcing costs; policy signals on outbound FDI and bilateral frameworks influence how Japanese retailers like JINS expand overseas, while capital repatriation rules and tax treatment constrain cash deployment and dividends; JINS must actively hedge USD- and CNY-linked sourcing exposure.

- FX risk: hedge USD/CNY exposure

- Yen level: ~150–160 JPY/USD (2024–25)

- Policy: MOF interventions in 2022–23

- Impact: repatriation rules affect dividends/cash strategy

Tariffs, yen swings and labor tightness reshape vision care demand; hedge suppliers now

Import tariffs raise landed costs (Japan MFN tariff ~2.7% WTO 2023) and FTAs (CPTPP, Japan-EU EPA) shift sourcing economics; WHO cites 2.2bn with vision impairment (1bn preventable) boosting addressable demand. Labor tightness (unemp ~2.6% 2024; foreign workers >2m 2023) and yen ~150–160 JPY/USD (2024–25) raise operating and sourcing costs; hedge and diversify suppliers.

| Issue | Key data | Impact |

|---|---|---|

| Tariffs | MFN ~2.7% (WTO 2023) | Higher COGS |

| Demand | 2.2bn impaired; 1bn preventable | Reimbursable sales |

| FX | 150–160 JPY/USD (2024–25) | Cost volatility |

What is included in the product

Explores how macro-environmental factors—Political, Economic, Social, Technological, Environmental, and Legal—uniquely affect JINS Holdings (Japan/global eyewear & retail‑tech), combining data‑driven trends and regulatory context to help executives, investors, and consultants identify strategic risks, opportunities and forward‑looking scenarios.

A concise, visually segmented PESTLE summary for JINS Holdings that streamlines external risk assessment, is easily editable for regional context, and ready to drop into presentations or share across teams.

Economic factors

FX volatility and cost of goods

Yen volatility—USD/JPY averaging roughly 155–160 in 2024–mid‑2025—raises landed costs for imported frames, lenses and chemicals, compressing gross margins for retailers like JINS. Passing costs risks demand elasticity in value‑sensitive segments where price hikes can cut volumes. Strategic hedging, mixed‑currency sourcing and aligning tiered price points and promotional levers to FX scenarios can stabilize margins and preserve market share.

Consumer spending cycles

Macroeconomic slowdowns delay discretionary eyewear upgrades and accessories, and with the global eyewear market at about $148 billion in 2023 and a ~7% CAGR to 2030, JINS may see near-term trading-down as consumers prioritize essentials. Prescription sales remain more resilient but can shift to lower-price frames; recovery phases typically boost demand for higher-margin fashion and premium lenses. JINS can tier assortments and price points to capture varied budgets across cycles.

Inflation in materials and logistics

Acetate, titanium, specialty coatings and freight carry cyclical inflation risk, with global container freight rates remaining roughly 30% above 2019 levels in 2024, keeping landed costs elevated. Tightness in specialty resins has periodically pushed lens and frame input margins by several percentage points for manufacturers in 2024. Long-term supplier contracts and nearshoring reduce volatility, and JINS should optimize SKU complexity to cut material waste.

E-commerce growth and omnichannel mix

E-commerce growth (global e‑commerce sales US$5.7 trillion in 2022, projected US$8.1 trillion by 2026 per Statista) lowers per‑transaction fulfillment costs but raises returns and CX expectations; higher online returns and demand for seamless experiences push JINS to invest in frictionless checkout, fast delivery and dynamic pricing. Click‑and‑collect can lift store productivity and attachment rates while price transparency intensifies DTC competition.

- Lower fulfillment cost per order

- Higher return/CX expectations

- Click‑and‑collect boosts store sales

- Price transparency favors DTC

- Need: frictionless checkout, fast delivery, smart pricing

Interest rates and lease economics

Higher interest rates since the Bank of Japan moved away from negative rates in 2023 have elevated financing costs for store fit-outs and distribution-center capex, squeezing project IRRs for JINS. Landlords in prime urban hubs often resist rent concessions despite footfall risk, increasing fixed-cost exposure. Embedding lease flexibility and performance-linked clauses can protect cash flow; JINS should prioritize high-ROI store formats and smaller footprints to preserve returns.

- financing-costs: BOJ exit from negative rates (2023) raised borrowing pressure

- landlord-power: limited concessions in prime hubs—higher fixed rent risk

- lease-mitigation: flexibility and performance-linked clauses protect cash flow

- portfolio-focus: prioritize high-ROI formats and smaller footprints

Tariffs, yen swings and labor tightness reshape vision care demand; hedge suppliers now

Yen at ~155–160 (2024–mid‑2025) raises imported input costs; global eyewear market ~$148bn (2023) with ~7% CAGR to 2030 tempers volume upside. Container rates ~+30% vs 2019 (2024) and e‑commerce growth (US$5.7tn 2022 → US$8.1tn 2026) shift channel economics; BOJ exit from negative rates (2023) increases financing costs for store CAPEX.

| Metric | 2023–2025 |

|---|---|

| USD/JPY | ~155–160 |

| Eyewear market | $148bn (2023), ~7% CAGR |

| Freight vs 2019 | ~+30% (2024) |

| E‑commerce | $5.7tn (2022) → $8.1tn (2026) |

| BOJ policy | Exit NIRP (2023) |

Preview the Actual Deliverable

JINS Holdings PESTLE Analysis

The JINS Holdings PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessment specific to JINS. No placeholders or teasers—this is the final file you’ll download instantly after payment.