JM Eagle Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

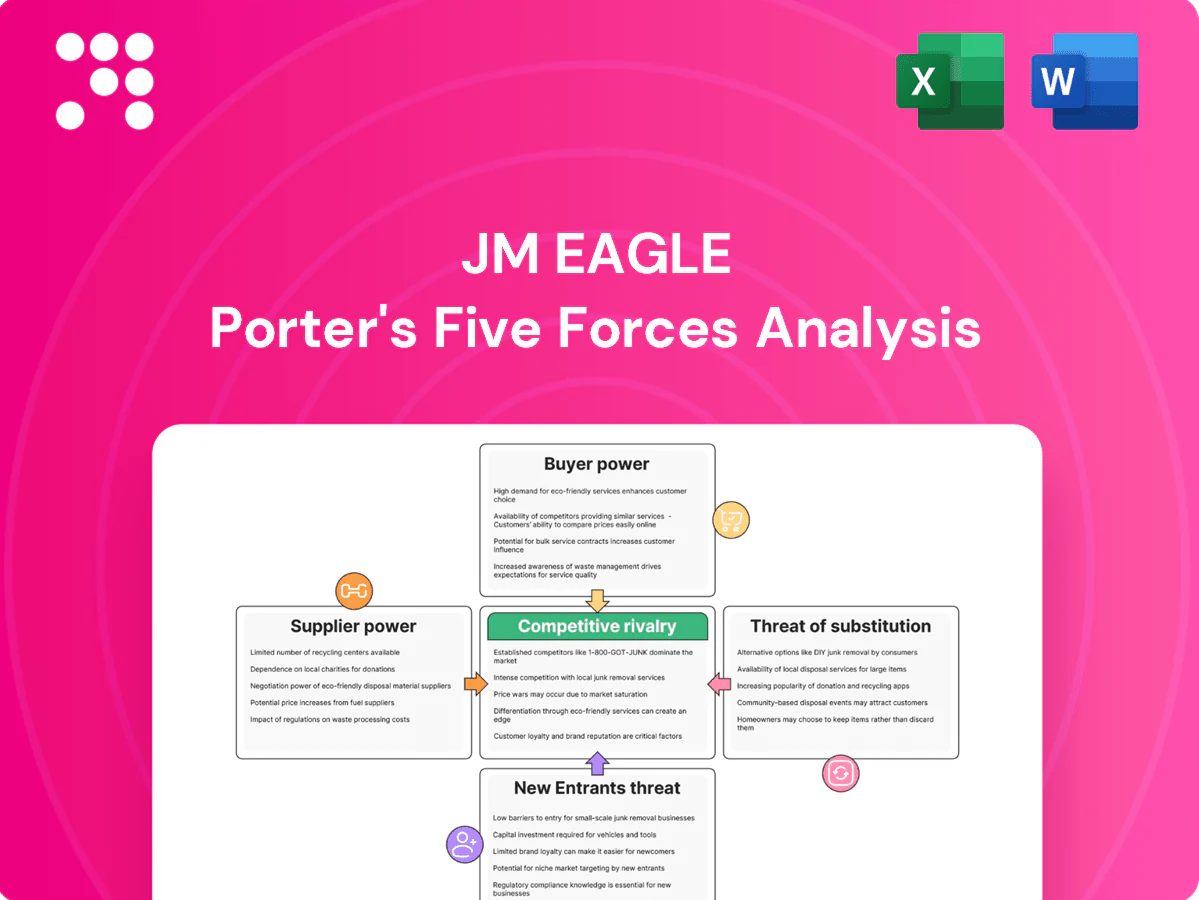

JM Eagle's Porter's Five Forces snapshot highlights supplier dynamics, buyer power, competitive rivalry, substitutes, and entry barriers shaping its PVC pipe dominance. This brief view teases strategic risks and market levers that matter to investors and managers. Ready for deeper, data-driven intelligence? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable implications.

Suppliers Bargaining Power

Petrochemical resin concentration

Primary inputs for JM Eagle are PVC and PE resins sourced from a relatively concentrated global set of producers including LyondellBasell, INEOS, SABIC, Sinopec and ExxonMobil, giving suppliers notable leverage in tight 2024 markets. JM Eagle mitigates risk through multi-sourcing and long-term contracts, but outages or force majeure events have in 2024 continued to cause rapid cost and availability shocks across the resin supply chain. Suppliers can therefore exert episodic pricing pressure despite JM Eagle’s contractual hedges.

Feedstock and energy volatility

Resin pricing for JM Eagle is closely linked to ethylene, chlorine and energy markets, creating cyclical input volatility that intensified in 2024 as upstream cost swings fed through the chain. Suppliers typically pass raw-material and fuel hikes to pipe makers, compressing margins during upcycles. Hedging and index-linked contracts used by manufacturers smooth some swings but do not eliminate exposure. During price spikes suppliers gain stronger bargaining leverage over producers.

Additives and compounders

Stabilizers, pigments and specialty additives for PVC are sourced from niche chemical suppliers whose products require qualification and performance certifications, creating meaningful switching friction for JM Eagle. Ongoing 2024 regulatory reviews (REACH, TSCA) have narrowed approved additive options in some markets, reducing supplier count. This situational scarcity gives niche suppliers episodic pricing power, particularly for certified flame-retardant or low-migration grades.

Qualification and compliance hurdles

Water and gas pipe products require AWWA, ASTM, NSF and other approvals tied to specific resin and compound formulations; re-qualifying new suppliers demands laboratory testing, field validation and lead time, which increases short-term dependence on approved vendors and creates lock-ins for critical SKUs, subtly strengthening supplier bargaining power.

- Approvals: AWWA/ASTM/NSF linked to formulations

- Re-qualification: testing, validation, lead time

- Effect: short-term dependence and higher supplier leverage

Logistics and regional supply

Resins and additives are bulky, so regional sourcing—especially near Gulf Coast chemistry hubs that hold roughly half of US petrochemical capacity—reduces freight and lead times. Railcar, port, or trucking bottlenecks can sharply tighten effective supply and raise supplier leverage. Proximity to Gulf hubs is an advantage for JM Eagle but can be a single-point systemic risk. Logistics constraints amplify supplier influence during disruptions, increasing spot premium and delay risk.

- Bulk freight sensitivity

- Gulf Coast ~50% petrochemical capacity

- Rail/port/truck bottlenecks raise supplier leverage

- Proximity = efficiency + concentration risk

Resin supplier concentration and Gulf Coast logistics amplify outage-driven pricing shocks

JM Eagle faces concentrated resin suppliers (LyondellBasell, INEOS, SABIC, Sinopec, ExxonMobil) giving episodic pricing leverage in tight 2024 markets; multi-sourcing and contracts reduce but do not eliminate outage-driven shocks. Additive approvals and AWWA/ASTM/NSF re-qualification create switching friction and short-term lock-in. Gulf Coast logistics concentration amplifies supplier power during disruptions.

| Metric | 2024 Fact |

|---|---|

| Major resin suppliers | LyondellBasell, INEOS, SABIC, Sinopec, ExxonMobil |

| Gulf Coast petrochemical share | ~50% |

What is included in the product

Customized Porter’s Five Forces analysis for JM Eagle that uncovers competitive drivers, supplier and buyer power, substitutes and entry risks, highlights disruptive threats and protective market dynamics for strategic use.

Concise one-sheet Porter's Five Forces for JM Eagle, mapping supplier, buyer, rivalry, substitutes and entry pressures with customizable scores and an instant radar chart—ready to drop into decks to pinpoint risks and guide mitigation.

Customers Bargaining Power

Large municipal and utility tenders

City water, sewer and gas utilities—among the 54,000+ community water systems reported by the US EPA—buy pipe at scale via formal competitive bids; large contracts commonly exceed $1 million, creating strong price pressure and allowing buyers to demand extended warranties and service terms, so this volume concentration materially elevates customer bargaining power for JM Eagle.

Standards-driven interchangeability

ASTM and AWWA standards (eg AWWA C900, ASTM D1784) make PVC and ductile-iron pipe dimensionally and performance-interchangeable across approved brands, lowering perceived differentiation. Buyers switch on price easily; approved vendor lists influence selections but rarely confer exclusivity. This dynamic sustains tight price competition and consistent margin pressure in municipal procurement.

Contractors and distributors leverage

Large contractors and national distributors aggregate demand across projects, negotiating rebates, delivery windows, and extended credit terms that compress supplier margins. Their ability to shift volume among PVC pipe suppliers and consolidate purchasing raises bargaining power and forces price and service competition. JM Eagle must match availability and minimize total cost-to-serve to retain share.

Total lifecycle cost focus

Buyers prioritize total lifecycle cost, weighing durability, installation speed, and corrosion resistance alongside unit price; PVC/PE advantages versus metals support value claims but similar lifecycle guarantees across suppliers have reduced visible differentiation. Widespread third-party certification (ASTM, ISO) compresses premium margins, enabling buyers to leverage parity to demand lower unit prices.

- Durability vs price

- Installation time savings

- Corrosion resistance parity

- Certification narrows differentiation

- Buyer leverage on unit price

Project timing sensitivity

Schedule certainty is critical in infrastructure builds; industry studies found about 40% of projects experienced schedule delays in 2024, driving contractors to favor suppliers with reliable capacity and logistics.

Buyers penalize delays through liquidated damages and rework costs, so suppliers meeting tight lead times can command modest premiums of 3–7% and win business despite higher prices.

Conversely, supply shortfalls rapidly erode pricing power and market share as purchasers shift to dependable alternatives.

- 40% of projects delayed in 2024

- Premiums for reliability: 3–7%

- Delays trigger liquidated damages and rework

- Dependable logistics = competitive advantage

Municipal bids prize low price; reliability earns 3–7% premium amid ~40% delays

Large municipal buyers (54,000+ US systems) buy by competitive bid with many contracts >$1M, creating strong price leverage. Standards (AWWA/ASTM) reduce differentiation, so buyers switch on price and demand warranties. Aggregators/contractors secure rebates and terms, compressing margins; 2024 saw ~40% project delays, giving reliable suppliers 3–7% premium.

| Metric | 2024 |

|---|---|

| Community systems | 54,000+ |

| Large contracts | >$1M |

| Project delays | ~40% |

| Premium for reliability | 3–7% |

Preview Before You Purchase

JM Eagle Porter's Five Forces Analysis

This preview is the exact JM Eagle Porter’s Five Forces Analysis you’ll receive immediately after purchase—no mockups, no placeholders. The file shown is fully formatted, professionally written, and ready for download and use the moment you buy. You’re seeing the final deliverable; purchase grants instant access to this identical document.

Go Beyond the Preview—Access the Full Strategic Report

JM Eagle's Porter's Five Forces snapshot highlights supplier dynamics, buyer power, competitive rivalry, substitutes, and entry barriers shaping its PVC pipe dominance. This brief view teases strategic risks and market levers that matter to investors and managers. Ready for deeper, data-driven intelligence? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable implications.

Suppliers Bargaining Power

Petrochemical resin concentration

Primary inputs for JM Eagle are PVC and PE resins sourced from a relatively concentrated global set of producers including LyondellBasell, INEOS, SABIC, Sinopec and ExxonMobil, giving suppliers notable leverage in tight 2024 markets. JM Eagle mitigates risk through multi-sourcing and long-term contracts, but outages or force majeure events have in 2024 continued to cause rapid cost and availability shocks across the resin supply chain. Suppliers can therefore exert episodic pricing pressure despite JM Eagle’s contractual hedges.

Feedstock and energy volatility

Resin pricing for JM Eagle is closely linked to ethylene, chlorine and energy markets, creating cyclical input volatility that intensified in 2024 as upstream cost swings fed through the chain. Suppliers typically pass raw-material and fuel hikes to pipe makers, compressing margins during upcycles. Hedging and index-linked contracts used by manufacturers smooth some swings but do not eliminate exposure. During price spikes suppliers gain stronger bargaining leverage over producers.

Additives and compounders

Stabilizers, pigments and specialty additives for PVC are sourced from niche chemical suppliers whose products require qualification and performance certifications, creating meaningful switching friction for JM Eagle. Ongoing 2024 regulatory reviews (REACH, TSCA) have narrowed approved additive options in some markets, reducing supplier count. This situational scarcity gives niche suppliers episodic pricing power, particularly for certified flame-retardant or low-migration grades.

Qualification and compliance hurdles

Water and gas pipe products require AWWA, ASTM, NSF and other approvals tied to specific resin and compound formulations; re-qualifying new suppliers demands laboratory testing, field validation and lead time, which increases short-term dependence on approved vendors and creates lock-ins for critical SKUs, subtly strengthening supplier bargaining power.

- Approvals: AWWA/ASTM/NSF linked to formulations

- Re-qualification: testing, validation, lead time

- Effect: short-term dependence and higher supplier leverage

Logistics and regional supply

Resins and additives are bulky, so regional sourcing—especially near Gulf Coast chemistry hubs that hold roughly half of US petrochemical capacity—reduces freight and lead times. Railcar, port, or trucking bottlenecks can sharply tighten effective supply and raise supplier leverage. Proximity to Gulf hubs is an advantage for JM Eagle but can be a single-point systemic risk. Logistics constraints amplify supplier influence during disruptions, increasing spot premium and delay risk.

- Bulk freight sensitivity

- Gulf Coast ~50% petrochemical capacity

- Rail/port/truck bottlenecks raise supplier leverage

- Proximity = efficiency + concentration risk

Resin supplier concentration and Gulf Coast logistics amplify outage-driven pricing shocks

JM Eagle faces concentrated resin suppliers (LyondellBasell, INEOS, SABIC, Sinopec, ExxonMobil) giving episodic pricing leverage in tight 2024 markets; multi-sourcing and contracts reduce but do not eliminate outage-driven shocks. Additive approvals and AWWA/ASTM/NSF re-qualification create switching friction and short-term lock-in. Gulf Coast logistics concentration amplifies supplier power during disruptions.

| Metric | 2024 Fact |

|---|---|

| Major resin suppliers | LyondellBasell, INEOS, SABIC, Sinopec, ExxonMobil |

| Gulf Coast petrochemical share | ~50% |

What is included in the product

Customized Porter’s Five Forces analysis for JM Eagle that uncovers competitive drivers, supplier and buyer power, substitutes and entry risks, highlights disruptive threats and protective market dynamics for strategic use.

Concise one-sheet Porter's Five Forces for JM Eagle, mapping supplier, buyer, rivalry, substitutes and entry pressures with customizable scores and an instant radar chart—ready to drop into decks to pinpoint risks and guide mitigation.

Customers Bargaining Power

Large municipal and utility tenders

City water, sewer and gas utilities—among the 54,000+ community water systems reported by the US EPA—buy pipe at scale via formal competitive bids; large contracts commonly exceed $1 million, creating strong price pressure and allowing buyers to demand extended warranties and service terms, so this volume concentration materially elevates customer bargaining power for JM Eagle.

Standards-driven interchangeability

ASTM and AWWA standards (eg AWWA C900, ASTM D1784) make PVC and ductile-iron pipe dimensionally and performance-interchangeable across approved brands, lowering perceived differentiation. Buyers switch on price easily; approved vendor lists influence selections but rarely confer exclusivity. This dynamic sustains tight price competition and consistent margin pressure in municipal procurement.

Contractors and distributors leverage

Large contractors and national distributors aggregate demand across projects, negotiating rebates, delivery windows, and extended credit terms that compress supplier margins. Their ability to shift volume among PVC pipe suppliers and consolidate purchasing raises bargaining power and forces price and service competition. JM Eagle must match availability and minimize total cost-to-serve to retain share.

Total lifecycle cost focus

Buyers prioritize total lifecycle cost, weighing durability, installation speed, and corrosion resistance alongside unit price; PVC/PE advantages versus metals support value claims but similar lifecycle guarantees across suppliers have reduced visible differentiation. Widespread third-party certification (ASTM, ISO) compresses premium margins, enabling buyers to leverage parity to demand lower unit prices.

- Durability vs price

- Installation time savings

- Corrosion resistance parity

- Certification narrows differentiation

- Buyer leverage on unit price

Project timing sensitivity

Schedule certainty is critical in infrastructure builds; industry studies found about 40% of projects experienced schedule delays in 2024, driving contractors to favor suppliers with reliable capacity and logistics.

Buyers penalize delays through liquidated damages and rework costs, so suppliers meeting tight lead times can command modest premiums of 3–7% and win business despite higher prices.

Conversely, supply shortfalls rapidly erode pricing power and market share as purchasers shift to dependable alternatives.

- 40% of projects delayed in 2024

- Premiums for reliability: 3–7%

- Delays trigger liquidated damages and rework

- Dependable logistics = competitive advantage

Municipal bids prize low price; reliability earns 3–7% premium amid ~40% delays

Large municipal buyers (54,000+ US systems) buy by competitive bid with many contracts >$1M, creating strong price leverage. Standards (AWWA/ASTM) reduce differentiation, so buyers switch on price and demand warranties. Aggregators/contractors secure rebates and terms, compressing margins; 2024 saw ~40% project delays, giving reliable suppliers 3–7% premium.

| Metric | 2024 |

|---|---|

| Community systems | 54,000+ |

| Large contracts | >$1M |

| Project delays | ~40% |

| Premium for reliability | 3–7% |

Preview Before You Purchase

JM Eagle Porter's Five Forces Analysis

This preview is the exact JM Eagle Porter’s Five Forces Analysis you’ll receive immediately after purchase—no mockups, no placeholders. The file shown is fully formatted, professionally written, and ready for download and use the moment you buy. You’re seeing the final deliverable; purchase grants instant access to this identical document.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

JM Eagle's Porter's Five Forces snapshot highlights supplier dynamics, buyer power, competitive rivalry, substitutes, and entry barriers shaping its PVC pipe dominance. This brief view teases strategic risks and market levers that matter to investors and managers. Ready for deeper, data-driven intelligence? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable implications.

Suppliers Bargaining Power

Petrochemical resin concentration

Primary inputs for JM Eagle are PVC and PE resins sourced from a relatively concentrated global set of producers including LyondellBasell, INEOS, SABIC, Sinopec and ExxonMobil, giving suppliers notable leverage in tight 2024 markets. JM Eagle mitigates risk through multi-sourcing and long-term contracts, but outages or force majeure events have in 2024 continued to cause rapid cost and availability shocks across the resin supply chain. Suppliers can therefore exert episodic pricing pressure despite JM Eagle’s contractual hedges.

Feedstock and energy volatility

Resin pricing for JM Eagle is closely linked to ethylene, chlorine and energy markets, creating cyclical input volatility that intensified in 2024 as upstream cost swings fed through the chain. Suppliers typically pass raw-material and fuel hikes to pipe makers, compressing margins during upcycles. Hedging and index-linked contracts used by manufacturers smooth some swings but do not eliminate exposure. During price spikes suppliers gain stronger bargaining leverage over producers.

Additives and compounders

Stabilizers, pigments and specialty additives for PVC are sourced from niche chemical suppliers whose products require qualification and performance certifications, creating meaningful switching friction for JM Eagle. Ongoing 2024 regulatory reviews (REACH, TSCA) have narrowed approved additive options in some markets, reducing supplier count. This situational scarcity gives niche suppliers episodic pricing power, particularly for certified flame-retardant or low-migration grades.

Qualification and compliance hurdles

Water and gas pipe products require AWWA, ASTM, NSF and other approvals tied to specific resin and compound formulations; re-qualifying new suppliers demands laboratory testing, field validation and lead time, which increases short-term dependence on approved vendors and creates lock-ins for critical SKUs, subtly strengthening supplier bargaining power.

- Approvals: AWWA/ASTM/NSF linked to formulations

- Re-qualification: testing, validation, lead time

- Effect: short-term dependence and higher supplier leverage

Logistics and regional supply

Resins and additives are bulky, so regional sourcing—especially near Gulf Coast chemistry hubs that hold roughly half of US petrochemical capacity—reduces freight and lead times. Railcar, port, or trucking bottlenecks can sharply tighten effective supply and raise supplier leverage. Proximity to Gulf hubs is an advantage for JM Eagle but can be a single-point systemic risk. Logistics constraints amplify supplier influence during disruptions, increasing spot premium and delay risk.

- Bulk freight sensitivity

- Gulf Coast ~50% petrochemical capacity

- Rail/port/truck bottlenecks raise supplier leverage

- Proximity = efficiency + concentration risk

Resin supplier concentration and Gulf Coast logistics amplify outage-driven pricing shocks

JM Eagle faces concentrated resin suppliers (LyondellBasell, INEOS, SABIC, Sinopec, ExxonMobil) giving episodic pricing leverage in tight 2024 markets; multi-sourcing and contracts reduce but do not eliminate outage-driven shocks. Additive approvals and AWWA/ASTM/NSF re-qualification create switching friction and short-term lock-in. Gulf Coast logistics concentration amplifies supplier power during disruptions.

| Metric | 2024 Fact |

|---|---|

| Major resin suppliers | LyondellBasell, INEOS, SABIC, Sinopec, ExxonMobil |

| Gulf Coast petrochemical share | ~50% |

What is included in the product

Customized Porter’s Five Forces analysis for JM Eagle that uncovers competitive drivers, supplier and buyer power, substitutes and entry risks, highlights disruptive threats and protective market dynamics for strategic use.

Concise one-sheet Porter's Five Forces for JM Eagle, mapping supplier, buyer, rivalry, substitutes and entry pressures with customizable scores and an instant radar chart—ready to drop into decks to pinpoint risks and guide mitigation.

Customers Bargaining Power

Large municipal and utility tenders

City water, sewer and gas utilities—among the 54,000+ community water systems reported by the US EPA—buy pipe at scale via formal competitive bids; large contracts commonly exceed $1 million, creating strong price pressure and allowing buyers to demand extended warranties and service terms, so this volume concentration materially elevates customer bargaining power for JM Eagle.

Standards-driven interchangeability

ASTM and AWWA standards (eg AWWA C900, ASTM D1784) make PVC and ductile-iron pipe dimensionally and performance-interchangeable across approved brands, lowering perceived differentiation. Buyers switch on price easily; approved vendor lists influence selections but rarely confer exclusivity. This dynamic sustains tight price competition and consistent margin pressure in municipal procurement.

Contractors and distributors leverage

Large contractors and national distributors aggregate demand across projects, negotiating rebates, delivery windows, and extended credit terms that compress supplier margins. Their ability to shift volume among PVC pipe suppliers and consolidate purchasing raises bargaining power and forces price and service competition. JM Eagle must match availability and minimize total cost-to-serve to retain share.

Total lifecycle cost focus

Buyers prioritize total lifecycle cost, weighing durability, installation speed, and corrosion resistance alongside unit price; PVC/PE advantages versus metals support value claims but similar lifecycle guarantees across suppliers have reduced visible differentiation. Widespread third-party certification (ASTM, ISO) compresses premium margins, enabling buyers to leverage parity to demand lower unit prices.

- Durability vs price

- Installation time savings

- Corrosion resistance parity

- Certification narrows differentiation

- Buyer leverage on unit price

Project timing sensitivity

Schedule certainty is critical in infrastructure builds; industry studies found about 40% of projects experienced schedule delays in 2024, driving contractors to favor suppliers with reliable capacity and logistics.

Buyers penalize delays through liquidated damages and rework costs, so suppliers meeting tight lead times can command modest premiums of 3–7% and win business despite higher prices.

Conversely, supply shortfalls rapidly erode pricing power and market share as purchasers shift to dependable alternatives.

- 40% of projects delayed in 2024

- Premiums for reliability: 3–7%

- Delays trigger liquidated damages and rework

- Dependable logistics = competitive advantage

Municipal bids prize low price; reliability earns 3–7% premium amid ~40% delays

Large municipal buyers (54,000+ US systems) buy by competitive bid with many contracts >$1M, creating strong price leverage. Standards (AWWA/ASTM) reduce differentiation, so buyers switch on price and demand warranties. Aggregators/contractors secure rebates and terms, compressing margins; 2024 saw ~40% project delays, giving reliable suppliers 3–7% premium.

| Metric | 2024 |

|---|---|

| Community systems | 54,000+ |

| Large contracts | >$1M |

| Project delays | ~40% |

| Premium for reliability | 3–7% |

Preview Before You Purchase

JM Eagle Porter's Five Forces Analysis

This preview is the exact JM Eagle Porter’s Five Forces Analysis you’ll receive immediately after purchase—no mockups, no placeholders. The file shown is fully formatted, professionally written, and ready for download and use the moment you buy. You’re seeing the final deliverable; purchase grants instant access to this identical document.