Johnson & Johnson Boston Consulting Group Matrix

Unlock Strategic Clarity

Johnson & Johnson sits at an interesting crossroads — a mix of global powerhouses, niche healers, and a few units that need hard choices. Our quick read shows where market share and growth collide, but it’s just the surface. Buy the full BCG Matrix to get quadrant-by-quadrant placement, data-backed recommendations, and an executable plan. Get the complete Word + Excel package and move from insight to action fast.

Stars

Darzalex (multiple myeloma)

Darzalex is the leader in the fast-growing multiple myeloma segment with strong clinical pull, reporting roughly $7.9B in 2024 sales and high-teens percentage year-over-year growth as usage deepens across lines of therapy. It keeps taking share as frontline and combination regimens expand, but growth remains capital-intensive with elevated reinvestment needs. Hold the line: sustained reinvestment can compound Darzalex into a powerhouse cash engine for J&J.

Tremfya (immunology)

Tremfya is gaining ground in psoriasis and psoriatic arthritis with clean Phase 3 and real‑world tolerability and simple dosing, helping it capture significant switch share; 2024 global sales reached about $4.1 billion while the psoriasis biologics category is ~22 billion USD and still expanding. Marketing and access spend remain justified—continued investment to fuel uptake is critical to cement leadership before new rivals enter.

Carvykti (CAR-T, myeloma)

Carvykti sits in the Stars quadrant as explosive demand drives rapid uptake: CARTITUDE-1 showed an overall response rate ~98% with deep, durable remissions, attracting clinicians and payers and creating a market accelerating into 2024. Limited direct CAR-T peers in myeloma and strong real-world adoption support defendable share if capacity scales. Johnson & Johnson should invest heavily in manufacturing and cold-chain logistics to unlock the full commercial curve. Capacity ramping and site activation are the key value levers.

Opsumit & Uptravi (pulmonary hypertension)

Opsumit and Uptravi sit in a durable, expanding PAH niche where prevalence is estimated at 15–50 cases per million and incidence 2–7 per million annually, supporting steady patient-level demand in 2024. Strong physician loyalty and real-world outcome data have sustained market share gains and adherence. The franchise’s breadth across prostacyclin and endothelin mechanisms plus ongoing lifecycle and access programs continue to drive uptake.

- Durable niche: PAH prevalence 15–50/million (2024)

- Defensive factors: physician loyalty, real-world outcomes

- Breadth: multiple lines/mechanisms (prostacyclin, endothelin)

- Support: lifecycle management and access programs maintaining growth

Biosense Webster (AFib ablation)

Biosense Webster is the category leader in electrophysiology mapping and AFib ablation within Johnson & Johnson, benefiting from secular tailwinds as AFib affects ~6 million Americans and an estimated 59 million people globally; procedure volumes and tech adoption have continued upward into 2024. High switching costs, strong ecosystem integration, and entrenched training programs protect share; continued investment in innovation and operator training widens the moat.

- Market position: leader in EP mapping and ablation

- Demand drivers: AFib prevalence ~6M US, ~59M global

- Growth: rising procedure volumes and adoption in 2024

- Moat: ecosystem, training, high switching costs; back R&D/training

7.9B, ~98% ORR, AFib 6M

Stars: Darzalex $7.9B (2024) with high‑teens growth; Tremfya $4.1B (2024) capturing psoriasis share; Carvykti ~98% ORR driving rapid CAR-T uptake; Biosense Webster benefits from AFib prevalence ~6M US/59M global; Opsumit/Uptravi serve PAH niche (15–50/million).

| Asset | 2024/$ | Key metric |

|---|---|---|

| Darzalex | 7.9B | High‑teens % growth |

| Tremfya | 4.1B | Large psoriasis share |

| Carvykti | — | ~98% ORR |

| Biosense | — | AFib 6M US/59M global |

What is included in the product

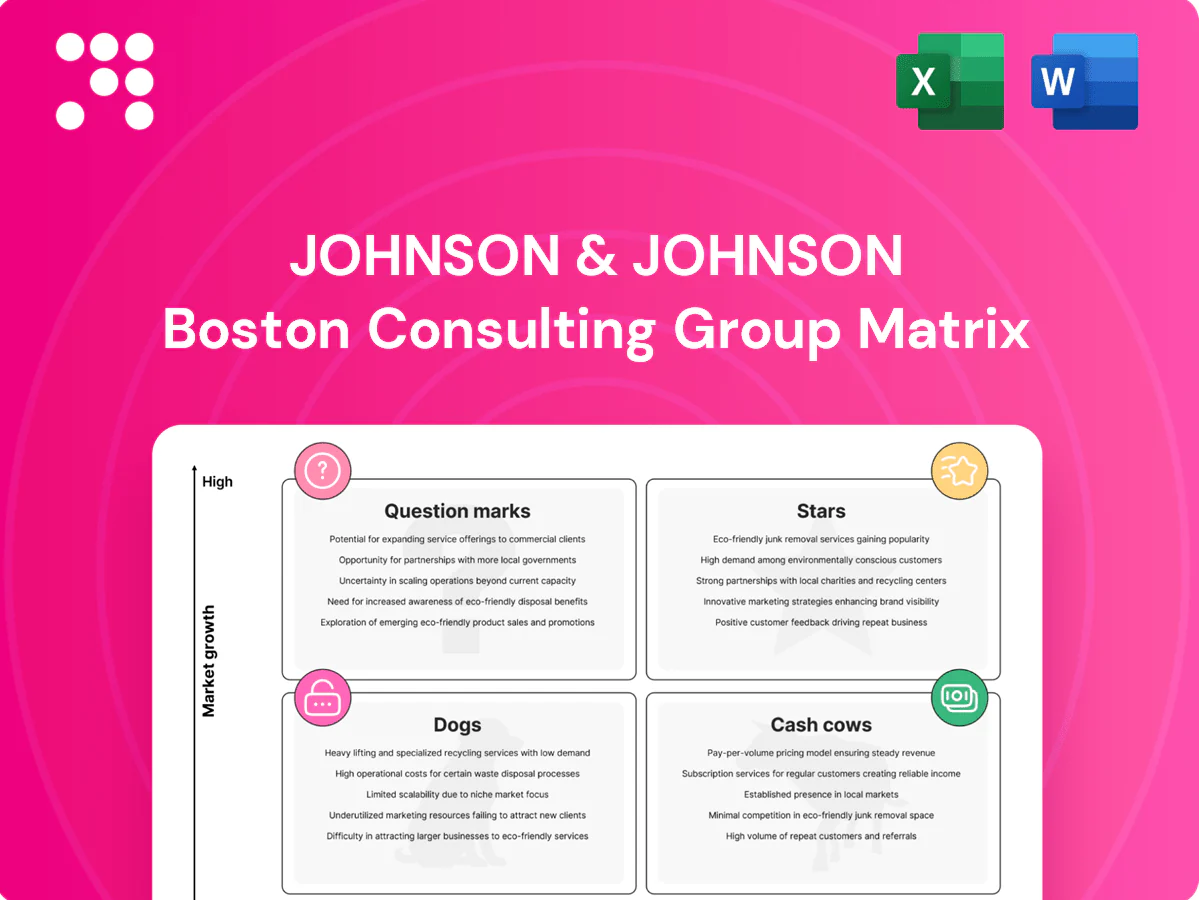

BCG analysis of Johnson & Johnson products: stars, cash cows, question marks and dogs with investment, divestment and risk guidance.

One-page Johnson & Johnson BCG Matrix highlighting business pain points for quick C-level decisions

Cash Cows

Stelara (immunology)

Stelara (ustekinumab) sits on a massive, high-margin base—generating roughly $8 billion in 2023—and dominates a mature immunology segment. Growth is moderating to low-single-digit rates as LOE dynamics and regional competitive entry approach. It continues to throw off substantial cash with modest promotion, so J&J can milk near-term cashflows while steering patients toward next-generation assets.

Xarelto (anticoagulant, U.S.)

Xarelto remains a large-scale, high-share U.S. anticoagulant with estimated 2024 U.S. sales around $3.4 billion and a sticky script base despite DOAC competition. Promotion needs are lower as patient persistence and refill rates keep cash conversion strong; gross-to-net dynamics remain favorable. Focus on optimizing contracting, rebates and defending cardiology and primary-care prescriber cohorts to protect margin and share.

Ethicon Surgical (stapling & energy)

Ethicon Surgical (stapling & energy) is J&J’s core surgical toolkit, leveraging entrenched hospital relationships and long procurement contracts. The stapling and energy markets are mature, procurement-driven and predictably cyclical. Scale and manufacturing efficiency generate steady cash flow for Medical Devices. Ongoing incremental product innovation and robust field support sustain high utilization and repeat purchasing.

DePuy Synthes (hips, knees, trauma)

DePuy Synthes leverages a significant installed base and strong surgeon loyalty across hips, knees and trauma, underpinning steady demand; J&J Medical Devices reported roughly $24.6 billion in 2024, with orthopedics a major contributor. Mix shifts and pricing pressure are manageable given scale and distribution reach, keeping margins resilient. Cash flow remains reliable despite modest procedure growth; focus is on ops excellence and selective premiumization to sustain returns.

- Installed base: durable market position

- 2024 Med Devices rev: ~$24.6B

- Scale offsets pricing/mix pressure

- Reliable cash flow with modest volume growth

- Strategy: ops excellence + targeted premiumization

ACUVUE (vision care)

ACUVUE is a cash cow for Johnson & Johnson, holding a leading share in the global soft contact lens category with strong brand equity and deep retail and professional channels that keep churn low; marketing spend is moderate relative to margins. Tight inventory management, incremental material and wear-time innovations, and steady distribution pricing maximize free cash flow.

- High-share brand

- Low churn via channel depth

- Moderate marketing intensity

- Keep supply tight

- Innovate edges

- Let cash roll

High-margin biologics, sticky Rx cash and $24.6B med-device scale fund R&D

Stelara generates very high-margin cash from a mature immunology base, allowing J&J to fund next-gen programs while growth moderates.

Xarelto (~$3.4B U.S. 2024) delivers sticky prescription cash with low promo intensity and focus on contracting to defend margins.

Ethicon/DePuy within Med Devices (2024 rev ~24.6B) provide steady, procurement-driven cash via installed bases and scale.

| Product | 2024 sales | Role |

|---|---|---|

| Stelara | high-$bn | Cash cow |

| Xarelto | $3.4B (US) | Cash cow |

| Med Devices | $24.6B | Cash generator |

| ACUVUE | major revenue | Stable cash |

Delivered as Shown

Johnson & Johnson BCG Matrix

The Johnson & Johnson BCG Matrix you're previewing is the exact file you'll receive after purchase. No watermarks, no placeholders—just the fully formatted strategic matrix tailored to J&J's portfolio. It’s ready to edit, print, or present straight away, backed by clear market insights and professional layout. Buy once, download instantly—no surprises, just actionable clarity.

Unlock Strategic Clarity

Johnson & Johnson sits at an interesting crossroads — a mix of global powerhouses, niche healers, and a few units that need hard choices. Our quick read shows where market share and growth collide, but it’s just the surface. Buy the full BCG Matrix to get quadrant-by-quadrant placement, data-backed recommendations, and an executable plan. Get the complete Word + Excel package and move from insight to action fast.

Stars

Darzalex (multiple myeloma)

Darzalex is the leader in the fast-growing multiple myeloma segment with strong clinical pull, reporting roughly $7.9B in 2024 sales and high-teens percentage year-over-year growth as usage deepens across lines of therapy. It keeps taking share as frontline and combination regimens expand, but growth remains capital-intensive with elevated reinvestment needs. Hold the line: sustained reinvestment can compound Darzalex into a powerhouse cash engine for J&J.

Tremfya (immunology)

Tremfya is gaining ground in psoriasis and psoriatic arthritis with clean Phase 3 and real‑world tolerability and simple dosing, helping it capture significant switch share; 2024 global sales reached about $4.1 billion while the psoriasis biologics category is ~22 billion USD and still expanding. Marketing and access spend remain justified—continued investment to fuel uptake is critical to cement leadership before new rivals enter.

Carvykti (CAR-T, myeloma)

Carvykti sits in the Stars quadrant as explosive demand drives rapid uptake: CARTITUDE-1 showed an overall response rate ~98% with deep, durable remissions, attracting clinicians and payers and creating a market accelerating into 2024. Limited direct CAR-T peers in myeloma and strong real-world adoption support defendable share if capacity scales. Johnson & Johnson should invest heavily in manufacturing and cold-chain logistics to unlock the full commercial curve. Capacity ramping and site activation are the key value levers.

Opsumit & Uptravi (pulmonary hypertension)

Opsumit and Uptravi sit in a durable, expanding PAH niche where prevalence is estimated at 15–50 cases per million and incidence 2–7 per million annually, supporting steady patient-level demand in 2024. Strong physician loyalty and real-world outcome data have sustained market share gains and adherence. The franchise’s breadth across prostacyclin and endothelin mechanisms plus ongoing lifecycle and access programs continue to drive uptake.

- Durable niche: PAH prevalence 15–50/million (2024)

- Defensive factors: physician loyalty, real-world outcomes

- Breadth: multiple lines/mechanisms (prostacyclin, endothelin)

- Support: lifecycle management and access programs maintaining growth

Biosense Webster (AFib ablation)

Biosense Webster is the category leader in electrophysiology mapping and AFib ablation within Johnson & Johnson, benefiting from secular tailwinds as AFib affects ~6 million Americans and an estimated 59 million people globally; procedure volumes and tech adoption have continued upward into 2024. High switching costs, strong ecosystem integration, and entrenched training programs protect share; continued investment in innovation and operator training widens the moat.

- Market position: leader in EP mapping and ablation

- Demand drivers: AFib prevalence ~6M US, ~59M global

- Growth: rising procedure volumes and adoption in 2024

- Moat: ecosystem, training, high switching costs; back R&D/training

7.9B, ~98% ORR, AFib 6M

Stars: Darzalex $7.9B (2024) with high‑teens growth; Tremfya $4.1B (2024) capturing psoriasis share; Carvykti ~98% ORR driving rapid CAR-T uptake; Biosense Webster benefits from AFib prevalence ~6M US/59M global; Opsumit/Uptravi serve PAH niche (15–50/million).

| Asset | 2024/$ | Key metric |

|---|---|---|

| Darzalex | 7.9B | High‑teens % growth |

| Tremfya | 4.1B | Large psoriasis share |

| Carvykti | — | ~98% ORR |

| Biosense | — | AFib 6M US/59M global |

What is included in the product

BCG analysis of Johnson & Johnson products: stars, cash cows, question marks and dogs with investment, divestment and risk guidance.

One-page Johnson & Johnson BCG Matrix highlighting business pain points for quick C-level decisions

Cash Cows

Stelara (immunology)

Stelara (ustekinumab) sits on a massive, high-margin base—generating roughly $8 billion in 2023—and dominates a mature immunology segment. Growth is moderating to low-single-digit rates as LOE dynamics and regional competitive entry approach. It continues to throw off substantial cash with modest promotion, so J&J can milk near-term cashflows while steering patients toward next-generation assets.

Xarelto (anticoagulant, U.S.)

Xarelto remains a large-scale, high-share U.S. anticoagulant with estimated 2024 U.S. sales around $3.4 billion and a sticky script base despite DOAC competition. Promotion needs are lower as patient persistence and refill rates keep cash conversion strong; gross-to-net dynamics remain favorable. Focus on optimizing contracting, rebates and defending cardiology and primary-care prescriber cohorts to protect margin and share.

Ethicon Surgical (stapling & energy)

Ethicon Surgical (stapling & energy) is J&J’s core surgical toolkit, leveraging entrenched hospital relationships and long procurement contracts. The stapling and energy markets are mature, procurement-driven and predictably cyclical. Scale and manufacturing efficiency generate steady cash flow for Medical Devices. Ongoing incremental product innovation and robust field support sustain high utilization and repeat purchasing.

DePuy Synthes (hips, knees, trauma)

DePuy Synthes leverages a significant installed base and strong surgeon loyalty across hips, knees and trauma, underpinning steady demand; J&J Medical Devices reported roughly $24.6 billion in 2024, with orthopedics a major contributor. Mix shifts and pricing pressure are manageable given scale and distribution reach, keeping margins resilient. Cash flow remains reliable despite modest procedure growth; focus is on ops excellence and selective premiumization to sustain returns.

- Installed base: durable market position

- 2024 Med Devices rev: ~$24.6B

- Scale offsets pricing/mix pressure

- Reliable cash flow with modest volume growth

- Strategy: ops excellence + targeted premiumization

ACUVUE (vision care)

ACUVUE is a cash cow for Johnson & Johnson, holding a leading share in the global soft contact lens category with strong brand equity and deep retail and professional channels that keep churn low; marketing spend is moderate relative to margins. Tight inventory management, incremental material and wear-time innovations, and steady distribution pricing maximize free cash flow.

- High-share brand

- Low churn via channel depth

- Moderate marketing intensity

- Keep supply tight

- Innovate edges

- Let cash roll

High-margin biologics, sticky Rx cash and $24.6B med-device scale fund R&D

Stelara generates very high-margin cash from a mature immunology base, allowing J&J to fund next-gen programs while growth moderates.

Xarelto (~$3.4B U.S. 2024) delivers sticky prescription cash with low promo intensity and focus on contracting to defend margins.

Ethicon/DePuy within Med Devices (2024 rev ~24.6B) provide steady, procurement-driven cash via installed bases and scale.

| Product | 2024 sales | Role |

|---|---|---|

| Stelara | high-$bn | Cash cow |

| Xarelto | $3.4B (US) | Cash cow |

| Med Devices | $24.6B | Cash generator |

| ACUVUE | major revenue | Stable cash |

Delivered as Shown

Johnson & Johnson BCG Matrix

The Johnson & Johnson BCG Matrix you're previewing is the exact file you'll receive after purchase. No watermarks, no placeholders—just the fully formatted strategic matrix tailored to J&J's portfolio. It’s ready to edit, print, or present straight away, backed by clear market insights and professional layout. Buy once, download instantly—no surprises, just actionable clarity.

Description

Unlock Strategic Clarity

Johnson & Johnson sits at an interesting crossroads — a mix of global powerhouses, niche healers, and a few units that need hard choices. Our quick read shows where market share and growth collide, but it’s just the surface. Buy the full BCG Matrix to get quadrant-by-quadrant placement, data-backed recommendations, and an executable plan. Get the complete Word + Excel package and move from insight to action fast.

Stars

Darzalex (multiple myeloma)

Darzalex is the leader in the fast-growing multiple myeloma segment with strong clinical pull, reporting roughly $7.9B in 2024 sales and high-teens percentage year-over-year growth as usage deepens across lines of therapy. It keeps taking share as frontline and combination regimens expand, but growth remains capital-intensive with elevated reinvestment needs. Hold the line: sustained reinvestment can compound Darzalex into a powerhouse cash engine for J&J.

Tremfya (immunology)

Tremfya is gaining ground in psoriasis and psoriatic arthritis with clean Phase 3 and real‑world tolerability and simple dosing, helping it capture significant switch share; 2024 global sales reached about $4.1 billion while the psoriasis biologics category is ~22 billion USD and still expanding. Marketing and access spend remain justified—continued investment to fuel uptake is critical to cement leadership before new rivals enter.

Carvykti (CAR-T, myeloma)

Carvykti sits in the Stars quadrant as explosive demand drives rapid uptake: CARTITUDE-1 showed an overall response rate ~98% with deep, durable remissions, attracting clinicians and payers and creating a market accelerating into 2024. Limited direct CAR-T peers in myeloma and strong real-world adoption support defendable share if capacity scales. Johnson & Johnson should invest heavily in manufacturing and cold-chain logistics to unlock the full commercial curve. Capacity ramping and site activation are the key value levers.

Opsumit & Uptravi (pulmonary hypertension)

Opsumit and Uptravi sit in a durable, expanding PAH niche where prevalence is estimated at 15–50 cases per million and incidence 2–7 per million annually, supporting steady patient-level demand in 2024. Strong physician loyalty and real-world outcome data have sustained market share gains and adherence. The franchise’s breadth across prostacyclin and endothelin mechanisms plus ongoing lifecycle and access programs continue to drive uptake.

- Durable niche: PAH prevalence 15–50/million (2024)

- Defensive factors: physician loyalty, real-world outcomes

- Breadth: multiple lines/mechanisms (prostacyclin, endothelin)

- Support: lifecycle management and access programs maintaining growth

Biosense Webster (AFib ablation)

Biosense Webster is the category leader in electrophysiology mapping and AFib ablation within Johnson & Johnson, benefiting from secular tailwinds as AFib affects ~6 million Americans and an estimated 59 million people globally; procedure volumes and tech adoption have continued upward into 2024. High switching costs, strong ecosystem integration, and entrenched training programs protect share; continued investment in innovation and operator training widens the moat.

- Market position: leader in EP mapping and ablation

- Demand drivers: AFib prevalence ~6M US, ~59M global

- Growth: rising procedure volumes and adoption in 2024

- Moat: ecosystem, training, high switching costs; back R&D/training

7.9B, ~98% ORR, AFib 6M

Stars: Darzalex $7.9B (2024) with high‑teens growth; Tremfya $4.1B (2024) capturing psoriasis share; Carvykti ~98% ORR driving rapid CAR-T uptake; Biosense Webster benefits from AFib prevalence ~6M US/59M global; Opsumit/Uptravi serve PAH niche (15–50/million).

| Asset | 2024/$ | Key metric |

|---|---|---|

| Darzalex | 7.9B | High‑teens % growth |

| Tremfya | 4.1B | Large psoriasis share |

| Carvykti | — | ~98% ORR |

| Biosense | — | AFib 6M US/59M global |

What is included in the product

BCG analysis of Johnson & Johnson products: stars, cash cows, question marks and dogs with investment, divestment and risk guidance.

One-page Johnson & Johnson BCG Matrix highlighting business pain points for quick C-level decisions

Cash Cows

Stelara (immunology)

Stelara (ustekinumab) sits on a massive, high-margin base—generating roughly $8 billion in 2023—and dominates a mature immunology segment. Growth is moderating to low-single-digit rates as LOE dynamics and regional competitive entry approach. It continues to throw off substantial cash with modest promotion, so J&J can milk near-term cashflows while steering patients toward next-generation assets.

Xarelto (anticoagulant, U.S.)

Xarelto remains a large-scale, high-share U.S. anticoagulant with estimated 2024 U.S. sales around $3.4 billion and a sticky script base despite DOAC competition. Promotion needs are lower as patient persistence and refill rates keep cash conversion strong; gross-to-net dynamics remain favorable. Focus on optimizing contracting, rebates and defending cardiology and primary-care prescriber cohorts to protect margin and share.

Ethicon Surgical (stapling & energy)

Ethicon Surgical (stapling & energy) is J&J’s core surgical toolkit, leveraging entrenched hospital relationships and long procurement contracts. The stapling and energy markets are mature, procurement-driven and predictably cyclical. Scale and manufacturing efficiency generate steady cash flow for Medical Devices. Ongoing incremental product innovation and robust field support sustain high utilization and repeat purchasing.

DePuy Synthes (hips, knees, trauma)

DePuy Synthes leverages a significant installed base and strong surgeon loyalty across hips, knees and trauma, underpinning steady demand; J&J Medical Devices reported roughly $24.6 billion in 2024, with orthopedics a major contributor. Mix shifts and pricing pressure are manageable given scale and distribution reach, keeping margins resilient. Cash flow remains reliable despite modest procedure growth; focus is on ops excellence and selective premiumization to sustain returns.

- Installed base: durable market position

- 2024 Med Devices rev: ~$24.6B

- Scale offsets pricing/mix pressure

- Reliable cash flow with modest volume growth

- Strategy: ops excellence + targeted premiumization

ACUVUE (vision care)

ACUVUE is a cash cow for Johnson & Johnson, holding a leading share in the global soft contact lens category with strong brand equity and deep retail and professional channels that keep churn low; marketing spend is moderate relative to margins. Tight inventory management, incremental material and wear-time innovations, and steady distribution pricing maximize free cash flow.

- High-share brand

- Low churn via channel depth

- Moderate marketing intensity

- Keep supply tight

- Innovate edges

- Let cash roll

High-margin biologics, sticky Rx cash and $24.6B med-device scale fund R&D

Stelara generates very high-margin cash from a mature immunology base, allowing J&J to fund next-gen programs while growth moderates.

Xarelto (~$3.4B U.S. 2024) delivers sticky prescription cash with low promo intensity and focus on contracting to defend margins.

Ethicon/DePuy within Med Devices (2024 rev ~24.6B) provide steady, procurement-driven cash via installed bases and scale.

| Product | 2024 sales | Role |

|---|---|---|

| Stelara | high-$bn | Cash cow |

| Xarelto | $3.4B (US) | Cash cow |

| Med Devices | $24.6B | Cash generator |

| ACUVUE | major revenue | Stable cash |

Delivered as Shown

Johnson & Johnson BCG Matrix

The Johnson & Johnson BCG Matrix you're previewing is the exact file you'll receive after purchase. No watermarks, no placeholders—just the fully formatted strategic matrix tailored to J&J's portfolio. It’s ready to edit, print, or present straight away, backed by clear market insights and professional layout. Buy once, download instantly—no surprises, just actionable clarity.