Johnson Controls International Porter's Five Forces Analysis

From Overview to Strategy Blueprint

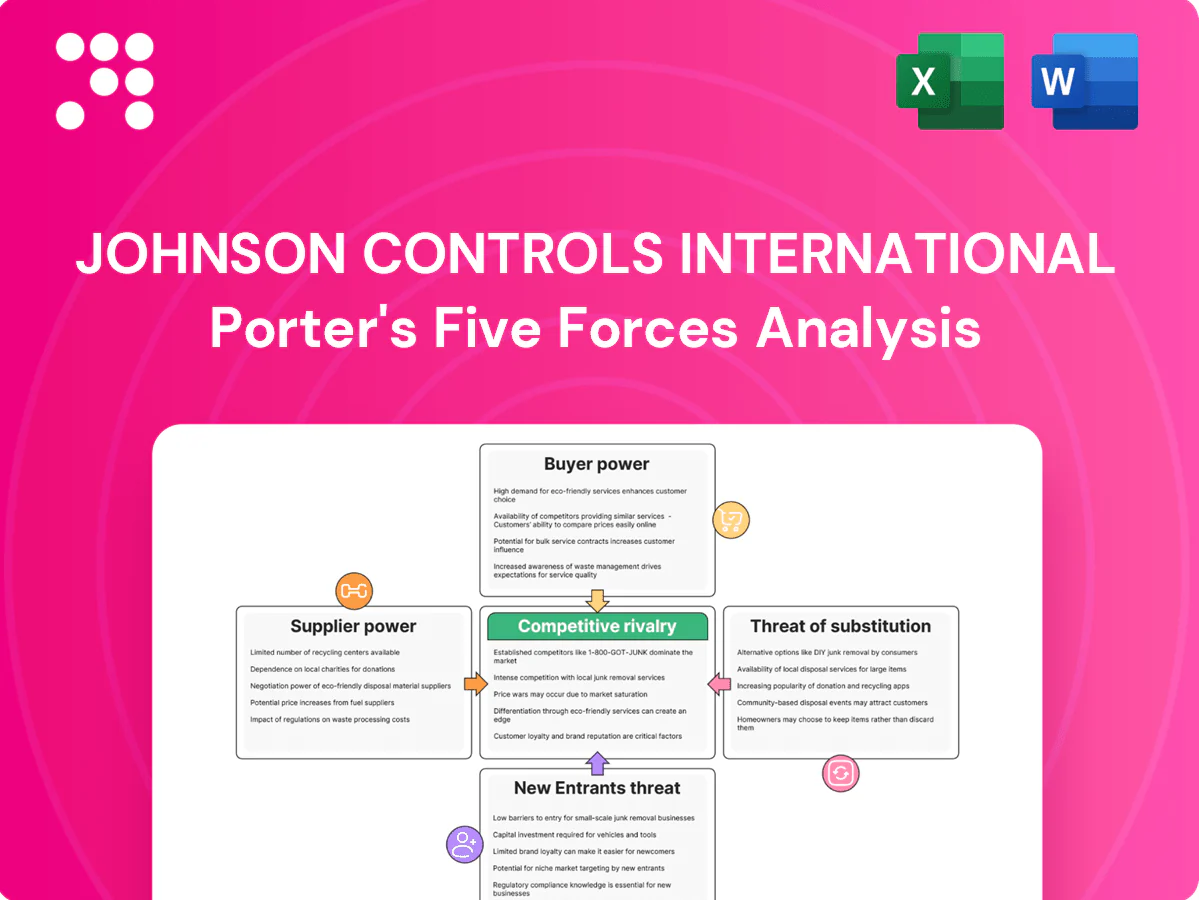

Johnson Controls International faces intense rivalry in building systems and automotive segments, with moderate supplier leverage and evolving substitute threats from smart-building software and EV tech; buyer power varies by large institutional contracts versus retail channels. Regulatory and technology shifts heighten entry barriers yet attract niche innovators. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Johnson Controls International.

Suppliers Bargaining Power

Concentrated critical components

Compressors, specialty sensors and control semiconductors are sourced from a limited set of Tier-1 suppliers, creating hold-up risk; semiconductor shortages peaked in 2021–22 and allocation issues linger into 2024. Lead-time spikes and allocation during shortages can delay projects and raise costs. JCI mitigates via dual-sourcing, approved vendor lists and design-for-substitution. Bespoke HVAC, fire and security specs retain supplier leverage in niches.

Materials and input volatility

Volatility in steel, copper, aluminum and electronics drove 2023–24 commodity swings often in the 10–30% range, pressuring equipment margins at Johnson Controls as suppliers pushed through surcharges faster than JCI could reprice bids. Hedging and index-linked contracts reduce exposure, but typical project cycles of 18–36 months create timing gaps that erode margins. Episodic global freight and logistics disruptions in 2023–24 added short-term cost spikes.

Technology roadmaps dependence

Controls at Johnson Controls depend on vendor-specified chipsets, connectivity modules and cybersecurity stacks, tying designs to third-party roadmaps; firmware lifecycles typically span 3–5 years, forcing periodic redesigns and R&D spend spikes. Strategic partnerships (vendor lock-in) secure early access but constrain architecture choices. Compliance to IEC 62443 and UL 2900 in 2024 further raises supplier influence and certification costs.

Switching costs in qualified components

Fire and life-safety systems require certified, tested parts, and requalification of components typically adds 6–12 months and can cost tens of thousands per part, so approved changes ripple through listings and warranties. That dependency gives incumbent suppliers pricing and priority leverage, while Johnson Controls mitigates risk with modular platforms and prequalified alternates to shorten qualification cycles.

- Requalification lag: 6–12 months

- Typical requal cost: tens of thousands per part

- Supplier leverage: pricing & priority

- JCI response: modular platforms, prequalified alternates

Long-term contracts and co-innovation

Long-term contracts and co-innovation with suppliers — backed by JCI’s global scale (operations in 150+ countries, ~100,000 employees in 2024) — use volume commitments and joint development to reduce supply risk at peak demand; suppliers gain share stability and roadmap input, which balances bargaining power but narrows JCI’s optionality; performance clauses and KPIs keep terms competitive.

- Volume commitments: secure peak supply

- Joint development: supplier roadmap input

- Trade-off: reduced sourcing optionality

- Controls: KPIs and performance clauses

Tier-1 supply: semiconductor shortages, 10-30% swings, 6-12m requal lag

Tier-1 suppliers concentrate compressors, sensors and chipsets, with semiconductor allocation issues persisting into 2024 and supplier hold-up risk; JCI (operations in 150+ countries, ~100,000 employees in 2024) uses dual-sourcing and long-term contracts to mitigate. Commodity swings of ~10–30% in 2023–24 squeezed equipment margins; requalification lags 6–12 months (costs: tens of thousands). Joint development stabilizes supply but limits optionality.

| Metric | Value (2023–24) |

|---|---|

| Employees / Countries | ~100,000 / 150+ |

| Commodity volatility | 10–30% |

| Requalification lag | 6–12 months |

| Requal cost | tens of thousands USD |

What is included in the product

Tailored Porter’s Five Forces analysis for Johnson Controls International, uncovering competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying disruptive technologies and market-entry risks.

Clear one-sheet Porter's Five Forces for Johnson Controls—instantly visualize competitive pressure with an editable spider chart, swap in your own data, and copy straight into pitch decks or executive reports—no macros needed.

Customers Bargaining Power

Large sophisticated buyers

Governments, campuses, hospitals and Fortune 500s run competitive RFPs; Fortune 500 denotes 500 firms, US has ~6,000 hospitals and ~4,000 degree‑granting colleges, concentrating demand. Professional procurement teams benchmark total cost and service SLAs. Volume and multi‑site scope materially enhance bargaining leverage. Integrators and ESCOs further consolidate buying power.

High switching costs in BMS

Once BMS and controls are installed, replacements disrupt operations: data migration, retraining, and re-integration with BAS, fire and security systems create significant downtime and project complexity. This stickiness tempers price pressure after installation, preserving vendor margins. Open protocols such as BACnet and Modbus (widely adopted by 2024) reduce but do not eliminate switching friction.

Lifecycle and performance contracts

Lifecycle, outcome-based energy guarantees shift buyer focus from capex to delivered savings, with EPCs commonly promising 15–30% energy reductions; purchasers now demand shared-risk models and uptime SLAs often targeting 99.5% availability. Johnson Controls can command 10–20% premium pricing for proven service capabilities, but poor performance triggers penalties (typically 5–10% of contract value) and frequent re-bidding.

Specification-driven purchases

Specification-driven purchases at Johnson Controls are steered by engineering specs, building codes and 2024 sustainability targets, forcing vendors to meet precise performance thresholds; buyers use alternate-or-equal clauses to maintain pricing pressure, while rigorous prequalification shortlists increase direct comparability and competitive bids. Digital analytics and ROI cases in 2024 serve as decisive tie-breakers when technical parity exists.

- Engineering specs dictate vendor inclusion

- Alternate-or-equal clauses preserve pricing leverage

- Prequalification narrows but heightens head-to-head comparison

- Digital analytics/ROI models decide final award

Global price transparency

Benchmark data and online sources make cross-vendor comparisons easier, accelerating buyer leverage. Multi-year frameworks commonly run 3–5 years and embed discount ladders and rebates that compress margins. Currency moves and intensified local competition frequently force deeper concessions on final terms. JCI must localize value propositions and service models to defend margin.

- Benchmark transparency: faster comparisons

- Frameworks: 3–5 year discount ladders

- FX & local rivals: pressure on terms

- JCI response: localize value to protect margin

Buyers demand 99.5% SLA; lock-in backs 10–20% premium

Large buyers (govt, campuses, ~6,000 US hospitals, ~4,000 colleges) run competitive RFPs and 3–5 year frameworks, giving strong leverage; buyers demand 99.5% SLAs and 15–30% energy savings under outcome contracts. Post-installation stickiness and BACnet/Modbus adoption (widely used by 2024) limit switching, letting JCI earn 10–20% premium but face 5–10% penalty risk for poor performance.

| Metric | Value (2024) |

|---|---|

| US hospitals | ~6,000 |

| US colleges | ~4,000 |

| SLA target | 99.5% |

| Energy guarantee | 15–30% |

| JCI premium | 10–20% |

| Penalty | 5–10% |

Preview Before You Purchase

Johnson Controls International Porter's Five Forces Analysis

This preview shows the exact Johnson Controls International Porter’s Five Forces analysis you’ll receive—fully formatted, complete and ready for download the moment you buy. It covers competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications. No placeholders or mockups—this is the deliverable.

From Overview to Strategy Blueprint

Johnson Controls International faces intense rivalry in building systems and automotive segments, with moderate supplier leverage and evolving substitute threats from smart-building software and EV tech; buyer power varies by large institutional contracts versus retail channels. Regulatory and technology shifts heighten entry barriers yet attract niche innovators. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Johnson Controls International.

Suppliers Bargaining Power

Concentrated critical components

Compressors, specialty sensors and control semiconductors are sourced from a limited set of Tier-1 suppliers, creating hold-up risk; semiconductor shortages peaked in 2021–22 and allocation issues linger into 2024. Lead-time spikes and allocation during shortages can delay projects and raise costs. JCI mitigates via dual-sourcing, approved vendor lists and design-for-substitution. Bespoke HVAC, fire and security specs retain supplier leverage in niches.

Materials and input volatility

Volatility in steel, copper, aluminum and electronics drove 2023–24 commodity swings often in the 10–30% range, pressuring equipment margins at Johnson Controls as suppliers pushed through surcharges faster than JCI could reprice bids. Hedging and index-linked contracts reduce exposure, but typical project cycles of 18–36 months create timing gaps that erode margins. Episodic global freight and logistics disruptions in 2023–24 added short-term cost spikes.

Technology roadmaps dependence

Controls at Johnson Controls depend on vendor-specified chipsets, connectivity modules and cybersecurity stacks, tying designs to third-party roadmaps; firmware lifecycles typically span 3–5 years, forcing periodic redesigns and R&D spend spikes. Strategic partnerships (vendor lock-in) secure early access but constrain architecture choices. Compliance to IEC 62443 and UL 2900 in 2024 further raises supplier influence and certification costs.

Switching costs in qualified components

Fire and life-safety systems require certified, tested parts, and requalification of components typically adds 6–12 months and can cost tens of thousands per part, so approved changes ripple through listings and warranties. That dependency gives incumbent suppliers pricing and priority leverage, while Johnson Controls mitigates risk with modular platforms and prequalified alternates to shorten qualification cycles.

- Requalification lag: 6–12 months

- Typical requal cost: tens of thousands per part

- Supplier leverage: pricing & priority

- JCI response: modular platforms, prequalified alternates

Long-term contracts and co-innovation

Long-term contracts and co-innovation with suppliers — backed by JCI’s global scale (operations in 150+ countries, ~100,000 employees in 2024) — use volume commitments and joint development to reduce supply risk at peak demand; suppliers gain share stability and roadmap input, which balances bargaining power but narrows JCI’s optionality; performance clauses and KPIs keep terms competitive.

- Volume commitments: secure peak supply

- Joint development: supplier roadmap input

- Trade-off: reduced sourcing optionality

- Controls: KPIs and performance clauses

Tier-1 supply: semiconductor shortages, 10-30% swings, 6-12m requal lag

Tier-1 suppliers concentrate compressors, sensors and chipsets, with semiconductor allocation issues persisting into 2024 and supplier hold-up risk; JCI (operations in 150+ countries, ~100,000 employees in 2024) uses dual-sourcing and long-term contracts to mitigate. Commodity swings of ~10–30% in 2023–24 squeezed equipment margins; requalification lags 6–12 months (costs: tens of thousands). Joint development stabilizes supply but limits optionality.

| Metric | Value (2023–24) |

|---|---|

| Employees / Countries | ~100,000 / 150+ |

| Commodity volatility | 10–30% |

| Requalification lag | 6–12 months |

| Requal cost | tens of thousands USD |

What is included in the product

Tailored Porter’s Five Forces analysis for Johnson Controls International, uncovering competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying disruptive technologies and market-entry risks.

Clear one-sheet Porter's Five Forces for Johnson Controls—instantly visualize competitive pressure with an editable spider chart, swap in your own data, and copy straight into pitch decks or executive reports—no macros needed.

Customers Bargaining Power

Large sophisticated buyers

Governments, campuses, hospitals and Fortune 500s run competitive RFPs; Fortune 500 denotes 500 firms, US has ~6,000 hospitals and ~4,000 degree‑granting colleges, concentrating demand. Professional procurement teams benchmark total cost and service SLAs. Volume and multi‑site scope materially enhance bargaining leverage. Integrators and ESCOs further consolidate buying power.

High switching costs in BMS

Once BMS and controls are installed, replacements disrupt operations: data migration, retraining, and re-integration with BAS, fire and security systems create significant downtime and project complexity. This stickiness tempers price pressure after installation, preserving vendor margins. Open protocols such as BACnet and Modbus (widely adopted by 2024) reduce but do not eliminate switching friction.

Lifecycle and performance contracts

Lifecycle, outcome-based energy guarantees shift buyer focus from capex to delivered savings, with EPCs commonly promising 15–30% energy reductions; purchasers now demand shared-risk models and uptime SLAs often targeting 99.5% availability. Johnson Controls can command 10–20% premium pricing for proven service capabilities, but poor performance triggers penalties (typically 5–10% of contract value) and frequent re-bidding.

Specification-driven purchases

Specification-driven purchases at Johnson Controls are steered by engineering specs, building codes and 2024 sustainability targets, forcing vendors to meet precise performance thresholds; buyers use alternate-or-equal clauses to maintain pricing pressure, while rigorous prequalification shortlists increase direct comparability and competitive bids. Digital analytics and ROI cases in 2024 serve as decisive tie-breakers when technical parity exists.

- Engineering specs dictate vendor inclusion

- Alternate-or-equal clauses preserve pricing leverage

- Prequalification narrows but heightens head-to-head comparison

- Digital analytics/ROI models decide final award

Global price transparency

Benchmark data and online sources make cross-vendor comparisons easier, accelerating buyer leverage. Multi-year frameworks commonly run 3–5 years and embed discount ladders and rebates that compress margins. Currency moves and intensified local competition frequently force deeper concessions on final terms. JCI must localize value propositions and service models to defend margin.

- Benchmark transparency: faster comparisons

- Frameworks: 3–5 year discount ladders

- FX & local rivals: pressure on terms

- JCI response: localize value to protect margin

Buyers demand 99.5% SLA; lock-in backs 10–20% premium

Large buyers (govt, campuses, ~6,000 US hospitals, ~4,000 colleges) run competitive RFPs and 3–5 year frameworks, giving strong leverage; buyers demand 99.5% SLAs and 15–30% energy savings under outcome contracts. Post-installation stickiness and BACnet/Modbus adoption (widely used by 2024) limit switching, letting JCI earn 10–20% premium but face 5–10% penalty risk for poor performance.

| Metric | Value (2024) |

|---|---|

| US hospitals | ~6,000 |

| US colleges | ~4,000 |

| SLA target | 99.5% |

| Energy guarantee | 15–30% |

| JCI premium | 10–20% |

| Penalty | 5–10% |

Preview Before You Purchase

Johnson Controls International Porter's Five Forces Analysis

This preview shows the exact Johnson Controls International Porter’s Five Forces analysis you’ll receive—fully formatted, complete and ready for download the moment you buy. It covers competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications. No placeholders or mockups—this is the deliverable.

Description

From Overview to Strategy Blueprint

Johnson Controls International faces intense rivalry in building systems and automotive segments, with moderate supplier leverage and evolving substitute threats from smart-building software and EV tech; buyer power varies by large institutional contracts versus retail channels. Regulatory and technology shifts heighten entry barriers yet attract niche innovators. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to Johnson Controls International.

Suppliers Bargaining Power

Concentrated critical components

Compressors, specialty sensors and control semiconductors are sourced from a limited set of Tier-1 suppliers, creating hold-up risk; semiconductor shortages peaked in 2021–22 and allocation issues linger into 2024. Lead-time spikes and allocation during shortages can delay projects and raise costs. JCI mitigates via dual-sourcing, approved vendor lists and design-for-substitution. Bespoke HVAC, fire and security specs retain supplier leverage in niches.

Materials and input volatility

Volatility in steel, copper, aluminum and electronics drove 2023–24 commodity swings often in the 10–30% range, pressuring equipment margins at Johnson Controls as suppliers pushed through surcharges faster than JCI could reprice bids. Hedging and index-linked contracts reduce exposure, but typical project cycles of 18–36 months create timing gaps that erode margins. Episodic global freight and logistics disruptions in 2023–24 added short-term cost spikes.

Technology roadmaps dependence

Controls at Johnson Controls depend on vendor-specified chipsets, connectivity modules and cybersecurity stacks, tying designs to third-party roadmaps; firmware lifecycles typically span 3–5 years, forcing periodic redesigns and R&D spend spikes. Strategic partnerships (vendor lock-in) secure early access but constrain architecture choices. Compliance to IEC 62443 and UL 2900 in 2024 further raises supplier influence and certification costs.

Switching costs in qualified components

Fire and life-safety systems require certified, tested parts, and requalification of components typically adds 6–12 months and can cost tens of thousands per part, so approved changes ripple through listings and warranties. That dependency gives incumbent suppliers pricing and priority leverage, while Johnson Controls mitigates risk with modular platforms and prequalified alternates to shorten qualification cycles.

- Requalification lag: 6–12 months

- Typical requal cost: tens of thousands per part

- Supplier leverage: pricing & priority

- JCI response: modular platforms, prequalified alternates

Long-term contracts and co-innovation

Long-term contracts and co-innovation with suppliers — backed by JCI’s global scale (operations in 150+ countries, ~100,000 employees in 2024) — use volume commitments and joint development to reduce supply risk at peak demand; suppliers gain share stability and roadmap input, which balances bargaining power but narrows JCI’s optionality; performance clauses and KPIs keep terms competitive.

- Volume commitments: secure peak supply

- Joint development: supplier roadmap input

- Trade-off: reduced sourcing optionality

- Controls: KPIs and performance clauses

Tier-1 supply: semiconductor shortages, 10-30% swings, 6-12m requal lag

Tier-1 suppliers concentrate compressors, sensors and chipsets, with semiconductor allocation issues persisting into 2024 and supplier hold-up risk; JCI (operations in 150+ countries, ~100,000 employees in 2024) uses dual-sourcing and long-term contracts to mitigate. Commodity swings of ~10–30% in 2023–24 squeezed equipment margins; requalification lags 6–12 months (costs: tens of thousands). Joint development stabilizes supply but limits optionality.

| Metric | Value (2023–24) |

|---|---|

| Employees / Countries | ~100,000 / 150+ |

| Commodity volatility | 10–30% |

| Requalification lag | 6–12 months |

| Requal cost | tens of thousands USD |

What is included in the product

Tailored Porter’s Five Forces analysis for Johnson Controls International, uncovering competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying disruptive technologies and market-entry risks.

Clear one-sheet Porter's Five Forces for Johnson Controls—instantly visualize competitive pressure with an editable spider chart, swap in your own data, and copy straight into pitch decks or executive reports—no macros needed.

Customers Bargaining Power

Large sophisticated buyers

Governments, campuses, hospitals and Fortune 500s run competitive RFPs; Fortune 500 denotes 500 firms, US has ~6,000 hospitals and ~4,000 degree‑granting colleges, concentrating demand. Professional procurement teams benchmark total cost and service SLAs. Volume and multi‑site scope materially enhance bargaining leverage. Integrators and ESCOs further consolidate buying power.

High switching costs in BMS

Once BMS and controls are installed, replacements disrupt operations: data migration, retraining, and re-integration with BAS, fire and security systems create significant downtime and project complexity. This stickiness tempers price pressure after installation, preserving vendor margins. Open protocols such as BACnet and Modbus (widely adopted by 2024) reduce but do not eliminate switching friction.

Lifecycle and performance contracts

Lifecycle, outcome-based energy guarantees shift buyer focus from capex to delivered savings, with EPCs commonly promising 15–30% energy reductions; purchasers now demand shared-risk models and uptime SLAs often targeting 99.5% availability. Johnson Controls can command 10–20% premium pricing for proven service capabilities, but poor performance triggers penalties (typically 5–10% of contract value) and frequent re-bidding.

Specification-driven purchases

Specification-driven purchases at Johnson Controls are steered by engineering specs, building codes and 2024 sustainability targets, forcing vendors to meet precise performance thresholds; buyers use alternate-or-equal clauses to maintain pricing pressure, while rigorous prequalification shortlists increase direct comparability and competitive bids. Digital analytics and ROI cases in 2024 serve as decisive tie-breakers when technical parity exists.

- Engineering specs dictate vendor inclusion

- Alternate-or-equal clauses preserve pricing leverage

- Prequalification narrows but heightens head-to-head comparison

- Digital analytics/ROI models decide final award

Global price transparency

Benchmark data and online sources make cross-vendor comparisons easier, accelerating buyer leverage. Multi-year frameworks commonly run 3–5 years and embed discount ladders and rebates that compress margins. Currency moves and intensified local competition frequently force deeper concessions on final terms. JCI must localize value propositions and service models to defend margin.

- Benchmark transparency: faster comparisons

- Frameworks: 3–5 year discount ladders

- FX & local rivals: pressure on terms

- JCI response: localize value to protect margin

Buyers demand 99.5% SLA; lock-in backs 10–20% premium

Large buyers (govt, campuses, ~6,000 US hospitals, ~4,000 colleges) run competitive RFPs and 3–5 year frameworks, giving strong leverage; buyers demand 99.5% SLAs and 15–30% energy savings under outcome contracts. Post-installation stickiness and BACnet/Modbus adoption (widely used by 2024) limit switching, letting JCI earn 10–20% premium but face 5–10% penalty risk for poor performance.

| Metric | Value (2024) |

|---|---|

| US hospitals | ~6,000 |

| US colleges | ~4,000 |

| SLA target | 99.5% |

| Energy guarantee | 15–30% |

| JCI premium | 10–20% |

| Penalty | 5–10% |

Preview Before You Purchase

Johnson Controls International Porter's Five Forces Analysis

This preview shows the exact Johnson Controls International Porter’s Five Forces analysis you’ll receive—fully formatted, complete and ready for download the moment you buy. It covers competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications. No placeholders or mockups—this is the deliverable.