Ningbo Joyson Electronic Boston Consulting Group Matrix

Actionable Strategy Starts Here

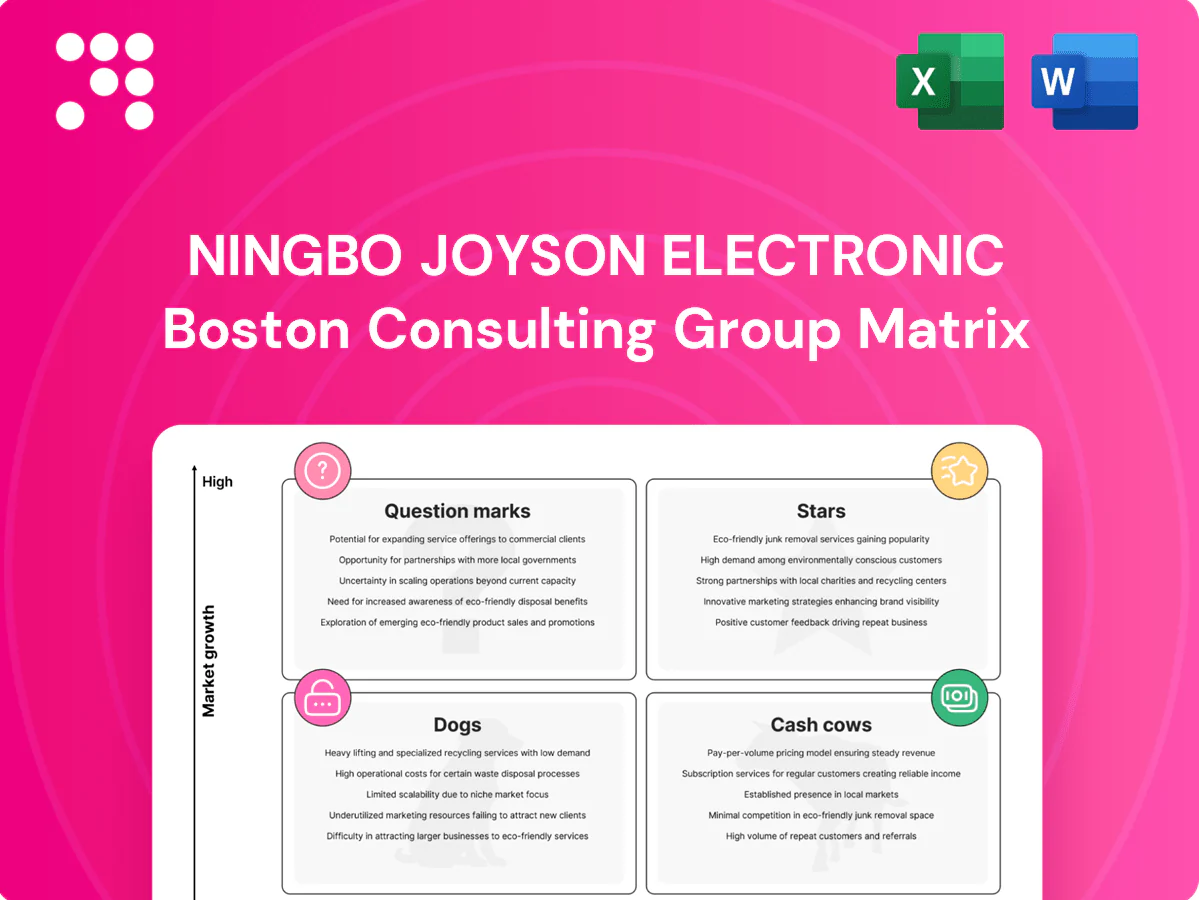

Ningbo Joyson’s BCG Matrix snapshot shows where its product lines land in a shifting auto-electronics market — who’s fueling growth, who’s funding it, and who’s a drag. This preview teases quadrant placements and trends; the full report gives precise placements, data-backed moves, and a ready-to-use Word + Excel package. Buy the complete BCG Matrix for clear investment priorities, tactical recommendations, and a presentation-ready strategic tool.

Stars

Airbag & Seatbelt Platforms (global programs)

High growth in safety content per vehicle—roughly a 25–30% increase since 2018—plus Joyson’s strong global share in airbag and seatbelt platforms positions this as a clear leader; worldwide airbag/seatbelt system demand remains robust with global market estimates near USD 30–35B in 2024. Mandates and emerging-market vehicle buildouts keep unit growth steep, so the program soaks cash for capacity and validation. Defend share via measurable quality wins and faster time-to-launch to protect ASPs. Done right, this Stars engine can convert into fat Cash Cow margins as volumes scale and fixed costs dilute.

Intelligent Cockpits & Large-Format Displays

OEMs are racing to larger integrated cockpits as the global automotive cockpit market tops about $30B in 2024 with a ~8% CAGR to 2029, and Joyson’s deep HMI stack maps directly to that demand. Growth is hot and competition hotter — stay aggressive on design wins and supply resilience. Keep investing in software, optics and thermal expertise. Nail platform reuse so today’s wins don’t bloat tomorrow’s costs.

Integrated HMI Platforms (hardware + middleware)

Bundling displays, input and UI middleware drives rapid stickiness and share: integrated HMI deals can lift OEM retention by 30–50% in early deployments. Market growth is strong—software-defined vehicle content grew ~20% YoY in 2024 with global HMI/IVI spend per vehicle eclipsing ~$1,000 in 2024. Continue pushing OTA-ready stacks and co-development with top OEMs; heavy upfront spend now secures multi-year platform lock-ins.

Advanced Safety Electronics (airbag ECUs, sensing)

Advanced Safety Electronics (airbag ECUs, sensing) benefits from rising per-vehicle content and platform consolidation that favor scaled suppliers; Joyson can leverage its safety credentials and ISO 26262 expertise to win next-gen controller programs. Semiconductor lead times averaged about 20 weeks in 2024, so protecting launch schedules is critical to retain Star status.

- Leverage safety credentials

- Invest in functional safety & silicon partnerships

- Protect lead times (20-week semiconductor avg 2024)

- Missed launches erode Star position

Global OEM Program Integration & Launch Capability

Operational scale is a decisive competitive weapon in fast-growing automotive-electronics segments; the global automotive electronics market was estimated at about $420 billion in 2024, favoring large OEM integrators.

Flawless launches drive share and cross-sell: faster PPAP and program management shorten time-to-revenue and enable repeat awards that expand module scope.

Investing in PPAP speed and dual-sourcing reduces launch defects and supply risk, paying back through larger, repeat program awards and higher lifetime contract value.

- Tags: program-management, PPAP-speed, dual-sourcing, repeat-awards, module-expansion

Convert safety and HMI Stars into Cash Cows: speed PPAP, reuse software, dual-source chips

Stars: high-growth safety and HMI franchises (airbag/seatbelt market ~$30–35B 2024; cockpit market ~$30B 2024) drive rapid share gains but consume capex for validation and supply resilience; semiconductor lead times ~20 weeks (2024) threaten launches. Invest in PPAP speed, software reuse and dual-sourcing to convert Stars into Cash Cows.

| Metric | 2024 |

|---|---|

| Airbag/seatbelt market | $30–35B |

| Cockpit market | $30B |

| HMI spend/vehicle | ~$1,000 |

| Semiconductor lead times | ~20 weeks |

What is included in the product

In-depth BCG analysis of Ningbo Joyson Electronics portfolio, identifying Stars, Cash Cows, Question Marks, Dogs and recommended moves.

One-page BCG matrix highlighting Ningbo Joyson units to simplify strategy and cut decision time.

Cash Cows

Legacy Seatbelt Mechanicals

Legacy Seatbelt Mechanicals sits in a mature market with Ningbo Joyson holding a high share and steady volumes; market growth ~2–3% p.a. means low topline expansion but reliable cash generation. Aim for yield >98% and scrap <0.5% to protect mid-30% segment margins. Targeted automation and footprint optimization (pilot gains +10–15% throughput) improve cash flow. Milk the business, maintain ISO/TS quality, avoid gold-plating.

Replacement & Service Airbag Components

Replacement and service airbag components deliver steady, predictable demand driven by the global automotive aftermarket, which was valued at about USD 446 billion in 2024, supporting recurring parts volumes for Ningbo Joyson Electronic. Growth is limited but margins remain resilient at scale due to strict safety compliance and supplier leverage. Focus on optimizing inventory turns and tightening warranty controls to preserve cash. Those cash flows fund higher-growth HMI investments.

Conventional Instrument Clusters (non-AR, non-3D)

Conventional instrument clusters remain cash cows for Ningbo Joyson, serving cost-sensitive trims that still represent roughly 70% of global light-vehicle volume in 2024 (≈75 million units). Feature growth is muted as premium buyers shift to large centralized displays; margins rely on aggressive cost-downs and reuse of electronics. Focus on locking multi-year supply contracts and maintaining minimal R&D to defend incumbency.

Standard HMI Switches & Controls

Standard HMI switches and controls are commodity-leaning but protected by incumbency and tooling barriers, so prioritize OEE improvements and supplier cost reductions while maintaining quality to avoid chargebacks.

Harvest cash from this cash cow through disciplined pricing and capex minimization; avoid chasing flashy upgrades that erode returns.

- Focus OEE gains, supplier cost-out, hold quality to prevent chargebacks

- Harvest cash, limit capex on nonessential upgrades

- Leverage tooling incumbency as competitive moat

Long-tail OEM Platform Contracts (late-life)

Long-tail OEM platform contracts in late-life still generate steady cash with minimal engineering, often sustaining 15-25% operating margins in 2024 while contributing roughly 8-12% of product-line revenue. Managing obsolescence and moving to small-batch production can cut per-unit costs by ~15-20%, and negotiating price stability over the tail secures predictable cash flow. These programs are ideal to park lean teams and preserve margin without heavy CAPEX.

- Cash margin: 15-25% (2024)

- Revenue share: 8-12% of line

- Small-batch cost cut: ~15-20%

- Low engineering spend, high predictability

Legacy auto parts: mid-30% margins, cash 15–25%, OEE-led play

Legacy seatbelt mechanicals, replacement airbags, instrument clusters and HMI switches generate steady cash with mid-30% segment margins and yield targets >98% (scrap <0.5%). Aftermarket demand (≈USD 446B in 2024) and 70% of LV volume (~75M units) underpin predictability. Cash margins 15–25% (2024); prioritize OEE, tooling moat, minimal capex.

| Metric | 2024 |

|---|---|

| Aftermarket value | USD 446B |

| LV share | 70% (~75M) |

| Cash margin | 15–25% |

Full Transparency, Always

Ningbo Joyson Electronic BCG Matrix

The file you're previewing is the exact Ningbo Joyson Electronic BCG Matrix report you'll receive after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready document tailored for strategic clarity. Once bought, the same file is yours to download, edit, print, or present to stakeholders instantly. It's crafted for immediate use in planning and investor decks.

Actionable Strategy Starts Here

Ningbo Joyson’s BCG Matrix snapshot shows where its product lines land in a shifting auto-electronics market — who’s fueling growth, who’s funding it, and who’s a drag. This preview teases quadrant placements and trends; the full report gives precise placements, data-backed moves, and a ready-to-use Word + Excel package. Buy the complete BCG Matrix for clear investment priorities, tactical recommendations, and a presentation-ready strategic tool.

Stars

Airbag & Seatbelt Platforms (global programs)

High growth in safety content per vehicle—roughly a 25–30% increase since 2018—plus Joyson’s strong global share in airbag and seatbelt platforms positions this as a clear leader; worldwide airbag/seatbelt system demand remains robust with global market estimates near USD 30–35B in 2024. Mandates and emerging-market vehicle buildouts keep unit growth steep, so the program soaks cash for capacity and validation. Defend share via measurable quality wins and faster time-to-launch to protect ASPs. Done right, this Stars engine can convert into fat Cash Cow margins as volumes scale and fixed costs dilute.

Intelligent Cockpits & Large-Format Displays

OEMs are racing to larger integrated cockpits as the global automotive cockpit market tops about $30B in 2024 with a ~8% CAGR to 2029, and Joyson’s deep HMI stack maps directly to that demand. Growth is hot and competition hotter — stay aggressive on design wins and supply resilience. Keep investing in software, optics and thermal expertise. Nail platform reuse so today’s wins don’t bloat tomorrow’s costs.

Integrated HMI Platforms (hardware + middleware)

Bundling displays, input and UI middleware drives rapid stickiness and share: integrated HMI deals can lift OEM retention by 30–50% in early deployments. Market growth is strong—software-defined vehicle content grew ~20% YoY in 2024 with global HMI/IVI spend per vehicle eclipsing ~$1,000 in 2024. Continue pushing OTA-ready stacks and co-development with top OEMs; heavy upfront spend now secures multi-year platform lock-ins.

Advanced Safety Electronics (airbag ECUs, sensing)

Advanced Safety Electronics (airbag ECUs, sensing) benefits from rising per-vehicle content and platform consolidation that favor scaled suppliers; Joyson can leverage its safety credentials and ISO 26262 expertise to win next-gen controller programs. Semiconductor lead times averaged about 20 weeks in 2024, so protecting launch schedules is critical to retain Star status.

- Leverage safety credentials

- Invest in functional safety & silicon partnerships

- Protect lead times (20-week semiconductor avg 2024)

- Missed launches erode Star position

Global OEM Program Integration & Launch Capability

Operational scale is a decisive competitive weapon in fast-growing automotive-electronics segments; the global automotive electronics market was estimated at about $420 billion in 2024, favoring large OEM integrators.

Flawless launches drive share and cross-sell: faster PPAP and program management shorten time-to-revenue and enable repeat awards that expand module scope.

Investing in PPAP speed and dual-sourcing reduces launch defects and supply risk, paying back through larger, repeat program awards and higher lifetime contract value.

- Tags: program-management, PPAP-speed, dual-sourcing, repeat-awards, module-expansion

Convert safety and HMI Stars into Cash Cows: speed PPAP, reuse software, dual-source chips

Stars: high-growth safety and HMI franchises (airbag/seatbelt market ~$30–35B 2024; cockpit market ~$30B 2024) drive rapid share gains but consume capex for validation and supply resilience; semiconductor lead times ~20 weeks (2024) threaten launches. Invest in PPAP speed, software reuse and dual-sourcing to convert Stars into Cash Cows.

| Metric | 2024 |

|---|---|

| Airbag/seatbelt market | $30–35B |

| Cockpit market | $30B |

| HMI spend/vehicle | ~$1,000 |

| Semiconductor lead times | ~20 weeks |

What is included in the product

In-depth BCG analysis of Ningbo Joyson Electronics portfolio, identifying Stars, Cash Cows, Question Marks, Dogs and recommended moves.

One-page BCG matrix highlighting Ningbo Joyson units to simplify strategy and cut decision time.

Cash Cows

Legacy Seatbelt Mechanicals

Legacy Seatbelt Mechanicals sits in a mature market with Ningbo Joyson holding a high share and steady volumes; market growth ~2–3% p.a. means low topline expansion but reliable cash generation. Aim for yield >98% and scrap <0.5% to protect mid-30% segment margins. Targeted automation and footprint optimization (pilot gains +10–15% throughput) improve cash flow. Milk the business, maintain ISO/TS quality, avoid gold-plating.

Replacement & Service Airbag Components

Replacement and service airbag components deliver steady, predictable demand driven by the global automotive aftermarket, which was valued at about USD 446 billion in 2024, supporting recurring parts volumes for Ningbo Joyson Electronic. Growth is limited but margins remain resilient at scale due to strict safety compliance and supplier leverage. Focus on optimizing inventory turns and tightening warranty controls to preserve cash. Those cash flows fund higher-growth HMI investments.

Conventional Instrument Clusters (non-AR, non-3D)

Conventional instrument clusters remain cash cows for Ningbo Joyson, serving cost-sensitive trims that still represent roughly 70% of global light-vehicle volume in 2024 (≈75 million units). Feature growth is muted as premium buyers shift to large centralized displays; margins rely on aggressive cost-downs and reuse of electronics. Focus on locking multi-year supply contracts and maintaining minimal R&D to defend incumbency.

Standard HMI Switches & Controls

Standard HMI switches and controls are commodity-leaning but protected by incumbency and tooling barriers, so prioritize OEE improvements and supplier cost reductions while maintaining quality to avoid chargebacks.

Harvest cash from this cash cow through disciplined pricing and capex minimization; avoid chasing flashy upgrades that erode returns.

- Focus OEE gains, supplier cost-out, hold quality to prevent chargebacks

- Harvest cash, limit capex on nonessential upgrades

- Leverage tooling incumbency as competitive moat

Long-tail OEM Platform Contracts (late-life)

Long-tail OEM platform contracts in late-life still generate steady cash with minimal engineering, often sustaining 15-25% operating margins in 2024 while contributing roughly 8-12% of product-line revenue. Managing obsolescence and moving to small-batch production can cut per-unit costs by ~15-20%, and negotiating price stability over the tail secures predictable cash flow. These programs are ideal to park lean teams and preserve margin without heavy CAPEX.

- Cash margin: 15-25% (2024)

- Revenue share: 8-12% of line

- Small-batch cost cut: ~15-20%

- Low engineering spend, high predictability

Legacy auto parts: mid-30% margins, cash 15–25%, OEE-led play

Legacy seatbelt mechanicals, replacement airbags, instrument clusters and HMI switches generate steady cash with mid-30% segment margins and yield targets >98% (scrap <0.5%). Aftermarket demand (≈USD 446B in 2024) and 70% of LV volume (~75M units) underpin predictability. Cash margins 15–25% (2024); prioritize OEE, tooling moat, minimal capex.

| Metric | 2024 |

|---|---|

| Aftermarket value | USD 446B |

| LV share | 70% (~75M) |

| Cash margin | 15–25% |

Full Transparency, Always

Ningbo Joyson Electronic BCG Matrix

The file you're previewing is the exact Ningbo Joyson Electronic BCG Matrix report you'll receive after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready document tailored for strategic clarity. Once bought, the same file is yours to download, edit, print, or present to stakeholders instantly. It's crafted for immediate use in planning and investor decks.

Original: $10.00

-65%$10.00

$3.50Description

Actionable Strategy Starts Here

Ningbo Joyson’s BCG Matrix snapshot shows where its product lines land in a shifting auto-electronics market — who’s fueling growth, who’s funding it, and who’s a drag. This preview teases quadrant placements and trends; the full report gives precise placements, data-backed moves, and a ready-to-use Word + Excel package. Buy the complete BCG Matrix for clear investment priorities, tactical recommendations, and a presentation-ready strategic tool.

Stars

Airbag & Seatbelt Platforms (global programs)

High growth in safety content per vehicle—roughly a 25–30% increase since 2018—plus Joyson’s strong global share in airbag and seatbelt platforms positions this as a clear leader; worldwide airbag/seatbelt system demand remains robust with global market estimates near USD 30–35B in 2024. Mandates and emerging-market vehicle buildouts keep unit growth steep, so the program soaks cash for capacity and validation. Defend share via measurable quality wins and faster time-to-launch to protect ASPs. Done right, this Stars engine can convert into fat Cash Cow margins as volumes scale and fixed costs dilute.

Intelligent Cockpits & Large-Format Displays

OEMs are racing to larger integrated cockpits as the global automotive cockpit market tops about $30B in 2024 with a ~8% CAGR to 2029, and Joyson’s deep HMI stack maps directly to that demand. Growth is hot and competition hotter — stay aggressive on design wins and supply resilience. Keep investing in software, optics and thermal expertise. Nail platform reuse so today’s wins don’t bloat tomorrow’s costs.

Integrated HMI Platforms (hardware + middleware)

Bundling displays, input and UI middleware drives rapid stickiness and share: integrated HMI deals can lift OEM retention by 30–50% in early deployments. Market growth is strong—software-defined vehicle content grew ~20% YoY in 2024 with global HMI/IVI spend per vehicle eclipsing ~$1,000 in 2024. Continue pushing OTA-ready stacks and co-development with top OEMs; heavy upfront spend now secures multi-year platform lock-ins.

Advanced Safety Electronics (airbag ECUs, sensing)

Advanced Safety Electronics (airbag ECUs, sensing) benefits from rising per-vehicle content and platform consolidation that favor scaled suppliers; Joyson can leverage its safety credentials and ISO 26262 expertise to win next-gen controller programs. Semiconductor lead times averaged about 20 weeks in 2024, so protecting launch schedules is critical to retain Star status.

- Leverage safety credentials

- Invest in functional safety & silicon partnerships

- Protect lead times (20-week semiconductor avg 2024)

- Missed launches erode Star position

Global OEM Program Integration & Launch Capability

Operational scale is a decisive competitive weapon in fast-growing automotive-electronics segments; the global automotive electronics market was estimated at about $420 billion in 2024, favoring large OEM integrators.

Flawless launches drive share and cross-sell: faster PPAP and program management shorten time-to-revenue and enable repeat awards that expand module scope.

Investing in PPAP speed and dual-sourcing reduces launch defects and supply risk, paying back through larger, repeat program awards and higher lifetime contract value.

- Tags: program-management, PPAP-speed, dual-sourcing, repeat-awards, module-expansion

Convert safety and HMI Stars into Cash Cows: speed PPAP, reuse software, dual-source chips

Stars: high-growth safety and HMI franchises (airbag/seatbelt market ~$30–35B 2024; cockpit market ~$30B 2024) drive rapid share gains but consume capex for validation and supply resilience; semiconductor lead times ~20 weeks (2024) threaten launches. Invest in PPAP speed, software reuse and dual-sourcing to convert Stars into Cash Cows.

| Metric | 2024 |

|---|---|

| Airbag/seatbelt market | $30–35B |

| Cockpit market | $30B |

| HMI spend/vehicle | ~$1,000 |

| Semiconductor lead times | ~20 weeks |

What is included in the product

In-depth BCG analysis of Ningbo Joyson Electronics portfolio, identifying Stars, Cash Cows, Question Marks, Dogs and recommended moves.

One-page BCG matrix highlighting Ningbo Joyson units to simplify strategy and cut decision time.

Cash Cows

Legacy Seatbelt Mechanicals

Legacy Seatbelt Mechanicals sits in a mature market with Ningbo Joyson holding a high share and steady volumes; market growth ~2–3% p.a. means low topline expansion but reliable cash generation. Aim for yield >98% and scrap <0.5% to protect mid-30% segment margins. Targeted automation and footprint optimization (pilot gains +10–15% throughput) improve cash flow. Milk the business, maintain ISO/TS quality, avoid gold-plating.

Replacement & Service Airbag Components

Replacement and service airbag components deliver steady, predictable demand driven by the global automotive aftermarket, which was valued at about USD 446 billion in 2024, supporting recurring parts volumes for Ningbo Joyson Electronic. Growth is limited but margins remain resilient at scale due to strict safety compliance and supplier leverage. Focus on optimizing inventory turns and tightening warranty controls to preserve cash. Those cash flows fund higher-growth HMI investments.

Conventional Instrument Clusters (non-AR, non-3D)

Conventional instrument clusters remain cash cows for Ningbo Joyson, serving cost-sensitive trims that still represent roughly 70% of global light-vehicle volume in 2024 (≈75 million units). Feature growth is muted as premium buyers shift to large centralized displays; margins rely on aggressive cost-downs and reuse of electronics. Focus on locking multi-year supply contracts and maintaining minimal R&D to defend incumbency.

Standard HMI Switches & Controls

Standard HMI switches and controls are commodity-leaning but protected by incumbency and tooling barriers, so prioritize OEE improvements and supplier cost reductions while maintaining quality to avoid chargebacks.

Harvest cash from this cash cow through disciplined pricing and capex minimization; avoid chasing flashy upgrades that erode returns.

- Focus OEE gains, supplier cost-out, hold quality to prevent chargebacks

- Harvest cash, limit capex on nonessential upgrades

- Leverage tooling incumbency as competitive moat

Long-tail OEM Platform Contracts (late-life)

Long-tail OEM platform contracts in late-life still generate steady cash with minimal engineering, often sustaining 15-25% operating margins in 2024 while contributing roughly 8-12% of product-line revenue. Managing obsolescence and moving to small-batch production can cut per-unit costs by ~15-20%, and negotiating price stability over the tail secures predictable cash flow. These programs are ideal to park lean teams and preserve margin without heavy CAPEX.

- Cash margin: 15-25% (2024)

- Revenue share: 8-12% of line

- Small-batch cost cut: ~15-20%

- Low engineering spend, high predictability

Legacy auto parts: mid-30% margins, cash 15–25%, OEE-led play

Legacy seatbelt mechanicals, replacement airbags, instrument clusters and HMI switches generate steady cash with mid-30% segment margins and yield targets >98% (scrap <0.5%). Aftermarket demand (≈USD 446B in 2024) and 70% of LV volume (~75M units) underpin predictability. Cash margins 15–25% (2024); prioritize OEE, tooling moat, minimal capex.

| Metric | 2024 |

|---|---|

| Aftermarket value | USD 446B |

| LV share | 70% (~75M) |

| Cash margin | 15–25% |

Full Transparency, Always

Ningbo Joyson Electronic BCG Matrix

The file you're previewing is the exact Ningbo Joyson Electronic BCG Matrix report you'll receive after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready document tailored for strategic clarity. Once bought, the same file is yours to download, edit, print, or present to stakeholders instantly. It's crafted for immediate use in planning and investor decks.