JSW Energy Boston Consulting Group Matrix

See the Bigger Picture

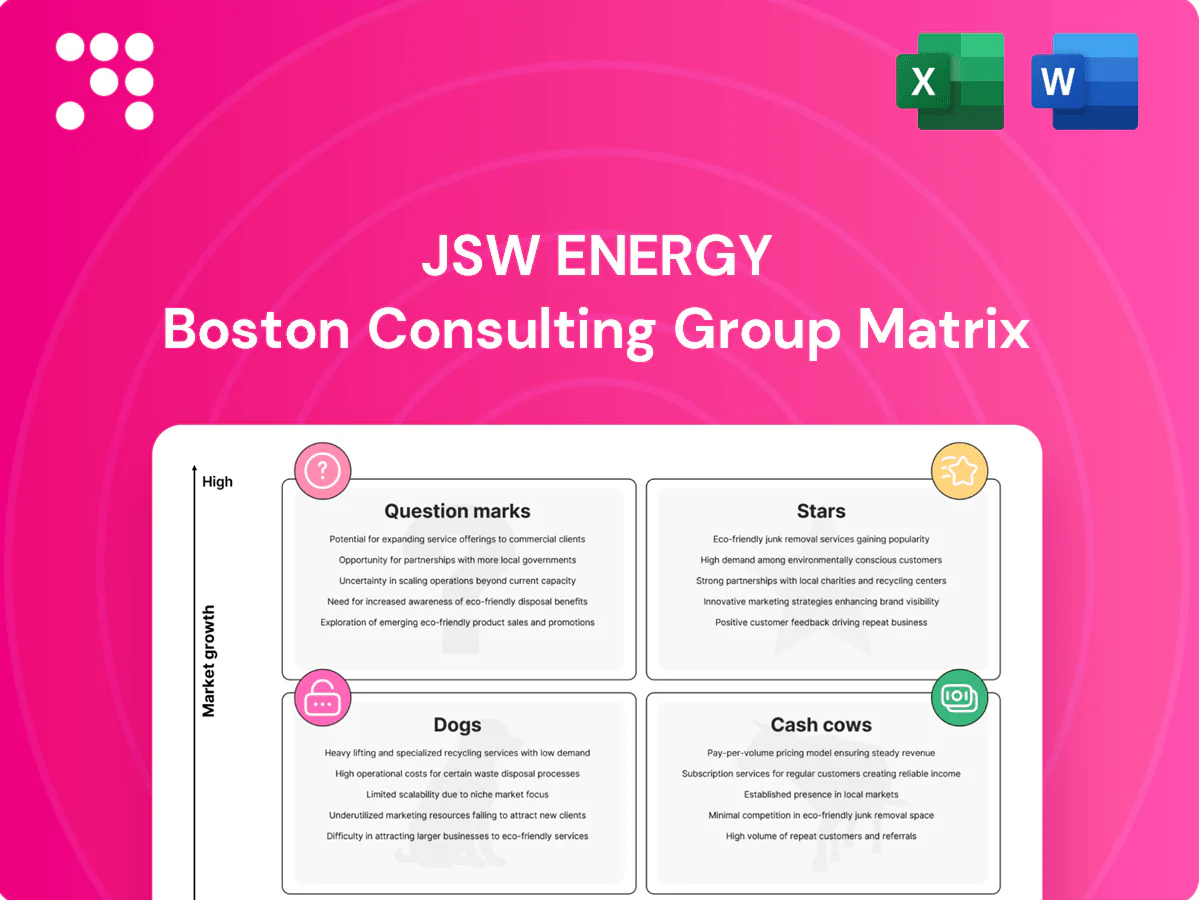

Curious where JSW Energy’s offerings sit in the market—Stars, Cash Cows, Dogs or Question Marks? This snapshot teases the story; buy the full BCG Matrix to get quadrant-by-quadrant placement, data-backed recommendations and a clear playbook for capital allocation. Instant download includes a polished Word report and a high-level Excel summary so you can present and act fast—purchase now and skip the guesswork.

Stars

Utility-scale renewables

High-growth wind and solar operations, with over 1 GW of commissioned renewable capacity and a multi-GW pipeline as of 2024, position JSW Energy in the Stars quadrant. Leader status in select states, backed by long-term PPAs, drives market share and visibility. The segment needs heavy capex and rollout muscle, but 2024 growth tailwinds justify sustained investment and could convert it into dependable cash generators if momentum continues.

Pumped storage build-out

Pumped storage build-out is a Star for JSW Energy as India races to 500 GW non-fossil capacity by 2030 and CEA estimates ~94 GW of pumped hydro potential, making massive grid-scale storage strategically critical. Early-mover control of sites and permits can translate to outsized market share. Capital hungry today, these projects form defensible moats as assets come online and can convert to future cash cows.

Long-tenor RE PPAs

Long-tenor RE PPAs (typically 15–25 years) give JSW Energy stable cashflows and guaranteed offtake as market demand surges; long contracts underpin project financing and merchant risk reduction. With renewables now central to growth, continuous execution and portfolio optimization are required to compress LCOE (solar LCOE down ~85% since 2010) and keep costs competitive. Investing to scale preserves leadership as the segment expands.

Hybrid RE parks (solar+wind+storage)

Hybrid RE parks (solar+wind+storage) offer integrated firm power that markets demand; first movers can secure premium tariffs and grid priority to grow share. Complexity raises capex and execution risk today, but battery pack costs fell to ~130 USD/kWh in 2024 (BNEF), improving returns. With scale these sites can dominate markets and generate substantial free cash flow later.

- Firm power premium: higher tariffs, grid priority

- Execution: greater capex, coordination risk

- 2024 battery cost: ~130 USD/kWh

- Scale outcome: market dominance → strong cash generation

Transmission linked to RE corridors

Transmission linked to RE corridors is the critical backbone for fast-compounding renewable evacuation; India targets 500 GW non-fossil capacity by 2030 and ~170 GW was operational by 2024, driving network demand. Securing key lines gives JSW Energy influence and share in growth nodes. Upfront capex and regulatory work are heavy, but payoffs track market expansion—keep building, today's star grid links become tomorrow's annuity.

- Influence: secures access to high-growth RE hubs

- Capex: large upfront spend and permitting burden

- Returns: revenue growth aligned with expanding RE volumes

1+ GW live; multi-GW pipeline; pumped hydro ~94 GW; storage ~130

High-growth renewables (1+ GW commissioned, multi-GW pipeline in 2024) and pumped hydro upside (CEA ~94 GW potential) make JSW Energy Stars; long PPAs (15–25 yrs) and hybrids raise premiums while capex and storage costs (~130 USD/kWh in 2024) are execution constraints.

| Metric | 2024 / Note |

|---|---|

| Commissioned RE | 1+ GW |

| Pipeline | Multi-GW |

| Battery cost | ~130 USD/kWh |

| Pumped hydro potential | ~94 GW (CEA) |

What is included in the product

Comprehensive BCG Matrix of JSW Energy with strategic insights on Stars, Cash Cows, Question Marks, Dogs, and investment actions.

One-page JSW Energy BCG matrix to spot underperformers and reallocate capital fast for clearer decisions.

Cash Cows

Thermal plants under firm PPAs

Thermal plants under firm PPAs form classic cash cows for JSW Energy: mature market, locked-in offtake and predictable dispatch yield high utilization and steady margins. With ~2.1 GW thermal capacity under long-term PPAs reported by JSW Energy in FY2024, recovered fixed charges sustain EBITDA stability. Limited growth capex beyond upkeep and efficiency tweaks; milk the cash to fund renewables while maintaining reliability.

O&M services for owned and third-party plants

O&M services for JSW Energy’s owned and third-party plants deliver stable, repeatable revenues in a mature Indian service market, supporting its ~5.4 GW portfolio as of Mar 2024. Scale and technical know-how drive cost advantages and healthy O&M margins versus project development. Incremental investment needs are low, largely limited to tools and talent. Surplus cash from generation is being directed to scale storage and renewables growth.

Transmission assets with regulated returns

Transmission assets with regulated returns deliver visible cash yield under tariff frameworks; CERC normative RoE for the 2019–24 period was 15.5%, supporting steady cashflow in FY24. Operating costs are predictable with upside from efficiency gains and loss reduction initiatives that lower technical losses and O&M spend. Minimal promotional spend focuses investment on reliability metrics; harvest cash while prudently reinforcing the network.

Power trading on contracted surplus

Power trading on contracted surplus leverages JSW Energy's ~4.8 GW portfolio (2024) to capture merchant spreads without heavy capex, converting excess generation into cash. In a mature, competitive market, disciplined, risk‑managed volumes delivered steady margin uplift in 2024. Systems and analytics upgrades improved scheduling and hedging efficiency; optimize, don't overreach.

- Leverage: portfolio surplus monetization

- Risk: disciplined, hedged volumes

- Efficiency: analytics/systems uplift

- Strategy: optimize, do not overreach

Hydro baseload with stable hydrology

Legacy hydro baseload at JSW Energy delivers low-variable-cost cash flow with high availability, underpinning steady EBITDA even as growth is modest; consolidated capacity was 4,842 MW in FY2024 and hydro assets provide resilient dispatch and ancillary services value. Maintenance capex for existing hydro is materially below greenfield spend, so incremental efficiency upgrades yield high IRR and should be prioritized to bank returns.

- FY2024 consolidated capacity: 4,842 MW

- Hydro: baseload reliability, high availability

- Maintenance capex << greenfield capex

- Prioritize efficiency upgrades to maximize cash generation

Thermal PPAs (2.1 GW) and hydro (4,842 MW) fund renewables.

Thermal PPAs (~2.1 GW) and legacy hydro (4,842 MW) deliver predictable, high‑margin cashflows; O&M on a ~5.4 GW portfolio provides steady recurring revenue while merchant trading of surplus (~4.8 GW) converts excess into incremental cash. Low upkeep capex lets JSW Energy harvest cash to fund renewables and storage growth.

| Metric | Value | FY2024 |

|---|---|---|

| Thermal under PPA | 2.1 GW | Stable EBITDA |

| Total portfolio (O&M) | 5.4 GW | Recurring revenue |

| Hydro | 4,842 MW | Baseload cash |

| CERC RoE (2019–24) | 15.5% | Regulated returns |

Preview = Final Product

JSW Energy BCG Matrix

The JSW Energy BCG Matrix you're previewing on this page is the exact file you'll receive after purchase — no watermarks, no placeholders. This final, fully formatted report maps market share and growth for JSW Energy's portfolio with clear visuals and strategic notes. Buy once and download immediately: ready to edit, present, or plug into planning sessions without surprises.

See the Bigger Picture

Curious where JSW Energy’s offerings sit in the market—Stars, Cash Cows, Dogs or Question Marks? This snapshot teases the story; buy the full BCG Matrix to get quadrant-by-quadrant placement, data-backed recommendations and a clear playbook for capital allocation. Instant download includes a polished Word report and a high-level Excel summary so you can present and act fast—purchase now and skip the guesswork.

Stars

Utility-scale renewables

High-growth wind and solar operations, with over 1 GW of commissioned renewable capacity and a multi-GW pipeline as of 2024, position JSW Energy in the Stars quadrant. Leader status in select states, backed by long-term PPAs, drives market share and visibility. The segment needs heavy capex and rollout muscle, but 2024 growth tailwinds justify sustained investment and could convert it into dependable cash generators if momentum continues.

Pumped storage build-out

Pumped storage build-out is a Star for JSW Energy as India races to 500 GW non-fossil capacity by 2030 and CEA estimates ~94 GW of pumped hydro potential, making massive grid-scale storage strategically critical. Early-mover control of sites and permits can translate to outsized market share. Capital hungry today, these projects form defensible moats as assets come online and can convert to future cash cows.

Long-tenor RE PPAs

Long-tenor RE PPAs (typically 15–25 years) give JSW Energy stable cashflows and guaranteed offtake as market demand surges; long contracts underpin project financing and merchant risk reduction. With renewables now central to growth, continuous execution and portfolio optimization are required to compress LCOE (solar LCOE down ~85% since 2010) and keep costs competitive. Investing to scale preserves leadership as the segment expands.

Hybrid RE parks (solar+wind+storage)

Hybrid RE parks (solar+wind+storage) offer integrated firm power that markets demand; first movers can secure premium tariffs and grid priority to grow share. Complexity raises capex and execution risk today, but battery pack costs fell to ~130 USD/kWh in 2024 (BNEF), improving returns. With scale these sites can dominate markets and generate substantial free cash flow later.

- Firm power premium: higher tariffs, grid priority

- Execution: greater capex, coordination risk

- 2024 battery cost: ~130 USD/kWh

- Scale outcome: market dominance → strong cash generation

Transmission linked to RE corridors

Transmission linked to RE corridors is the critical backbone for fast-compounding renewable evacuation; India targets 500 GW non-fossil capacity by 2030 and ~170 GW was operational by 2024, driving network demand. Securing key lines gives JSW Energy influence and share in growth nodes. Upfront capex and regulatory work are heavy, but payoffs track market expansion—keep building, today's star grid links become tomorrow's annuity.

- Influence: secures access to high-growth RE hubs

- Capex: large upfront spend and permitting burden

- Returns: revenue growth aligned with expanding RE volumes

1+ GW live; multi-GW pipeline; pumped hydro ~94 GW; storage ~130

High-growth renewables (1+ GW commissioned, multi-GW pipeline in 2024) and pumped hydro upside (CEA ~94 GW potential) make JSW Energy Stars; long PPAs (15–25 yrs) and hybrids raise premiums while capex and storage costs (~130 USD/kWh in 2024) are execution constraints.

| Metric | 2024 / Note |

|---|---|

| Commissioned RE | 1+ GW |

| Pipeline | Multi-GW |

| Battery cost | ~130 USD/kWh |

| Pumped hydro potential | ~94 GW (CEA) |

What is included in the product

Comprehensive BCG Matrix of JSW Energy with strategic insights on Stars, Cash Cows, Question Marks, Dogs, and investment actions.

One-page JSW Energy BCG matrix to spot underperformers and reallocate capital fast for clearer decisions.

Cash Cows

Thermal plants under firm PPAs

Thermal plants under firm PPAs form classic cash cows for JSW Energy: mature market, locked-in offtake and predictable dispatch yield high utilization and steady margins. With ~2.1 GW thermal capacity under long-term PPAs reported by JSW Energy in FY2024, recovered fixed charges sustain EBITDA stability. Limited growth capex beyond upkeep and efficiency tweaks; milk the cash to fund renewables while maintaining reliability.

O&M services for owned and third-party plants

O&M services for JSW Energy’s owned and third-party plants deliver stable, repeatable revenues in a mature Indian service market, supporting its ~5.4 GW portfolio as of Mar 2024. Scale and technical know-how drive cost advantages and healthy O&M margins versus project development. Incremental investment needs are low, largely limited to tools and talent. Surplus cash from generation is being directed to scale storage and renewables growth.

Transmission assets with regulated returns

Transmission assets with regulated returns deliver visible cash yield under tariff frameworks; CERC normative RoE for the 2019–24 period was 15.5%, supporting steady cashflow in FY24. Operating costs are predictable with upside from efficiency gains and loss reduction initiatives that lower technical losses and O&M spend. Minimal promotional spend focuses investment on reliability metrics; harvest cash while prudently reinforcing the network.

Power trading on contracted surplus

Power trading on contracted surplus leverages JSW Energy's ~4.8 GW portfolio (2024) to capture merchant spreads without heavy capex, converting excess generation into cash. In a mature, competitive market, disciplined, risk‑managed volumes delivered steady margin uplift in 2024. Systems and analytics upgrades improved scheduling and hedging efficiency; optimize, don't overreach.

- Leverage: portfolio surplus monetization

- Risk: disciplined, hedged volumes

- Efficiency: analytics/systems uplift

- Strategy: optimize, do not overreach

Hydro baseload with stable hydrology

Legacy hydro baseload at JSW Energy delivers low-variable-cost cash flow with high availability, underpinning steady EBITDA even as growth is modest; consolidated capacity was 4,842 MW in FY2024 and hydro assets provide resilient dispatch and ancillary services value. Maintenance capex for existing hydro is materially below greenfield spend, so incremental efficiency upgrades yield high IRR and should be prioritized to bank returns.

- FY2024 consolidated capacity: 4,842 MW

- Hydro: baseload reliability, high availability

- Maintenance capex << greenfield capex

- Prioritize efficiency upgrades to maximize cash generation

Thermal PPAs (2.1 GW) and hydro (4,842 MW) fund renewables.

Thermal PPAs (~2.1 GW) and legacy hydro (4,842 MW) deliver predictable, high‑margin cashflows; O&M on a ~5.4 GW portfolio provides steady recurring revenue while merchant trading of surplus (~4.8 GW) converts excess into incremental cash. Low upkeep capex lets JSW Energy harvest cash to fund renewables and storage growth.

| Metric | Value | FY2024 |

|---|---|---|

| Thermal under PPA | 2.1 GW | Stable EBITDA |

| Total portfolio (O&M) | 5.4 GW | Recurring revenue |

| Hydro | 4,842 MW | Baseload cash |

| CERC RoE (2019–24) | 15.5% | Regulated returns |

Preview = Final Product

JSW Energy BCG Matrix

The JSW Energy BCG Matrix you're previewing on this page is the exact file you'll receive after purchase — no watermarks, no placeholders. This final, fully formatted report maps market share and growth for JSW Energy's portfolio with clear visuals and strategic notes. Buy once and download immediately: ready to edit, present, or plug into planning sessions without surprises.

Original: $10.00

-65%$10.00

$3.50Description

See the Bigger Picture

Curious where JSW Energy’s offerings sit in the market—Stars, Cash Cows, Dogs or Question Marks? This snapshot teases the story; buy the full BCG Matrix to get quadrant-by-quadrant placement, data-backed recommendations and a clear playbook for capital allocation. Instant download includes a polished Word report and a high-level Excel summary so you can present and act fast—purchase now and skip the guesswork.

Stars

Utility-scale renewables

High-growth wind and solar operations, with over 1 GW of commissioned renewable capacity and a multi-GW pipeline as of 2024, position JSW Energy in the Stars quadrant. Leader status in select states, backed by long-term PPAs, drives market share and visibility. The segment needs heavy capex and rollout muscle, but 2024 growth tailwinds justify sustained investment and could convert it into dependable cash generators if momentum continues.

Pumped storage build-out

Pumped storage build-out is a Star for JSW Energy as India races to 500 GW non-fossil capacity by 2030 and CEA estimates ~94 GW of pumped hydro potential, making massive grid-scale storage strategically critical. Early-mover control of sites and permits can translate to outsized market share. Capital hungry today, these projects form defensible moats as assets come online and can convert to future cash cows.

Long-tenor RE PPAs

Long-tenor RE PPAs (typically 15–25 years) give JSW Energy stable cashflows and guaranteed offtake as market demand surges; long contracts underpin project financing and merchant risk reduction. With renewables now central to growth, continuous execution and portfolio optimization are required to compress LCOE (solar LCOE down ~85% since 2010) and keep costs competitive. Investing to scale preserves leadership as the segment expands.

Hybrid RE parks (solar+wind+storage)

Hybrid RE parks (solar+wind+storage) offer integrated firm power that markets demand; first movers can secure premium tariffs and grid priority to grow share. Complexity raises capex and execution risk today, but battery pack costs fell to ~130 USD/kWh in 2024 (BNEF), improving returns. With scale these sites can dominate markets and generate substantial free cash flow later.

- Firm power premium: higher tariffs, grid priority

- Execution: greater capex, coordination risk

- 2024 battery cost: ~130 USD/kWh

- Scale outcome: market dominance → strong cash generation

Transmission linked to RE corridors

Transmission linked to RE corridors is the critical backbone for fast-compounding renewable evacuation; India targets 500 GW non-fossil capacity by 2030 and ~170 GW was operational by 2024, driving network demand. Securing key lines gives JSW Energy influence and share in growth nodes. Upfront capex and regulatory work are heavy, but payoffs track market expansion—keep building, today's star grid links become tomorrow's annuity.

- Influence: secures access to high-growth RE hubs

- Capex: large upfront spend and permitting burden

- Returns: revenue growth aligned with expanding RE volumes

1+ GW live; multi-GW pipeline; pumped hydro ~94 GW; storage ~130

High-growth renewables (1+ GW commissioned, multi-GW pipeline in 2024) and pumped hydro upside (CEA ~94 GW potential) make JSW Energy Stars; long PPAs (15–25 yrs) and hybrids raise premiums while capex and storage costs (~130 USD/kWh in 2024) are execution constraints.

| Metric | 2024 / Note |

|---|---|

| Commissioned RE | 1+ GW |

| Pipeline | Multi-GW |

| Battery cost | ~130 USD/kWh |

| Pumped hydro potential | ~94 GW (CEA) |

What is included in the product

Comprehensive BCG Matrix of JSW Energy with strategic insights on Stars, Cash Cows, Question Marks, Dogs, and investment actions.

One-page JSW Energy BCG matrix to spot underperformers and reallocate capital fast for clearer decisions.

Cash Cows

Thermal plants under firm PPAs

Thermal plants under firm PPAs form classic cash cows for JSW Energy: mature market, locked-in offtake and predictable dispatch yield high utilization and steady margins. With ~2.1 GW thermal capacity under long-term PPAs reported by JSW Energy in FY2024, recovered fixed charges sustain EBITDA stability. Limited growth capex beyond upkeep and efficiency tweaks; milk the cash to fund renewables while maintaining reliability.

O&M services for owned and third-party plants

O&M services for JSW Energy’s owned and third-party plants deliver stable, repeatable revenues in a mature Indian service market, supporting its ~5.4 GW portfolio as of Mar 2024. Scale and technical know-how drive cost advantages and healthy O&M margins versus project development. Incremental investment needs are low, largely limited to tools and talent. Surplus cash from generation is being directed to scale storage and renewables growth.

Transmission assets with regulated returns

Transmission assets with regulated returns deliver visible cash yield under tariff frameworks; CERC normative RoE for the 2019–24 period was 15.5%, supporting steady cashflow in FY24. Operating costs are predictable with upside from efficiency gains and loss reduction initiatives that lower technical losses and O&M spend. Minimal promotional spend focuses investment on reliability metrics; harvest cash while prudently reinforcing the network.

Power trading on contracted surplus

Power trading on contracted surplus leverages JSW Energy's ~4.8 GW portfolio (2024) to capture merchant spreads without heavy capex, converting excess generation into cash. In a mature, competitive market, disciplined, risk‑managed volumes delivered steady margin uplift in 2024. Systems and analytics upgrades improved scheduling and hedging efficiency; optimize, don't overreach.

- Leverage: portfolio surplus monetization

- Risk: disciplined, hedged volumes

- Efficiency: analytics/systems uplift

- Strategy: optimize, do not overreach

Hydro baseload with stable hydrology

Legacy hydro baseload at JSW Energy delivers low-variable-cost cash flow with high availability, underpinning steady EBITDA even as growth is modest; consolidated capacity was 4,842 MW in FY2024 and hydro assets provide resilient dispatch and ancillary services value. Maintenance capex for existing hydro is materially below greenfield spend, so incremental efficiency upgrades yield high IRR and should be prioritized to bank returns.

- FY2024 consolidated capacity: 4,842 MW

- Hydro: baseload reliability, high availability

- Maintenance capex << greenfield capex

- Prioritize efficiency upgrades to maximize cash generation

Thermal PPAs (2.1 GW) and hydro (4,842 MW) fund renewables.

Thermal PPAs (~2.1 GW) and legacy hydro (4,842 MW) deliver predictable, high‑margin cashflows; O&M on a ~5.4 GW portfolio provides steady recurring revenue while merchant trading of surplus (~4.8 GW) converts excess into incremental cash. Low upkeep capex lets JSW Energy harvest cash to fund renewables and storage growth.

| Metric | Value | FY2024 |

|---|---|---|

| Thermal under PPA | 2.1 GW | Stable EBITDA |

| Total portfolio (O&M) | 5.4 GW | Recurring revenue |

| Hydro | 4,842 MW | Baseload cash |

| CERC RoE (2019–24) | 15.5% | Regulated returns |

Preview = Final Product

JSW Energy BCG Matrix

The JSW Energy BCG Matrix you're previewing on this page is the exact file you'll receive after purchase — no watermarks, no placeholders. This final, fully formatted report maps market share and growth for JSW Energy's portfolio with clear visuals and strategic notes. Buy once and download immediately: ready to edit, present, or plug into planning sessions without surprises.