Jubilant Pharmova Porter's Five Forces Analysis

From Overview to Strategy Blueprint

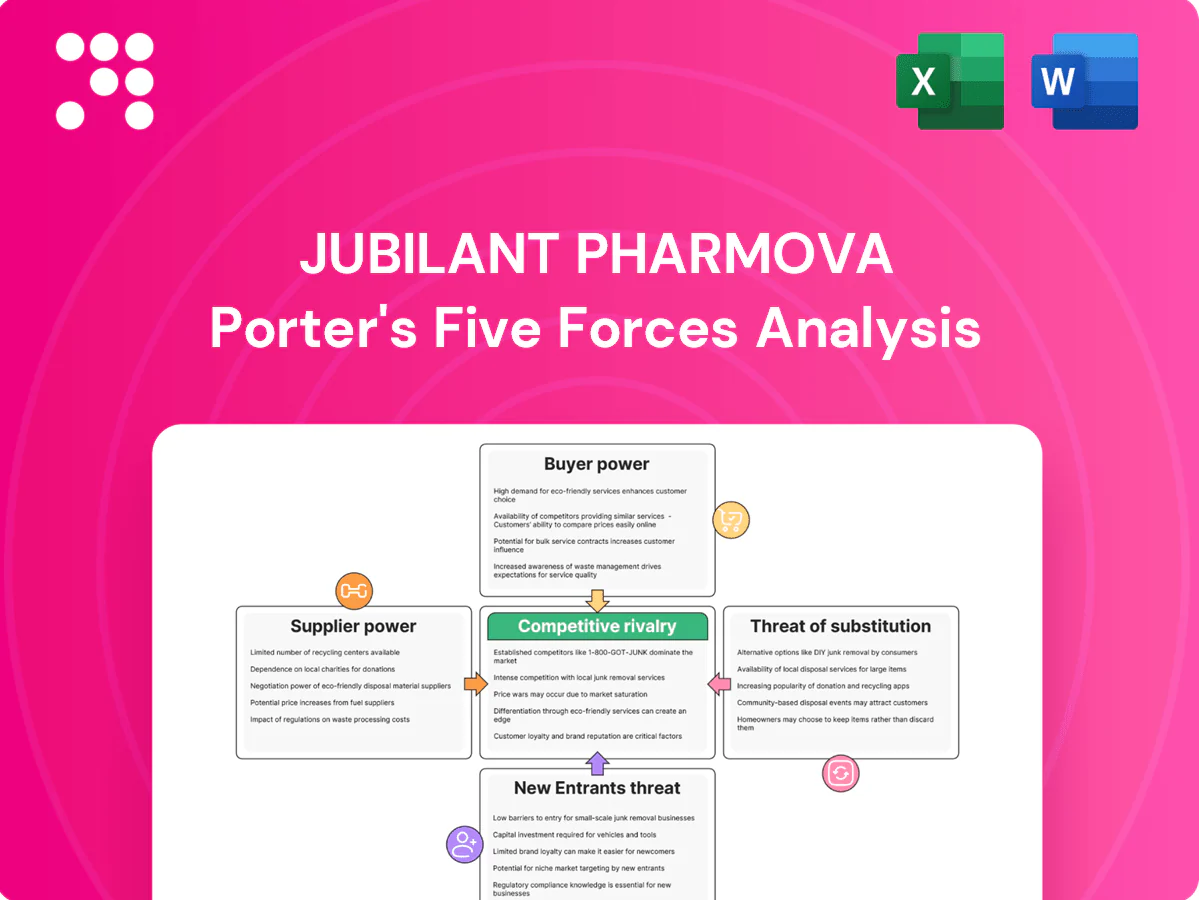

Jubilant Pharmova faces moderate buyer power, supplier concentration in specialty APIs, and steady rivalry driven by contract manufacturing scale—while regulatory barriers limit new entrants. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated radioisotope sources

Key radioisotopes such as Mo-99/Tc-99m, I-131 and Lu-177 are produced by a handful of specialized reactors and commercial producers (fewer than 10 global suppliers), concentrating supply power; outages or regulatory noncompliance rapidly tighten availability and can drive spot-price volatility. Long-term contracts and dual-sourcing mitigate risk but substitution is constrained by strict GMP and radionuclidic purity specs, elevating supplier leverage for Jubilant Pharmova’s radiopharma inputs.

Specialty APIs, biologics, and excipients

Sterile injectables and allergy immunotherapy depend on high-spec APIs, biologics and sterile-grade excipients/containers, and the qualified supplier pool is narrow due to GMP and sterility demands. Supplier qualification and certification commonly take 6–12 months, with equipment revalidation cycles often every 3 years, making supplier switching slow and costly. When capacity tightens, suppliers gain leverage to negotiate price, lead times and contract terms.

Cold-chain and hazmat logistics

Cold-chain and hazmat shipments for Jubilant Pharmova require niche logistics providers due to time-sensitive, radioactive and temperature-controlled handling, with pharmaceuticals accounting for about 6% of global air cargo value (IATA).

Route permits, compliance and specialized packaging narrow alternatives and raise switching costs, while disruptions can quickly spike freight premiums and give logistics partners bargaining leverage.

Building partial in-house cold-chain capacity mitigates but does not eliminate this supplier power.

Specialized equipment and maintenance

Specialized cyclotrons, hot cells, isolators and aseptic fill-finish lines come from a small set of OEMs (e.g., IBA for cyclotrons). In 2024 OEM concentration keeps service contracts and spare parts as bottlenecks, increasing downtime risk and dependence on approved vendors. Vendors embed pricing power via maintenance and validation cycles.

- Limited OEM pool (cyclotrons: IBA prominent)

- Service/spare parts bottlenecks

- Downtime raises vendor dependence

- Maintenance/validation drive margin capture

CRO/CRMO scientific inputs

For CRO/CRMO scientific inputs, niche assay kits, reference standards, and proprietary software concentrate supply and create dependency; method validation ties processes to specific inputs and regulatory bodies in 2024 continue to require revalidation and filings for significant changes, often causing months-long delays, strengthening select suppliers’ negotiating stance.

- Supplier concentration: high for niche assays

- Switching cost: revalidation + regulatory filing

- Time impact: delays measured in months (2024)

- Negotiation leverage: strong for specialized suppliers

Concentrated radioisotope supply drives high switching costs and logistics leverage

Supplier power is high: key radioisotopes sourced from fewer than 10 global producers create scarcity and spot-price volatility; switching is limited by GMP and purity specs. Sterile APIs and OEM equipment require 6–12 month qualification cycles and vendor-tied maintenance, raising switching costs. Cold-chain/logistics are niche, with pharma ~6% of global air cargo value (IATA), giving carriers leverage.

| Metric | 2024 |

|---|---|

| Radioisotope suppliers | fewer than 10 |

| Supplier qualification | 6–12 months |

| Pharma share of air cargo value | 6% (IATA) |

What is included in the product

Tailored Porter's Five Forces analysis of Jubilant Pharmova that uncovers key drivers of competition, buyer and supplier power, substitution threats and entry barriers, identifying strategic risks and opportunities for market positioning.

A concise one-sheet Porter's Five Forces for Jubilant Pharmova that highlights competitive pressures, supplier power, regulatory risks and buyer dynamics to speed strategic decisions; editable radar chart and simple layout make it easy to adapt for pitch decks or scenario analysis.

Customers Bargaining Power

Hospitals and nuclear medicine centers

Large hospital systems and imaging chains buy radiopharmaceuticals at scale and use competitive tenders and service-level guarantees to compress margins. However, time-critical delivery, short isotope half-lives and stringent regulatory equivalence (cold-chain, GMP) limit switching. In 2024 global nuclear medicine procedures were ~30 million, sustaining steady demand. Buyer power is therefore moderate, constrained by clinical protocols and uptime needs.

Group purchasing and government tenders

In 2024 GPOs—serving roughly 90% of US hospitals—and public tenders aggregate demand to force price pressure on injectables, pushing suppliers like Jubilant Pharmova to offer steep volume discounts. Volume commitments often trade off against margin compression and higher working capital. Compliance, supply assurance and past recalls strongly influence awards, with buyers using multi‑year, multi‑site (commonly 3–5 year) contracts to secure leverage.

Pharma sponsors in CDMO/CRDMO

Large pharma sponsors exercise strong leverage over Jubilant Pharmova on price, timelines, IP terms and tech-transfer support, especially given their scale and share of outsourced spend; in 2024 the global CDMO market was estimated at about $120 billion, expanding buyer choice. Competitive CDMO capacity further weakens provider pricing power for non-niche work, while validated processes and regulatory filings create significant switching costs. Customer power therefore varies sharply by project complexity and availability of qualified capacity.

Therapy-area differentiation

Unique radiodiagnostics and niche immunotherapies limit buyer alternatives for Jubilant Pharmova, increasing switching costs and reducing price sensitivity.

Clinical performance and supply continuity often trump price in specialty segments, giving the company leverage with hospitals and imaging centers.

Where generics or multi-source labels exist, purchasers demand steep discounts, but therapy-area differentiation tempers buyer power in specialty niches.

- Limited alternatives increase bargaining leverage

- Clinical efficacy and availability outweigh price

- Generics drive aggressive discounting

- Differentiation reduces buyer pressure

Service and reliability sensitivity

For short half-life products, on-time, in-full (OTIF) delivery is critical; industry OTIF targets are typically ≥95% for critical pharma SKUs, and failures swiftly shift negotiating leverage to buyers who demand penalties, backup supply and redundancy. Vendors with documented high reliability secure premium contractual terms and lower penalty exposure.

- OTIF target ≥95%

- Penalties/contingency clauses common

- Backup supply required for critical SKUs

- Reliability records improve vendor terms

GPOs ~90%, 30M procedures, OTIF ≥95%, $120B CDMO

Customers wield moderate-to-high power: GPOs (covering ~90% of US hospitals) and tenders compress prices, while niche radiopharma demand (~30M nuclear medicine procedures in 2024) and short isotope half-lives create switching barriers; OTIF targets ≥95% and a $120B global CDMO market (2024) split leverage by segment.

| Metric | 2024 Value |

|---|---|

| US GPO coverage | ~90% |

| Nuclear procedures | ~30M |

| OTIF target | ≥95% |

| Global CDMO market | $120B |

Full Version Awaits

Jubilant Pharmova Porter's Five Forces Analysis

This preview shows the exact Jubilant Pharmova Porter’s Five Forces analysis you’ll receive—fully formatted and ready for use. No mockups or placeholders: the document displayed is the same file available for instant download after purchase. Use it immediately for research or decision-making.

From Overview to Strategy Blueprint

Jubilant Pharmova faces moderate buyer power, supplier concentration in specialty APIs, and steady rivalry driven by contract manufacturing scale—while regulatory barriers limit new entrants. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated radioisotope sources

Key radioisotopes such as Mo-99/Tc-99m, I-131 and Lu-177 are produced by a handful of specialized reactors and commercial producers (fewer than 10 global suppliers), concentrating supply power; outages or regulatory noncompliance rapidly tighten availability and can drive spot-price volatility. Long-term contracts and dual-sourcing mitigate risk but substitution is constrained by strict GMP and radionuclidic purity specs, elevating supplier leverage for Jubilant Pharmova’s radiopharma inputs.

Specialty APIs, biologics, and excipients

Sterile injectables and allergy immunotherapy depend on high-spec APIs, biologics and sterile-grade excipients/containers, and the qualified supplier pool is narrow due to GMP and sterility demands. Supplier qualification and certification commonly take 6–12 months, with equipment revalidation cycles often every 3 years, making supplier switching slow and costly. When capacity tightens, suppliers gain leverage to negotiate price, lead times and contract terms.

Cold-chain and hazmat logistics

Cold-chain and hazmat shipments for Jubilant Pharmova require niche logistics providers due to time-sensitive, radioactive and temperature-controlled handling, with pharmaceuticals accounting for about 6% of global air cargo value (IATA).

Route permits, compliance and specialized packaging narrow alternatives and raise switching costs, while disruptions can quickly spike freight premiums and give logistics partners bargaining leverage.

Building partial in-house cold-chain capacity mitigates but does not eliminate this supplier power.

Specialized equipment and maintenance

Specialized cyclotrons, hot cells, isolators and aseptic fill-finish lines come from a small set of OEMs (e.g., IBA for cyclotrons). In 2024 OEM concentration keeps service contracts and spare parts as bottlenecks, increasing downtime risk and dependence on approved vendors. Vendors embed pricing power via maintenance and validation cycles.

- Limited OEM pool (cyclotrons: IBA prominent)

- Service/spare parts bottlenecks

- Downtime raises vendor dependence

- Maintenance/validation drive margin capture

CRO/CRMO scientific inputs

For CRO/CRMO scientific inputs, niche assay kits, reference standards, and proprietary software concentrate supply and create dependency; method validation ties processes to specific inputs and regulatory bodies in 2024 continue to require revalidation and filings for significant changes, often causing months-long delays, strengthening select suppliers’ negotiating stance.

- Supplier concentration: high for niche assays

- Switching cost: revalidation + regulatory filing

- Time impact: delays measured in months (2024)

- Negotiation leverage: strong for specialized suppliers

Concentrated radioisotope supply drives high switching costs and logistics leverage

Supplier power is high: key radioisotopes sourced from fewer than 10 global producers create scarcity and spot-price volatility; switching is limited by GMP and purity specs. Sterile APIs and OEM equipment require 6–12 month qualification cycles and vendor-tied maintenance, raising switching costs. Cold-chain/logistics are niche, with pharma ~6% of global air cargo value (IATA), giving carriers leverage.

| Metric | 2024 |

|---|---|

| Radioisotope suppliers | fewer than 10 |

| Supplier qualification | 6–12 months |

| Pharma share of air cargo value | 6% (IATA) |

What is included in the product

Tailored Porter's Five Forces analysis of Jubilant Pharmova that uncovers key drivers of competition, buyer and supplier power, substitution threats and entry barriers, identifying strategic risks and opportunities for market positioning.

A concise one-sheet Porter's Five Forces for Jubilant Pharmova that highlights competitive pressures, supplier power, regulatory risks and buyer dynamics to speed strategic decisions; editable radar chart and simple layout make it easy to adapt for pitch decks or scenario analysis.

Customers Bargaining Power

Hospitals and nuclear medicine centers

Large hospital systems and imaging chains buy radiopharmaceuticals at scale and use competitive tenders and service-level guarantees to compress margins. However, time-critical delivery, short isotope half-lives and stringent regulatory equivalence (cold-chain, GMP) limit switching. In 2024 global nuclear medicine procedures were ~30 million, sustaining steady demand. Buyer power is therefore moderate, constrained by clinical protocols and uptime needs.

Group purchasing and government tenders

In 2024 GPOs—serving roughly 90% of US hospitals—and public tenders aggregate demand to force price pressure on injectables, pushing suppliers like Jubilant Pharmova to offer steep volume discounts. Volume commitments often trade off against margin compression and higher working capital. Compliance, supply assurance and past recalls strongly influence awards, with buyers using multi‑year, multi‑site (commonly 3–5 year) contracts to secure leverage.

Pharma sponsors in CDMO/CRDMO

Large pharma sponsors exercise strong leverage over Jubilant Pharmova on price, timelines, IP terms and tech-transfer support, especially given their scale and share of outsourced spend; in 2024 the global CDMO market was estimated at about $120 billion, expanding buyer choice. Competitive CDMO capacity further weakens provider pricing power for non-niche work, while validated processes and regulatory filings create significant switching costs. Customer power therefore varies sharply by project complexity and availability of qualified capacity.

Therapy-area differentiation

Unique radiodiagnostics and niche immunotherapies limit buyer alternatives for Jubilant Pharmova, increasing switching costs and reducing price sensitivity.

Clinical performance and supply continuity often trump price in specialty segments, giving the company leverage with hospitals and imaging centers.

Where generics or multi-source labels exist, purchasers demand steep discounts, but therapy-area differentiation tempers buyer power in specialty niches.

- Limited alternatives increase bargaining leverage

- Clinical efficacy and availability outweigh price

- Generics drive aggressive discounting

- Differentiation reduces buyer pressure

Service and reliability sensitivity

For short half-life products, on-time, in-full (OTIF) delivery is critical; industry OTIF targets are typically ≥95% for critical pharma SKUs, and failures swiftly shift negotiating leverage to buyers who demand penalties, backup supply and redundancy. Vendors with documented high reliability secure premium contractual terms and lower penalty exposure.

- OTIF target ≥95%

- Penalties/contingency clauses common

- Backup supply required for critical SKUs

- Reliability records improve vendor terms

GPOs ~90%, 30M procedures, OTIF ≥95%, $120B CDMO

Customers wield moderate-to-high power: GPOs (covering ~90% of US hospitals) and tenders compress prices, while niche radiopharma demand (~30M nuclear medicine procedures in 2024) and short isotope half-lives create switching barriers; OTIF targets ≥95% and a $120B global CDMO market (2024) split leverage by segment.

| Metric | 2024 Value |

|---|---|

| US GPO coverage | ~90% |

| Nuclear procedures | ~30M |

| OTIF target | ≥95% |

| Global CDMO market | $120B |

Full Version Awaits

Jubilant Pharmova Porter's Five Forces Analysis

This preview shows the exact Jubilant Pharmova Porter’s Five Forces analysis you’ll receive—fully formatted and ready for use. No mockups or placeholders: the document displayed is the same file available for instant download after purchase. Use it immediately for research or decision-making.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Jubilant Pharmova faces moderate buyer power, supplier concentration in specialty APIs, and steady rivalry driven by contract manufacturing scale—while regulatory barriers limit new entrants. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated radioisotope sources

Key radioisotopes such as Mo-99/Tc-99m, I-131 and Lu-177 are produced by a handful of specialized reactors and commercial producers (fewer than 10 global suppliers), concentrating supply power; outages or regulatory noncompliance rapidly tighten availability and can drive spot-price volatility. Long-term contracts and dual-sourcing mitigate risk but substitution is constrained by strict GMP and radionuclidic purity specs, elevating supplier leverage for Jubilant Pharmova’s radiopharma inputs.

Specialty APIs, biologics, and excipients

Sterile injectables and allergy immunotherapy depend on high-spec APIs, biologics and sterile-grade excipients/containers, and the qualified supplier pool is narrow due to GMP and sterility demands. Supplier qualification and certification commonly take 6–12 months, with equipment revalidation cycles often every 3 years, making supplier switching slow and costly. When capacity tightens, suppliers gain leverage to negotiate price, lead times and contract terms.

Cold-chain and hazmat logistics

Cold-chain and hazmat shipments for Jubilant Pharmova require niche logistics providers due to time-sensitive, radioactive and temperature-controlled handling, with pharmaceuticals accounting for about 6% of global air cargo value (IATA).

Route permits, compliance and specialized packaging narrow alternatives and raise switching costs, while disruptions can quickly spike freight premiums and give logistics partners bargaining leverage.

Building partial in-house cold-chain capacity mitigates but does not eliminate this supplier power.

Specialized equipment and maintenance

Specialized cyclotrons, hot cells, isolators and aseptic fill-finish lines come from a small set of OEMs (e.g., IBA for cyclotrons). In 2024 OEM concentration keeps service contracts and spare parts as bottlenecks, increasing downtime risk and dependence on approved vendors. Vendors embed pricing power via maintenance and validation cycles.

- Limited OEM pool (cyclotrons: IBA prominent)

- Service/spare parts bottlenecks

- Downtime raises vendor dependence

- Maintenance/validation drive margin capture

CRO/CRMO scientific inputs

For CRO/CRMO scientific inputs, niche assay kits, reference standards, and proprietary software concentrate supply and create dependency; method validation ties processes to specific inputs and regulatory bodies in 2024 continue to require revalidation and filings for significant changes, often causing months-long delays, strengthening select suppliers’ negotiating stance.

- Supplier concentration: high for niche assays

- Switching cost: revalidation + regulatory filing

- Time impact: delays measured in months (2024)

- Negotiation leverage: strong for specialized suppliers

Concentrated radioisotope supply drives high switching costs and logistics leverage

Supplier power is high: key radioisotopes sourced from fewer than 10 global producers create scarcity and spot-price volatility; switching is limited by GMP and purity specs. Sterile APIs and OEM equipment require 6–12 month qualification cycles and vendor-tied maintenance, raising switching costs. Cold-chain/logistics are niche, with pharma ~6% of global air cargo value (IATA), giving carriers leverage.

| Metric | 2024 |

|---|---|

| Radioisotope suppliers | fewer than 10 |

| Supplier qualification | 6–12 months |

| Pharma share of air cargo value | 6% (IATA) |

What is included in the product

Tailored Porter's Five Forces analysis of Jubilant Pharmova that uncovers key drivers of competition, buyer and supplier power, substitution threats and entry barriers, identifying strategic risks and opportunities for market positioning.

A concise one-sheet Porter's Five Forces for Jubilant Pharmova that highlights competitive pressures, supplier power, regulatory risks and buyer dynamics to speed strategic decisions; editable radar chart and simple layout make it easy to adapt for pitch decks or scenario analysis.

Customers Bargaining Power

Hospitals and nuclear medicine centers

Large hospital systems and imaging chains buy radiopharmaceuticals at scale and use competitive tenders and service-level guarantees to compress margins. However, time-critical delivery, short isotope half-lives and stringent regulatory equivalence (cold-chain, GMP) limit switching. In 2024 global nuclear medicine procedures were ~30 million, sustaining steady demand. Buyer power is therefore moderate, constrained by clinical protocols and uptime needs.

Group purchasing and government tenders

In 2024 GPOs—serving roughly 90% of US hospitals—and public tenders aggregate demand to force price pressure on injectables, pushing suppliers like Jubilant Pharmova to offer steep volume discounts. Volume commitments often trade off against margin compression and higher working capital. Compliance, supply assurance and past recalls strongly influence awards, with buyers using multi‑year, multi‑site (commonly 3–5 year) contracts to secure leverage.

Pharma sponsors in CDMO/CRDMO

Large pharma sponsors exercise strong leverage over Jubilant Pharmova on price, timelines, IP terms and tech-transfer support, especially given their scale and share of outsourced spend; in 2024 the global CDMO market was estimated at about $120 billion, expanding buyer choice. Competitive CDMO capacity further weakens provider pricing power for non-niche work, while validated processes and regulatory filings create significant switching costs. Customer power therefore varies sharply by project complexity and availability of qualified capacity.

Therapy-area differentiation

Unique radiodiagnostics and niche immunotherapies limit buyer alternatives for Jubilant Pharmova, increasing switching costs and reducing price sensitivity.

Clinical performance and supply continuity often trump price in specialty segments, giving the company leverage with hospitals and imaging centers.

Where generics or multi-source labels exist, purchasers demand steep discounts, but therapy-area differentiation tempers buyer power in specialty niches.

- Limited alternatives increase bargaining leverage

- Clinical efficacy and availability outweigh price

- Generics drive aggressive discounting

- Differentiation reduces buyer pressure

Service and reliability sensitivity

For short half-life products, on-time, in-full (OTIF) delivery is critical; industry OTIF targets are typically ≥95% for critical pharma SKUs, and failures swiftly shift negotiating leverage to buyers who demand penalties, backup supply and redundancy. Vendors with documented high reliability secure premium contractual terms and lower penalty exposure.

- OTIF target ≥95%

- Penalties/contingency clauses common

- Backup supply required for critical SKUs

- Reliability records improve vendor terms

GPOs ~90%, 30M procedures, OTIF ≥95%, $120B CDMO

Customers wield moderate-to-high power: GPOs (covering ~90% of US hospitals) and tenders compress prices, while niche radiopharma demand (~30M nuclear medicine procedures in 2024) and short isotope half-lives create switching barriers; OTIF targets ≥95% and a $120B global CDMO market (2024) split leverage by segment.

| Metric | 2024 Value |

|---|---|

| US GPO coverage | ~90% |

| Nuclear procedures | ~30M |

| OTIF target | ≥95% |

| Global CDMO market | $120B |

Full Version Awaits

Jubilant Pharmova Porter's Five Forces Analysis

This preview shows the exact Jubilant Pharmova Porter’s Five Forces analysis you’ll receive—fully formatted and ready for use. No mockups or placeholders: the document displayed is the same file available for instant download after purchase. Use it immediately for research or decision-making.