Judges Scientific Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

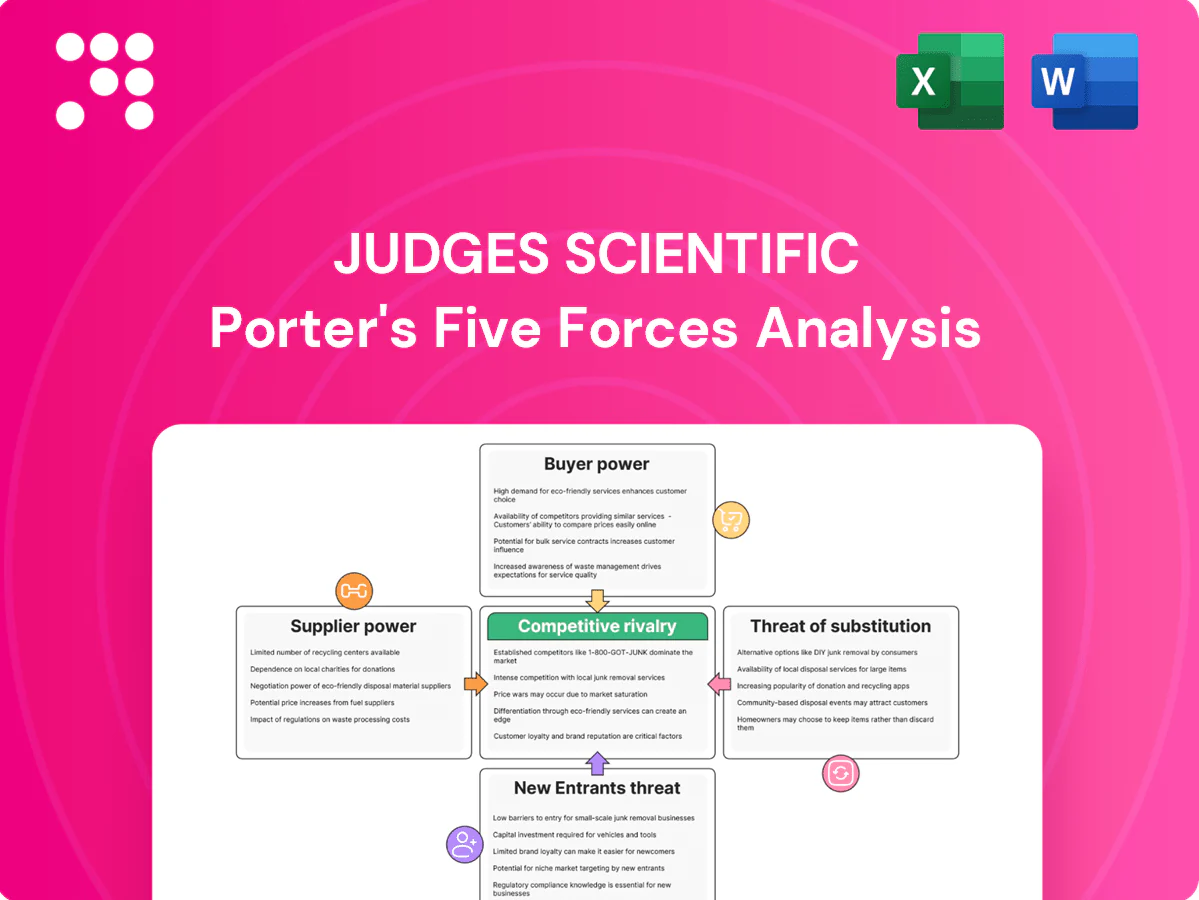

Judges Scientific faces moderate supplier power, niche customer bargaining, and evolving substitute risks as it navigates specialty instruments and testing services; competitive rivalry centers on innovation and service depth. This snapshot hints at strategic pressure points—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Specialized components

Judges’ instruments rely on precision optics, sensors, vacuum parts and specialty electronics that remain non‑commoditized; the global precision optics market was about $16.2bn in 2023 and is growing ~6% annually, keeping supplier niches prized. Such niche suppliers with proprietary know‑how raise leverage on pricing and contract terms, and increase dependence on supplier quality and continuity.

Concentration pockets

While many parts are fragmented, certain subassemblies such as high‑end detectors and lasers have few qualified vendors, creating single‑source exposure that elevates switching costs and supplier margin extraction. Limited alternatives concentrate bargaining power in these pockets, and negotiation leverage varies across Judges Scientific’s portfolio depending on each subsidiary’s category mix. Risk mitigation relies on dual sourcing and strategic inventory.

Qualification lock‑in

Scientific instruments require rigorous qualification and compliance testing, and requalifying a new supplier demands engineering time, formal documentation and often customer revalidation cycles that can delay deployment. This qualification lock‑in reduces short‑term buyer flexibility, raising switching costs and operational risk. As a result, incumbent suppliers gain leverage and stronger bargaining power at renewal and price negotiations.

Lead‑time and scarcity

Cyclical shortages in semiconductors, precision machined parts and optics have pushed lead times well above pre‑pandemic norms, with semiconductor lead times peaking above 20 weeks in 2021–22 and remaining elevated thereafter, extending Judges Scientific production cycles. Tight supply lets suppliers prioritize larger customers and pass surcharges, while volatility disrupts schedules, strains inventory and increases working capital needs, harming delivery performance.

- Lead times: peaked >20 weeks (2021–22)

- Supplier power: prioritization and surcharges

- Impact: schedule disruption, higher inventory and working capital

Mitigation levers

Multi-sourcing, design-for-supply and strategic inventories can materially moderate supplier power for Judges Scientific, while group-level purchasing aggregates demand across c.40 operating companies (2024), improving negotiating leverage. Long-term agreements and joint development lower supply risk for critical parts, but these levers need coordination to avoid eroding niche agility.

- Multi-sourcing

- Design-for-supply

- Strategic inventories

- Group purchasing (c.40 companies, 2024)

- Long-term agreements & joint development

- Coordination vs niche agility

Precision optics supply squeeze - $16.2bn market, concentrated vendors

Judges relies on non‑commoditized precision optics/electronics (precision optics ~$16.2bn market in 2023, ~6% CAGR) and a c.40‑company group (2024), concentrating supplier power in lasers/detectors with few qualified vendors and requalification lock‑in. Covid-era lead times peaked >20 weeks (2021–22), raising inventories and working capital; multi‑sourcing and group purchasing partially mitigate this.

| Metric | Value |

|---|---|

| Precision optics market (2023) | $16.2bn |

| Optics CAGR | ~6% pa |

| Operating companies (2024) | c.40 |

| Lead times peak | >20 weeks (2021–22) |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and industry-specific disruptors affecting Judges Scientific's pricing, margins and growth prospects. Includes strategic commentary and data-driven insights for investors, management and academic use.

A concise one-sheet Porter's Five Forces for Judges Scientific—instantly highlights supplier, buyer, entrant, substitute and rivalry pressures so leadership can make fast, informed strategic decisions.

Customers Bargaining Power

Technical spec priority

Customers—universities, research institutes, industrial labs and regulated sectors—prioritise technical specs: performance, accuracy and reliability often trump unit price, reducing direct price sensitivity for mission‑critical tools. Value‑in‑use framing lets vendors sustain margins; the global scientific instruments market was estimated at about $69bn in 2024, underpinning premium pricing for high‑spec equipment.

Procurement formality

Tenders, framework agreements and grant budgets introduce structured competition for Judges Scientific suppliers. Formal procurement increases buyer leverage on discounts and service terms. Frameworks typically run 3–5 years, creating intense negotiation windows. Once placed, laboratory systems can be sticky for years; public procurement equals about 12% of GDP in OECD countries.

High switching costs

Installed instruments require extensive user training, SOPs and method validation—often entailing 40+ hours of training and validation per platform, raising direct adoption costs. Switching vendors triggers downtime, retraining and data continuity risks that can equal weeks of lost productivity and measurable revenue impact. Deep integration with LIMS and workflows locks choices, weakening buyer power post-install and reducing negotiating leverage.

Consolidated accounts

Consolidated accounts give large pharma, semiconductor and aerospace buyers strong leverage over Judges Scientific by bundling volumes, demanding global service SLAs and securing price concessions; in 2024 this trend intensified as centralized procurement prioritized single-vendor global agreements. Volume rebates and bundled service packages are commonly used as bargaining chips, while smaller academic labs remain price-sensitive with limited negotiating power.

- Large buyers: bundle volumes, demand global SLAs

- Negotiation tools: volume rebates, service packages

- Smaller labs: price-constrained, low leverage

Service and uptime

Aftermarket support, calibration and spares are mission-critical for Judges Scientific (AIM: JDG), letting buyers trade renewal timing to extract lower service fees; robust uptime guarantees allow the group to charge premium ASPs while weak service reduces switching costs and raises buyer power, pressuring margins.

Performance, uptime and validation drive premium pricing in the $69bn scientific instruments market

Customers prioritise performance, accuracy and uptime over unit price, enabling Judges Scientific (AIM: JDG) to sustain premium ASPs in a global scientific instruments market ~69bn in 2024. Procurement frameworks (3–5yr) and large buyers (global SLAs, volume rebates) increase buyer leverage, while installed-base stickiness, 40+ hr validation and LIMS integration raise switching costs. Public procurement ~12% of OECD GDP concentrates negotiation power in consolidated accounts.

| Metric | Value |

|---|---|

| Market 2024 | $69bn |

| Public procurement | ~12% GDP (OECD) |

| Training/validation | 40+ hrs |

Same Document Delivered

Judges Scientific Porter's Five Forces Analysis

You’re viewing the Judges Scientific Porter’s Five Forces Analysis and this preview is the exact document you’ll receive after purchase—no placeholders or mockups. The full file is professionally formatted, ready to download and use immediately upon payment. Content covers competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications tailored to Judges Scientific.

A Must-Have Tool for Decision-Makers

Judges Scientific faces moderate supplier power, niche customer bargaining, and evolving substitute risks as it navigates specialty instruments and testing services; competitive rivalry centers on innovation and service depth. This snapshot hints at strategic pressure points—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Specialized components

Judges’ instruments rely on precision optics, sensors, vacuum parts and specialty electronics that remain non‑commoditized; the global precision optics market was about $16.2bn in 2023 and is growing ~6% annually, keeping supplier niches prized. Such niche suppliers with proprietary know‑how raise leverage on pricing and contract terms, and increase dependence on supplier quality and continuity.

Concentration pockets

While many parts are fragmented, certain subassemblies such as high‑end detectors and lasers have few qualified vendors, creating single‑source exposure that elevates switching costs and supplier margin extraction. Limited alternatives concentrate bargaining power in these pockets, and negotiation leverage varies across Judges Scientific’s portfolio depending on each subsidiary’s category mix. Risk mitigation relies on dual sourcing and strategic inventory.

Qualification lock‑in

Scientific instruments require rigorous qualification and compliance testing, and requalifying a new supplier demands engineering time, formal documentation and often customer revalidation cycles that can delay deployment. This qualification lock‑in reduces short‑term buyer flexibility, raising switching costs and operational risk. As a result, incumbent suppliers gain leverage and stronger bargaining power at renewal and price negotiations.

Lead‑time and scarcity

Cyclical shortages in semiconductors, precision machined parts and optics have pushed lead times well above pre‑pandemic norms, with semiconductor lead times peaking above 20 weeks in 2021–22 and remaining elevated thereafter, extending Judges Scientific production cycles. Tight supply lets suppliers prioritize larger customers and pass surcharges, while volatility disrupts schedules, strains inventory and increases working capital needs, harming delivery performance.

- Lead times: peaked >20 weeks (2021–22)

- Supplier power: prioritization and surcharges

- Impact: schedule disruption, higher inventory and working capital

Mitigation levers

Multi-sourcing, design-for-supply and strategic inventories can materially moderate supplier power for Judges Scientific, while group-level purchasing aggregates demand across c.40 operating companies (2024), improving negotiating leverage. Long-term agreements and joint development lower supply risk for critical parts, but these levers need coordination to avoid eroding niche agility.

- Multi-sourcing

- Design-for-supply

- Strategic inventories

- Group purchasing (c.40 companies, 2024)

- Long-term agreements & joint development

- Coordination vs niche agility

Precision optics supply squeeze - $16.2bn market, concentrated vendors

Judges relies on non‑commoditized precision optics/electronics (precision optics ~$16.2bn market in 2023, ~6% CAGR) and a c.40‑company group (2024), concentrating supplier power in lasers/detectors with few qualified vendors and requalification lock‑in. Covid-era lead times peaked >20 weeks (2021–22), raising inventories and working capital; multi‑sourcing and group purchasing partially mitigate this.

| Metric | Value |

|---|---|

| Precision optics market (2023) | $16.2bn |

| Optics CAGR | ~6% pa |

| Operating companies (2024) | c.40 |

| Lead times peak | >20 weeks (2021–22) |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and industry-specific disruptors affecting Judges Scientific's pricing, margins and growth prospects. Includes strategic commentary and data-driven insights for investors, management and academic use.

A concise one-sheet Porter's Five Forces for Judges Scientific—instantly highlights supplier, buyer, entrant, substitute and rivalry pressures so leadership can make fast, informed strategic decisions.

Customers Bargaining Power

Technical spec priority

Customers—universities, research institutes, industrial labs and regulated sectors—prioritise technical specs: performance, accuracy and reliability often trump unit price, reducing direct price sensitivity for mission‑critical tools. Value‑in‑use framing lets vendors sustain margins; the global scientific instruments market was estimated at about $69bn in 2024, underpinning premium pricing for high‑spec equipment.

Procurement formality

Tenders, framework agreements and grant budgets introduce structured competition for Judges Scientific suppliers. Formal procurement increases buyer leverage on discounts and service terms. Frameworks typically run 3–5 years, creating intense negotiation windows. Once placed, laboratory systems can be sticky for years; public procurement equals about 12% of GDP in OECD countries.

High switching costs

Installed instruments require extensive user training, SOPs and method validation—often entailing 40+ hours of training and validation per platform, raising direct adoption costs. Switching vendors triggers downtime, retraining and data continuity risks that can equal weeks of lost productivity and measurable revenue impact. Deep integration with LIMS and workflows locks choices, weakening buyer power post-install and reducing negotiating leverage.

Consolidated accounts

Consolidated accounts give large pharma, semiconductor and aerospace buyers strong leverage over Judges Scientific by bundling volumes, demanding global service SLAs and securing price concessions; in 2024 this trend intensified as centralized procurement prioritized single-vendor global agreements. Volume rebates and bundled service packages are commonly used as bargaining chips, while smaller academic labs remain price-sensitive with limited negotiating power.

- Large buyers: bundle volumes, demand global SLAs

- Negotiation tools: volume rebates, service packages

- Smaller labs: price-constrained, low leverage

Service and uptime

Aftermarket support, calibration and spares are mission-critical for Judges Scientific (AIM: JDG), letting buyers trade renewal timing to extract lower service fees; robust uptime guarantees allow the group to charge premium ASPs while weak service reduces switching costs and raises buyer power, pressuring margins.

Performance, uptime and validation drive premium pricing in the $69bn scientific instruments market

Customers prioritise performance, accuracy and uptime over unit price, enabling Judges Scientific (AIM: JDG) to sustain premium ASPs in a global scientific instruments market ~69bn in 2024. Procurement frameworks (3–5yr) and large buyers (global SLAs, volume rebates) increase buyer leverage, while installed-base stickiness, 40+ hr validation and LIMS integration raise switching costs. Public procurement ~12% of OECD GDP concentrates negotiation power in consolidated accounts.

| Metric | Value |

|---|---|

| Market 2024 | $69bn |

| Public procurement | ~12% GDP (OECD) |

| Training/validation | 40+ hrs |

Same Document Delivered

Judges Scientific Porter's Five Forces Analysis

You’re viewing the Judges Scientific Porter’s Five Forces Analysis and this preview is the exact document you’ll receive after purchase—no placeholders or mockups. The full file is professionally formatted, ready to download and use immediately upon payment. Content covers competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications tailored to Judges Scientific.

Description

A Must-Have Tool for Decision-Makers

Judges Scientific faces moderate supplier power, niche customer bargaining, and evolving substitute risks as it navigates specialty instruments and testing services; competitive rivalry centers on innovation and service depth. This snapshot hints at strategic pressure points—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Specialized components

Judges’ instruments rely on precision optics, sensors, vacuum parts and specialty electronics that remain non‑commoditized; the global precision optics market was about $16.2bn in 2023 and is growing ~6% annually, keeping supplier niches prized. Such niche suppliers with proprietary know‑how raise leverage on pricing and contract terms, and increase dependence on supplier quality and continuity.

Concentration pockets

While many parts are fragmented, certain subassemblies such as high‑end detectors and lasers have few qualified vendors, creating single‑source exposure that elevates switching costs and supplier margin extraction. Limited alternatives concentrate bargaining power in these pockets, and negotiation leverage varies across Judges Scientific’s portfolio depending on each subsidiary’s category mix. Risk mitigation relies on dual sourcing and strategic inventory.

Qualification lock‑in

Scientific instruments require rigorous qualification and compliance testing, and requalifying a new supplier demands engineering time, formal documentation and often customer revalidation cycles that can delay deployment. This qualification lock‑in reduces short‑term buyer flexibility, raising switching costs and operational risk. As a result, incumbent suppliers gain leverage and stronger bargaining power at renewal and price negotiations.

Lead‑time and scarcity

Cyclical shortages in semiconductors, precision machined parts and optics have pushed lead times well above pre‑pandemic norms, with semiconductor lead times peaking above 20 weeks in 2021–22 and remaining elevated thereafter, extending Judges Scientific production cycles. Tight supply lets suppliers prioritize larger customers and pass surcharges, while volatility disrupts schedules, strains inventory and increases working capital needs, harming delivery performance.

- Lead times: peaked >20 weeks (2021–22)

- Supplier power: prioritization and surcharges

- Impact: schedule disruption, higher inventory and working capital

Mitigation levers

Multi-sourcing, design-for-supply and strategic inventories can materially moderate supplier power for Judges Scientific, while group-level purchasing aggregates demand across c.40 operating companies (2024), improving negotiating leverage. Long-term agreements and joint development lower supply risk for critical parts, but these levers need coordination to avoid eroding niche agility.

- Multi-sourcing

- Design-for-supply

- Strategic inventories

- Group purchasing (c.40 companies, 2024)

- Long-term agreements & joint development

- Coordination vs niche agility

Precision optics supply squeeze - $16.2bn market, concentrated vendors

Judges relies on non‑commoditized precision optics/electronics (precision optics ~$16.2bn market in 2023, ~6% CAGR) and a c.40‑company group (2024), concentrating supplier power in lasers/detectors with few qualified vendors and requalification lock‑in. Covid-era lead times peaked >20 weeks (2021–22), raising inventories and working capital; multi‑sourcing and group purchasing partially mitigate this.

| Metric | Value |

|---|---|

| Precision optics market (2023) | $16.2bn |

| Optics CAGR | ~6% pa |

| Operating companies (2024) | c.40 |

| Lead times peak | >20 weeks (2021–22) |

What is included in the product

Analyzes competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and industry-specific disruptors affecting Judges Scientific's pricing, margins and growth prospects. Includes strategic commentary and data-driven insights for investors, management and academic use.

A concise one-sheet Porter's Five Forces for Judges Scientific—instantly highlights supplier, buyer, entrant, substitute and rivalry pressures so leadership can make fast, informed strategic decisions.

Customers Bargaining Power

Technical spec priority

Customers—universities, research institutes, industrial labs and regulated sectors—prioritise technical specs: performance, accuracy and reliability often trump unit price, reducing direct price sensitivity for mission‑critical tools. Value‑in‑use framing lets vendors sustain margins; the global scientific instruments market was estimated at about $69bn in 2024, underpinning premium pricing for high‑spec equipment.

Procurement formality

Tenders, framework agreements and grant budgets introduce structured competition for Judges Scientific suppliers. Formal procurement increases buyer leverage on discounts and service terms. Frameworks typically run 3–5 years, creating intense negotiation windows. Once placed, laboratory systems can be sticky for years; public procurement equals about 12% of GDP in OECD countries.

High switching costs

Installed instruments require extensive user training, SOPs and method validation—often entailing 40+ hours of training and validation per platform, raising direct adoption costs. Switching vendors triggers downtime, retraining and data continuity risks that can equal weeks of lost productivity and measurable revenue impact. Deep integration with LIMS and workflows locks choices, weakening buyer power post-install and reducing negotiating leverage.

Consolidated accounts

Consolidated accounts give large pharma, semiconductor and aerospace buyers strong leverage over Judges Scientific by bundling volumes, demanding global service SLAs and securing price concessions; in 2024 this trend intensified as centralized procurement prioritized single-vendor global agreements. Volume rebates and bundled service packages are commonly used as bargaining chips, while smaller academic labs remain price-sensitive with limited negotiating power.

- Large buyers: bundle volumes, demand global SLAs

- Negotiation tools: volume rebates, service packages

- Smaller labs: price-constrained, low leverage

Service and uptime

Aftermarket support, calibration and spares are mission-critical for Judges Scientific (AIM: JDG), letting buyers trade renewal timing to extract lower service fees; robust uptime guarantees allow the group to charge premium ASPs while weak service reduces switching costs and raises buyer power, pressuring margins.

Performance, uptime and validation drive premium pricing in the $69bn scientific instruments market

Customers prioritise performance, accuracy and uptime over unit price, enabling Judges Scientific (AIM: JDG) to sustain premium ASPs in a global scientific instruments market ~69bn in 2024. Procurement frameworks (3–5yr) and large buyers (global SLAs, volume rebates) increase buyer leverage, while installed-base stickiness, 40+ hr validation and LIMS integration raise switching costs. Public procurement ~12% of OECD GDP concentrates negotiation power in consolidated accounts.

| Metric | Value |

|---|---|

| Market 2024 | $69bn |

| Public procurement | ~12% GDP (OECD) |

| Training/validation | 40+ hrs |

Same Document Delivered

Judges Scientific Porter's Five Forces Analysis

You’re viewing the Judges Scientific Porter’s Five Forces Analysis and this preview is the exact document you’ll receive after purchase—no placeholders or mockups. The full file is professionally formatted, ready to download and use immediately upon payment. Content covers competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications tailored to Judges Scientific.