Jyske Bank Business Model Canvas

Bank Business Model Canvas: customer segments, value propositions, channels, revenue

Unlock the strategic blueprint behind Jyske Bank with our Business Model Canvas—outlining customer segments, value propositions, channels and revenue streams. This concise, actionable canvas reveals growth levers and cost drivers. Ideal for investors, consultants and entrepreneurs. Download the full Word/Excel pack to apply these insights.

Partnerships

Payment and card networks

Partnerships with Visa (operating in over 200 countries and territories) and Mastercard (over 210 countries and territories) plus Danish domestic rails like NETS/Dankort enable Jyske Bank to issue cards, acquire transactions and support cross-border flows. These ties give access to Visa Token Service and Mastercard Digital Enablement Service, fraud tools and dispute layers for secure digital commerce. Co‑brand and interchange deals optimize economics and UX.

Mortgage and real estate ecosystem

Alliances with mortgage funding vehicles, valuers, brokers and real estate agents streamline home financing for Jyske Bank, tapping into Denmark’s mortgage market of about 3.25 trillion DKK in 2024. These partners lift pipeline quality and shorten turnaround times, improving origination efficiency. Regulated data-sharing enhances risk assessment and pricing accuracy, while co-marketing boosts visibility among homebuyers and property investors.

Fintech and core banking vendors

Collaborations with fintechs and technology providers accelerate Jyske Banks digital features and delivered 20–30% cost-efficiency gains in 2024 through automation and platform reuse. APIs, cloud services and analytics platforms expanded innovation capacity, with cloud-hosted workloads rising markedly in 2024. Vendor relationships span core banking, payments, AML/KYC and cybersecurity, while sandbox pilots cut time-to-market for new propositions by up to 50%.

Insurers and bancassurance partners

Insurers and bancassurance partners enable Jyske Bank to offer bundled protection for retail and corporate clients, with joint product design aligning coverage to lending and savings needs; bancassurance channels accounted for about 20% of European life premiums in 2024. Revenue-sharing and white-label options diversify income, while claims and servicing integrations cut friction and speed payouts.

- Partnerships: insurer underwriting

- Product: co-designed coverage

- Revenue: fee/share models

- Service: integrated claims

Regulators and industry bodies

Jyske Bank engages constructively with the Danish Financial Supervisory Authority, the European Central Bank and Finance Denmark, ensuring compliance and stability across 3 primary regulatory/industry partners; these relationships shape policy alignment and access to market infrastructures such as TARGET2 and VP Securities. Participation in Finance Denmark and European Banking Federation fora promotes best practices and supports credibility and trust among stakeholders.

- 3 primary partners: Danish FSA, ECB, Finance Denmark

- 2 key infrastructures: TARGET2, VP Securities

- Industry fora: Finance Denmark, EBF

Partner-led payments & lending — 3.25T DKK, 20–30%

Key partnerships (Visa, Mastercard, NETS), mortgage funders, fintechs, insurers and regulators underpin Jyske Bank’s payments, origination, digital and insurance capabilities. 2024 metrics: Danish mortgage market ~3.25 trillion DKK; 20–30% cost-efficiency from automation; bancassurance ~20% EU life premiums; card networks cover 200–210+ countries.

| Metric | Value (2024) |

|---|---|

| Danish mortgage market | 3.25 trillion DKK |

| Digital cost-efficiency | 20–30% |

| Bancassurance share | ~20% |

| Card network reach | 200–210+ countries |

| Regulatory partners | 3 primary |

What is included in the product

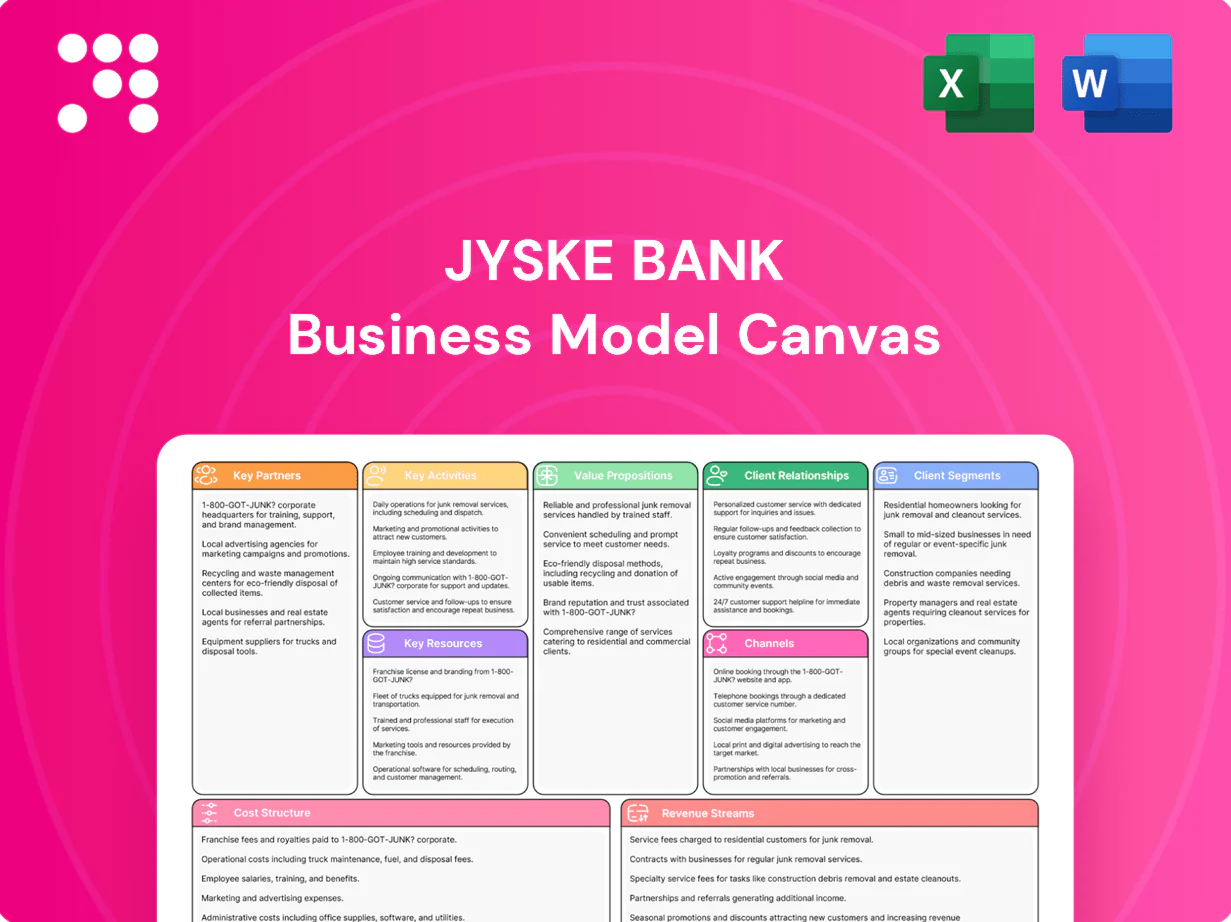

A concise, pre-built Business Model Canvas for Jyske Bank mapping all 9 blocks—customer segments, value propositions, channels, revenue streams, key resources, partners, activities, cost structure and customer relationships—aligned with real-world operations, competitive advantages and linked SWOT insights for presentations, investor discussions and strategic decision-making.

High-level view of Jyske Bank’s business model with editable cells that relieve pain by quickly pinpointing revenue streams, cost drivers and customer segments for faster decision-making.

Activities

Lending and mortgage origination

Jyske Bank structures, prices and underwrites consumer, SME, corporate and mortgage loans through segment-specific credit frameworks, supporting a loan portfolio exceeding 200 billion DKK (2024). Rigorous pipeline management and continuous credit monitoring keep default rates low and portfolio quality high. Independent collateral valuation and tight documentation reduce loss-given-default. Ongoing servicing and relationship management drive retention and cross-sell of savings, insurance and advisory services.

Deposit gathering and payments

Jyske Bank attracts current and savings accounts to fund its balance sheet, holding approximately DKK 250bn in customer deposits in 2024 to support lending and liquidity. It manages transaction services and corporate cash management, offering instant payments via Denmark's real-time rails and P27 participation for cross-border clearing. The bank optimizes deposit pricing while maintaining liquidity buffers to keep LCR above 100% and CET1 around 12%.

Wealth and asset management

Jyske Bank offers advisory, discretionary mandates and funds for retail, affluent and institutional clients, backed by a group balance sheet of c. DKK 566bn (2024). Portfolio construction, in-house research and centralized risk oversight drive outcomes and performance targets. Distribution via 70+ branches plus digital channels expands reach, while operational excellence and compliance enable scalable delivery.

Digital product development

Jyske Bank builds and iterates mobile, online banking and APIs to serve a digitally active Danish market (Eurostat 2024: 95% of Danes use online banking). UX, data analytics and automation boost engagement and efficiency; continuous delivery and cybersecurity hardening (IBM 2024: avg breach cost 4.45 million USD) protect services. Partner integrations accelerate time-to-market and innovation.

- Mobile, online, API development

- UX, analytics, automation

- Continuous delivery, cyber hardening

- Partner integrations for speed

Risk, compliance, and treasury

Credit, market, liquidity and operational risks are managed under Basel/CRR frameworks (CET1 min 4.5% plus 2.5% conservation buffer) and EU prudential rules; AML/KYC, sanctions and conduct controls protect the franchise. Treasury manages funding, interest-rate risk and capital allocation while stress testing and regulatory reporting (LCR 100%+) underpin resilience.

- Regulatory minima: CET1 7.0%

- LCR target: 100%+

- Key controls: AML/KYC, sanctions, conduct

- Core tasks: funding, IRR, capital, stress tests

Resilient lender with >200bn DKK loans, ~250bn DKK deposits

Jyske Bank originates, prices and services consumer, SME, corporate and mortgage loans (loan book >200bn DKK in 2024) while managing credit, collateral and collections to preserve asset quality. It funds lending via customer deposits (~250bn DKK, 2024), optimises liquidity and maintains LCR >100% and CET1 ~12%. Wealth management (AUM via group balance sheet c.566bn DKK, 2024), digital platforms and API integrations drive distribution and cross-sell.

| Metric | 2024 |

|---|---|

| Loan portfolio | >200bn DKK |

| Customer deposits | ~250bn DKK |

| Group balance sheet | ~566bn DKK |

| CET1 | ~12% |

| LCR | >100% |

Full Version Awaits

Business Model Canvas

The Jyske Bank Business Model Canvas you’re previewing is the actual deliverable—not a mockup—and reflects the full structure, headings, and content you’ll receive after purchase. When you complete your order, you’ll get this same professional, ready-to-edit document in downloadable formats for immediate use. No extras, no placeholders—what you see is what you’ll own.

Bank Business Model Canvas: customer segments, value propositions, channels, revenue

Unlock the strategic blueprint behind Jyske Bank with our Business Model Canvas—outlining customer segments, value propositions, channels and revenue streams. This concise, actionable canvas reveals growth levers and cost drivers. Ideal for investors, consultants and entrepreneurs. Download the full Word/Excel pack to apply these insights.

Partnerships

Payment and card networks

Partnerships with Visa (operating in over 200 countries and territories) and Mastercard (over 210 countries and territories) plus Danish domestic rails like NETS/Dankort enable Jyske Bank to issue cards, acquire transactions and support cross-border flows. These ties give access to Visa Token Service and Mastercard Digital Enablement Service, fraud tools and dispute layers for secure digital commerce. Co‑brand and interchange deals optimize economics and UX.

Mortgage and real estate ecosystem

Alliances with mortgage funding vehicles, valuers, brokers and real estate agents streamline home financing for Jyske Bank, tapping into Denmark’s mortgage market of about 3.25 trillion DKK in 2024. These partners lift pipeline quality and shorten turnaround times, improving origination efficiency. Regulated data-sharing enhances risk assessment and pricing accuracy, while co-marketing boosts visibility among homebuyers and property investors.

Fintech and core banking vendors

Collaborations with fintechs and technology providers accelerate Jyske Banks digital features and delivered 20–30% cost-efficiency gains in 2024 through automation and platform reuse. APIs, cloud services and analytics platforms expanded innovation capacity, with cloud-hosted workloads rising markedly in 2024. Vendor relationships span core banking, payments, AML/KYC and cybersecurity, while sandbox pilots cut time-to-market for new propositions by up to 50%.

Insurers and bancassurance partners

Insurers and bancassurance partners enable Jyske Bank to offer bundled protection for retail and corporate clients, with joint product design aligning coverage to lending and savings needs; bancassurance channels accounted for about 20% of European life premiums in 2024. Revenue-sharing and white-label options diversify income, while claims and servicing integrations cut friction and speed payouts.

- Partnerships: insurer underwriting

- Product: co-designed coverage

- Revenue: fee/share models

- Service: integrated claims

Regulators and industry bodies

Jyske Bank engages constructively with the Danish Financial Supervisory Authority, the European Central Bank and Finance Denmark, ensuring compliance and stability across 3 primary regulatory/industry partners; these relationships shape policy alignment and access to market infrastructures such as TARGET2 and VP Securities. Participation in Finance Denmark and European Banking Federation fora promotes best practices and supports credibility and trust among stakeholders.

- 3 primary partners: Danish FSA, ECB, Finance Denmark

- 2 key infrastructures: TARGET2, VP Securities

- Industry fora: Finance Denmark, EBF

Partner-led payments & lending — 3.25T DKK, 20–30%

Key partnerships (Visa, Mastercard, NETS), mortgage funders, fintechs, insurers and regulators underpin Jyske Bank’s payments, origination, digital and insurance capabilities. 2024 metrics: Danish mortgage market ~3.25 trillion DKK; 20–30% cost-efficiency from automation; bancassurance ~20% EU life premiums; card networks cover 200–210+ countries.

| Metric | Value (2024) |

|---|---|

| Danish mortgage market | 3.25 trillion DKK |

| Digital cost-efficiency | 20–30% |

| Bancassurance share | ~20% |

| Card network reach | 200–210+ countries |

| Regulatory partners | 3 primary |

What is included in the product

A concise, pre-built Business Model Canvas for Jyske Bank mapping all 9 blocks—customer segments, value propositions, channels, revenue streams, key resources, partners, activities, cost structure and customer relationships—aligned with real-world operations, competitive advantages and linked SWOT insights for presentations, investor discussions and strategic decision-making.

High-level view of Jyske Bank’s business model with editable cells that relieve pain by quickly pinpointing revenue streams, cost drivers and customer segments for faster decision-making.

Activities

Lending and mortgage origination

Jyske Bank structures, prices and underwrites consumer, SME, corporate and mortgage loans through segment-specific credit frameworks, supporting a loan portfolio exceeding 200 billion DKK (2024). Rigorous pipeline management and continuous credit monitoring keep default rates low and portfolio quality high. Independent collateral valuation and tight documentation reduce loss-given-default. Ongoing servicing and relationship management drive retention and cross-sell of savings, insurance and advisory services.

Deposit gathering and payments

Jyske Bank attracts current and savings accounts to fund its balance sheet, holding approximately DKK 250bn in customer deposits in 2024 to support lending and liquidity. It manages transaction services and corporate cash management, offering instant payments via Denmark's real-time rails and P27 participation for cross-border clearing. The bank optimizes deposit pricing while maintaining liquidity buffers to keep LCR above 100% and CET1 around 12%.

Wealth and asset management

Jyske Bank offers advisory, discretionary mandates and funds for retail, affluent and institutional clients, backed by a group balance sheet of c. DKK 566bn (2024). Portfolio construction, in-house research and centralized risk oversight drive outcomes and performance targets. Distribution via 70+ branches plus digital channels expands reach, while operational excellence and compliance enable scalable delivery.

Digital product development

Jyske Bank builds and iterates mobile, online banking and APIs to serve a digitally active Danish market (Eurostat 2024: 95% of Danes use online banking). UX, data analytics and automation boost engagement and efficiency; continuous delivery and cybersecurity hardening (IBM 2024: avg breach cost 4.45 million USD) protect services. Partner integrations accelerate time-to-market and innovation.

- Mobile, online, API development

- UX, analytics, automation

- Continuous delivery, cyber hardening

- Partner integrations for speed

Risk, compliance, and treasury

Credit, market, liquidity and operational risks are managed under Basel/CRR frameworks (CET1 min 4.5% plus 2.5% conservation buffer) and EU prudential rules; AML/KYC, sanctions and conduct controls protect the franchise. Treasury manages funding, interest-rate risk and capital allocation while stress testing and regulatory reporting (LCR 100%+) underpin resilience.

- Regulatory minima: CET1 7.0%

- LCR target: 100%+

- Key controls: AML/KYC, sanctions, conduct

- Core tasks: funding, IRR, capital, stress tests

Resilient lender with >200bn DKK loans, ~250bn DKK deposits

Jyske Bank originates, prices and services consumer, SME, corporate and mortgage loans (loan book >200bn DKK in 2024) while managing credit, collateral and collections to preserve asset quality. It funds lending via customer deposits (~250bn DKK, 2024), optimises liquidity and maintains LCR >100% and CET1 ~12%. Wealth management (AUM via group balance sheet c.566bn DKK, 2024), digital platforms and API integrations drive distribution and cross-sell.

| Metric | 2024 |

|---|---|

| Loan portfolio | >200bn DKK |

| Customer deposits | ~250bn DKK |

| Group balance sheet | ~566bn DKK |

| CET1 | ~12% |

| LCR | >100% |

Full Version Awaits

Business Model Canvas

The Jyske Bank Business Model Canvas you’re previewing is the actual deliverable—not a mockup—and reflects the full structure, headings, and content you’ll receive after purchase. When you complete your order, you’ll get this same professional, ready-to-edit document in downloadable formats for immediate use. No extras, no placeholders—what you see is what you’ll own.

Original: $10.00

-65%$10.00

$3.50Description

Bank Business Model Canvas: customer segments, value propositions, channels, revenue

Unlock the strategic blueprint behind Jyske Bank with our Business Model Canvas—outlining customer segments, value propositions, channels and revenue streams. This concise, actionable canvas reveals growth levers and cost drivers. Ideal for investors, consultants and entrepreneurs. Download the full Word/Excel pack to apply these insights.

Partnerships

Payment and card networks

Partnerships with Visa (operating in over 200 countries and territories) and Mastercard (over 210 countries and territories) plus Danish domestic rails like NETS/Dankort enable Jyske Bank to issue cards, acquire transactions and support cross-border flows. These ties give access to Visa Token Service and Mastercard Digital Enablement Service, fraud tools and dispute layers for secure digital commerce. Co‑brand and interchange deals optimize economics and UX.

Mortgage and real estate ecosystem

Alliances with mortgage funding vehicles, valuers, brokers and real estate agents streamline home financing for Jyske Bank, tapping into Denmark’s mortgage market of about 3.25 trillion DKK in 2024. These partners lift pipeline quality and shorten turnaround times, improving origination efficiency. Regulated data-sharing enhances risk assessment and pricing accuracy, while co-marketing boosts visibility among homebuyers and property investors.

Fintech and core banking vendors

Collaborations with fintechs and technology providers accelerate Jyske Banks digital features and delivered 20–30% cost-efficiency gains in 2024 through automation and platform reuse. APIs, cloud services and analytics platforms expanded innovation capacity, with cloud-hosted workloads rising markedly in 2024. Vendor relationships span core banking, payments, AML/KYC and cybersecurity, while sandbox pilots cut time-to-market for new propositions by up to 50%.

Insurers and bancassurance partners

Insurers and bancassurance partners enable Jyske Bank to offer bundled protection for retail and corporate clients, with joint product design aligning coverage to lending and savings needs; bancassurance channels accounted for about 20% of European life premiums in 2024. Revenue-sharing and white-label options diversify income, while claims and servicing integrations cut friction and speed payouts.

- Partnerships: insurer underwriting

- Product: co-designed coverage

- Revenue: fee/share models

- Service: integrated claims

Regulators and industry bodies

Jyske Bank engages constructively with the Danish Financial Supervisory Authority, the European Central Bank and Finance Denmark, ensuring compliance and stability across 3 primary regulatory/industry partners; these relationships shape policy alignment and access to market infrastructures such as TARGET2 and VP Securities. Participation in Finance Denmark and European Banking Federation fora promotes best practices and supports credibility and trust among stakeholders.

- 3 primary partners: Danish FSA, ECB, Finance Denmark

- 2 key infrastructures: TARGET2, VP Securities

- Industry fora: Finance Denmark, EBF

Partner-led payments & lending — 3.25T DKK, 20–30%

Key partnerships (Visa, Mastercard, NETS), mortgage funders, fintechs, insurers and regulators underpin Jyske Bank’s payments, origination, digital and insurance capabilities. 2024 metrics: Danish mortgage market ~3.25 trillion DKK; 20–30% cost-efficiency from automation; bancassurance ~20% EU life premiums; card networks cover 200–210+ countries.

| Metric | Value (2024) |

|---|---|

| Danish mortgage market | 3.25 trillion DKK |

| Digital cost-efficiency | 20–30% |

| Bancassurance share | ~20% |

| Card network reach | 200–210+ countries |

| Regulatory partners | 3 primary |

What is included in the product

A concise, pre-built Business Model Canvas for Jyske Bank mapping all 9 blocks—customer segments, value propositions, channels, revenue streams, key resources, partners, activities, cost structure and customer relationships—aligned with real-world operations, competitive advantages and linked SWOT insights for presentations, investor discussions and strategic decision-making.

High-level view of Jyske Bank’s business model with editable cells that relieve pain by quickly pinpointing revenue streams, cost drivers and customer segments for faster decision-making.

Activities

Lending and mortgage origination

Jyske Bank structures, prices and underwrites consumer, SME, corporate and mortgage loans through segment-specific credit frameworks, supporting a loan portfolio exceeding 200 billion DKK (2024). Rigorous pipeline management and continuous credit monitoring keep default rates low and portfolio quality high. Independent collateral valuation and tight documentation reduce loss-given-default. Ongoing servicing and relationship management drive retention and cross-sell of savings, insurance and advisory services.

Deposit gathering and payments

Jyske Bank attracts current and savings accounts to fund its balance sheet, holding approximately DKK 250bn in customer deposits in 2024 to support lending and liquidity. It manages transaction services and corporate cash management, offering instant payments via Denmark's real-time rails and P27 participation for cross-border clearing. The bank optimizes deposit pricing while maintaining liquidity buffers to keep LCR above 100% and CET1 around 12%.

Wealth and asset management

Jyske Bank offers advisory, discretionary mandates and funds for retail, affluent and institutional clients, backed by a group balance sheet of c. DKK 566bn (2024). Portfolio construction, in-house research and centralized risk oversight drive outcomes and performance targets. Distribution via 70+ branches plus digital channels expands reach, while operational excellence and compliance enable scalable delivery.

Digital product development

Jyske Bank builds and iterates mobile, online banking and APIs to serve a digitally active Danish market (Eurostat 2024: 95% of Danes use online banking). UX, data analytics and automation boost engagement and efficiency; continuous delivery and cybersecurity hardening (IBM 2024: avg breach cost 4.45 million USD) protect services. Partner integrations accelerate time-to-market and innovation.

- Mobile, online, API development

- UX, analytics, automation

- Continuous delivery, cyber hardening

- Partner integrations for speed

Risk, compliance, and treasury

Credit, market, liquidity and operational risks are managed under Basel/CRR frameworks (CET1 min 4.5% plus 2.5% conservation buffer) and EU prudential rules; AML/KYC, sanctions and conduct controls protect the franchise. Treasury manages funding, interest-rate risk and capital allocation while stress testing and regulatory reporting (LCR 100%+) underpin resilience.

- Regulatory minima: CET1 7.0%

- LCR target: 100%+

- Key controls: AML/KYC, sanctions, conduct

- Core tasks: funding, IRR, capital, stress tests

Resilient lender with >200bn DKK loans, ~250bn DKK deposits

Jyske Bank originates, prices and services consumer, SME, corporate and mortgage loans (loan book >200bn DKK in 2024) while managing credit, collateral and collections to preserve asset quality. It funds lending via customer deposits (~250bn DKK, 2024), optimises liquidity and maintains LCR >100% and CET1 ~12%. Wealth management (AUM via group balance sheet c.566bn DKK, 2024), digital platforms and API integrations drive distribution and cross-sell.

| Metric | 2024 |

|---|---|

| Loan portfolio | >200bn DKK |

| Customer deposits | ~250bn DKK |

| Group balance sheet | ~566bn DKK |

| CET1 | ~12% |

| LCR | >100% |

Full Version Awaits

Business Model Canvas

The Jyske Bank Business Model Canvas you’re previewing is the actual deliverable—not a mockup—and reflects the full structure, headings, and content you’ll receive after purchase. When you complete your order, you’ll get this same professional, ready-to-edit document in downloadable formats for immediate use. No extras, no placeholders—what you see is what you’ll own.