Kadant Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

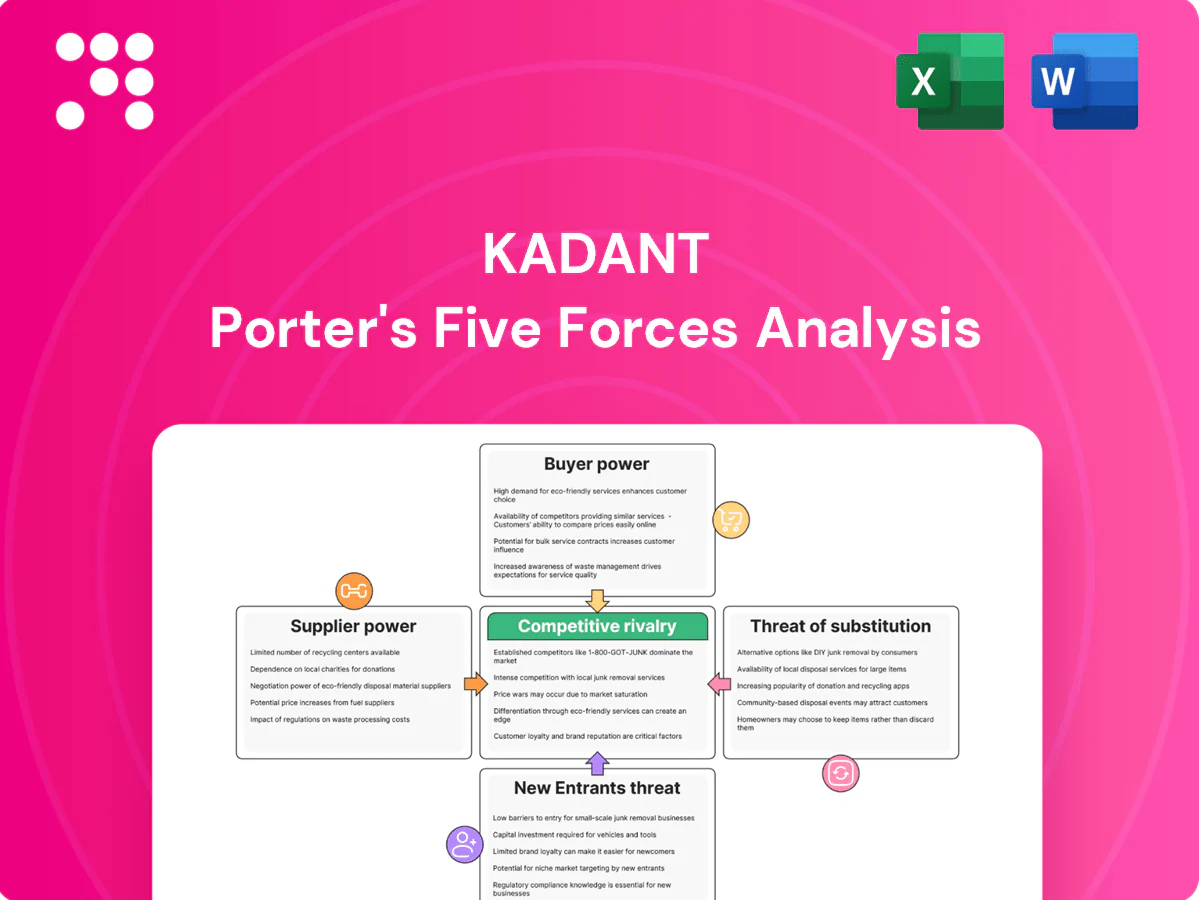

Kadant operates in a niche industrial technology market where supplier relationships, moderate buyer bargaining, and steady but specialized rivalries define margins and innovation incentives. Threats from substitutes and new entrants are limited but evolving with automation and recycling trends. This snapshot highlights key pressures—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Specialized components, limited sources

Many Kadant systems require precision castings, seals, and engineered alloys sourced from a handful of qualified vendors, often resulting in lead times of 8–16 weeks and limited alternatives. Qualification and testing can add 3–6 months, raising switching costs. This concentration gives suppliers pricing and delivery leverage, pressuring margins and inventory levels.

Commodity inputs temper leverage

Commodity inputs temper supplier leverage: steel, fittings and standard electronics are widely available from multiple global vendors, keeping supplier concentration low. In 2024 Kadant uses competitive bidding and hedging to mitigate price spikes and preserve margins. Its scale and multi-sourcing reduce single-supplier dependence and switching risk. Commodity cycles can still pressure margins but remain manageable with procurement controls.

Quality and reliability criticality

Performance and mill uptime, typically targeted above 90% in the pulp and paper sector, make component reliability critical and increase supplier influence over Kadant. High failure risk discourages rapid supplier changes, raising switching costs and procurement lead times. Tight tolerances and industry certifications limit qualified vendors, concentrating supply and enabling a quality premium that supports supplier pricing power.

Global footprint enables optionality

Kadant’s global footprint enables regional supplier diversification, allowing nearshoring and dual-sourcing that reduce geopolitical and logistics risks while aggregating demand across sites to negotiate improved terms.

However, regional qualification of suppliers increases complexity and adds certification and logistics costs, tempering some bargaining gains.

- regional diversification

- nearshoring and dual-sourcing

- demand aggregation for better terms

- qualification complexity and cost

ESG and compliance constraints

Sustainable sourcing and regulatory compliance narrow Kadant’s vendor pool, with REACH covering ~22,000 substances and RoHS restricting hazardous components, while traceability and industry audits filter out lower-cost, noncompliant suppliers. This elevates entry barriers for new vendors and can raise input costs, and suppliers with verified ESG credentials secure stronger negotiation leverage and price premiums.

- REACH ~22,000 substances

- RoHS limits hazardous components

- Audits/traceability exclude low-cost vendors

- ESG-certified suppliers gain pricing power

Supplier concentration and REACH compliance boost vendor leverage, squeezing margins

Supplier concentration for precision castings and alloys (8–16 week lead times; 3–6 month qualification) gives vendors pricing/delivery leverage, pressuring margins. Commodity inputs (steel, electronics) remain competitive; 2024 bidding/hedging reduced volatility. Reliability (mill uptime >90%) and ESG/REACH compliance (~22,000 substances) raise switching costs and favor certified suppliers.

| Metric | 2024 Value |

|---|---|

| Precision lead time | 8–16 weeks |

| Qualification time | 3–6 months |

| Mill uptime target | >90% |

| REACH scope | ~22,000 substances |

What is included in the product

Concise Porter's Five Forces assessment for Kadant that uncovers competitive drivers, supplier and buyer power, threat of entrants and substitutes, and highlights disruptive forces and strategic vulnerabilities.

One-sheet Kadant Porter’s Five Forces summary that highlights relief points—instantly pinpoint supplier or buyer pressure, benchmark threat levels, and export clean visuals for decks to accelerate strategic decisions.

Customers Bargaining Power

Concentrated, professional purchasers

Paper, packaging and tissue producers are sizable, sophisticated buyers — large integrated players such as International Paper, WestRock, Smurfit Kappa, UPM and SCA drive procurement trends. Centralized procurement teams and competitive tenders markedly heighten price pressure on suppliers. Buyers routinely benchmark equipment and services across global vendors, giving them strong negotiation leverage on new equipment awards.

High switching costs in aftermarket

Installed-base parts, wear components, and service are highly tailored to Kadant designs, creating technical barriers that raise switching costs for customers. Downtime risk and compatibility concerns materially reduce buyers willingness to change suppliers, while long equipment lifecycles lock in recurring spare-part and service revenue streams. These factors collectively weaken buyer bargaining power on spares and services.

Performance over price trade-offs

Energy efficiency, yield and water savings—which can represent roughly 20–30% of mill operating costs—directly boost margins, so buyers accept higher upfront prices for solutions that lift OEE and sustainability. A 2024 industry trend shows over 60% of mills prioritize efficiency investments, shifting negotiations from unit price to total cost of ownership. Clear, measured ROI case studies (payback often <3 years) blunt buyer leverage and reduce pure price haggling.

Cyclical demand and budget constraints

Industry cycles and pulp-price volatility drive capex timing; in 2024 pulp markets remained volatile, amplifying project deferrals as buyers sought discounts in downturns while urgent replacement demand in upcycles reduced price sensitivity. Kadant’s diversified end-markets (paper, packaging, tissue, fiber) partly smooth revenue swings and bargaining pressure.

- Buyers defer in downturns, push discounts

- Upcycles lower price elasticity

- 2024 pulp volatility raised buyer leverage

- Kadant diversification mitigates exposure

Multi-year contracts and standards

Framework agreements and plant standardization lock vendors in by creating volume commitments and service SLAs; Kadant reported approximately $600 million in 2024 sales, gaining predictable demand while buyers secure supply and service continuity. These contracts commonly embed price escalation clauses, shifting long-term price risk onto buyers while keeping Kadant under continuous KPI scrutiny and performance reviews.

- Volume lock-in: long-term framework agreements

- Price risk: embedded escalation clauses

- Buyer benefit: assured supply & SLAs

- Kadant impact: predictable demand, ongoing KPI oversight

Large mills drive tender pricing; ROI 3y, 20–30% energy

Kadant buyers are large, centralized mills (Kadant sales ~$600M in 2024) driving tender-based pricing and strong negotiation leverage.

Switching costs for spares/services are high due to proprietary designs, reducing buyer power on aftermarket pricing.

Efficiency ROI (payback <3y) and 20–30% energy/water impact shift focus to TCO; >60% of mills prioritized efficiency in 2024.

| Metric | Value |

|---|---|

| Kadant 2024 sales | $600M |

| Mill efficiency priority | >60% |

| Energy/water impact | 20–30% |

| Typical ROI | <3 years |

Full Version Awaits

Kadant Porter's Five Forces Analysis

This preview shows the exact Kadant Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. It covers competitive rivalry, supplier and buyer power, and threats of entry and substitution with actionable insights.

A Must-Have Tool for Decision-Makers

Kadant operates in a niche industrial technology market where supplier relationships, moderate buyer bargaining, and steady but specialized rivalries define margins and innovation incentives. Threats from substitutes and new entrants are limited but evolving with automation and recycling trends. This snapshot highlights key pressures—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Specialized components, limited sources

Many Kadant systems require precision castings, seals, and engineered alloys sourced from a handful of qualified vendors, often resulting in lead times of 8–16 weeks and limited alternatives. Qualification and testing can add 3–6 months, raising switching costs. This concentration gives suppliers pricing and delivery leverage, pressuring margins and inventory levels.

Commodity inputs temper leverage

Commodity inputs temper supplier leverage: steel, fittings and standard electronics are widely available from multiple global vendors, keeping supplier concentration low. In 2024 Kadant uses competitive bidding and hedging to mitigate price spikes and preserve margins. Its scale and multi-sourcing reduce single-supplier dependence and switching risk. Commodity cycles can still pressure margins but remain manageable with procurement controls.

Quality and reliability criticality

Performance and mill uptime, typically targeted above 90% in the pulp and paper sector, make component reliability critical and increase supplier influence over Kadant. High failure risk discourages rapid supplier changes, raising switching costs and procurement lead times. Tight tolerances and industry certifications limit qualified vendors, concentrating supply and enabling a quality premium that supports supplier pricing power.

Global footprint enables optionality

Kadant’s global footprint enables regional supplier diversification, allowing nearshoring and dual-sourcing that reduce geopolitical and logistics risks while aggregating demand across sites to negotiate improved terms.

However, regional qualification of suppliers increases complexity and adds certification and logistics costs, tempering some bargaining gains.

- regional diversification

- nearshoring and dual-sourcing

- demand aggregation for better terms

- qualification complexity and cost

ESG and compliance constraints

Sustainable sourcing and regulatory compliance narrow Kadant’s vendor pool, with REACH covering ~22,000 substances and RoHS restricting hazardous components, while traceability and industry audits filter out lower-cost, noncompliant suppliers. This elevates entry barriers for new vendors and can raise input costs, and suppliers with verified ESG credentials secure stronger negotiation leverage and price premiums.

- REACH ~22,000 substances

- RoHS limits hazardous components

- Audits/traceability exclude low-cost vendors

- ESG-certified suppliers gain pricing power

Supplier concentration and REACH compliance boost vendor leverage, squeezing margins

Supplier concentration for precision castings and alloys (8–16 week lead times; 3–6 month qualification) gives vendors pricing/delivery leverage, pressuring margins. Commodity inputs (steel, electronics) remain competitive; 2024 bidding/hedging reduced volatility. Reliability (mill uptime >90%) and ESG/REACH compliance (~22,000 substances) raise switching costs and favor certified suppliers.

| Metric | 2024 Value |

|---|---|

| Precision lead time | 8–16 weeks |

| Qualification time | 3–6 months |

| Mill uptime target | >90% |

| REACH scope | ~22,000 substances |

What is included in the product

Concise Porter's Five Forces assessment for Kadant that uncovers competitive drivers, supplier and buyer power, threat of entrants and substitutes, and highlights disruptive forces and strategic vulnerabilities.

One-sheet Kadant Porter’s Five Forces summary that highlights relief points—instantly pinpoint supplier or buyer pressure, benchmark threat levels, and export clean visuals for decks to accelerate strategic decisions.

Customers Bargaining Power

Concentrated, professional purchasers

Paper, packaging and tissue producers are sizable, sophisticated buyers — large integrated players such as International Paper, WestRock, Smurfit Kappa, UPM and SCA drive procurement trends. Centralized procurement teams and competitive tenders markedly heighten price pressure on suppliers. Buyers routinely benchmark equipment and services across global vendors, giving them strong negotiation leverage on new equipment awards.

High switching costs in aftermarket

Installed-base parts, wear components, and service are highly tailored to Kadant designs, creating technical barriers that raise switching costs for customers. Downtime risk and compatibility concerns materially reduce buyers willingness to change suppliers, while long equipment lifecycles lock in recurring spare-part and service revenue streams. These factors collectively weaken buyer bargaining power on spares and services.

Performance over price trade-offs

Energy efficiency, yield and water savings—which can represent roughly 20–30% of mill operating costs—directly boost margins, so buyers accept higher upfront prices for solutions that lift OEE and sustainability. A 2024 industry trend shows over 60% of mills prioritize efficiency investments, shifting negotiations from unit price to total cost of ownership. Clear, measured ROI case studies (payback often <3 years) blunt buyer leverage and reduce pure price haggling.

Cyclical demand and budget constraints

Industry cycles and pulp-price volatility drive capex timing; in 2024 pulp markets remained volatile, amplifying project deferrals as buyers sought discounts in downturns while urgent replacement demand in upcycles reduced price sensitivity. Kadant’s diversified end-markets (paper, packaging, tissue, fiber) partly smooth revenue swings and bargaining pressure.

- Buyers defer in downturns, push discounts

- Upcycles lower price elasticity

- 2024 pulp volatility raised buyer leverage

- Kadant diversification mitigates exposure

Multi-year contracts and standards

Framework agreements and plant standardization lock vendors in by creating volume commitments and service SLAs; Kadant reported approximately $600 million in 2024 sales, gaining predictable demand while buyers secure supply and service continuity. These contracts commonly embed price escalation clauses, shifting long-term price risk onto buyers while keeping Kadant under continuous KPI scrutiny and performance reviews.

- Volume lock-in: long-term framework agreements

- Price risk: embedded escalation clauses

- Buyer benefit: assured supply & SLAs

- Kadant impact: predictable demand, ongoing KPI oversight

Large mills drive tender pricing; ROI 3y, 20–30% energy

Kadant buyers are large, centralized mills (Kadant sales ~$600M in 2024) driving tender-based pricing and strong negotiation leverage.

Switching costs for spares/services are high due to proprietary designs, reducing buyer power on aftermarket pricing.

Efficiency ROI (payback <3y) and 20–30% energy/water impact shift focus to TCO; >60% of mills prioritized efficiency in 2024.

| Metric | Value |

|---|---|

| Kadant 2024 sales | $600M |

| Mill efficiency priority | >60% |

| Energy/water impact | 20–30% |

| Typical ROI | <3 years |

Full Version Awaits

Kadant Porter's Five Forces Analysis

This preview shows the exact Kadant Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. It covers competitive rivalry, supplier and buyer power, and threats of entry and substitution with actionable insights.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Kadant operates in a niche industrial technology market where supplier relationships, moderate buyer bargaining, and steady but specialized rivalries define margins and innovation incentives. Threats from substitutes and new entrants are limited but evolving with automation and recycling trends. This snapshot highlights key pressures—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Specialized components, limited sources

Many Kadant systems require precision castings, seals, and engineered alloys sourced from a handful of qualified vendors, often resulting in lead times of 8–16 weeks and limited alternatives. Qualification and testing can add 3–6 months, raising switching costs. This concentration gives suppliers pricing and delivery leverage, pressuring margins and inventory levels.

Commodity inputs temper leverage

Commodity inputs temper supplier leverage: steel, fittings and standard electronics are widely available from multiple global vendors, keeping supplier concentration low. In 2024 Kadant uses competitive bidding and hedging to mitigate price spikes and preserve margins. Its scale and multi-sourcing reduce single-supplier dependence and switching risk. Commodity cycles can still pressure margins but remain manageable with procurement controls.

Quality and reliability criticality

Performance and mill uptime, typically targeted above 90% in the pulp and paper sector, make component reliability critical and increase supplier influence over Kadant. High failure risk discourages rapid supplier changes, raising switching costs and procurement lead times. Tight tolerances and industry certifications limit qualified vendors, concentrating supply and enabling a quality premium that supports supplier pricing power.

Global footprint enables optionality

Kadant’s global footprint enables regional supplier diversification, allowing nearshoring and dual-sourcing that reduce geopolitical and logistics risks while aggregating demand across sites to negotiate improved terms.

However, regional qualification of suppliers increases complexity and adds certification and logistics costs, tempering some bargaining gains.

- regional diversification

- nearshoring and dual-sourcing

- demand aggregation for better terms

- qualification complexity and cost

ESG and compliance constraints

Sustainable sourcing and regulatory compliance narrow Kadant’s vendor pool, with REACH covering ~22,000 substances and RoHS restricting hazardous components, while traceability and industry audits filter out lower-cost, noncompliant suppliers. This elevates entry barriers for new vendors and can raise input costs, and suppliers with verified ESG credentials secure stronger negotiation leverage and price premiums.

- REACH ~22,000 substances

- RoHS limits hazardous components

- Audits/traceability exclude low-cost vendors

- ESG-certified suppliers gain pricing power

Supplier concentration and REACH compliance boost vendor leverage, squeezing margins

Supplier concentration for precision castings and alloys (8–16 week lead times; 3–6 month qualification) gives vendors pricing/delivery leverage, pressuring margins. Commodity inputs (steel, electronics) remain competitive; 2024 bidding/hedging reduced volatility. Reliability (mill uptime >90%) and ESG/REACH compliance (~22,000 substances) raise switching costs and favor certified suppliers.

| Metric | 2024 Value |

|---|---|

| Precision lead time | 8–16 weeks |

| Qualification time | 3–6 months |

| Mill uptime target | >90% |

| REACH scope | ~22,000 substances |

What is included in the product

Concise Porter's Five Forces assessment for Kadant that uncovers competitive drivers, supplier and buyer power, threat of entrants and substitutes, and highlights disruptive forces and strategic vulnerabilities.

One-sheet Kadant Porter’s Five Forces summary that highlights relief points—instantly pinpoint supplier or buyer pressure, benchmark threat levels, and export clean visuals for decks to accelerate strategic decisions.

Customers Bargaining Power

Concentrated, professional purchasers

Paper, packaging and tissue producers are sizable, sophisticated buyers — large integrated players such as International Paper, WestRock, Smurfit Kappa, UPM and SCA drive procurement trends. Centralized procurement teams and competitive tenders markedly heighten price pressure on suppliers. Buyers routinely benchmark equipment and services across global vendors, giving them strong negotiation leverage on new equipment awards.

High switching costs in aftermarket

Installed-base parts, wear components, and service are highly tailored to Kadant designs, creating technical barriers that raise switching costs for customers. Downtime risk and compatibility concerns materially reduce buyers willingness to change suppliers, while long equipment lifecycles lock in recurring spare-part and service revenue streams. These factors collectively weaken buyer bargaining power on spares and services.

Performance over price trade-offs

Energy efficiency, yield and water savings—which can represent roughly 20–30% of mill operating costs—directly boost margins, so buyers accept higher upfront prices for solutions that lift OEE and sustainability. A 2024 industry trend shows over 60% of mills prioritize efficiency investments, shifting negotiations from unit price to total cost of ownership. Clear, measured ROI case studies (payback often <3 years) blunt buyer leverage and reduce pure price haggling.

Cyclical demand and budget constraints

Industry cycles and pulp-price volatility drive capex timing; in 2024 pulp markets remained volatile, amplifying project deferrals as buyers sought discounts in downturns while urgent replacement demand in upcycles reduced price sensitivity. Kadant’s diversified end-markets (paper, packaging, tissue, fiber) partly smooth revenue swings and bargaining pressure.

- Buyers defer in downturns, push discounts

- Upcycles lower price elasticity

- 2024 pulp volatility raised buyer leverage

- Kadant diversification mitigates exposure

Multi-year contracts and standards

Framework agreements and plant standardization lock vendors in by creating volume commitments and service SLAs; Kadant reported approximately $600 million in 2024 sales, gaining predictable demand while buyers secure supply and service continuity. These contracts commonly embed price escalation clauses, shifting long-term price risk onto buyers while keeping Kadant under continuous KPI scrutiny and performance reviews.

- Volume lock-in: long-term framework agreements

- Price risk: embedded escalation clauses

- Buyer benefit: assured supply & SLAs

- Kadant impact: predictable demand, ongoing KPI oversight

Large mills drive tender pricing; ROI 3y, 20–30% energy

Kadant buyers are large, centralized mills (Kadant sales ~$600M in 2024) driving tender-based pricing and strong negotiation leverage.

Switching costs for spares/services are high due to proprietary designs, reducing buyer power on aftermarket pricing.

Efficiency ROI (payback <3y) and 20–30% energy/water impact shift focus to TCO; >60% of mills prioritized efficiency in 2024.

| Metric | Value |

|---|---|

| Kadant 2024 sales | $600M |

| Mill efficiency priority | >60% |

| Energy/water impact | 20–30% |

| Typical ROI | <3 years |

Full Version Awaits

Kadant Porter's Five Forces Analysis

This preview shows the exact Kadant Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. It covers competitive rivalry, supplier and buyer power, and threats of entry and substitution with actionable insights.