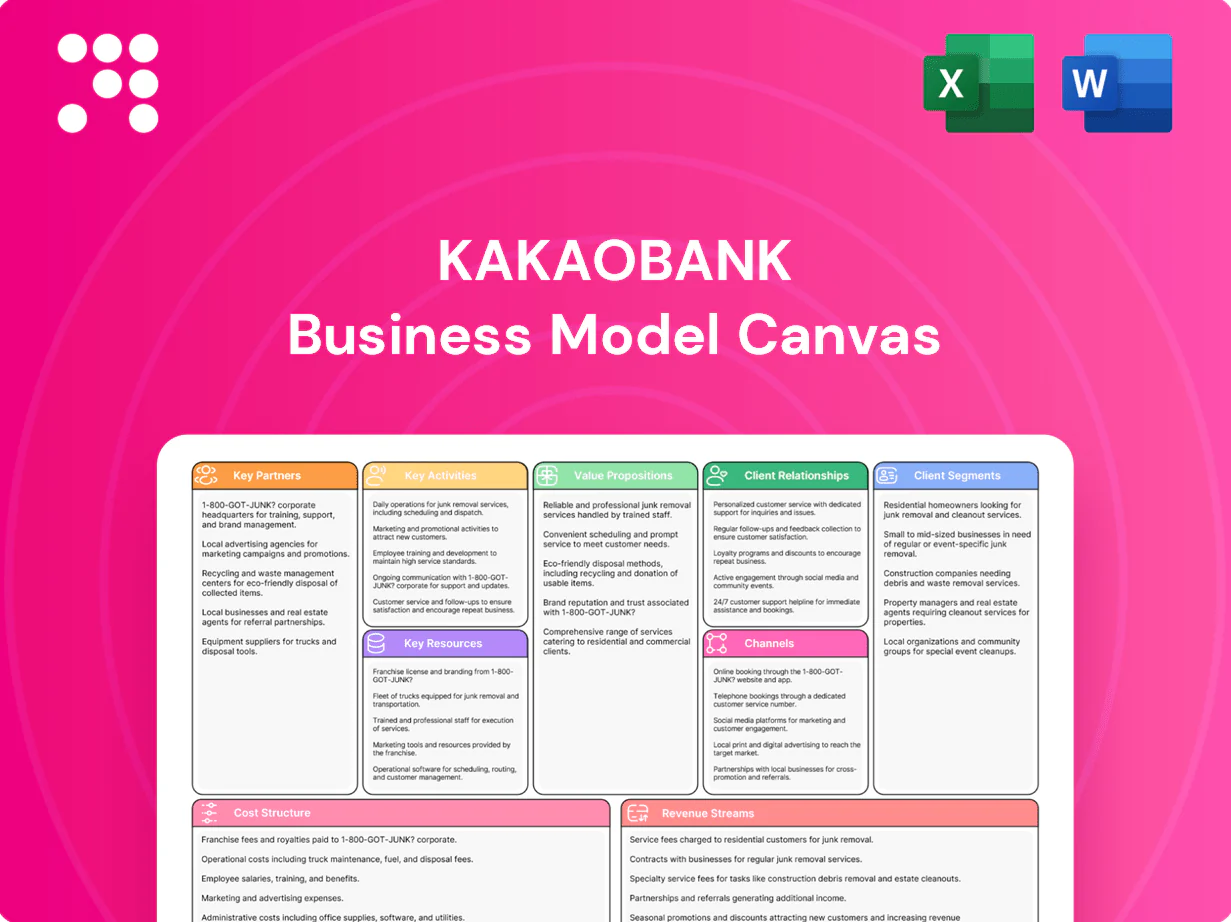

KakaoBank Business Model Canvas

Unlock a digital bank's strategic blueprint: full Business Model Canvas for investors

Unlock KakaoBank’s strategic blueprint with our full Business Model Canvas—revealing how its digital-first value propositions, partnerships, and revenue streams drive rapid customer adoption. Ideal for investors, founders, and analysts seeking actionable insights. Purchase the complete, editable Canvas to benchmark and build winning strategy.

Partnerships

Kakao Ecosystem Partners

Integration with KakaoTalk (~50M MAU in 2024), Kakao Pay (over 33M users in 2024) and Kakao affiliates boosts KakaoBank reach and daily usage. Cross-promotion and one-tap logins cut acquisition friction and lift activation rates. Consented shared data improves credit risk models and personalization. Strong ecosystem stickiness reduces churn and raises lifetime value.

Payment Networks & Card Issuers

Visa, Mastercard and domestic networks enable KakaoBank debit/credit acceptance while co-brand issuers and processors handle real-time authorization and settlement; KakaoBank served over 20 million customers in 2024. Network ties unlock global commerce and travel use-cases via cross-border acceptance and FX routing. Interchange economics improve with scale as higher card volume raises net fee income per transaction.

Regulators & Compliance Bodies

Collaboration with FSC, FSS, KFTC and KOFIU ensures KakaoBank complies with banking and AML rules while serving over 20 million customers as of 2024. Engagement in regulatory sandboxes has accelerated product rollout and pilot testing under supervised conditions. Transparent reporting to regulators builds trust and supports license stability. Ongoing policy dialogue helps shape Korea’s digital banking standards and risk frameworks.

Cloud & Cybersecurity Vendors

Cloud IaaS/PaaS deliver scalable, compliant infrastructure for KakaoBank (supporting over 18 million retail customers), with SLAs typically 99.9–99.99% and certifications like ISO 27001 and SOC 2 for audits.

Security vendors enhance fraud detection, identity verification and threat response, while pay-as-you-go cost elasticity absorbs peak demand and shrinks capex.

- SLAs: 99.9–99.99%

- Certs: ISO 27001, SOC 2

- Users: 18M+

Credit Bureaus & Data Providers

Partnerships with credit bureaus and alternative data providers give KakaoBank richer bureau signals and thin-file coverage, improving underwriting and pricing for its >18 million customers (2024). Ongoing data feeds enable near real-time portfolio monitoring and quicker remediation, while integrated dispute workflows strengthen customer trust and reduce resolution times.

- Coverage: >18M customers (2024)

- Benefit: better pricing & underwriting

- Feature: real-time portfolio feeds

- Trust: dispute/remediation processes

Ecosystem drives growth with 50M/33M/20M+ users and cards

Integration with KakaoTalk (≈50M MAU in 2024), Kakao Pay (33M users) and affiliates drives acquisition, activation and retention for KakaoBank (20M+ customers in 2024). Card networks and issuers enable global acceptance and interchange revenue. Regulators, cloud and security vendors ensure compliance, scalability and fraud protection.

| Partner | Role | Metric (2024) |

|---|---|---|

| Kakao ecosystem | Distribution/UX | 50M MAU / 33M users |

| Card networks | Payments/FX | 20M+ customers |

| Regulators & vendors | Compliance/Infra | ISO27001, SOC2 |

What is included in the product

A comprehensive Business Model Canvas tailored to KakaoBank’s digital-first banking strategy, covering customer segments, channels, value propositions, revenue streams, and cost structure across the 9 classic blocks. Reflects real-world operations and competitive advantages, includes SWOT-linked insights and is ideal for presentations, investor discussions, and strategic decision-making.

High-level view of KakaoBank’s business model with editable cells, mapping digital channels, seamless onboarding, and low-cost operations to relieve customer pain points and internal inefficiencies.

Activities

Mobile App Development

Continuous iOS/Android release cycles keep KakaoBank’s UX leading since its 2017 launch, supporting rapid growth to over 10 million customers by 2019; A/B testing drives onboarding and conversion improvements, while secure coding standards and regular penetration tests shrink attack surfaces; strong accessibility and performance engineering boost adoption and retention in mobile-first South Korea.

Digital Onboarding & KYC/AML

eKYC with biometrics enables KakaoBank to open accounts in minutes, supporting its customer base of over 20 million (2023). Sanctions, PEP and real-time transaction screening reduce compliance risk through automated flags and blocking. Ongoing CDD and risk-based EDD meet Korean regulatory thresholds and global AML standards. Process automation has driven material efficiency gains, lowering cost-to-serve by roughly a third.

Credit Underwriting & Risk

Scorecards and ML models price personal and card loans at scale, underpinning KakaoBank’s retail offering to roughly 18.1 million customers and a retail loan book near KRW 60 trillion (2024). Portfolio monitoring tracks delinquency and LGD to contain NPLs and capital strain. Collections strategies balance recovery with customer experience, using segmented, digital-first treatments. Limits and dynamic pricing are adjusted frequently to reflect macro rate and unemployment shifts.

Treasury & Liquidity Management

KakaoBank optimises deposit management to fund lending while maintaining asset-liability matching; in 2024 ALM policies actively hedge interest-rate risk across retail loan portfolios. Liquidity buffers are sized to meet Korea's regulatory liquidity ratios (LCR ≥ 100%) and internal targets, and regular stress testing informs capital allocation and contingency funding plans.

- Deposit funding → efficient loan origination

- ALM hedges → interest-rate risk management

- Liquidity buffers → regulatory LCR ≥ 100%

- Stress tests → capital & contingency planning

Customer Support & Engagement

Customer Support & Engagement at KakaoBank leverages in-app chat and call-back to resolve issues rapidly, supporting over 20 million customers in 2024 and capitalizing on South Korea's ~98% smartphone penetration (2024). Proactive alerts cut missed payments and fraud exposure, lifecycle campaigns boost cross-sell and retention, and continuous feedback loops feed the product roadmap.

- in-app chat & call-back: rapid resolution

- proactive alerts: fewer missed payments/fraud

- lifecycle campaigns: higher cross-sell & retention

- feedback loops: product roadmap input

Digital bank: ~20M customers, KRW 60T loans, -33% cost-to-serve, LCR ≥100%

KakaoBank runs rapid mobile release cycles, eKYC biometrics and ML credit models powering ~20M customers (2024) and a retail loan book ~KRW 60T (2024); process automation cut cost-to-serve ~33%. ALM hedges maintain LCR ≥100% with active stress tests; in-app support and proactive alerts leverage Korea's 98% smartphone penetration (2024) to boost retention.

| Metric | 2024 |

|---|---|

| Customers | ~20M |

| Loan book | KRW 60T |

| Cost-to-serve | -33% |

| Smartphone pen. | 98% |

| LCR | ≥100% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact KakaoBank Business Model Canvas you'll receive after purchase. It's not a mockup—this snapshot comes from the final editable file, formatted and structured as shown. After checkout you'll instantly download the complete document (Word and Excel), ready to edit, present, or share without alterations.

Unlock a digital bank's strategic blueprint: full Business Model Canvas for investors

Unlock KakaoBank’s strategic blueprint with our full Business Model Canvas—revealing how its digital-first value propositions, partnerships, and revenue streams drive rapid customer adoption. Ideal for investors, founders, and analysts seeking actionable insights. Purchase the complete, editable Canvas to benchmark and build winning strategy.

Partnerships

Kakao Ecosystem Partners

Integration with KakaoTalk (~50M MAU in 2024), Kakao Pay (over 33M users in 2024) and Kakao affiliates boosts KakaoBank reach and daily usage. Cross-promotion and one-tap logins cut acquisition friction and lift activation rates. Consented shared data improves credit risk models and personalization. Strong ecosystem stickiness reduces churn and raises lifetime value.

Payment Networks & Card Issuers

Visa, Mastercard and domestic networks enable KakaoBank debit/credit acceptance while co-brand issuers and processors handle real-time authorization and settlement; KakaoBank served over 20 million customers in 2024. Network ties unlock global commerce and travel use-cases via cross-border acceptance and FX routing. Interchange economics improve with scale as higher card volume raises net fee income per transaction.

Regulators & Compliance Bodies

Collaboration with FSC, FSS, KFTC and KOFIU ensures KakaoBank complies with banking and AML rules while serving over 20 million customers as of 2024. Engagement in regulatory sandboxes has accelerated product rollout and pilot testing under supervised conditions. Transparent reporting to regulators builds trust and supports license stability. Ongoing policy dialogue helps shape Korea’s digital banking standards and risk frameworks.

Cloud & Cybersecurity Vendors

Cloud IaaS/PaaS deliver scalable, compliant infrastructure for KakaoBank (supporting over 18 million retail customers), with SLAs typically 99.9–99.99% and certifications like ISO 27001 and SOC 2 for audits.

Security vendors enhance fraud detection, identity verification and threat response, while pay-as-you-go cost elasticity absorbs peak demand and shrinks capex.

- SLAs: 99.9–99.99%

- Certs: ISO 27001, SOC 2

- Users: 18M+

Credit Bureaus & Data Providers

Partnerships with credit bureaus and alternative data providers give KakaoBank richer bureau signals and thin-file coverage, improving underwriting and pricing for its >18 million customers (2024). Ongoing data feeds enable near real-time portfolio monitoring and quicker remediation, while integrated dispute workflows strengthen customer trust and reduce resolution times.

- Coverage: >18M customers (2024)

- Benefit: better pricing & underwriting

- Feature: real-time portfolio feeds

- Trust: dispute/remediation processes

Ecosystem drives growth with 50M/33M/20M+ users and cards

Integration with KakaoTalk (≈50M MAU in 2024), Kakao Pay (33M users) and affiliates drives acquisition, activation and retention for KakaoBank (20M+ customers in 2024). Card networks and issuers enable global acceptance and interchange revenue. Regulators, cloud and security vendors ensure compliance, scalability and fraud protection.

| Partner | Role | Metric (2024) |

|---|---|---|

| Kakao ecosystem | Distribution/UX | 50M MAU / 33M users |

| Card networks | Payments/FX | 20M+ customers |

| Regulators & vendors | Compliance/Infra | ISO27001, SOC2 |

What is included in the product

A comprehensive Business Model Canvas tailored to KakaoBank’s digital-first banking strategy, covering customer segments, channels, value propositions, revenue streams, and cost structure across the 9 classic blocks. Reflects real-world operations and competitive advantages, includes SWOT-linked insights and is ideal for presentations, investor discussions, and strategic decision-making.

High-level view of KakaoBank’s business model with editable cells, mapping digital channels, seamless onboarding, and low-cost operations to relieve customer pain points and internal inefficiencies.

Activities

Mobile App Development

Continuous iOS/Android release cycles keep KakaoBank’s UX leading since its 2017 launch, supporting rapid growth to over 10 million customers by 2019; A/B testing drives onboarding and conversion improvements, while secure coding standards and regular penetration tests shrink attack surfaces; strong accessibility and performance engineering boost adoption and retention in mobile-first South Korea.

Digital Onboarding & KYC/AML

eKYC with biometrics enables KakaoBank to open accounts in minutes, supporting its customer base of over 20 million (2023). Sanctions, PEP and real-time transaction screening reduce compliance risk through automated flags and blocking. Ongoing CDD and risk-based EDD meet Korean regulatory thresholds and global AML standards. Process automation has driven material efficiency gains, lowering cost-to-serve by roughly a third.

Credit Underwriting & Risk

Scorecards and ML models price personal and card loans at scale, underpinning KakaoBank’s retail offering to roughly 18.1 million customers and a retail loan book near KRW 60 trillion (2024). Portfolio monitoring tracks delinquency and LGD to contain NPLs and capital strain. Collections strategies balance recovery with customer experience, using segmented, digital-first treatments. Limits and dynamic pricing are adjusted frequently to reflect macro rate and unemployment shifts.

Treasury & Liquidity Management

KakaoBank optimises deposit management to fund lending while maintaining asset-liability matching; in 2024 ALM policies actively hedge interest-rate risk across retail loan portfolios. Liquidity buffers are sized to meet Korea's regulatory liquidity ratios (LCR ≥ 100%) and internal targets, and regular stress testing informs capital allocation and contingency funding plans.

- Deposit funding → efficient loan origination

- ALM hedges → interest-rate risk management

- Liquidity buffers → regulatory LCR ≥ 100%

- Stress tests → capital & contingency planning

Customer Support & Engagement

Customer Support & Engagement at KakaoBank leverages in-app chat and call-back to resolve issues rapidly, supporting over 20 million customers in 2024 and capitalizing on South Korea's ~98% smartphone penetration (2024). Proactive alerts cut missed payments and fraud exposure, lifecycle campaigns boost cross-sell and retention, and continuous feedback loops feed the product roadmap.

- in-app chat & call-back: rapid resolution

- proactive alerts: fewer missed payments/fraud

- lifecycle campaigns: higher cross-sell & retention

- feedback loops: product roadmap input

Digital bank: ~20M customers, KRW 60T loans, -33% cost-to-serve, LCR ≥100%

KakaoBank runs rapid mobile release cycles, eKYC biometrics and ML credit models powering ~20M customers (2024) and a retail loan book ~KRW 60T (2024); process automation cut cost-to-serve ~33%. ALM hedges maintain LCR ≥100% with active stress tests; in-app support and proactive alerts leverage Korea's 98% smartphone penetration (2024) to boost retention.

| Metric | 2024 |

|---|---|

| Customers | ~20M |

| Loan book | KRW 60T |

| Cost-to-serve | -33% |

| Smartphone pen. | 98% |

| LCR | ≥100% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact KakaoBank Business Model Canvas you'll receive after purchase. It's not a mockup—this snapshot comes from the final editable file, formatted and structured as shown. After checkout you'll instantly download the complete document (Word and Excel), ready to edit, present, or share without alterations.

Description

Unlock a digital bank's strategic blueprint: full Business Model Canvas for investors

Unlock KakaoBank’s strategic blueprint with our full Business Model Canvas—revealing how its digital-first value propositions, partnerships, and revenue streams drive rapid customer adoption. Ideal for investors, founders, and analysts seeking actionable insights. Purchase the complete, editable Canvas to benchmark and build winning strategy.

Partnerships

Kakao Ecosystem Partners

Integration with KakaoTalk (~50M MAU in 2024), Kakao Pay (over 33M users in 2024) and Kakao affiliates boosts KakaoBank reach and daily usage. Cross-promotion and one-tap logins cut acquisition friction and lift activation rates. Consented shared data improves credit risk models and personalization. Strong ecosystem stickiness reduces churn and raises lifetime value.

Payment Networks & Card Issuers

Visa, Mastercard and domestic networks enable KakaoBank debit/credit acceptance while co-brand issuers and processors handle real-time authorization and settlement; KakaoBank served over 20 million customers in 2024. Network ties unlock global commerce and travel use-cases via cross-border acceptance and FX routing. Interchange economics improve with scale as higher card volume raises net fee income per transaction.

Regulators & Compliance Bodies

Collaboration with FSC, FSS, KFTC and KOFIU ensures KakaoBank complies with banking and AML rules while serving over 20 million customers as of 2024. Engagement in regulatory sandboxes has accelerated product rollout and pilot testing under supervised conditions. Transparent reporting to regulators builds trust and supports license stability. Ongoing policy dialogue helps shape Korea’s digital banking standards and risk frameworks.

Cloud & Cybersecurity Vendors

Cloud IaaS/PaaS deliver scalable, compliant infrastructure for KakaoBank (supporting over 18 million retail customers), with SLAs typically 99.9–99.99% and certifications like ISO 27001 and SOC 2 for audits.

Security vendors enhance fraud detection, identity verification and threat response, while pay-as-you-go cost elasticity absorbs peak demand and shrinks capex.

- SLAs: 99.9–99.99%

- Certs: ISO 27001, SOC 2

- Users: 18M+

Credit Bureaus & Data Providers

Partnerships with credit bureaus and alternative data providers give KakaoBank richer bureau signals and thin-file coverage, improving underwriting and pricing for its >18 million customers (2024). Ongoing data feeds enable near real-time portfolio monitoring and quicker remediation, while integrated dispute workflows strengthen customer trust and reduce resolution times.

- Coverage: >18M customers (2024)

- Benefit: better pricing & underwriting

- Feature: real-time portfolio feeds

- Trust: dispute/remediation processes

Ecosystem drives growth with 50M/33M/20M+ users and cards

Integration with KakaoTalk (≈50M MAU in 2024), Kakao Pay (33M users) and affiliates drives acquisition, activation and retention for KakaoBank (20M+ customers in 2024). Card networks and issuers enable global acceptance and interchange revenue. Regulators, cloud and security vendors ensure compliance, scalability and fraud protection.

| Partner | Role | Metric (2024) |

|---|---|---|

| Kakao ecosystem | Distribution/UX | 50M MAU / 33M users |

| Card networks | Payments/FX | 20M+ customers |

| Regulators & vendors | Compliance/Infra | ISO27001, SOC2 |

What is included in the product

A comprehensive Business Model Canvas tailored to KakaoBank’s digital-first banking strategy, covering customer segments, channels, value propositions, revenue streams, and cost structure across the 9 classic blocks. Reflects real-world operations and competitive advantages, includes SWOT-linked insights and is ideal for presentations, investor discussions, and strategic decision-making.

High-level view of KakaoBank’s business model with editable cells, mapping digital channels, seamless onboarding, and low-cost operations to relieve customer pain points and internal inefficiencies.

Activities

Mobile App Development

Continuous iOS/Android release cycles keep KakaoBank’s UX leading since its 2017 launch, supporting rapid growth to over 10 million customers by 2019; A/B testing drives onboarding and conversion improvements, while secure coding standards and regular penetration tests shrink attack surfaces; strong accessibility and performance engineering boost adoption and retention in mobile-first South Korea.

Digital Onboarding & KYC/AML

eKYC with biometrics enables KakaoBank to open accounts in minutes, supporting its customer base of over 20 million (2023). Sanctions, PEP and real-time transaction screening reduce compliance risk through automated flags and blocking. Ongoing CDD and risk-based EDD meet Korean regulatory thresholds and global AML standards. Process automation has driven material efficiency gains, lowering cost-to-serve by roughly a third.

Credit Underwriting & Risk

Scorecards and ML models price personal and card loans at scale, underpinning KakaoBank’s retail offering to roughly 18.1 million customers and a retail loan book near KRW 60 trillion (2024). Portfolio monitoring tracks delinquency and LGD to contain NPLs and capital strain. Collections strategies balance recovery with customer experience, using segmented, digital-first treatments. Limits and dynamic pricing are adjusted frequently to reflect macro rate and unemployment shifts.

Treasury & Liquidity Management

KakaoBank optimises deposit management to fund lending while maintaining asset-liability matching; in 2024 ALM policies actively hedge interest-rate risk across retail loan portfolios. Liquidity buffers are sized to meet Korea's regulatory liquidity ratios (LCR ≥ 100%) and internal targets, and regular stress testing informs capital allocation and contingency funding plans.

- Deposit funding → efficient loan origination

- ALM hedges → interest-rate risk management

- Liquidity buffers → regulatory LCR ≥ 100%

- Stress tests → capital & contingency planning

Customer Support & Engagement

Customer Support & Engagement at KakaoBank leverages in-app chat and call-back to resolve issues rapidly, supporting over 20 million customers in 2024 and capitalizing on South Korea's ~98% smartphone penetration (2024). Proactive alerts cut missed payments and fraud exposure, lifecycle campaigns boost cross-sell and retention, and continuous feedback loops feed the product roadmap.

- in-app chat & call-back: rapid resolution

- proactive alerts: fewer missed payments/fraud

- lifecycle campaigns: higher cross-sell & retention

- feedback loops: product roadmap input

Digital bank: ~20M customers, KRW 60T loans, -33% cost-to-serve, LCR ≥100%

KakaoBank runs rapid mobile release cycles, eKYC biometrics and ML credit models powering ~20M customers (2024) and a retail loan book ~KRW 60T (2024); process automation cut cost-to-serve ~33%. ALM hedges maintain LCR ≥100% with active stress tests; in-app support and proactive alerts leverage Korea's 98% smartphone penetration (2024) to boost retention.

| Metric | 2024 |

|---|---|

| Customers | ~20M |

| Loan book | KRW 60T |

| Cost-to-serve | -33% |

| Smartphone pen. | 98% |

| LCR | ≥100% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact KakaoBank Business Model Canvas you'll receive after purchase. It's not a mockup—this snapshot comes from the final editable file, formatted and structured as shown. After checkout you'll instantly download the complete document (Word and Excel), ready to edit, present, or share without alterations.