Kansai Paint Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

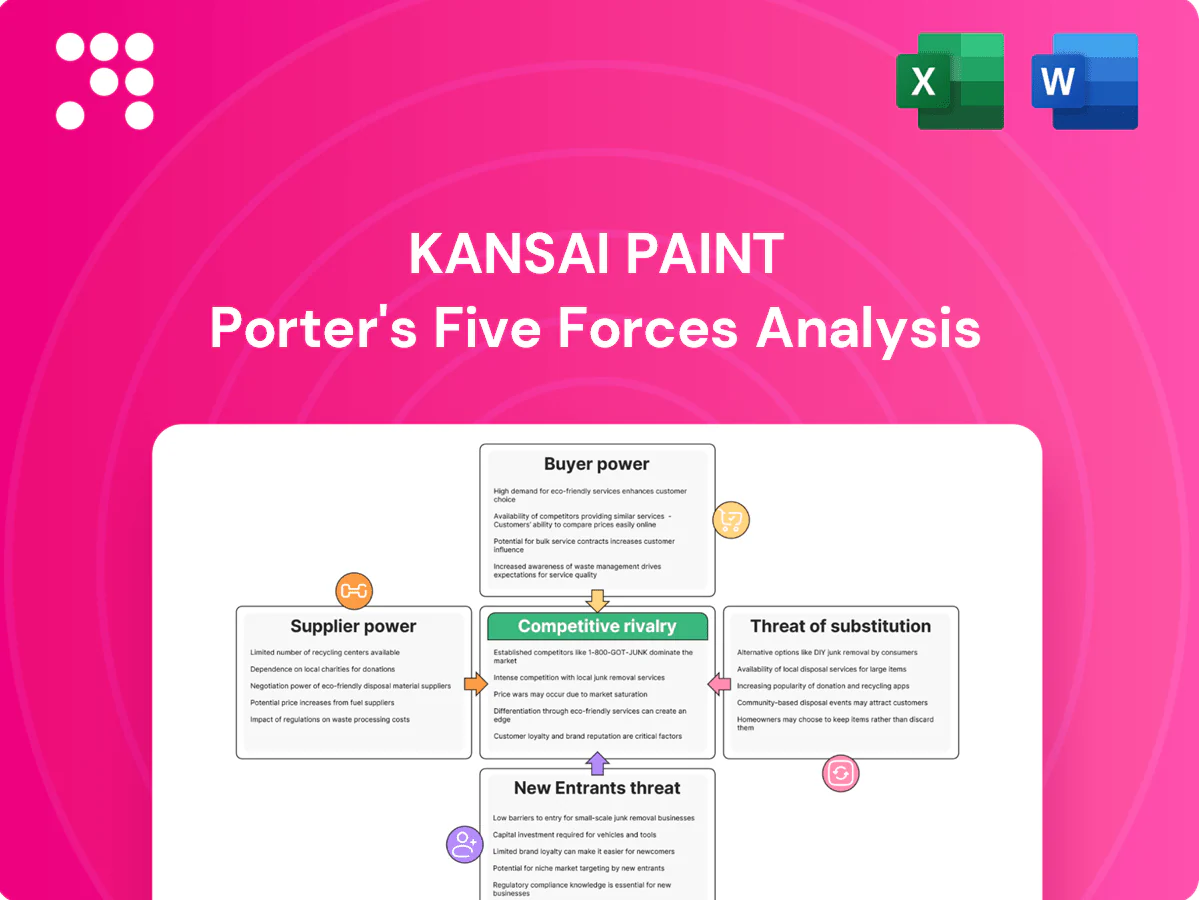

Kansai Paint faces moderate supplier power, intense rivalry with global and local coatings players, and growing pressure from substitutes and sustainability-driven shifts, while barriers to entry remain mixed across segments; this brief snapshot highlights key tensions shaping profitability. Unlock the full Porter's Five Forces Analysis to explore Kansai Paint’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material concentration

Core inputs—resins, solvents, pigments and titanium dioxide—are largely supplied by a concentrated petrochemical/specialty chemicals set; top five TiO2 producers account for roughly 60% of global capacity in 2024, elevating supplier leverage. Kansai reduces risk through multi-sourcing and regional supplier diversification and long-term contracts, yet limited alternatives for high‑purity additives and specialty grades preserve supplier bargaining power.

Commodity price volatility

Oil-linked feedstocks and TiO2, with Brent averaging about $86/bbl in 2024 and TiO2 near $2,700/ton in many markets, swing with global cycles and can compress Kansai Paint margins. Suppliers typically pass through hikes faster than paint makers can reprice contracts. Hedging and formula-based supply agreements damp spikes but do not eliminate exposure. Volatility heightens supplier leverage in tight market periods.

Switching and qualification costs

Changing a resin or pigment requires reformulation, lab and field testing and customer requalification, typically delaying launches by 3–12 months and creating strong inertia. This technical lock-in raises effective switching costs and strengthens key suppliers, often formalized in 3–5 year supply agreements. Kansai’s sustained R&D investment and global application labs expand approved alternates, reducing dependency over time.

Sustainability and compliance demands

Rising VOC limits and REACH oversight (ECHA lists over 22,000 registered substances as of 2024) plus tighter ESG procurement constrain supplier choice to compliant producers, concentrating leverage with qualified input suppliers. Certified low-VOC and bio-based inputs are scarcer and command price premiums, narrowing Kansai Paint’s supplier pool relative to its sustainability goals. Co-development partnerships can create mutual dependence and rebalance supplier power.

- REACH registrations: over 22,000 (ECHA, 2024)

- Certified inputs: limited availability, higher price premiums

- Mitigation: co-development to share IP and dependency

Scale and bargaining leverage

Kansai’s global scale provides meaningful volume leverage versus smaller rivals, supported by FY2023 consolidated net sales of ¥476.7 billion, enabling better purchase terms and logistics rates. Regional procurement hubs aggregate demand to negotiate rebates and priority allocation with suppliers, improving input cost control. In tight capacity segments such as specialty resins supplier power persists, so strategic partnerships are used to secure capacity and co-develop formulations.

- Scale: FY2023 sales ¥476.7bn

- Procurement: regional hubs for rebates/prioritization

- Risk: specialty resins — persistent supplier power

- Mitigation: strategic supplier partnerships for capacity/innovation

TiO2 supplier power: top5 60%, Brent $86, TiO2 $2,700 (2024)

Suppliers hold moderate-high power: top five TiO2 producers ~60% global capacity (2024), Brent ~$86/bbl and TiO2 ~ $2,700/ton in 2024, creating cost pass-through and margin risk. Technical switching costs (3–12 months) and REACH constraints (22,000+ registrations, 2024) reinforce supplier leverage despite Kansai’s FY2023 sales ¥476.7bn and multi-sourcing/partnerships.

| Metric | 2024/2023 |

|---|---|

| TiO2 top5 share | ~60% |

| Brent | $86/bbl (2024) |

| TiO2 price | $2,700/ton |

| REACH registrations | 22,000+ |

| Kansai sales | ¥476.7bn (FY2023) |

What is included in the product

Provides a tailored Porter's Five Forces assessment for Kansai Paint, highlighting competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and regulatory/technological disruptors shaping pricing, margins, and growth prospects.

Clear, one-sheet Porter's Five Forces for Kansai Paint—instantly highlights competitive pressures with an editable radar chart and customizable scores to reflect market shifts. Clean layout ready for decks, no macros, and seamless Excel/Word integration for fast boardroom decisions.

Customers Bargaining Power

OEM and industrial buyer concentration

Automotive and industrial OEMs purchase through large, negotiated contracts—often exceeding USD 100 million—giving them strong price leverage over suppliers. They enforce strict specifications, on-time global delivery and aftermarket service, while consolidated procurement organizations concentrate buying power. Kansai Paint faces margin pressure as OEMs push costs down and must deliver technical differentiation, service and total cost-of-ownership improvements to retain contracts.

Switching costs and qualification

Coatings are performance-critical, so switching vendors requires trials, line approvals and incurs warranty risk, raising effective switching costs and tempering buyer power; Kansai Paint reported consolidated revenues of JPY 389.8 billion for FY2023 (ended March 2024), reflecting scale that supports extensive qualification capabilities. Once alternatives are qualified, buyers can leverage competition to negotiate pricing. Kansai’s technical support network and field engineers deepen customer stickiness and reduce churn.

Price sensitivity in decorative

Retail and contractor buyers show high price sensitivity in decorative paints, with private-label and local brands often capturing over 25% share in some markets, increasing customer bargaining power. Kansai can offset price focus through brand strength, proven durability and low-VOC/low-odor claims, plus channel incentive programs and warranties that steer decisions beyond price.

Performance and service expectations

Buyers demand durability, corrosion resistance and application efficiency to lower lifecycle costs; technical service, fast color-matching and reliable logistics drive purchasing decisions and raise bargaining power. Superior service and application support reduce perceived substitutability, making service a differentiator. Kansai’s global R&D and on-site application teams function as key bargaining counters by tying customers to performance and support.

- Durability-focused buyers

- Technical service & color-matching speed

- Logistics reliability

- Kansai R&D & application support

Tendering and long-cycle contracts

Tender-driven institutional and infrastructure projects amplify buyer power for Kansai Paint as public and large private tenders dominate contract allocation; the global paints & coatings market was about USD 167 billion in 2024 and large tenders can represent 20–30% of segment volumes. Long-cycle contracts lock prices and service levels, squeezing margins in downturns, while escalation clauses mitigate input spikes; repeat-award and past-performance tilt outcomes in favour of established suppliers.

- Tenders raise buyer leverage

- Long-cycle contracts compress margins in downturns

- Escalation clauses protect against input inflation

- Past performance increases award probability

Buyer power strong: tenders 20–30%, private-labels > 25%

Customers exert strong leverage via large OEM contracts, tender-driven procurement (20–30% volumes) and price pressure in decorative channels; Kansai Paint reported JPY 389.8 billion revenue for FY2023 (ended Mar 2024) while the global market was ~USD 167 billion in 2024. Switching costs and technical service mitigate but do not eliminate buyer power; private-labels exceed 25% in some markets.

| Metric | Value |

|---|---|

| Kansai FY2023 revenue | JPY 389.8 bn |

| Global market 2024 | USD 167 bn |

| Tender share | 20–30% |

| Private-label share | >25% (some markets) |

Preview the Actual Deliverable

Kansai Paint Porter's Five Forces Analysis

This preview shows the exact Kansai Paint Porter's Five Forces analysis you'll receive—no placeholders or mockups. The full, professionally formatted document covers supplier power, buyer power, competitive rivalry, threats of entry and substitutes, and strategic implications. You'll get instant access to this identical file immediately after purchase.

A Must-Have Tool for Decision-Makers

Kansai Paint faces moderate supplier power, intense rivalry with global and local coatings players, and growing pressure from substitutes and sustainability-driven shifts, while barriers to entry remain mixed across segments; this brief snapshot highlights key tensions shaping profitability. Unlock the full Porter's Five Forces Analysis to explore Kansai Paint’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material concentration

Core inputs—resins, solvents, pigments and titanium dioxide—are largely supplied by a concentrated petrochemical/specialty chemicals set; top five TiO2 producers account for roughly 60% of global capacity in 2024, elevating supplier leverage. Kansai reduces risk through multi-sourcing and regional supplier diversification and long-term contracts, yet limited alternatives for high‑purity additives and specialty grades preserve supplier bargaining power.

Commodity price volatility

Oil-linked feedstocks and TiO2, with Brent averaging about $86/bbl in 2024 and TiO2 near $2,700/ton in many markets, swing with global cycles and can compress Kansai Paint margins. Suppliers typically pass through hikes faster than paint makers can reprice contracts. Hedging and formula-based supply agreements damp spikes but do not eliminate exposure. Volatility heightens supplier leverage in tight market periods.

Switching and qualification costs

Changing a resin or pigment requires reformulation, lab and field testing and customer requalification, typically delaying launches by 3–12 months and creating strong inertia. This technical lock-in raises effective switching costs and strengthens key suppliers, often formalized in 3–5 year supply agreements. Kansai’s sustained R&D investment and global application labs expand approved alternates, reducing dependency over time.

Sustainability and compliance demands

Rising VOC limits and REACH oversight (ECHA lists over 22,000 registered substances as of 2024) plus tighter ESG procurement constrain supplier choice to compliant producers, concentrating leverage with qualified input suppliers. Certified low-VOC and bio-based inputs are scarcer and command price premiums, narrowing Kansai Paint’s supplier pool relative to its sustainability goals. Co-development partnerships can create mutual dependence and rebalance supplier power.

- REACH registrations: over 22,000 (ECHA, 2024)

- Certified inputs: limited availability, higher price premiums

- Mitigation: co-development to share IP and dependency

Scale and bargaining leverage

Kansai’s global scale provides meaningful volume leverage versus smaller rivals, supported by FY2023 consolidated net sales of ¥476.7 billion, enabling better purchase terms and logistics rates. Regional procurement hubs aggregate demand to negotiate rebates and priority allocation with suppliers, improving input cost control. In tight capacity segments such as specialty resins supplier power persists, so strategic partnerships are used to secure capacity and co-develop formulations.

- Scale: FY2023 sales ¥476.7bn

- Procurement: regional hubs for rebates/prioritization

- Risk: specialty resins — persistent supplier power

- Mitigation: strategic supplier partnerships for capacity/innovation

TiO2 supplier power: top5 60%, Brent $86, TiO2 $2,700 (2024)

Suppliers hold moderate-high power: top five TiO2 producers ~60% global capacity (2024), Brent ~$86/bbl and TiO2 ~ $2,700/ton in 2024, creating cost pass-through and margin risk. Technical switching costs (3–12 months) and REACH constraints (22,000+ registrations, 2024) reinforce supplier leverage despite Kansai’s FY2023 sales ¥476.7bn and multi-sourcing/partnerships.

| Metric | 2024/2023 |

|---|---|

| TiO2 top5 share | ~60% |

| Brent | $86/bbl (2024) |

| TiO2 price | $2,700/ton |

| REACH registrations | 22,000+ |

| Kansai sales | ¥476.7bn (FY2023) |

What is included in the product

Provides a tailored Porter's Five Forces assessment for Kansai Paint, highlighting competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and regulatory/technological disruptors shaping pricing, margins, and growth prospects.

Clear, one-sheet Porter's Five Forces for Kansai Paint—instantly highlights competitive pressures with an editable radar chart and customizable scores to reflect market shifts. Clean layout ready for decks, no macros, and seamless Excel/Word integration for fast boardroom decisions.

Customers Bargaining Power

OEM and industrial buyer concentration

Automotive and industrial OEMs purchase through large, negotiated contracts—often exceeding USD 100 million—giving them strong price leverage over suppliers. They enforce strict specifications, on-time global delivery and aftermarket service, while consolidated procurement organizations concentrate buying power. Kansai Paint faces margin pressure as OEMs push costs down and must deliver technical differentiation, service and total cost-of-ownership improvements to retain contracts.

Switching costs and qualification

Coatings are performance-critical, so switching vendors requires trials, line approvals and incurs warranty risk, raising effective switching costs and tempering buyer power; Kansai Paint reported consolidated revenues of JPY 389.8 billion for FY2023 (ended March 2024), reflecting scale that supports extensive qualification capabilities. Once alternatives are qualified, buyers can leverage competition to negotiate pricing. Kansai’s technical support network and field engineers deepen customer stickiness and reduce churn.

Price sensitivity in decorative

Retail and contractor buyers show high price sensitivity in decorative paints, with private-label and local brands often capturing over 25% share in some markets, increasing customer bargaining power. Kansai can offset price focus through brand strength, proven durability and low-VOC/low-odor claims, plus channel incentive programs and warranties that steer decisions beyond price.

Performance and service expectations

Buyers demand durability, corrosion resistance and application efficiency to lower lifecycle costs; technical service, fast color-matching and reliable logistics drive purchasing decisions and raise bargaining power. Superior service and application support reduce perceived substitutability, making service a differentiator. Kansai’s global R&D and on-site application teams function as key bargaining counters by tying customers to performance and support.

- Durability-focused buyers

- Technical service & color-matching speed

- Logistics reliability

- Kansai R&D & application support

Tendering and long-cycle contracts

Tender-driven institutional and infrastructure projects amplify buyer power for Kansai Paint as public and large private tenders dominate contract allocation; the global paints & coatings market was about USD 167 billion in 2024 and large tenders can represent 20–30% of segment volumes. Long-cycle contracts lock prices and service levels, squeezing margins in downturns, while escalation clauses mitigate input spikes; repeat-award and past-performance tilt outcomes in favour of established suppliers.

- Tenders raise buyer leverage

- Long-cycle contracts compress margins in downturns

- Escalation clauses protect against input inflation

- Past performance increases award probability

Buyer power strong: tenders 20–30%, private-labels > 25%

Customers exert strong leverage via large OEM contracts, tender-driven procurement (20–30% volumes) and price pressure in decorative channels; Kansai Paint reported JPY 389.8 billion revenue for FY2023 (ended Mar 2024) while the global market was ~USD 167 billion in 2024. Switching costs and technical service mitigate but do not eliminate buyer power; private-labels exceed 25% in some markets.

| Metric | Value |

|---|---|

| Kansai FY2023 revenue | JPY 389.8 bn |

| Global market 2024 | USD 167 bn |

| Tender share | 20–30% |

| Private-label share | >25% (some markets) |

Preview the Actual Deliverable

Kansai Paint Porter's Five Forces Analysis

This preview shows the exact Kansai Paint Porter's Five Forces analysis you'll receive—no placeholders or mockups. The full, professionally formatted document covers supplier power, buyer power, competitive rivalry, threats of entry and substitutes, and strategic implications. You'll get instant access to this identical file immediately after purchase.

Description

A Must-Have Tool for Decision-Makers

Kansai Paint faces moderate supplier power, intense rivalry with global and local coatings players, and growing pressure from substitutes and sustainability-driven shifts, while barriers to entry remain mixed across segments; this brief snapshot highlights key tensions shaping profitability. Unlock the full Porter's Five Forces Analysis to explore Kansai Paint’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material concentration

Core inputs—resins, solvents, pigments and titanium dioxide—are largely supplied by a concentrated petrochemical/specialty chemicals set; top five TiO2 producers account for roughly 60% of global capacity in 2024, elevating supplier leverage. Kansai reduces risk through multi-sourcing and regional supplier diversification and long-term contracts, yet limited alternatives for high‑purity additives and specialty grades preserve supplier bargaining power.

Commodity price volatility

Oil-linked feedstocks and TiO2, with Brent averaging about $86/bbl in 2024 and TiO2 near $2,700/ton in many markets, swing with global cycles and can compress Kansai Paint margins. Suppliers typically pass through hikes faster than paint makers can reprice contracts. Hedging and formula-based supply agreements damp spikes but do not eliminate exposure. Volatility heightens supplier leverage in tight market periods.

Switching and qualification costs

Changing a resin or pigment requires reformulation, lab and field testing and customer requalification, typically delaying launches by 3–12 months and creating strong inertia. This technical lock-in raises effective switching costs and strengthens key suppliers, often formalized in 3–5 year supply agreements. Kansai’s sustained R&D investment and global application labs expand approved alternates, reducing dependency over time.

Sustainability and compliance demands

Rising VOC limits and REACH oversight (ECHA lists over 22,000 registered substances as of 2024) plus tighter ESG procurement constrain supplier choice to compliant producers, concentrating leverage with qualified input suppliers. Certified low-VOC and bio-based inputs are scarcer and command price premiums, narrowing Kansai Paint’s supplier pool relative to its sustainability goals. Co-development partnerships can create mutual dependence and rebalance supplier power.

- REACH registrations: over 22,000 (ECHA, 2024)

- Certified inputs: limited availability, higher price premiums

- Mitigation: co-development to share IP and dependency

Scale and bargaining leverage

Kansai’s global scale provides meaningful volume leverage versus smaller rivals, supported by FY2023 consolidated net sales of ¥476.7 billion, enabling better purchase terms and logistics rates. Regional procurement hubs aggregate demand to negotiate rebates and priority allocation with suppliers, improving input cost control. In tight capacity segments such as specialty resins supplier power persists, so strategic partnerships are used to secure capacity and co-develop formulations.

- Scale: FY2023 sales ¥476.7bn

- Procurement: regional hubs for rebates/prioritization

- Risk: specialty resins — persistent supplier power

- Mitigation: strategic supplier partnerships for capacity/innovation

TiO2 supplier power: top5 60%, Brent $86, TiO2 $2,700 (2024)

Suppliers hold moderate-high power: top five TiO2 producers ~60% global capacity (2024), Brent ~$86/bbl and TiO2 ~ $2,700/ton in 2024, creating cost pass-through and margin risk. Technical switching costs (3–12 months) and REACH constraints (22,000+ registrations, 2024) reinforce supplier leverage despite Kansai’s FY2023 sales ¥476.7bn and multi-sourcing/partnerships.

| Metric | 2024/2023 |

|---|---|

| TiO2 top5 share | ~60% |

| Brent | $86/bbl (2024) |

| TiO2 price | $2,700/ton |

| REACH registrations | 22,000+ |

| Kansai sales | ¥476.7bn (FY2023) |

What is included in the product

Provides a tailored Porter's Five Forces assessment for Kansai Paint, highlighting competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and regulatory/technological disruptors shaping pricing, margins, and growth prospects.

Clear, one-sheet Porter's Five Forces for Kansai Paint—instantly highlights competitive pressures with an editable radar chart and customizable scores to reflect market shifts. Clean layout ready for decks, no macros, and seamless Excel/Word integration for fast boardroom decisions.

Customers Bargaining Power

OEM and industrial buyer concentration

Automotive and industrial OEMs purchase through large, negotiated contracts—often exceeding USD 100 million—giving them strong price leverage over suppliers. They enforce strict specifications, on-time global delivery and aftermarket service, while consolidated procurement organizations concentrate buying power. Kansai Paint faces margin pressure as OEMs push costs down and must deliver technical differentiation, service and total cost-of-ownership improvements to retain contracts.

Switching costs and qualification

Coatings are performance-critical, so switching vendors requires trials, line approvals and incurs warranty risk, raising effective switching costs and tempering buyer power; Kansai Paint reported consolidated revenues of JPY 389.8 billion for FY2023 (ended March 2024), reflecting scale that supports extensive qualification capabilities. Once alternatives are qualified, buyers can leverage competition to negotiate pricing. Kansai’s technical support network and field engineers deepen customer stickiness and reduce churn.

Price sensitivity in decorative

Retail and contractor buyers show high price sensitivity in decorative paints, with private-label and local brands often capturing over 25% share in some markets, increasing customer bargaining power. Kansai can offset price focus through brand strength, proven durability and low-VOC/low-odor claims, plus channel incentive programs and warranties that steer decisions beyond price.

Performance and service expectations

Buyers demand durability, corrosion resistance and application efficiency to lower lifecycle costs; technical service, fast color-matching and reliable logistics drive purchasing decisions and raise bargaining power. Superior service and application support reduce perceived substitutability, making service a differentiator. Kansai’s global R&D and on-site application teams function as key bargaining counters by tying customers to performance and support.

- Durability-focused buyers

- Technical service & color-matching speed

- Logistics reliability

- Kansai R&D & application support

Tendering and long-cycle contracts

Tender-driven institutional and infrastructure projects amplify buyer power for Kansai Paint as public and large private tenders dominate contract allocation; the global paints & coatings market was about USD 167 billion in 2024 and large tenders can represent 20–30% of segment volumes. Long-cycle contracts lock prices and service levels, squeezing margins in downturns, while escalation clauses mitigate input spikes; repeat-award and past-performance tilt outcomes in favour of established suppliers.

- Tenders raise buyer leverage

- Long-cycle contracts compress margins in downturns

- Escalation clauses protect against input inflation

- Past performance increases award probability

Buyer power strong: tenders 20–30%, private-labels > 25%

Customers exert strong leverage via large OEM contracts, tender-driven procurement (20–30% volumes) and price pressure in decorative channels; Kansai Paint reported JPY 389.8 billion revenue for FY2023 (ended Mar 2024) while the global market was ~USD 167 billion in 2024. Switching costs and technical service mitigate but do not eliminate buyer power; private-labels exceed 25% in some markets.

| Metric | Value |

|---|---|

| Kansai FY2023 revenue | JPY 389.8 bn |

| Global market 2024 | USD 167 bn |

| Tender share | 20–30% |

| Private-label share | >25% (some markets) |

Preview the Actual Deliverable

Kansai Paint Porter's Five Forces Analysis

This preview shows the exact Kansai Paint Porter's Five Forces analysis you'll receive—no placeholders or mockups. The full, professionally formatted document covers supplier power, buyer power, competitive rivalry, threats of entry and substitutes, and strategic implications. You'll get instant access to this identical file immediately after purchase.