Kansai Paint PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE Analysis of Kansai Paint—three concise sections reveal how political, economic, social, and technological forces reshape its market position. Use these insights to anticipate risks and spot growth opportunities. Purchase the full report for a complete, actionable breakdown you can deploy immediately.

Political factors

Trade policies and tariffs

Shifts in tariffs on chemicals and pigments directly alter input costs and compress pricing flexibility, prompting Kansai Paint to adopt dual-supply and friend-shoring strategies; RCEP, in force since 2022 and covering about 30% of world GDP, can lower regional tariff barriers if leveraged. Regionalization increases the need to balance local production with global scale to absorb tariff shocks and preserve margins. Preferential agreements in Asia and Africa offer targeted growth corridors.

Geopolitical instability

Geopolitical instability disrupts feedstock availability and shipping lanes, raising costs and complicating insurance for paint-grade petrochemicals; Japan imports roughly 90% of its energy, making regional supply shocks material. Sanctions regimes constrain dealings with suppliers and customers in affected jurisdictions. Political risk in emerging markets forces Kansai Paint to consider plant location, inventory buffers and tariffs. Business continuity requires multi-site redundancy and elevated safety stocks.

Government industrial policies

Subsidies for EVs (global EV sales ~14 million in 2023, IEA 2024), plus infrastructure and Japan housing starts near 800,000 units in 2023 (MLIT), shift demand toward corrosion-resistant and automotive coatings. Localization mandates in China and other markets drive joint ventures and tech transfer, raising capex and licensing revenue opportunities. Public procurement increasingly specifies low-VOC/low-carbon paints, and active engagement with policy bodies aligns Kansai Paint R&D with national green priorities.

Currency and capital controls

Restrictions on forex in certain markets constrain repatriation and raw-material payments, forcing Kansai Paint to reroute cash and extend payables; global FX reserves stood near $12.9 trillion at end-2024 (IMF), underscoring active central-bank intervention. Hedging policies must price political FX risk; local-currency pricing limits volatility but raises operational complexity; treasury centralization balances liquidity and regional risk.

- FX controls → delayed repatriation/payments

- Hedging must cover political FX moves

- Local-currency pricing reduces translation risk

- Centralized treasury optimizes liquidity/risk

Regulatory harmonization efforts

APAC moves toward shared chemical standards and broader GHS adoption across 60+ economies by 2024 can streamline Kansai Paint approvals and reduce duplication. Divergences between EU REACH, US TSCA and Japan’s Chemical Substances Control Law still force tailored formulations and paperwork. Active participation in standards committees like national paint associations reduces compliance surprises and speeds multi‑jurisdiction launches.

- APAC GHS: 60+ economies (2024)

- Key divergences: REACH vs TSCA vs Japan CSCL

- Standards committee engagement: lowers regulatory delay risk

Tariffs, RCEP and Japan energy risks spur friend‑shoring, dual sourcing and coatings demand

Tariff shifts and RCEP (in force 2022, covers ~30% of world GDP) affect input costs, prompting friend‑shoring and dual sourcing to protect margins. Geopolitical shocks and Japan's ~90% energy import dependence raise feedstock, shipping and insurance risk. Policy trends (global EV sales ~14m in 2023; Japan housing starts ~800k in 2023) boost demand for automotive and low‑VOC coatings.

| Risk | Impact | Key data |

|---|---|---|

| Tariffs | Higher input costs | RCEP ~30% world GDP |

| Geopolitics | Supply/insurance shocks | Japan imports ~90% energy |

| Policy | Demand shift to low‑VOC/auto | EVs ~14m (2023); housing ~800k (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Kansai Paint, using current data and trends to highlight region- and industry-specific risks and opportunities; designed for executives and investors with forward-looking insights, scenario implications, and deck-ready findings that link external drivers to competitive strategy and regulatory compliance.

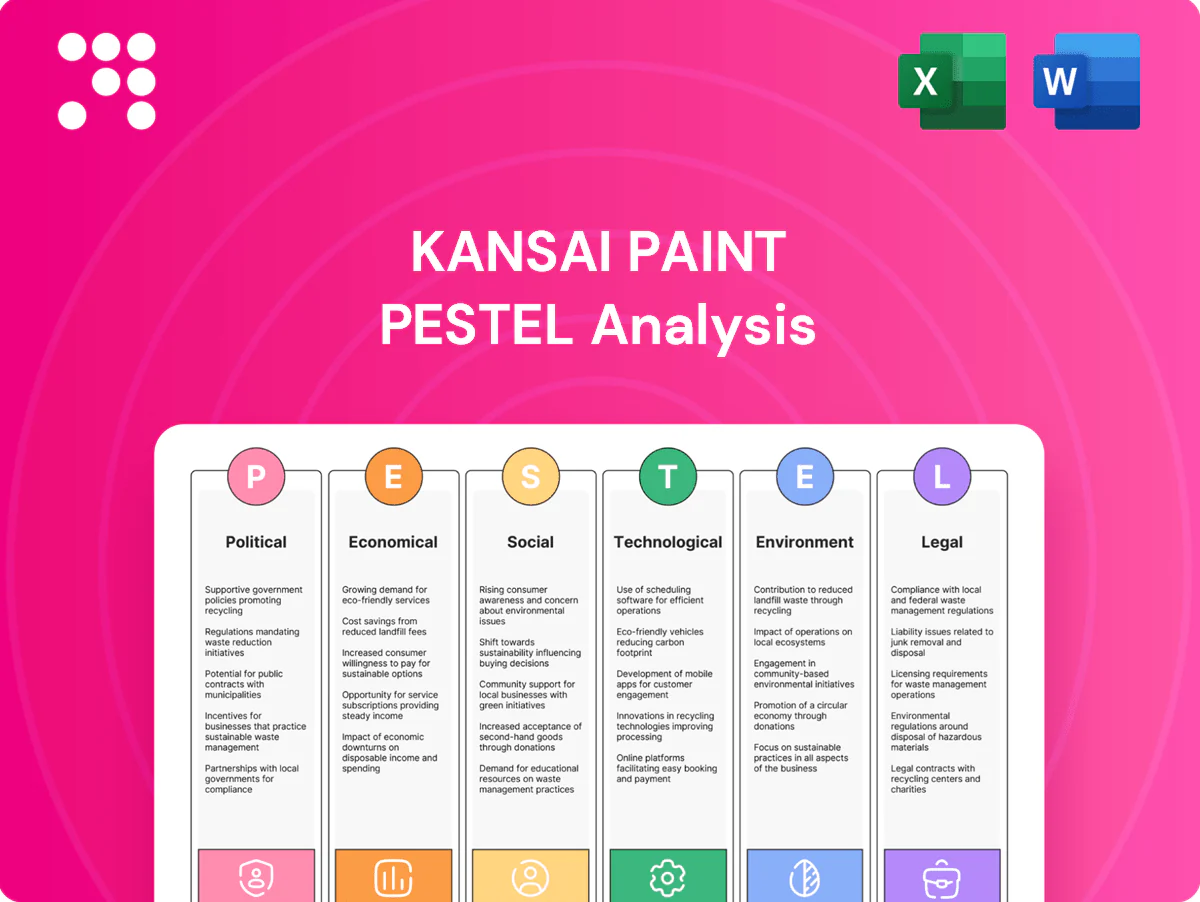

Visually segmented PESTLE summary for Kansai Paint that highlights regulatory, supply-chain and market risks for quick stakeholder alignment and ready insertion into presentations or strategy packs.

Economic factors

Automotive and construction cycles

Vehicle production (about 73m units globally in 2024) and US housing starts (~1.4m annualized in 2024) directly drive volumes in Kansai Paints OEM and decorative lines, so auto and construction slowdowns compress margins and raise price sensitivity. Diversification across industrial, automotive, decorative and 32+ geographies smooths revenue. Aftermarket and refurbishment, representing roughly 20–25% of coatings demand, dampen cyclicality in downturns.

Raw material inflation

Volatility in solvents, resins and pigments materially drives Kansai Paints cost of goods sold and working capital, with raw materials representing around 60% of paint COGS. Index-linked contracts and formula pricing enable quicker pass-through of input inflation. Vertical partnerships and use of recycled inputs improve input-cost stability. Inventory optimization reduces exposure to short-term spikes while avoiding costly overstocking.

Exchange-rate fluctuations

Yen volatility — USD/JPY moved from ~115 in 2021 to around 150 by 2024 — affects Kansai Paints consolidated results and export competitiveness as translation weakens yen-reported overseas revenue. Extensive local production across APAC, Europe and Americas provides natural hedges that cut transactional exposure. Active financial hedging programs and dollar-linked pricing clauses help protect margins. FX swings also reshape acquisition valuations and raise cross-border capex costs.

Emerging market growth

Rising urbanization in India (≈35.5% urban, UN 2022), ASEAN (~49% urban, World Bank 2022) and Africa (~43% urban, UN 2022) expands decorative-paint demand. Elevated infrastructure spending—ADB estimates Asia needs $26 trillion 2016–2030—lifts industrial and protective coatings. Affordability tiers and sachet sizing capture value segments; distribution depth and tinting networks are critical for scale.

- Urbanization: India 35.5% (UN 2022)

- ASEAN: ~49% (World Bank 2022)

- Africa: ~43% (UN 2022)

- Asia infra need: $26T (ADB 2017)

Capital availability and rates

Higher rates raise capex hurdle rates and inventory carrying costs; Japan 10‑yr yield near 0.8% in 2025 tightens WACC for Kansai Paint. Energy‑efficient plants and waste reduction projects need clear ROIs; global green bond issuance was about $500bn in 2024, easing access to green finance and lowering WACC for sustainability projects. M&A timing hinges on credit spreads and target valuations.

- Capex hurdle up — higher rates

- Inventory cost rise

- Clear ROI required for efficiency projects

- Green finance cuts WACC

- M&A sensitive to credit spreads

Tariffs, RCEP and Japan energy risks spur friend‑shoring, dual sourcing and coatings demand

Vehicle production (~73m units 2024) and US housing starts (~1.4m 2024) drive volumes; aftermarket (~20–25% demand) and 32+ country footprint smooth cyclicality. Raw materials (~60% of COGS) and solvent/resin volatility compress margins; index pricing and local production mitigate. USD/JPY ~150 (2024) and Japan 10y ~0.8% (2025) affect translation, capex and M&A timing.

| Metric | Value |

|---|---|

| Global vehicle prod | ~73m (2024) |

| US housing starts | ~1.4m (2024) |

| Raw materials share of COGS | ~60% |

| Aftermarket share | 20–25% |

| USD/JPY | ~150 (2024) |

| Japan 10y | ~0.8% (2025) |

| Green bond issuance | ~$500bn (2024) |

What You See Is What You Get

Kansai Paint PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Kansai Paint PESTLE Analysis delivers a concise, structured review of political, economic, social, technological, legal, and environmental factors affecting the company. The content, layout, and data are final and downloadable immediately after buying.

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE Analysis of Kansai Paint—three concise sections reveal how political, economic, social, and technological forces reshape its market position. Use these insights to anticipate risks and spot growth opportunities. Purchase the full report for a complete, actionable breakdown you can deploy immediately.

Political factors

Trade policies and tariffs

Shifts in tariffs on chemicals and pigments directly alter input costs and compress pricing flexibility, prompting Kansai Paint to adopt dual-supply and friend-shoring strategies; RCEP, in force since 2022 and covering about 30% of world GDP, can lower regional tariff barriers if leveraged. Regionalization increases the need to balance local production with global scale to absorb tariff shocks and preserve margins. Preferential agreements in Asia and Africa offer targeted growth corridors.

Geopolitical instability

Geopolitical instability disrupts feedstock availability and shipping lanes, raising costs and complicating insurance for paint-grade petrochemicals; Japan imports roughly 90% of its energy, making regional supply shocks material. Sanctions regimes constrain dealings with suppliers and customers in affected jurisdictions. Political risk in emerging markets forces Kansai Paint to consider plant location, inventory buffers and tariffs. Business continuity requires multi-site redundancy and elevated safety stocks.

Government industrial policies

Subsidies for EVs (global EV sales ~14 million in 2023, IEA 2024), plus infrastructure and Japan housing starts near 800,000 units in 2023 (MLIT), shift demand toward corrosion-resistant and automotive coatings. Localization mandates in China and other markets drive joint ventures and tech transfer, raising capex and licensing revenue opportunities. Public procurement increasingly specifies low-VOC/low-carbon paints, and active engagement with policy bodies aligns Kansai Paint R&D with national green priorities.

Currency and capital controls

Restrictions on forex in certain markets constrain repatriation and raw-material payments, forcing Kansai Paint to reroute cash and extend payables; global FX reserves stood near $12.9 trillion at end-2024 (IMF), underscoring active central-bank intervention. Hedging policies must price political FX risk; local-currency pricing limits volatility but raises operational complexity; treasury centralization balances liquidity and regional risk.

- FX controls → delayed repatriation/payments

- Hedging must cover political FX moves

- Local-currency pricing reduces translation risk

- Centralized treasury optimizes liquidity/risk

Regulatory harmonization efforts

APAC moves toward shared chemical standards and broader GHS adoption across 60+ economies by 2024 can streamline Kansai Paint approvals and reduce duplication. Divergences between EU REACH, US TSCA and Japan’s Chemical Substances Control Law still force tailored formulations and paperwork. Active participation in standards committees like national paint associations reduces compliance surprises and speeds multi‑jurisdiction launches.

- APAC GHS: 60+ economies (2024)

- Key divergences: REACH vs TSCA vs Japan CSCL

- Standards committee engagement: lowers regulatory delay risk

Tariffs, RCEP and Japan energy risks spur friend‑shoring, dual sourcing and coatings demand

Tariff shifts and RCEP (in force 2022, covers ~30% of world GDP) affect input costs, prompting friend‑shoring and dual sourcing to protect margins. Geopolitical shocks and Japan's ~90% energy import dependence raise feedstock, shipping and insurance risk. Policy trends (global EV sales ~14m in 2023; Japan housing starts ~800k in 2023) boost demand for automotive and low‑VOC coatings.

| Risk | Impact | Key data |

|---|---|---|

| Tariffs | Higher input costs | RCEP ~30% world GDP |

| Geopolitics | Supply/insurance shocks | Japan imports ~90% energy |

| Policy | Demand shift to low‑VOC/auto | EVs ~14m (2023); housing ~800k (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Kansai Paint, using current data and trends to highlight region- and industry-specific risks and opportunities; designed for executives and investors with forward-looking insights, scenario implications, and deck-ready findings that link external drivers to competitive strategy and regulatory compliance.

Visually segmented PESTLE summary for Kansai Paint that highlights regulatory, supply-chain and market risks for quick stakeholder alignment and ready insertion into presentations or strategy packs.

Economic factors

Automotive and construction cycles

Vehicle production (about 73m units globally in 2024) and US housing starts (~1.4m annualized in 2024) directly drive volumes in Kansai Paints OEM and decorative lines, so auto and construction slowdowns compress margins and raise price sensitivity. Diversification across industrial, automotive, decorative and 32+ geographies smooths revenue. Aftermarket and refurbishment, representing roughly 20–25% of coatings demand, dampen cyclicality in downturns.

Raw material inflation

Volatility in solvents, resins and pigments materially drives Kansai Paints cost of goods sold and working capital, with raw materials representing around 60% of paint COGS. Index-linked contracts and formula pricing enable quicker pass-through of input inflation. Vertical partnerships and use of recycled inputs improve input-cost stability. Inventory optimization reduces exposure to short-term spikes while avoiding costly overstocking.

Exchange-rate fluctuations

Yen volatility — USD/JPY moved from ~115 in 2021 to around 150 by 2024 — affects Kansai Paints consolidated results and export competitiveness as translation weakens yen-reported overseas revenue. Extensive local production across APAC, Europe and Americas provides natural hedges that cut transactional exposure. Active financial hedging programs and dollar-linked pricing clauses help protect margins. FX swings also reshape acquisition valuations and raise cross-border capex costs.

Emerging market growth

Rising urbanization in India (≈35.5% urban, UN 2022), ASEAN (~49% urban, World Bank 2022) and Africa (~43% urban, UN 2022) expands decorative-paint demand. Elevated infrastructure spending—ADB estimates Asia needs $26 trillion 2016–2030—lifts industrial and protective coatings. Affordability tiers and sachet sizing capture value segments; distribution depth and tinting networks are critical for scale.

- Urbanization: India 35.5% (UN 2022)

- ASEAN: ~49% (World Bank 2022)

- Africa: ~43% (UN 2022)

- Asia infra need: $26T (ADB 2017)

Capital availability and rates

Higher rates raise capex hurdle rates and inventory carrying costs; Japan 10‑yr yield near 0.8% in 2025 tightens WACC for Kansai Paint. Energy‑efficient plants and waste reduction projects need clear ROIs; global green bond issuance was about $500bn in 2024, easing access to green finance and lowering WACC for sustainability projects. M&A timing hinges on credit spreads and target valuations.

- Capex hurdle up — higher rates

- Inventory cost rise

- Clear ROI required for efficiency projects

- Green finance cuts WACC

- M&A sensitive to credit spreads

Tariffs, RCEP and Japan energy risks spur friend‑shoring, dual sourcing and coatings demand

Vehicle production (~73m units 2024) and US housing starts (~1.4m 2024) drive volumes; aftermarket (~20–25% demand) and 32+ country footprint smooth cyclicality. Raw materials (~60% of COGS) and solvent/resin volatility compress margins; index pricing and local production mitigate. USD/JPY ~150 (2024) and Japan 10y ~0.8% (2025) affect translation, capex and M&A timing.

| Metric | Value |

|---|---|

| Global vehicle prod | ~73m (2024) |

| US housing starts | ~1.4m (2024) |

| Raw materials share of COGS | ~60% |

| Aftermarket share | 20–25% |

| USD/JPY | ~150 (2024) |

| Japan 10y | ~0.8% (2025) |

| Green bond issuance | ~$500bn (2024) |

What You See Is What You Get

Kansai Paint PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Kansai Paint PESTLE Analysis delivers a concise, structured review of political, economic, social, technological, legal, and environmental factors affecting the company. The content, layout, and data are final and downloadable immediately after buying.

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE Analysis of Kansai Paint—three concise sections reveal how political, economic, social, and technological forces reshape its market position. Use these insights to anticipate risks and spot growth opportunities. Purchase the full report for a complete, actionable breakdown you can deploy immediately.

Political factors

Trade policies and tariffs

Shifts in tariffs on chemicals and pigments directly alter input costs and compress pricing flexibility, prompting Kansai Paint to adopt dual-supply and friend-shoring strategies; RCEP, in force since 2022 and covering about 30% of world GDP, can lower regional tariff barriers if leveraged. Regionalization increases the need to balance local production with global scale to absorb tariff shocks and preserve margins. Preferential agreements in Asia and Africa offer targeted growth corridors.

Geopolitical instability

Geopolitical instability disrupts feedstock availability and shipping lanes, raising costs and complicating insurance for paint-grade petrochemicals; Japan imports roughly 90% of its energy, making regional supply shocks material. Sanctions regimes constrain dealings with suppliers and customers in affected jurisdictions. Political risk in emerging markets forces Kansai Paint to consider plant location, inventory buffers and tariffs. Business continuity requires multi-site redundancy and elevated safety stocks.

Government industrial policies

Subsidies for EVs (global EV sales ~14 million in 2023, IEA 2024), plus infrastructure and Japan housing starts near 800,000 units in 2023 (MLIT), shift demand toward corrosion-resistant and automotive coatings. Localization mandates in China and other markets drive joint ventures and tech transfer, raising capex and licensing revenue opportunities. Public procurement increasingly specifies low-VOC/low-carbon paints, and active engagement with policy bodies aligns Kansai Paint R&D with national green priorities.

Currency and capital controls

Restrictions on forex in certain markets constrain repatriation and raw-material payments, forcing Kansai Paint to reroute cash and extend payables; global FX reserves stood near $12.9 trillion at end-2024 (IMF), underscoring active central-bank intervention. Hedging policies must price political FX risk; local-currency pricing limits volatility but raises operational complexity; treasury centralization balances liquidity and regional risk.

- FX controls → delayed repatriation/payments

- Hedging must cover political FX moves

- Local-currency pricing reduces translation risk

- Centralized treasury optimizes liquidity/risk

Regulatory harmonization efforts

APAC moves toward shared chemical standards and broader GHS adoption across 60+ economies by 2024 can streamline Kansai Paint approvals and reduce duplication. Divergences between EU REACH, US TSCA and Japan’s Chemical Substances Control Law still force tailored formulations and paperwork. Active participation in standards committees like national paint associations reduces compliance surprises and speeds multi‑jurisdiction launches.

- APAC GHS: 60+ economies (2024)

- Key divergences: REACH vs TSCA vs Japan CSCL

- Standards committee engagement: lowers regulatory delay risk

Tariffs, RCEP and Japan energy risks spur friend‑shoring, dual sourcing and coatings demand

Tariff shifts and RCEP (in force 2022, covers ~30% of world GDP) affect input costs, prompting friend‑shoring and dual sourcing to protect margins. Geopolitical shocks and Japan's ~90% energy import dependence raise feedstock, shipping and insurance risk. Policy trends (global EV sales ~14m in 2023; Japan housing starts ~800k in 2023) boost demand for automotive and low‑VOC coatings.

| Risk | Impact | Key data |

|---|---|---|

| Tariffs | Higher input costs | RCEP ~30% world GDP |

| Geopolitics | Supply/insurance shocks | Japan imports ~90% energy |

| Policy | Demand shift to low‑VOC/auto | EVs ~14m (2023); housing ~800k (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Kansai Paint, using current data and trends to highlight region- and industry-specific risks and opportunities; designed for executives and investors with forward-looking insights, scenario implications, and deck-ready findings that link external drivers to competitive strategy and regulatory compliance.

Visually segmented PESTLE summary for Kansai Paint that highlights regulatory, supply-chain and market risks for quick stakeholder alignment and ready insertion into presentations or strategy packs.

Economic factors

Automotive and construction cycles

Vehicle production (about 73m units globally in 2024) and US housing starts (~1.4m annualized in 2024) directly drive volumes in Kansai Paints OEM and decorative lines, so auto and construction slowdowns compress margins and raise price sensitivity. Diversification across industrial, automotive, decorative and 32+ geographies smooths revenue. Aftermarket and refurbishment, representing roughly 20–25% of coatings demand, dampen cyclicality in downturns.

Raw material inflation

Volatility in solvents, resins and pigments materially drives Kansai Paints cost of goods sold and working capital, with raw materials representing around 60% of paint COGS. Index-linked contracts and formula pricing enable quicker pass-through of input inflation. Vertical partnerships and use of recycled inputs improve input-cost stability. Inventory optimization reduces exposure to short-term spikes while avoiding costly overstocking.

Exchange-rate fluctuations

Yen volatility — USD/JPY moved from ~115 in 2021 to around 150 by 2024 — affects Kansai Paints consolidated results and export competitiveness as translation weakens yen-reported overseas revenue. Extensive local production across APAC, Europe and Americas provides natural hedges that cut transactional exposure. Active financial hedging programs and dollar-linked pricing clauses help protect margins. FX swings also reshape acquisition valuations and raise cross-border capex costs.

Emerging market growth

Rising urbanization in India (≈35.5% urban, UN 2022), ASEAN (~49% urban, World Bank 2022) and Africa (~43% urban, UN 2022) expands decorative-paint demand. Elevated infrastructure spending—ADB estimates Asia needs $26 trillion 2016–2030—lifts industrial and protective coatings. Affordability tiers and sachet sizing capture value segments; distribution depth and tinting networks are critical for scale.

- Urbanization: India 35.5% (UN 2022)

- ASEAN: ~49% (World Bank 2022)

- Africa: ~43% (UN 2022)

- Asia infra need: $26T (ADB 2017)

Capital availability and rates

Higher rates raise capex hurdle rates and inventory carrying costs; Japan 10‑yr yield near 0.8% in 2025 tightens WACC for Kansai Paint. Energy‑efficient plants and waste reduction projects need clear ROIs; global green bond issuance was about $500bn in 2024, easing access to green finance and lowering WACC for sustainability projects. M&A timing hinges on credit spreads and target valuations.

- Capex hurdle up — higher rates

- Inventory cost rise

- Clear ROI required for efficiency projects

- Green finance cuts WACC

- M&A sensitive to credit spreads

Tariffs, RCEP and Japan energy risks spur friend‑shoring, dual sourcing and coatings demand

Vehicle production (~73m units 2024) and US housing starts (~1.4m 2024) drive volumes; aftermarket (~20–25% demand) and 32+ country footprint smooth cyclicality. Raw materials (~60% of COGS) and solvent/resin volatility compress margins; index pricing and local production mitigate. USD/JPY ~150 (2024) and Japan 10y ~0.8% (2025) affect translation, capex and M&A timing.

| Metric | Value |

|---|---|

| Global vehicle prod | ~73m (2024) |

| US housing starts | ~1.4m (2024) |

| Raw materials share of COGS | ~60% |

| Aftermarket share | 20–25% |

| USD/JPY | ~150 (2024) |

| Japan 10y | ~0.8% (2025) |

| Green bond issuance | ~$500bn (2024) |

What You See Is What You Get

Kansai Paint PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Kansai Paint PESTLE Analysis delivers a concise, structured review of political, economic, social, technological, legal, and environmental factors affecting the company. The content, layout, and data are final and downloadable immediately after buying.