KAP Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

KAP faces nuanced competitive pressures—supplier leverage, buyer bargaining, substitute threats, and entry barriers each shape its margins and strategic options. This snapshot outlines key dynamics, but the full Porter's Five Forces Analysis quantifies force intensity, risks, and strategic implications. Unlock the complete report for visuals, force ratings, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Concentrated critical inputs

Petrochemical feedstocks, timber, and specialty chemicals often derive from a small group of suppliers—in 2024 the top 5 ethylene producers held about 35% of global capacity, top 10 specialty-chemical firms ~45% market share, and Russia+Canada accounted for roughly 45% of softwood lumber exports—concentrated supply elevates pricing power and enables take-or-pay clauses. KAP can mitigate via multi-sourcing and staggered long-term contracts; backward integration or hedging further reduces exposure.

Energy and logistics constraints

Energy and logistics constraints: 2024 load-shedding and port backlogs raised input and transport risk, with Durban vessel delays reported up to 14 days, prompting suppliers to levy surcharges or prioritise larger buyers. KAP’s scale strengthens negotiating leverage but cannot remove systemic exposure. On-site generation and private logistics investments have materially reduced interruption costs for large agribusinesses.

Specialized equipment/OEM dependency

Logistics fleets and industrial plants depend on a concentrated set of OEMs and spare‑part ecosystems, with proprietary standards and lead times often in the 8–16 week range that increase supplier lock‑in. KAP’s volume discounts and framework agreements typically trim parts spend by roughly 10–15%, while predictive maintenance can cut unplanned downtime by up to 50% and maintenance costs by 20–30%, and vendor‑managed inventory further reduces stockouts and emergency procurements.

Labor and skills scarcity

- Skilled scarcity: uneven regional availability

- Cost pressure: wage negotiations and unions

- Mitigation: KAP training + retention

- Tech offset: automation reduces skill reliance

Commodity price pass-through

Oil, polymers and resins trade on global hubs with high volatility; Brent averaged about $86/bbl in 2024, driving feedstock swings that suppliers seek to pass through via index‑linked contracts. KAP can mirror inputs in customer pricing formulas while tactical inventory and 3–12 month hedging reduce margin variability.

- Index‑linked supply contracts

- Align customer pricing formulas

- Inventory buffer + 3–12m hedges

Pricing power vs supply‑chain strain: Brent $86, delays to 14 days

Concentrated feedstock and OEM markets (top‑5 ethylene ~35%, top‑10 specialty chem ~45%, Russia+Canada ~45% softwood exports) give suppliers pricing power; Brent averaged ~$86/bbl in 2024. Logistics and labor shortages (Durban delays up to 14 days; driver median wage $48,310) raise pass‑through risk. KAP offsets via multi‑sourcing, hedges, LT contracts, vertical options and capex in logistics.

| Metric | 2024 Value |

|---|---|

| Top‑5 ethylene share | ~35% |

| Top‑10 specialty chem | ~45% |

| Softwood exports (RU+CA) | ~45% |

| Brent avg | $86/bbl |

| Durban max delay | 14 days |

| Driver median wage (US) | $48,310 |

What is included in the product

Tailored Porter's Five Forces analysis for KAP uncovers competitive drivers, supplier/buyer power, threats from substitutes and new entrants, and identifies disruptive forces and strategic levers to protect market share and pricing—delivered in fully editable format for reports, decks, or academic use.

A concise KAP Porter's Five Forces one-sheet that visualizes competitive pressure with an instant radar chart, lets you swap in data and scenarios without macros, and exports cleanly into decks—streamlining analysis and speeding strategic decisions.

Customers Bargaining Power

Large B2B anchor customers

KAP serves sizable FMCG, mining, retail and manufacturing accounts that exert strong price and SLA leverage; large B2B buyers commonly secure volume rebates (typically 3–7%) and service-level penalties tied to KPI breaches. Contract renewals in 2024 have been highly competitive and data-driven, with benchmarking and TCO analysis central to negotiations. Cross-selling across divisions reduces single-contract concentration and weakens buyer-specific bargaining power.

Price transparency and benchmarking

Commodity-linked inputs and freight rates are widely benchmarked, with buyers often tracking landed-cost variances of 5–15% across suppliers. Purchasers compare landed cost, uptime, and on-time delivery metrics, commonly targeting >95% uptime and OTIF benchmarks. KAP must justify any premium through demonstrated reliability and integrated solutions, using analytics and KPI dashboards to enable value-based selling and measurable ROI.

Switching costs vary by division

Complex logistics networks and customized chemicals raise switching frictions for KAP, with specialty offerings—which represent roughly one-third of the global chemical market—harder to substitute than commodity lines. Standardized products face easier substitution and price pressure. KAP increases stickiness via embedded systems, regional warehousing, technical support and multi-year SLAs (commonly 3–5 years) that lock in mutual commitments.

Demand cyclicality

Industrial and consumer cycles shift buyer volumes and bargaining stance; US manufacturing capacity utilization averaged 77.4% in 2024 (Federal Reserve), tightening supplier leverage. In downturns buyers push for price relief and flexible terms, and KAP retains share via capacity planning and variable-cost levers. Tiered pricing with volume bands balances utilization and margin.

- Demand swing: cyclical volume shocks

- 2024: 77.4% US capacity utilization

- KAP levers: capacity planning, variable costs

- Pricing: tiered bands to protect margin

Compliance and ESG requirements

Corporate buyers now demand audited safety, quality and sustainability; non-compliance can lead to disqualification and regulatory penalties, as seen with the EU CSRD expanding mandatory reporting to about 50,000 companies from 2024. KAP uses certifications and end-to-end traceability to defend pricing and reduce churn. Strong ESG leadership can shift perceived ESG costs into differentiation and price premium opportunities.

- CSRD ~50,000 companies (2024)

- Certifications + traceability = price defense

- ESG can become differentiation, not just cost

Buyers push 3–7% rebates and >95% uptime in 2024

KAP faces strong B2B buyer leverage: volume rebates 3–7%, SLA penalties common, buyers demand >95% uptime and benchmark landed-cost variances 5–15%. 2024 negotiations are data-driven; US capacity utilization 77.4% tightens supply. ESG/CSRD (~50,000 firms from 2024) raises compliance thresholds that KAP monetizes via traceability and certifications.

| Metric | Value |

|---|---|

| Volume rebates | 3–7% |

| Uptime target | >95% |

| Landed-cost variance | 5–15% |

| US cap. util. (2024) | 77.4% |

| CSRD scope (2024) | ~50,000 firms |

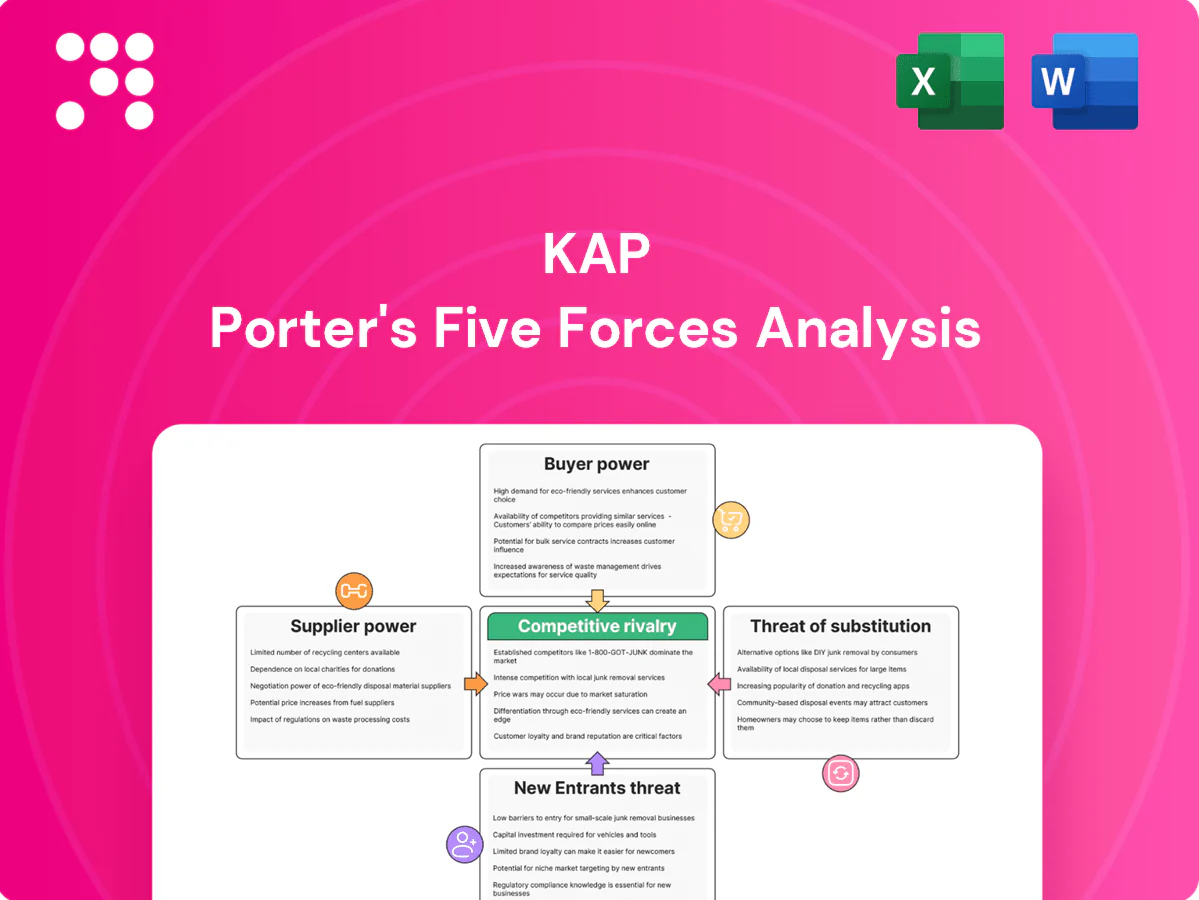

What You See Is What You Get

KAP Porter's Five Forces Analysis

This preview shows the exact KAP Porter's Five Forces Analysis document you'll receive immediately after purchase—no placeholders. The file is fully formatted and ready for download the moment you buy. No mockups or samples; this is the final deliverable prepared for immediate use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

KAP faces nuanced competitive pressures—supplier leverage, buyer bargaining, substitute threats, and entry barriers each shape its margins and strategic options. This snapshot outlines key dynamics, but the full Porter's Five Forces Analysis quantifies force intensity, risks, and strategic implications. Unlock the complete report for visuals, force ratings, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Concentrated critical inputs

Petrochemical feedstocks, timber, and specialty chemicals often derive from a small group of suppliers—in 2024 the top 5 ethylene producers held about 35% of global capacity, top 10 specialty-chemical firms ~45% market share, and Russia+Canada accounted for roughly 45% of softwood lumber exports—concentrated supply elevates pricing power and enables take-or-pay clauses. KAP can mitigate via multi-sourcing and staggered long-term contracts; backward integration or hedging further reduces exposure.

Energy and logistics constraints

Energy and logistics constraints: 2024 load-shedding and port backlogs raised input and transport risk, with Durban vessel delays reported up to 14 days, prompting suppliers to levy surcharges or prioritise larger buyers. KAP’s scale strengthens negotiating leverage but cannot remove systemic exposure. On-site generation and private logistics investments have materially reduced interruption costs for large agribusinesses.

Specialized equipment/OEM dependency

Logistics fleets and industrial plants depend on a concentrated set of OEMs and spare‑part ecosystems, with proprietary standards and lead times often in the 8–16 week range that increase supplier lock‑in. KAP’s volume discounts and framework agreements typically trim parts spend by roughly 10–15%, while predictive maintenance can cut unplanned downtime by up to 50% and maintenance costs by 20–30%, and vendor‑managed inventory further reduces stockouts and emergency procurements.

Labor and skills scarcity

- Skilled scarcity: uneven regional availability

- Cost pressure: wage negotiations and unions

- Mitigation: KAP training + retention

- Tech offset: automation reduces skill reliance

Commodity price pass-through

Oil, polymers and resins trade on global hubs with high volatility; Brent averaged about $86/bbl in 2024, driving feedstock swings that suppliers seek to pass through via index‑linked contracts. KAP can mirror inputs in customer pricing formulas while tactical inventory and 3–12 month hedging reduce margin variability.

- Index‑linked supply contracts

- Align customer pricing formulas

- Inventory buffer + 3–12m hedges

Pricing power vs supply‑chain strain: Brent $86, delays to 14 days

Concentrated feedstock and OEM markets (top‑5 ethylene ~35%, top‑10 specialty chem ~45%, Russia+Canada ~45% softwood exports) give suppliers pricing power; Brent averaged ~$86/bbl in 2024. Logistics and labor shortages (Durban delays up to 14 days; driver median wage $48,310) raise pass‑through risk. KAP offsets via multi‑sourcing, hedges, LT contracts, vertical options and capex in logistics.

| Metric | 2024 Value |

|---|---|

| Top‑5 ethylene share | ~35% |

| Top‑10 specialty chem | ~45% |

| Softwood exports (RU+CA) | ~45% |

| Brent avg | $86/bbl |

| Durban max delay | 14 days |

| Driver median wage (US) | $48,310 |

What is included in the product

Tailored Porter's Five Forces analysis for KAP uncovers competitive drivers, supplier/buyer power, threats from substitutes and new entrants, and identifies disruptive forces and strategic levers to protect market share and pricing—delivered in fully editable format for reports, decks, or academic use.

A concise KAP Porter's Five Forces one-sheet that visualizes competitive pressure with an instant radar chart, lets you swap in data and scenarios without macros, and exports cleanly into decks—streamlining analysis and speeding strategic decisions.

Customers Bargaining Power

Large B2B anchor customers

KAP serves sizable FMCG, mining, retail and manufacturing accounts that exert strong price and SLA leverage; large B2B buyers commonly secure volume rebates (typically 3–7%) and service-level penalties tied to KPI breaches. Contract renewals in 2024 have been highly competitive and data-driven, with benchmarking and TCO analysis central to negotiations. Cross-selling across divisions reduces single-contract concentration and weakens buyer-specific bargaining power.

Price transparency and benchmarking

Commodity-linked inputs and freight rates are widely benchmarked, with buyers often tracking landed-cost variances of 5–15% across suppliers. Purchasers compare landed cost, uptime, and on-time delivery metrics, commonly targeting >95% uptime and OTIF benchmarks. KAP must justify any premium through demonstrated reliability and integrated solutions, using analytics and KPI dashboards to enable value-based selling and measurable ROI.

Switching costs vary by division

Complex logistics networks and customized chemicals raise switching frictions for KAP, with specialty offerings—which represent roughly one-third of the global chemical market—harder to substitute than commodity lines. Standardized products face easier substitution and price pressure. KAP increases stickiness via embedded systems, regional warehousing, technical support and multi-year SLAs (commonly 3–5 years) that lock in mutual commitments.

Demand cyclicality

Industrial and consumer cycles shift buyer volumes and bargaining stance; US manufacturing capacity utilization averaged 77.4% in 2024 (Federal Reserve), tightening supplier leverage. In downturns buyers push for price relief and flexible terms, and KAP retains share via capacity planning and variable-cost levers. Tiered pricing with volume bands balances utilization and margin.

- Demand swing: cyclical volume shocks

- 2024: 77.4% US capacity utilization

- KAP levers: capacity planning, variable costs

- Pricing: tiered bands to protect margin

Compliance and ESG requirements

Corporate buyers now demand audited safety, quality and sustainability; non-compliance can lead to disqualification and regulatory penalties, as seen with the EU CSRD expanding mandatory reporting to about 50,000 companies from 2024. KAP uses certifications and end-to-end traceability to defend pricing and reduce churn. Strong ESG leadership can shift perceived ESG costs into differentiation and price premium opportunities.

- CSRD ~50,000 companies (2024)

- Certifications + traceability = price defense

- ESG can become differentiation, not just cost

Buyers push 3–7% rebates and >95% uptime in 2024

KAP faces strong B2B buyer leverage: volume rebates 3–7%, SLA penalties common, buyers demand >95% uptime and benchmark landed-cost variances 5–15%. 2024 negotiations are data-driven; US capacity utilization 77.4% tightens supply. ESG/CSRD (~50,000 firms from 2024) raises compliance thresholds that KAP monetizes via traceability and certifications.

| Metric | Value |

|---|---|

| Volume rebates | 3–7% |

| Uptime target | >95% |

| Landed-cost variance | 5–15% |

| US cap. util. (2024) | 77.4% |

| CSRD scope (2024) | ~50,000 firms |

What You See Is What You Get

KAP Porter's Five Forces Analysis

This preview shows the exact KAP Porter's Five Forces Analysis document you'll receive immediately after purchase—no placeholders. The file is fully formatted and ready for download the moment you buy. No mockups or samples; this is the final deliverable prepared for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

KAP faces nuanced competitive pressures—supplier leverage, buyer bargaining, substitute threats, and entry barriers each shape its margins and strategic options. This snapshot outlines key dynamics, but the full Porter's Five Forces Analysis quantifies force intensity, risks, and strategic implications. Unlock the complete report for visuals, force ratings, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Concentrated critical inputs

Petrochemical feedstocks, timber, and specialty chemicals often derive from a small group of suppliers—in 2024 the top 5 ethylene producers held about 35% of global capacity, top 10 specialty-chemical firms ~45% market share, and Russia+Canada accounted for roughly 45% of softwood lumber exports—concentrated supply elevates pricing power and enables take-or-pay clauses. KAP can mitigate via multi-sourcing and staggered long-term contracts; backward integration or hedging further reduces exposure.

Energy and logistics constraints

Energy and logistics constraints: 2024 load-shedding and port backlogs raised input and transport risk, with Durban vessel delays reported up to 14 days, prompting suppliers to levy surcharges or prioritise larger buyers. KAP’s scale strengthens negotiating leverage but cannot remove systemic exposure. On-site generation and private logistics investments have materially reduced interruption costs for large agribusinesses.

Specialized equipment/OEM dependency

Logistics fleets and industrial plants depend on a concentrated set of OEMs and spare‑part ecosystems, with proprietary standards and lead times often in the 8–16 week range that increase supplier lock‑in. KAP’s volume discounts and framework agreements typically trim parts spend by roughly 10–15%, while predictive maintenance can cut unplanned downtime by up to 50% and maintenance costs by 20–30%, and vendor‑managed inventory further reduces stockouts and emergency procurements.

Labor and skills scarcity

- Skilled scarcity: uneven regional availability

- Cost pressure: wage negotiations and unions

- Mitigation: KAP training + retention

- Tech offset: automation reduces skill reliance

Commodity price pass-through

Oil, polymers and resins trade on global hubs with high volatility; Brent averaged about $86/bbl in 2024, driving feedstock swings that suppliers seek to pass through via index‑linked contracts. KAP can mirror inputs in customer pricing formulas while tactical inventory and 3–12 month hedging reduce margin variability.

- Index‑linked supply contracts

- Align customer pricing formulas

- Inventory buffer + 3–12m hedges

Pricing power vs supply‑chain strain: Brent $86, delays to 14 days

Concentrated feedstock and OEM markets (top‑5 ethylene ~35%, top‑10 specialty chem ~45%, Russia+Canada ~45% softwood exports) give suppliers pricing power; Brent averaged ~$86/bbl in 2024. Logistics and labor shortages (Durban delays up to 14 days; driver median wage $48,310) raise pass‑through risk. KAP offsets via multi‑sourcing, hedges, LT contracts, vertical options and capex in logistics.

| Metric | 2024 Value |

|---|---|

| Top‑5 ethylene share | ~35% |

| Top‑10 specialty chem | ~45% |

| Softwood exports (RU+CA) | ~45% |

| Brent avg | $86/bbl |

| Durban max delay | 14 days |

| Driver median wage (US) | $48,310 |

What is included in the product

Tailored Porter's Five Forces analysis for KAP uncovers competitive drivers, supplier/buyer power, threats from substitutes and new entrants, and identifies disruptive forces and strategic levers to protect market share and pricing—delivered in fully editable format for reports, decks, or academic use.

A concise KAP Porter's Five Forces one-sheet that visualizes competitive pressure with an instant radar chart, lets you swap in data and scenarios without macros, and exports cleanly into decks—streamlining analysis and speeding strategic decisions.

Customers Bargaining Power

Large B2B anchor customers

KAP serves sizable FMCG, mining, retail and manufacturing accounts that exert strong price and SLA leverage; large B2B buyers commonly secure volume rebates (typically 3–7%) and service-level penalties tied to KPI breaches. Contract renewals in 2024 have been highly competitive and data-driven, with benchmarking and TCO analysis central to negotiations. Cross-selling across divisions reduces single-contract concentration and weakens buyer-specific bargaining power.

Price transparency and benchmarking

Commodity-linked inputs and freight rates are widely benchmarked, with buyers often tracking landed-cost variances of 5–15% across suppliers. Purchasers compare landed cost, uptime, and on-time delivery metrics, commonly targeting >95% uptime and OTIF benchmarks. KAP must justify any premium through demonstrated reliability and integrated solutions, using analytics and KPI dashboards to enable value-based selling and measurable ROI.

Switching costs vary by division

Complex logistics networks and customized chemicals raise switching frictions for KAP, with specialty offerings—which represent roughly one-third of the global chemical market—harder to substitute than commodity lines. Standardized products face easier substitution and price pressure. KAP increases stickiness via embedded systems, regional warehousing, technical support and multi-year SLAs (commonly 3–5 years) that lock in mutual commitments.

Demand cyclicality

Industrial and consumer cycles shift buyer volumes and bargaining stance; US manufacturing capacity utilization averaged 77.4% in 2024 (Federal Reserve), tightening supplier leverage. In downturns buyers push for price relief and flexible terms, and KAP retains share via capacity planning and variable-cost levers. Tiered pricing with volume bands balances utilization and margin.

- Demand swing: cyclical volume shocks

- 2024: 77.4% US capacity utilization

- KAP levers: capacity planning, variable costs

- Pricing: tiered bands to protect margin

Compliance and ESG requirements

Corporate buyers now demand audited safety, quality and sustainability; non-compliance can lead to disqualification and regulatory penalties, as seen with the EU CSRD expanding mandatory reporting to about 50,000 companies from 2024. KAP uses certifications and end-to-end traceability to defend pricing and reduce churn. Strong ESG leadership can shift perceived ESG costs into differentiation and price premium opportunities.

- CSRD ~50,000 companies (2024)

- Certifications + traceability = price defense

- ESG can become differentiation, not just cost

Buyers push 3–7% rebates and >95% uptime in 2024

KAP faces strong B2B buyer leverage: volume rebates 3–7%, SLA penalties common, buyers demand >95% uptime and benchmark landed-cost variances 5–15%. 2024 negotiations are data-driven; US capacity utilization 77.4% tightens supply. ESG/CSRD (~50,000 firms from 2024) raises compliance thresholds that KAP monetizes via traceability and certifications.

| Metric | Value |

|---|---|

| Volume rebates | 3–7% |

| Uptime target | >95% |

| Landed-cost variance | 5–15% |

| US cap. util. (2024) | 77.4% |

| CSRD scope (2024) | ~50,000 firms |

What You See Is What You Get

KAP Porter's Five Forces Analysis

This preview shows the exact KAP Porter's Five Forces Analysis document you'll receive immediately after purchase—no placeholders. The file is fully formatted and ready for download the moment you buy. No mockups or samples; this is the final deliverable prepared for immediate use.