KAP PESTLE Analysis

Your Competitive Advantage Starts with This Report

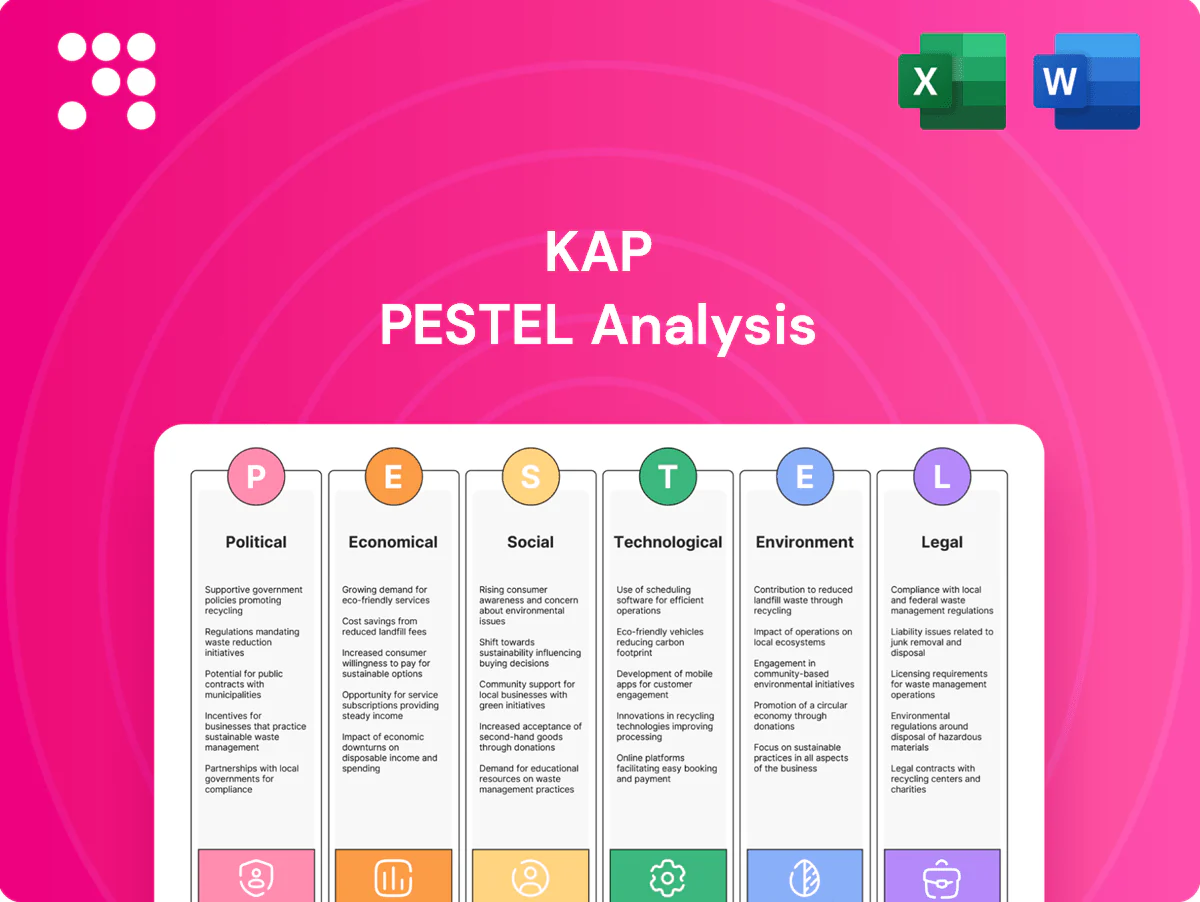

Unlock how political, economic, social, technological, legal, and environmental forces are shaping KAP’s trajectory with our concise PESTLE snapshot—ideal for investors and strategists who need actionable context fast. Buy the full analysis to access detailed risks, opportunities, and ready-to-use insights for smarter decisions.

Political factors

Policy stability in SA

Policy stability after the May 2024 national election and subsequent cabinet reshuffle directly affects logistics, chemicals and manufacturing permits, with manufacturing representing about 13% of South Africa’s GDP. Shifts in industrial and energy policy drive input-cost volatility and can delay capital deployment; persistent Eskom constraints remain a material risk. KAP must monitor cabinet priorities and policy continuity and use scenario planning to hedge abrupt changes.

State logistics governance

Transnet performance and the 2024 Transnet turnaround plan directly affect freight reliability and costs, while port reforms shape berth availability and tariffs. Expanded public‑private collaborations and concessioning since 2024 can open capacity but require tight KPIs. Governance lapses risk service drops; KAP must embed route diversification and contract clauses reflecting these operational risks.

B-BBEE and localization

B-BBEE rules shape ownership, procurement and supplier development and KAP must improve equity ownership and supplier-development metrics to compete for large contracts. Firms with level 1–2 B-BBEE scores secure preferential access to state and corporate deals; South African public procurement was about R1.5 trillion in 2023/24, with B-BBEE points decisive on many awards. Localization incentives (tax allowances, local-content credits) can unlock capex support but increase compliance workload; aligning supply chains to capture preferential opportunities is essential for KAP.

Trade and tariff exposure

Import tariffs on chemicals and equipment materially squeeze margins; AfCFTA covers 54 countries and targets tariff liberalization of about 90% of goods, while SADC comprises 16 member states requiring customs agility for market access; anti-dumping measures in the region can abruptly shift pricing dynamics; KAP must maintain flexible sourcing and rigorous trade compliance.

- Tariff exposure

- AfCFTA ~90% liberalisation

- SADC 16 members — customs agility

- Anti-dumping risk

- Flexible sourcing & compliance

Energy policy trajectory

Regulatory support for private generation and renewables lowers load-shedding exposure and improves supply security, while licensing and wheeling frameworks directly affect project timelines and bankability. Fuel levies and carbon pricing — EU ETS around €90/ton in 2024 — shift operating costs toward low-carbon generation. KAP benefits from early participation in IPP rounds and embedded generation to lock lower long-term marginal costs and hedge grid risk.

- Regulatory support: improves supply security

- Licensing/wheeling: affects project viability and financing

- Carbon price: ~€90/ton (EU ETS 2024) increases fossil operating costs

- KAP advantage: early IPP/embedded generation reduces long-term marginal cost

Policy, ports and carbon pricing reshape manufacturing, procurement and AfCFTA trade

Policy stability post‑May 2024 election and cabinet changes affects permits and energy policy; manufacturing ~13% of GDP. Transnet turnaround and port reforms determine freight costs; public procurement ≈R1.5tn (2023/24). B‑BBEE levels drive contract access; AfCFTA 54 countries ~90% liberalisation impacts tariffs. Renewables policy and carbon pricing (EU ETS ~€90/t in 2024) shift operating costs.

| Metric | Value |

|---|---|

| Manufacturing % GDP | ~13% |

| Public procurement 2023/24 | R1.5tn |

| AfCFTA coverage | 54 countries; ~90% liberalisation |

| EU ETS 2024 | ~€90/ton |

What is included in the product

Explores how external macro-environmental factors uniquely affect the KAP across six dimensions: Political, Economic, Social, Technological, Environmental, and Legal. Backed by current data and forward-looking insights, it helps executives, consultants, and entrepreneurs identify risks, opportunities, and strategic actions tailored to the KAP's region and industry.

KAP PESTLE delivers a clean, visually segmented summary of external risks and opportunities for quick reference in meetings or presentations. It’s editable, shareable, and written in simple language to align teams fast.

Economic factors

GDP and freight cycles

Logistics volumes closely follow GDP and industrial output; IMF estimated global GDP growth at about 3.1% in 2024 and 3.0% in 2025, signalling modest demand for freight after pandemic-era swings. Slower growth compresses yields and utilization, pushing spot rates down and idle capacity up. Upswings require rapid capacity scaling—container spot rates jumped intermittently by over 40% in past cycles—so KAP should balance fixed and variable fleet capacity to smooth volatility.

Rand volatility

Rand volatility directly raises costs for KAP by increasing prices of imported chemical feedstock, capex and USD-denominated debt servicing; USD/ZAR traded around 18.5 in mid‑2025, up from ~17.0 a year earlier, amplifying input cost pressure. A weaker rand has lifted equipment and feedstock costs by double digits for some suppliers. Active FX hedging, aligning rand revenues with import exposure and contractual pricing clauses help protect margins.

Inflation and rates

High inflation—headline CPI running 3–8% across major markets in 2024—lifts wages, fuel and maintenance costs, squeezing margins for KAP. Interest rates (Fed funds 5.25–5.50% in 2024; ECB and BoE similarly elevated) increase financing costs for fleet and plants. Pass-through to customers often lags, so KAP needs rigorous cost control and dynamic pricing to protect cash flow.

Commodity and energy costs

Oil and petrochemical prices drive logistics fuel and chemical inputs; Brent averaged about 85 USD/bbl in 2024 and traded 80–95 USD/bbl in early 2025, raising transport and feedstock costs ~12–18% YoY. Industrial electricity tariffs rose ~6–10% in many markets in 2024 and outages added up to ~4% of OPEX. Efficiency programs and energy diversification can cut energy spend 10–25%, and procurement should lock 12–24 month hedges or long-term supply deals.

- Price exposure: Brent ~85 USD/bbl (2024 average)

- Tariff/outage impact: +6–10% tariffs, outages ≈4% OPEX

- Mitigation: efficiency 10–25% savings; 12–24 month hedges

Labor market dynamics

Skilled labor shortages are constraining output and pushing wage growth higher; US job openings remained elevated at about 8.1 million in Dec 2024 (BLS JOLTS), sustaining upward wage pressure and productivity drag. Unionized sectors complicate staffing strategies with collective bargaining and higher turnover risk, while targeted training pipelines and retention programs are increasingly essential. Automation investments can progressively offset shortages and restore margins over a multi-year horizon.

- Skilled shortages: 8.1M US job openings (Dec 2024, BLS)

- Wage pressure: sustained above-prepandemic growth in 2024

- Union complexity: higher negotiation-driven cost volatility

- Mitigation: training, retention, automation

Policy, ports and carbon pricing reshape manufacturing, procurement and AfCFTA trade

Global GDP growth slowed to IMF estimates of 3.1% (2024) and 3.0% (2025), moderating freight demand and rate volatility.

Rand at ~18.5 ZAR/USD mid-2025 raises import, capex and debt costs; Brent ~85 USD/bbl (2024 avg) keeps fuel/feedstock high.

High inflation (CPI 3–8% in 2024) and elevated rates (Fed 5.25–5.50% 2024) squeeze margins; hedge, pricing and efficiency are essential.

| Metric | Value |

|---|---|

| GDP growth | 3.1% (2024), 3.0% (2025) |

| USD/ZAR | ~18.5 (mid‑2025) |

| Brent | ~85 USD/bbl (2024 avg) |

Same Document Delivered

KAP PESTLE Analysis

The preview shown here is the exact KAP PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or teasers. After payment you’ll instantly own this finished, professionally structured report.

Your Competitive Advantage Starts with This Report

Unlock how political, economic, social, technological, legal, and environmental forces are shaping KAP’s trajectory with our concise PESTLE snapshot—ideal for investors and strategists who need actionable context fast. Buy the full analysis to access detailed risks, opportunities, and ready-to-use insights for smarter decisions.

Political factors

Policy stability in SA

Policy stability after the May 2024 national election and subsequent cabinet reshuffle directly affects logistics, chemicals and manufacturing permits, with manufacturing representing about 13% of South Africa’s GDP. Shifts in industrial and energy policy drive input-cost volatility and can delay capital deployment; persistent Eskom constraints remain a material risk. KAP must monitor cabinet priorities and policy continuity and use scenario planning to hedge abrupt changes.

State logistics governance

Transnet performance and the 2024 Transnet turnaround plan directly affect freight reliability and costs, while port reforms shape berth availability and tariffs. Expanded public‑private collaborations and concessioning since 2024 can open capacity but require tight KPIs. Governance lapses risk service drops; KAP must embed route diversification and contract clauses reflecting these operational risks.

B-BBEE and localization

B-BBEE rules shape ownership, procurement and supplier development and KAP must improve equity ownership and supplier-development metrics to compete for large contracts. Firms with level 1–2 B-BBEE scores secure preferential access to state and corporate deals; South African public procurement was about R1.5 trillion in 2023/24, with B-BBEE points decisive on many awards. Localization incentives (tax allowances, local-content credits) can unlock capex support but increase compliance workload; aligning supply chains to capture preferential opportunities is essential for KAP.

Trade and tariff exposure

Import tariffs on chemicals and equipment materially squeeze margins; AfCFTA covers 54 countries and targets tariff liberalization of about 90% of goods, while SADC comprises 16 member states requiring customs agility for market access; anti-dumping measures in the region can abruptly shift pricing dynamics; KAP must maintain flexible sourcing and rigorous trade compliance.

- Tariff exposure

- AfCFTA ~90% liberalisation

- SADC 16 members — customs agility

- Anti-dumping risk

- Flexible sourcing & compliance

Energy policy trajectory

Regulatory support for private generation and renewables lowers load-shedding exposure and improves supply security, while licensing and wheeling frameworks directly affect project timelines and bankability. Fuel levies and carbon pricing — EU ETS around €90/ton in 2024 — shift operating costs toward low-carbon generation. KAP benefits from early participation in IPP rounds and embedded generation to lock lower long-term marginal costs and hedge grid risk.

- Regulatory support: improves supply security

- Licensing/wheeling: affects project viability and financing

- Carbon price: ~€90/ton (EU ETS 2024) increases fossil operating costs

- KAP advantage: early IPP/embedded generation reduces long-term marginal cost

Policy, ports and carbon pricing reshape manufacturing, procurement and AfCFTA trade

Policy stability post‑May 2024 election and cabinet changes affects permits and energy policy; manufacturing ~13% of GDP. Transnet turnaround and port reforms determine freight costs; public procurement ≈R1.5tn (2023/24). B‑BBEE levels drive contract access; AfCFTA 54 countries ~90% liberalisation impacts tariffs. Renewables policy and carbon pricing (EU ETS ~€90/t in 2024) shift operating costs.

| Metric | Value |

|---|---|

| Manufacturing % GDP | ~13% |

| Public procurement 2023/24 | R1.5tn |

| AfCFTA coverage | 54 countries; ~90% liberalisation |

| EU ETS 2024 | ~€90/ton |

What is included in the product

Explores how external macro-environmental factors uniquely affect the KAP across six dimensions: Political, Economic, Social, Technological, Environmental, and Legal. Backed by current data and forward-looking insights, it helps executives, consultants, and entrepreneurs identify risks, opportunities, and strategic actions tailored to the KAP's region and industry.

KAP PESTLE delivers a clean, visually segmented summary of external risks and opportunities for quick reference in meetings or presentations. It’s editable, shareable, and written in simple language to align teams fast.

Economic factors

GDP and freight cycles

Logistics volumes closely follow GDP and industrial output; IMF estimated global GDP growth at about 3.1% in 2024 and 3.0% in 2025, signalling modest demand for freight after pandemic-era swings. Slower growth compresses yields and utilization, pushing spot rates down and idle capacity up. Upswings require rapid capacity scaling—container spot rates jumped intermittently by over 40% in past cycles—so KAP should balance fixed and variable fleet capacity to smooth volatility.

Rand volatility

Rand volatility directly raises costs for KAP by increasing prices of imported chemical feedstock, capex and USD-denominated debt servicing; USD/ZAR traded around 18.5 in mid‑2025, up from ~17.0 a year earlier, amplifying input cost pressure. A weaker rand has lifted equipment and feedstock costs by double digits for some suppliers. Active FX hedging, aligning rand revenues with import exposure and contractual pricing clauses help protect margins.

Inflation and rates

High inflation—headline CPI running 3–8% across major markets in 2024—lifts wages, fuel and maintenance costs, squeezing margins for KAP. Interest rates (Fed funds 5.25–5.50% in 2024; ECB and BoE similarly elevated) increase financing costs for fleet and plants. Pass-through to customers often lags, so KAP needs rigorous cost control and dynamic pricing to protect cash flow.

Commodity and energy costs

Oil and petrochemical prices drive logistics fuel and chemical inputs; Brent averaged about 85 USD/bbl in 2024 and traded 80–95 USD/bbl in early 2025, raising transport and feedstock costs ~12–18% YoY. Industrial electricity tariffs rose ~6–10% in many markets in 2024 and outages added up to ~4% of OPEX. Efficiency programs and energy diversification can cut energy spend 10–25%, and procurement should lock 12–24 month hedges or long-term supply deals.

- Price exposure: Brent ~85 USD/bbl (2024 average)

- Tariff/outage impact: +6–10% tariffs, outages ≈4% OPEX

- Mitigation: efficiency 10–25% savings; 12–24 month hedges

Labor market dynamics

Skilled labor shortages are constraining output and pushing wage growth higher; US job openings remained elevated at about 8.1 million in Dec 2024 (BLS JOLTS), sustaining upward wage pressure and productivity drag. Unionized sectors complicate staffing strategies with collective bargaining and higher turnover risk, while targeted training pipelines and retention programs are increasingly essential. Automation investments can progressively offset shortages and restore margins over a multi-year horizon.

- Skilled shortages: 8.1M US job openings (Dec 2024, BLS)

- Wage pressure: sustained above-prepandemic growth in 2024

- Union complexity: higher negotiation-driven cost volatility

- Mitigation: training, retention, automation

Policy, ports and carbon pricing reshape manufacturing, procurement and AfCFTA trade

Global GDP growth slowed to IMF estimates of 3.1% (2024) and 3.0% (2025), moderating freight demand and rate volatility.

Rand at ~18.5 ZAR/USD mid-2025 raises import, capex and debt costs; Brent ~85 USD/bbl (2024 avg) keeps fuel/feedstock high.

High inflation (CPI 3–8% in 2024) and elevated rates (Fed 5.25–5.50% 2024) squeeze margins; hedge, pricing and efficiency are essential.

| Metric | Value |

|---|---|

| GDP growth | 3.1% (2024), 3.0% (2025) |

| USD/ZAR | ~18.5 (mid‑2025) |

| Brent | ~85 USD/bbl (2024 avg) |

Same Document Delivered

KAP PESTLE Analysis

The preview shown here is the exact KAP PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or teasers. After payment you’ll instantly own this finished, professionally structured report.

Description

Your Competitive Advantage Starts with This Report

Unlock how political, economic, social, technological, legal, and environmental forces are shaping KAP’s trajectory with our concise PESTLE snapshot—ideal for investors and strategists who need actionable context fast. Buy the full analysis to access detailed risks, opportunities, and ready-to-use insights for smarter decisions.

Political factors

Policy stability in SA

Policy stability after the May 2024 national election and subsequent cabinet reshuffle directly affects logistics, chemicals and manufacturing permits, with manufacturing representing about 13% of South Africa’s GDP. Shifts in industrial and energy policy drive input-cost volatility and can delay capital deployment; persistent Eskom constraints remain a material risk. KAP must monitor cabinet priorities and policy continuity and use scenario planning to hedge abrupt changes.

State logistics governance

Transnet performance and the 2024 Transnet turnaround plan directly affect freight reliability and costs, while port reforms shape berth availability and tariffs. Expanded public‑private collaborations and concessioning since 2024 can open capacity but require tight KPIs. Governance lapses risk service drops; KAP must embed route diversification and contract clauses reflecting these operational risks.

B-BBEE and localization

B-BBEE rules shape ownership, procurement and supplier development and KAP must improve equity ownership and supplier-development metrics to compete for large contracts. Firms with level 1–2 B-BBEE scores secure preferential access to state and corporate deals; South African public procurement was about R1.5 trillion in 2023/24, with B-BBEE points decisive on many awards. Localization incentives (tax allowances, local-content credits) can unlock capex support but increase compliance workload; aligning supply chains to capture preferential opportunities is essential for KAP.

Trade and tariff exposure

Import tariffs on chemicals and equipment materially squeeze margins; AfCFTA covers 54 countries and targets tariff liberalization of about 90% of goods, while SADC comprises 16 member states requiring customs agility for market access; anti-dumping measures in the region can abruptly shift pricing dynamics; KAP must maintain flexible sourcing and rigorous trade compliance.

- Tariff exposure

- AfCFTA ~90% liberalisation

- SADC 16 members — customs agility

- Anti-dumping risk

- Flexible sourcing & compliance

Energy policy trajectory

Regulatory support for private generation and renewables lowers load-shedding exposure and improves supply security, while licensing and wheeling frameworks directly affect project timelines and bankability. Fuel levies and carbon pricing — EU ETS around €90/ton in 2024 — shift operating costs toward low-carbon generation. KAP benefits from early participation in IPP rounds and embedded generation to lock lower long-term marginal costs and hedge grid risk.

- Regulatory support: improves supply security

- Licensing/wheeling: affects project viability and financing

- Carbon price: ~€90/ton (EU ETS 2024) increases fossil operating costs

- KAP advantage: early IPP/embedded generation reduces long-term marginal cost

Policy, ports and carbon pricing reshape manufacturing, procurement and AfCFTA trade

Policy stability post‑May 2024 election and cabinet changes affects permits and energy policy; manufacturing ~13% of GDP. Transnet turnaround and port reforms determine freight costs; public procurement ≈R1.5tn (2023/24). B‑BBEE levels drive contract access; AfCFTA 54 countries ~90% liberalisation impacts tariffs. Renewables policy and carbon pricing (EU ETS ~€90/t in 2024) shift operating costs.

| Metric | Value |

|---|---|

| Manufacturing % GDP | ~13% |

| Public procurement 2023/24 | R1.5tn |

| AfCFTA coverage | 54 countries; ~90% liberalisation |

| EU ETS 2024 | ~€90/ton |

What is included in the product

Explores how external macro-environmental factors uniquely affect the KAP across six dimensions: Political, Economic, Social, Technological, Environmental, and Legal. Backed by current data and forward-looking insights, it helps executives, consultants, and entrepreneurs identify risks, opportunities, and strategic actions tailored to the KAP's region and industry.

KAP PESTLE delivers a clean, visually segmented summary of external risks and opportunities for quick reference in meetings or presentations. It’s editable, shareable, and written in simple language to align teams fast.

Economic factors

GDP and freight cycles

Logistics volumes closely follow GDP and industrial output; IMF estimated global GDP growth at about 3.1% in 2024 and 3.0% in 2025, signalling modest demand for freight after pandemic-era swings. Slower growth compresses yields and utilization, pushing spot rates down and idle capacity up. Upswings require rapid capacity scaling—container spot rates jumped intermittently by over 40% in past cycles—so KAP should balance fixed and variable fleet capacity to smooth volatility.

Rand volatility

Rand volatility directly raises costs for KAP by increasing prices of imported chemical feedstock, capex and USD-denominated debt servicing; USD/ZAR traded around 18.5 in mid‑2025, up from ~17.0 a year earlier, amplifying input cost pressure. A weaker rand has lifted equipment and feedstock costs by double digits for some suppliers. Active FX hedging, aligning rand revenues with import exposure and contractual pricing clauses help protect margins.

Inflation and rates

High inflation—headline CPI running 3–8% across major markets in 2024—lifts wages, fuel and maintenance costs, squeezing margins for KAP. Interest rates (Fed funds 5.25–5.50% in 2024; ECB and BoE similarly elevated) increase financing costs for fleet and plants. Pass-through to customers often lags, so KAP needs rigorous cost control and dynamic pricing to protect cash flow.

Commodity and energy costs

Oil and petrochemical prices drive logistics fuel and chemical inputs; Brent averaged about 85 USD/bbl in 2024 and traded 80–95 USD/bbl in early 2025, raising transport and feedstock costs ~12–18% YoY. Industrial electricity tariffs rose ~6–10% in many markets in 2024 and outages added up to ~4% of OPEX. Efficiency programs and energy diversification can cut energy spend 10–25%, and procurement should lock 12–24 month hedges or long-term supply deals.

- Price exposure: Brent ~85 USD/bbl (2024 average)

- Tariff/outage impact: +6–10% tariffs, outages ≈4% OPEX

- Mitigation: efficiency 10–25% savings; 12–24 month hedges

Labor market dynamics

Skilled labor shortages are constraining output and pushing wage growth higher; US job openings remained elevated at about 8.1 million in Dec 2024 (BLS JOLTS), sustaining upward wage pressure and productivity drag. Unionized sectors complicate staffing strategies with collective bargaining and higher turnover risk, while targeted training pipelines and retention programs are increasingly essential. Automation investments can progressively offset shortages and restore margins over a multi-year horizon.

- Skilled shortages: 8.1M US job openings (Dec 2024, BLS)

- Wage pressure: sustained above-prepandemic growth in 2024

- Union complexity: higher negotiation-driven cost volatility

- Mitigation: training, retention, automation

Policy, ports and carbon pricing reshape manufacturing, procurement and AfCFTA trade

Global GDP growth slowed to IMF estimates of 3.1% (2024) and 3.0% (2025), moderating freight demand and rate volatility.

Rand at ~18.5 ZAR/USD mid-2025 raises import, capex and debt costs; Brent ~85 USD/bbl (2024 avg) keeps fuel/feedstock high.

High inflation (CPI 3–8% in 2024) and elevated rates (Fed 5.25–5.50% 2024) squeeze margins; hedge, pricing and efficiency are essential.

| Metric | Value |

|---|---|

| GDP growth | 3.1% (2024), 3.0% (2025) |

| USD/ZAR | ~18.5 (mid‑2025) |

| Brent | ~85 USD/bbl (2024 avg) |

Same Document Delivered

KAP PESTLE Analysis

The preview shown here is the exact KAP PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file, with no placeholders or teasers. After payment you’ll instantly own this finished, professionally structured report.