Karoon Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

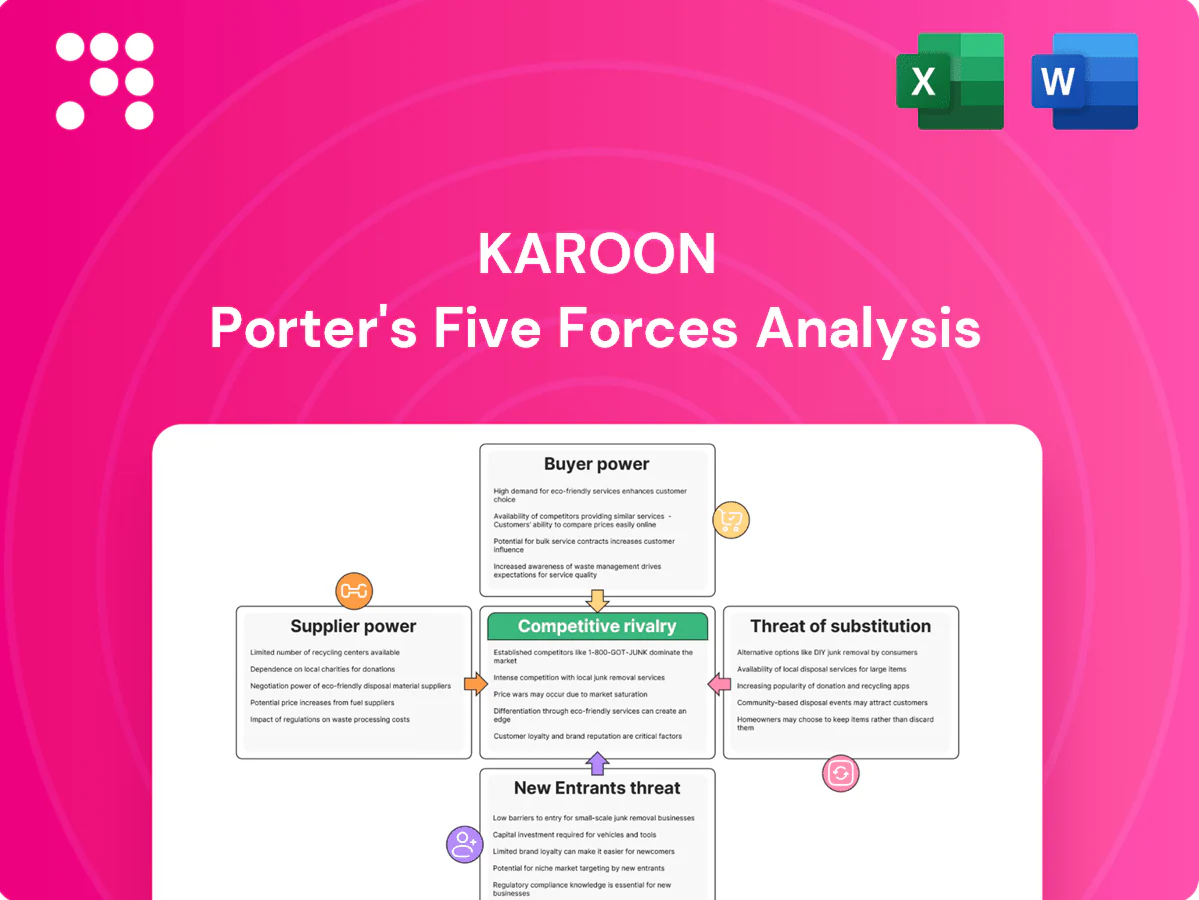

Karoon’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, entrant threats and substitute risks shaping its margins and growth outlook. This concise view surfaces key competitive dynamics and strategic vulnerabilities investors should note. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals and actionable insights to inform smarter investment and strategic decisions.

Suppliers Bargaining Power

Concentrated oilfield services

Drilling rigs, subsea systems and completion services are concentrated among a few OEMs and contractors, with the top five oilfield services firms generating over $100 billion in combined revenue in 2024, limiting alternatives and raising Karoon’s switching costs and scheduling risk. Vendor backlogs and cyclical pricing pressure can compress margins. Strategic partnerships and multi-year contracts (typical 3–5 years) can partially mitigate supplier power.

FPSO and marine logistics dependence

Production in Brazil heavily relies on leased FPSOs and specialized vessels; by 2024 Brazil hosted about 40–50 of the global ~150 FPSO fleet, concentrating supplier power. Availability and dayrates are cyclical — market tightness pushed dayrates from typical $150–$300k/day to spikes of 30–60% in 2022–24. Unplanned downtime shifts operational leverage to suppliers, so negotiating uptime-linked, availability-based payment terms mitigates that risk and aligns incentives.

Local content and regulatory-driven sourcing

Brazil’s 2024 local content and compliance rules narrow Karoon’s eligible supplier base, concentrating bargaining power with qualified domestic providers such as those favored in Petrobras procurement policies. Certification and audits raise procurement timelines and costs, often adding months to project schedules and measurable cost premiums. Early vendor engagement and prequalification reduce delay risk and help contain inflationary pass-throughs.

Specialized technology and data providers

Seismic, reservoir modeling and digital solutions are supplied by niche specialists, creating technical lock-ins; major operators in 2024 still rely heavily on vendor-specific toolchains. License and service fees materially affect unit economics, with enterprise software subscriptions often representing a significant recurring cost. Adoption of open-standard architectures (eg OSDU) in 2024 improved data portability and reduced migration friction for many operators.

- Vendor lock-in: niche proprietary tech

- Costs: recurring license/service fees impact margins

- Portability: open standards (OSDU) rising in 2024

Skilled labor and HSE requirements

- Vacancy rate ~15%

- Wage inflation 6–8% (2024)

- Training lead time 18–36 months

- Contract clauses: safety KPIs, LDs, performance bonds

Supplier power squeezes margins; Brazil hosts 40-50 of global FPSOs

Supplier power is high: top oilfield OEMs and contractors concentrate supply, raising switching costs and margin risk. Brazil hosts ~40–50 of the ~150 global FPSOs (2024), tightening dayrates and availability. Crew vacancy ~15% and wage inflation 6–8% (2024) sustain supplier leverage; OSDU uptake in 2024 began lowering software lock-in.

| Metric | 2024 | Implication |

|---|---|---|

| Top OEM concentration | Top5>$100bn revenue | High switching cost |

| FPSOs in Brazil | 40–50/150 | Availability pressure |

| Crew vacancy/wage | 15% / 6–8% | Cost inflation |

What is included in the product

Provides a tailored Porter’s Five Forces assessment of Karoon, uncovering competitive intensity, buyer and supplier leverage, threat of new entrants and substitutes, and industry rivalry; highlights disruptive threats and strategic levers to protect margins and inform investor or management decisions.

Concise Karoon Porter’s Five Forces—visualizes supplier, buyer, entrant, substitute and rivalry pressures to pinpoint strategic pain points and speed boardroom decisions.

Customers Bargaining Power

Commodity price-taking dynamics

Crude is sold on Brent terms, with Brent averaging about 86 USD/bbl in 2024, constraining Karoon’s pricing discretion and allowing buyers to benchmark and press for narrow differentials. Revenue swings are driven largely by global price moves rather than bilateral contracts. Company hedging programs can dampen realized volatility but cannot fully remove market exposure.

Differentials by crude quality and location

API gravity and sulfur drive realized prices: light sweet grades (>30° API, <0.5% S) fetched premiums of roughly $2–4/bbl in 2024 versus heavy sour discounts of $3–6/bbl. Proximity to Brazilian refineries or export routes lowered netback erosion; transport/handling added commonly $1–5/bbl inland, while optimized offtake logistics cut discount pressure by up to ~$1.5/bbl.

Diverse buyer base of traders and refiners

Karoon's buyers include multiple global traders and regional refiners, with the top three traders handling roughly 40% of physical crude flows in 2024, limiting single-buyer dominance. A mix of spot and term contracts (typical terms 12–36 months) gives counterparties optionality, yet suppliers can be switched within days to weeks. Deeper, reliable relationships still secure preferential liftings and payment terms.

Contractual terms and credit risk

Payment terms, lifting schedules and quality tolerances are negotiated case-by-case; in 2024 strong buyers increasingly demand tighter specs and contractual penalties, raising operational risk for sellers. Credit and counterparty risk management directly compresses achievable pricing, while pre-approval processes and letters of credit materially improve cash security amid a global trade finance gap of about 2.5 trillion USD in 2024.

- Payment terms: negotiated timing and security

- Lifting schedules: delivery flexibility vs penalties

- Quality tolerances: tighter specs raise costs

- Risk mitigation: pre-approval, LCs improve pricing leverage

ESG-driven demand shifts

Buyers increasingly prioritize lower-carbon barrels and traceability; 2024 offtake markets show verified low-carbon crude trades earning premiums (reported range roughly $2–6 per barrel) and better access to European and Asian refiners. Carbon intensity disclosures and emissions management raise supplier attractiveness; certification (e.g., low-carbon or methane intensity labels) unlocks offtake channels and premium pools.

- Traceability: higher demand from refiners and majors

- Premiums: ~$2–6/boe reported in 2024

- Disclosure: required by many buyers for contract access

- Certification: opens new offtake streams

Buyers have medium leverage; Brent 86 USD/bbl, top-3 traders ~40%

Buyers exert medium bargaining power: Brent pricing (~86 USD/bbl in 2024) caps seller pricing, while top-three traders handled ~40% of flows giving buyers concentration leverage. Quality and low-carbon premiums (~2–6 USD/bbl) and transport costs (1–5 USD/bbl) materially shift netbacks; term contracts (12–36 months) and LCs partly mitigate buyer optionality.

| Metric | 2024 value |

|---|---|

| Brent average | 86 USD/bbl |

| Top-3 traders share | ~40% |

| Low-carbon premium | 2–6 USD/bbl |

| Transport impact | 1–5 USD/bbl |

| Contract terms | 12–36 months |

Preview the Actual Deliverable

Karoon Porter's Five Forces Analysis

This preview is the exact Karoon Porter Five Forces analysis you'll receive after purchase: a concise evaluation of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. The document is fully formatted, final and ready for immediate download and use.

Go Beyond the Preview—Access the Full Strategic Report

Karoon’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, entrant threats and substitute risks shaping its margins and growth outlook. This concise view surfaces key competitive dynamics and strategic vulnerabilities investors should note. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals and actionable insights to inform smarter investment and strategic decisions.

Suppliers Bargaining Power

Concentrated oilfield services

Drilling rigs, subsea systems and completion services are concentrated among a few OEMs and contractors, with the top five oilfield services firms generating over $100 billion in combined revenue in 2024, limiting alternatives and raising Karoon’s switching costs and scheduling risk. Vendor backlogs and cyclical pricing pressure can compress margins. Strategic partnerships and multi-year contracts (typical 3–5 years) can partially mitigate supplier power.

FPSO and marine logistics dependence

Production in Brazil heavily relies on leased FPSOs and specialized vessels; by 2024 Brazil hosted about 40–50 of the global ~150 FPSO fleet, concentrating supplier power. Availability and dayrates are cyclical — market tightness pushed dayrates from typical $150–$300k/day to spikes of 30–60% in 2022–24. Unplanned downtime shifts operational leverage to suppliers, so negotiating uptime-linked, availability-based payment terms mitigates that risk and aligns incentives.

Local content and regulatory-driven sourcing

Brazil’s 2024 local content and compliance rules narrow Karoon’s eligible supplier base, concentrating bargaining power with qualified domestic providers such as those favored in Petrobras procurement policies. Certification and audits raise procurement timelines and costs, often adding months to project schedules and measurable cost premiums. Early vendor engagement and prequalification reduce delay risk and help contain inflationary pass-throughs.

Specialized technology and data providers

Seismic, reservoir modeling and digital solutions are supplied by niche specialists, creating technical lock-ins; major operators in 2024 still rely heavily on vendor-specific toolchains. License and service fees materially affect unit economics, with enterprise software subscriptions often representing a significant recurring cost. Adoption of open-standard architectures (eg OSDU) in 2024 improved data portability and reduced migration friction for many operators.

- Vendor lock-in: niche proprietary tech

- Costs: recurring license/service fees impact margins

- Portability: open standards (OSDU) rising in 2024

Skilled labor and HSE requirements

- Vacancy rate ~15%

- Wage inflation 6–8% (2024)

- Training lead time 18–36 months

- Contract clauses: safety KPIs, LDs, performance bonds

Supplier power squeezes margins; Brazil hosts 40-50 of global FPSOs

Supplier power is high: top oilfield OEMs and contractors concentrate supply, raising switching costs and margin risk. Brazil hosts ~40–50 of the ~150 global FPSOs (2024), tightening dayrates and availability. Crew vacancy ~15% and wage inflation 6–8% (2024) sustain supplier leverage; OSDU uptake in 2024 began lowering software lock-in.

| Metric | 2024 | Implication |

|---|---|---|

| Top OEM concentration | Top5>$100bn revenue | High switching cost |

| FPSOs in Brazil | 40–50/150 | Availability pressure |

| Crew vacancy/wage | 15% / 6–8% | Cost inflation |

What is included in the product

Provides a tailored Porter’s Five Forces assessment of Karoon, uncovering competitive intensity, buyer and supplier leverage, threat of new entrants and substitutes, and industry rivalry; highlights disruptive threats and strategic levers to protect margins and inform investor or management decisions.

Concise Karoon Porter’s Five Forces—visualizes supplier, buyer, entrant, substitute and rivalry pressures to pinpoint strategic pain points and speed boardroom decisions.

Customers Bargaining Power

Commodity price-taking dynamics

Crude is sold on Brent terms, with Brent averaging about 86 USD/bbl in 2024, constraining Karoon’s pricing discretion and allowing buyers to benchmark and press for narrow differentials. Revenue swings are driven largely by global price moves rather than bilateral contracts. Company hedging programs can dampen realized volatility but cannot fully remove market exposure.

Differentials by crude quality and location

API gravity and sulfur drive realized prices: light sweet grades (>30° API, <0.5% S) fetched premiums of roughly $2–4/bbl in 2024 versus heavy sour discounts of $3–6/bbl. Proximity to Brazilian refineries or export routes lowered netback erosion; transport/handling added commonly $1–5/bbl inland, while optimized offtake logistics cut discount pressure by up to ~$1.5/bbl.

Diverse buyer base of traders and refiners

Karoon's buyers include multiple global traders and regional refiners, with the top three traders handling roughly 40% of physical crude flows in 2024, limiting single-buyer dominance. A mix of spot and term contracts (typical terms 12–36 months) gives counterparties optionality, yet suppliers can be switched within days to weeks. Deeper, reliable relationships still secure preferential liftings and payment terms.

Contractual terms and credit risk

Payment terms, lifting schedules and quality tolerances are negotiated case-by-case; in 2024 strong buyers increasingly demand tighter specs and contractual penalties, raising operational risk for sellers. Credit and counterparty risk management directly compresses achievable pricing, while pre-approval processes and letters of credit materially improve cash security amid a global trade finance gap of about 2.5 trillion USD in 2024.

- Payment terms: negotiated timing and security

- Lifting schedules: delivery flexibility vs penalties

- Quality tolerances: tighter specs raise costs

- Risk mitigation: pre-approval, LCs improve pricing leverage

ESG-driven demand shifts

Buyers increasingly prioritize lower-carbon barrels and traceability; 2024 offtake markets show verified low-carbon crude trades earning premiums (reported range roughly $2–6 per barrel) and better access to European and Asian refiners. Carbon intensity disclosures and emissions management raise supplier attractiveness; certification (e.g., low-carbon or methane intensity labels) unlocks offtake channels and premium pools.

- Traceability: higher demand from refiners and majors

- Premiums: ~$2–6/boe reported in 2024

- Disclosure: required by many buyers for contract access

- Certification: opens new offtake streams

Buyers have medium leverage; Brent 86 USD/bbl, top-3 traders ~40%

Buyers exert medium bargaining power: Brent pricing (~86 USD/bbl in 2024) caps seller pricing, while top-three traders handled ~40% of flows giving buyers concentration leverage. Quality and low-carbon premiums (~2–6 USD/bbl) and transport costs (1–5 USD/bbl) materially shift netbacks; term contracts (12–36 months) and LCs partly mitigate buyer optionality.

| Metric | 2024 value |

|---|---|

| Brent average | 86 USD/bbl |

| Top-3 traders share | ~40% |

| Low-carbon premium | 2–6 USD/bbl |

| Transport impact | 1–5 USD/bbl |

| Contract terms | 12–36 months |

Preview the Actual Deliverable

Karoon Porter's Five Forces Analysis

This preview is the exact Karoon Porter Five Forces analysis you'll receive after purchase: a concise evaluation of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. The document is fully formatted, final and ready for immediate download and use.

Description

Go Beyond the Preview—Access the Full Strategic Report

Karoon’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, entrant threats and substitute risks shaping its margins and growth outlook. This concise view surfaces key competitive dynamics and strategic vulnerabilities investors should note. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals and actionable insights to inform smarter investment and strategic decisions.

Suppliers Bargaining Power

Concentrated oilfield services

Drilling rigs, subsea systems and completion services are concentrated among a few OEMs and contractors, with the top five oilfield services firms generating over $100 billion in combined revenue in 2024, limiting alternatives and raising Karoon’s switching costs and scheduling risk. Vendor backlogs and cyclical pricing pressure can compress margins. Strategic partnerships and multi-year contracts (typical 3–5 years) can partially mitigate supplier power.

FPSO and marine logistics dependence

Production in Brazil heavily relies on leased FPSOs and specialized vessels; by 2024 Brazil hosted about 40–50 of the global ~150 FPSO fleet, concentrating supplier power. Availability and dayrates are cyclical — market tightness pushed dayrates from typical $150–$300k/day to spikes of 30–60% in 2022–24. Unplanned downtime shifts operational leverage to suppliers, so negotiating uptime-linked, availability-based payment terms mitigates that risk and aligns incentives.

Local content and regulatory-driven sourcing

Brazil’s 2024 local content and compliance rules narrow Karoon’s eligible supplier base, concentrating bargaining power with qualified domestic providers such as those favored in Petrobras procurement policies. Certification and audits raise procurement timelines and costs, often adding months to project schedules and measurable cost premiums. Early vendor engagement and prequalification reduce delay risk and help contain inflationary pass-throughs.

Specialized technology and data providers

Seismic, reservoir modeling and digital solutions are supplied by niche specialists, creating technical lock-ins; major operators in 2024 still rely heavily on vendor-specific toolchains. License and service fees materially affect unit economics, with enterprise software subscriptions often representing a significant recurring cost. Adoption of open-standard architectures (eg OSDU) in 2024 improved data portability and reduced migration friction for many operators.

- Vendor lock-in: niche proprietary tech

- Costs: recurring license/service fees impact margins

- Portability: open standards (OSDU) rising in 2024

Skilled labor and HSE requirements

- Vacancy rate ~15%

- Wage inflation 6–8% (2024)

- Training lead time 18–36 months

- Contract clauses: safety KPIs, LDs, performance bonds

Supplier power squeezes margins; Brazil hosts 40-50 of global FPSOs

Supplier power is high: top oilfield OEMs and contractors concentrate supply, raising switching costs and margin risk. Brazil hosts ~40–50 of the ~150 global FPSOs (2024), tightening dayrates and availability. Crew vacancy ~15% and wage inflation 6–8% (2024) sustain supplier leverage; OSDU uptake in 2024 began lowering software lock-in.

| Metric | 2024 | Implication |

|---|---|---|

| Top OEM concentration | Top5>$100bn revenue | High switching cost |

| FPSOs in Brazil | 40–50/150 | Availability pressure |

| Crew vacancy/wage | 15% / 6–8% | Cost inflation |

What is included in the product

Provides a tailored Porter’s Five Forces assessment of Karoon, uncovering competitive intensity, buyer and supplier leverage, threat of new entrants and substitutes, and industry rivalry; highlights disruptive threats and strategic levers to protect margins and inform investor or management decisions.

Concise Karoon Porter’s Five Forces—visualizes supplier, buyer, entrant, substitute and rivalry pressures to pinpoint strategic pain points and speed boardroom decisions.

Customers Bargaining Power

Commodity price-taking dynamics

Crude is sold on Brent terms, with Brent averaging about 86 USD/bbl in 2024, constraining Karoon’s pricing discretion and allowing buyers to benchmark and press for narrow differentials. Revenue swings are driven largely by global price moves rather than bilateral contracts. Company hedging programs can dampen realized volatility but cannot fully remove market exposure.

Differentials by crude quality and location

API gravity and sulfur drive realized prices: light sweet grades (>30° API, <0.5% S) fetched premiums of roughly $2–4/bbl in 2024 versus heavy sour discounts of $3–6/bbl. Proximity to Brazilian refineries or export routes lowered netback erosion; transport/handling added commonly $1–5/bbl inland, while optimized offtake logistics cut discount pressure by up to ~$1.5/bbl.

Diverse buyer base of traders and refiners

Karoon's buyers include multiple global traders and regional refiners, with the top three traders handling roughly 40% of physical crude flows in 2024, limiting single-buyer dominance. A mix of spot and term contracts (typical terms 12–36 months) gives counterparties optionality, yet suppliers can be switched within days to weeks. Deeper, reliable relationships still secure preferential liftings and payment terms.

Contractual terms and credit risk

Payment terms, lifting schedules and quality tolerances are negotiated case-by-case; in 2024 strong buyers increasingly demand tighter specs and contractual penalties, raising operational risk for sellers. Credit and counterparty risk management directly compresses achievable pricing, while pre-approval processes and letters of credit materially improve cash security amid a global trade finance gap of about 2.5 trillion USD in 2024.

- Payment terms: negotiated timing and security

- Lifting schedules: delivery flexibility vs penalties

- Quality tolerances: tighter specs raise costs

- Risk mitigation: pre-approval, LCs improve pricing leverage

ESG-driven demand shifts

Buyers increasingly prioritize lower-carbon barrels and traceability; 2024 offtake markets show verified low-carbon crude trades earning premiums (reported range roughly $2–6 per barrel) and better access to European and Asian refiners. Carbon intensity disclosures and emissions management raise supplier attractiveness; certification (e.g., low-carbon or methane intensity labels) unlocks offtake channels and premium pools.

- Traceability: higher demand from refiners and majors

- Premiums: ~$2–6/boe reported in 2024

- Disclosure: required by many buyers for contract access

- Certification: opens new offtake streams

Buyers have medium leverage; Brent 86 USD/bbl, top-3 traders ~40%

Buyers exert medium bargaining power: Brent pricing (~86 USD/bbl in 2024) caps seller pricing, while top-three traders handled ~40% of flows giving buyers concentration leverage. Quality and low-carbon premiums (~2–6 USD/bbl) and transport costs (1–5 USD/bbl) materially shift netbacks; term contracts (12–36 months) and LCs partly mitigate buyer optionality.

| Metric | 2024 value |

|---|---|

| Brent average | 86 USD/bbl |

| Top-3 traders share | ~40% |

| Low-carbon premium | 2–6 USD/bbl |

| Transport impact | 1–5 USD/bbl |

| Contract terms | 12–36 months |

Preview the Actual Deliverable

Karoon Porter's Five Forces Analysis

This preview is the exact Karoon Porter Five Forces analysis you'll receive after purchase: a concise evaluation of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. The document is fully formatted, final and ready for immediate download and use.