Kaufman & Broad Porter's Five Forces Analysis

From Overview to Strategy Blueprint

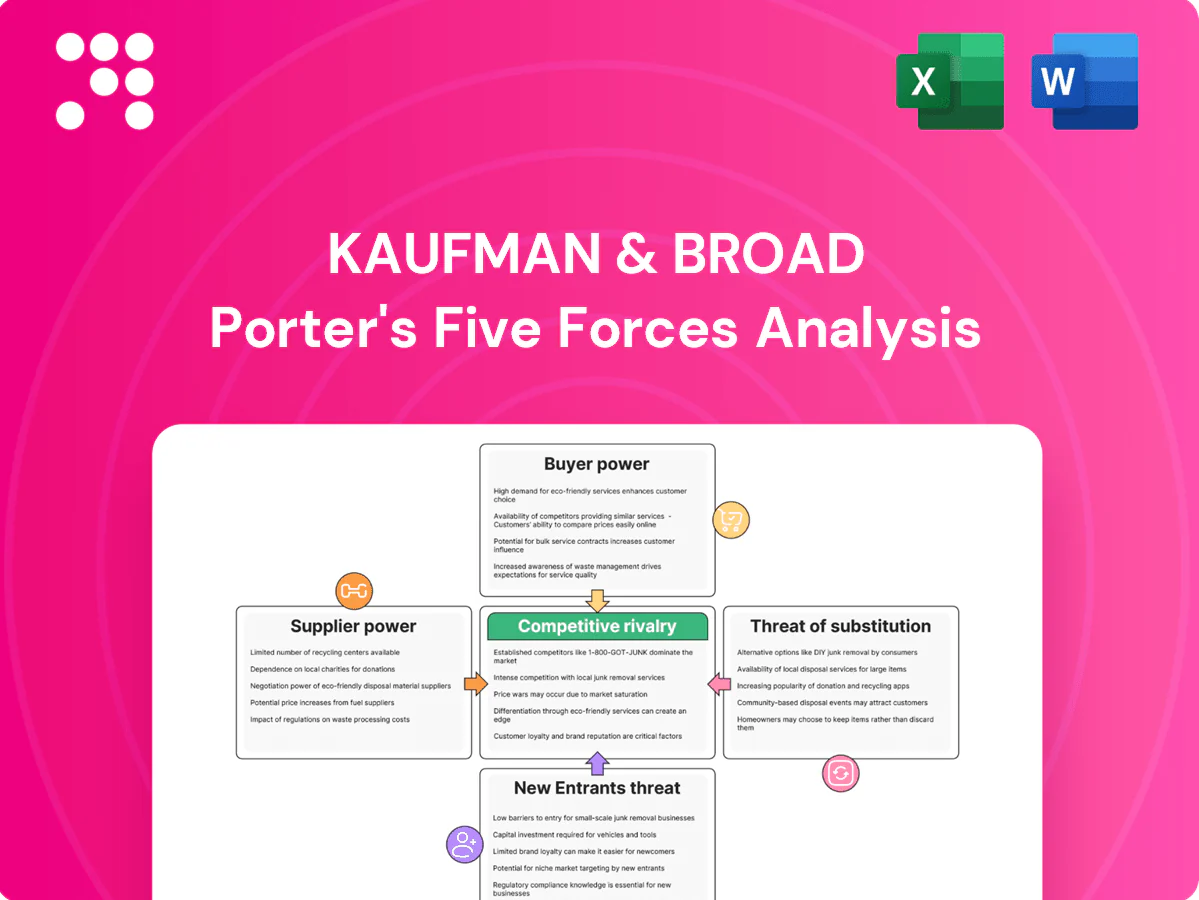

Kaufman & Broad faces moderate buyer power, concentrated suppliers in construction inputs, and steady threats from new entrants and substitutes as urban housing evolves. This snapshot highlights strategic pressure points and competitive levers. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Kaufman & Broad’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated materials suppliers

Core inputs like cement, steel, glass and insulation come from a concentrated EU supplier base, giving suppliers pricing leverage and making materials roughly 40% of build costs in France (2024). Energy-linked input swings have driven volatility — material price indices moved about 15% between 2022–2024, often passed to developers. Kaufman & Broad mitigates via framework contracts and vendor diversification, but technical standards and sudden spikes still compress margins.

Scarce specialized subcontractors

MEP, façade and finishing subcontractors are capacity-constrained in busy regions; in 2024 subcontractor bid premiums rose roughly 5–8% and average MEP lead times lengthened by about 4–6 weeks, enabling specialists to cherry-pick higher-margin work or demand tougher payment and warranty terms. This elevates execution risk and scheduling/holding costs for large residential programs. Preferred-partner agreements and steady volumes can temper their pricing power.

Landowners and municipalities

Buildable land is the scarcest supplier, with landowners and municipalities controlling zoning, permits and often extracting premiums; in tight urban markets land can represent 30–50% of total development cost. Competitive tenders for prime plots routinely push prices up and attach design or affordability obligations, increasing acquisition bids by double-digit percentages. Municipal gatekeeping typically lengthens timelines by 6–18 months and raises soft costs (planning, studies, levies) by 5–15%. Early-stage land assembly and strong urban relationships are therefore critical to rebalance supplier power and secure project viability.

Labor costs and regulation

- Wage inflation: ~6% (2024)

- Collective coverage: ~70%

- Safety/training add to baseline costs

- Mitigation: planning, productivity tech

ESG and imported components

ESG-driven demand for low-carbon materials, certified timber and traceable fixtures in 2024 narrows Kaufman & Broad’s supplier pool, raising supplier leverage as import-dependent items face FX swings (≈8–12% intrayear in 2023–24) and logistics cost volatility; institutional sales with ESG clauses (≈60% of large French contracts in 2024) reinforce strict sourcing and pricing power.

- Certified timber limits suppliers

- Imports exposed to FX/logistics

- Institutional ESG boosts supplier leverage

- Dual-sourcing & design-to-value reduce exposure

Suppliers' leverage: materials ≈40%, indices ≈15%, ESG ≈60%

Suppliers hold strong leverage: core materials ≈40% of build cost (France, 2024) with material indices swinging ≈15% (2022–24), subcontractor premiums up 5–8% and MEP lead times +4–6 weeks, land 30–50% of project cost, labor unit costs +6% (2024) with ~70% collective coverage; institutional ESG clauses ≈60% of large contracts heighten certified-supply constraints.

| Metric | 2024 value |

|---|---|

| Materials % of build | ≈40% |

| Material index swing (2022–24) | ≈15% |

| Subcontractor premium | 5–8% |

| Land % of cost | 30–50% |

| Labor inflation | ≈6% |

| Collective coverage | ≈70% |

| Institutional ESG share | ≈60% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Kaufman & Broad, with detailed evaluation of suppliers, buyers, substitutes, and industry rivalry to inform strategic positioning and investment decisions.

A one-sheet Porter’s Five Forces for Kaufman & Broad that maps competitive pressures, lets you tweak inputs for scenario testing, and exports clean visuals for decks—no macros required.

Customers Bargaining Power

Mortgage-rate sensitivity

Individual buyers’ affordability hinges on French mortgage rates and credit criteria; Banque de France data showed average new housing loan rates near 3.2% in 2024, tightening borrower capacity. When rates rise buyers increasingly demand discounts, upgrades or staged payment plans, boosting their bargaining power and slowing sales velocity. Flexible pricing and phased payments help preserve absorption by aligning cashflows with tighter borrower budgets.

Institutional bulk buyers

Institutional bulk buyers such as funds and social landlords purchase blocks at scale from Kaufman & Broad, leveraging volume to negotiate discounts and specific build specs. Their repeat business anchored ~30% of deliveries in 2024, stabilizing volumes but compressing margins. These buyers impose ESG and delivery KPIs with penalty regimes, so a balanced mix between retail and institutional sales protects pricing and margin volatility.

High comparability across developers

Residential offers from Kaufman & Broad are highly comparable on location, layout and energy performance, so buyers can benchmark easily against other French developers and local players; RE2020 has applied since 2022, making energy labels a standard comparison point. Over 80% of French buyers search listings online (SeLoger/IFOP trends 2024), amplifying price pressure. Differentiation via design, amenities and superior RE2020 performance reduces pure price-only competition.

Quality, warranty, and reputation

Buyers press on snag rates, delivery punctuality and after-sales service; in 2024 surveys roughly 70% of homebuyers said visible defects or delays prompted price concessions or cancellation. Negative reviews convert quickly into lost deals, while Kaufman & Broads stronger brand lowers return risk and lifts willingness to pay. Proactive customer care and digital handover tools (e-delivery, defect tracking) dilute buyer leverage.

- Snag rates & delivery punctuality drive concessions

- Negative reviews → faster deal losses

- Strong brand reduces returns, raises price tolerance

- Digital handover + proactive care weakens buyer power

Policy-driven expectations

Tax-incentivized affordability and energy-efficiency programs in 2024 have anchored buyer expectations on lower prices and higher performance; when incentives tighten, buyers amplify demands for upfront value and efficiency. Builders face rising compliance costs that cannot always be fully passed to buyers, making lifetime-cost messaging (energy savings, maintenance) vital to defend pricing.

- Policy sensitivity: buyers calibrate willingness-to-pay to incentive levels

- Cost pressure: compliance often compresses margins

- Defense: quantified lifetime savings strengthen price resilience

Tighter affordability: 3.2% rates and 30% institutional buying compress prices

Buyers’ affordability tightened as average new housing loan rates ≈3.2% in 2024, increasing discount pressure and demand for staged payments. Institutional bulk buyers (~30% of deliveries 2024) exert volume-driven price/spec leverage. High comparability and online search (~80% of buyers) intensify price competition; snag/delivery issues drove concessions in ~70% of cases. Strong brand and digital aftercare reduce buyer power.

| Metric | 2024 value |

|---|---|

| Avg mortgage rate | ≈3.2% |

| Institutional share | ~30% |

| Online search | ~80% |

| Concession driver (snags) | ~70% |

Full Version Awaits

Kaufman & Broad Porter's Five Forces Analysis

This preview shows the exact Kaufman & Broad Porter’s Five Forces analysis you’ll receive after purchase—no placeholders. It presents the full, professionally formatted assessment of competitive rivalry, supplier and buyer power, and the threats of new entrants and substitutes. You’ll get this identical file instantly upon payment.

From Overview to Strategy Blueprint

Kaufman & Broad faces moderate buyer power, concentrated suppliers in construction inputs, and steady threats from new entrants and substitutes as urban housing evolves. This snapshot highlights strategic pressure points and competitive levers. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Kaufman & Broad’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated materials suppliers

Core inputs like cement, steel, glass and insulation come from a concentrated EU supplier base, giving suppliers pricing leverage and making materials roughly 40% of build costs in France (2024). Energy-linked input swings have driven volatility — material price indices moved about 15% between 2022–2024, often passed to developers. Kaufman & Broad mitigates via framework contracts and vendor diversification, but technical standards and sudden spikes still compress margins.

Scarce specialized subcontractors

MEP, façade and finishing subcontractors are capacity-constrained in busy regions; in 2024 subcontractor bid premiums rose roughly 5–8% and average MEP lead times lengthened by about 4–6 weeks, enabling specialists to cherry-pick higher-margin work or demand tougher payment and warranty terms. This elevates execution risk and scheduling/holding costs for large residential programs. Preferred-partner agreements and steady volumes can temper their pricing power.

Landowners and municipalities

Buildable land is the scarcest supplier, with landowners and municipalities controlling zoning, permits and often extracting premiums; in tight urban markets land can represent 30–50% of total development cost. Competitive tenders for prime plots routinely push prices up and attach design or affordability obligations, increasing acquisition bids by double-digit percentages. Municipal gatekeeping typically lengthens timelines by 6–18 months and raises soft costs (planning, studies, levies) by 5–15%. Early-stage land assembly and strong urban relationships are therefore critical to rebalance supplier power and secure project viability.

Labor costs and regulation

- Wage inflation: ~6% (2024)

- Collective coverage: ~70%

- Safety/training add to baseline costs

- Mitigation: planning, productivity tech

ESG and imported components

ESG-driven demand for low-carbon materials, certified timber and traceable fixtures in 2024 narrows Kaufman & Broad’s supplier pool, raising supplier leverage as import-dependent items face FX swings (≈8–12% intrayear in 2023–24) and logistics cost volatility; institutional sales with ESG clauses (≈60% of large French contracts in 2024) reinforce strict sourcing and pricing power.

- Certified timber limits suppliers

- Imports exposed to FX/logistics

- Institutional ESG boosts supplier leverage

- Dual-sourcing & design-to-value reduce exposure

Suppliers' leverage: materials ≈40%, indices ≈15%, ESG ≈60%

Suppliers hold strong leverage: core materials ≈40% of build cost (France, 2024) with material indices swinging ≈15% (2022–24), subcontractor premiums up 5–8% and MEP lead times +4–6 weeks, land 30–50% of project cost, labor unit costs +6% (2024) with ~70% collective coverage; institutional ESG clauses ≈60% of large contracts heighten certified-supply constraints.

| Metric | 2024 value |

|---|---|

| Materials % of build | ≈40% |

| Material index swing (2022–24) | ≈15% |

| Subcontractor premium | 5–8% |

| Land % of cost | 30–50% |

| Labor inflation | ≈6% |

| Collective coverage | ≈70% |

| Institutional ESG share | ≈60% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Kaufman & Broad, with detailed evaluation of suppliers, buyers, substitutes, and industry rivalry to inform strategic positioning and investment decisions.

A one-sheet Porter’s Five Forces for Kaufman & Broad that maps competitive pressures, lets you tweak inputs for scenario testing, and exports clean visuals for decks—no macros required.

Customers Bargaining Power

Mortgage-rate sensitivity

Individual buyers’ affordability hinges on French mortgage rates and credit criteria; Banque de France data showed average new housing loan rates near 3.2% in 2024, tightening borrower capacity. When rates rise buyers increasingly demand discounts, upgrades or staged payment plans, boosting their bargaining power and slowing sales velocity. Flexible pricing and phased payments help preserve absorption by aligning cashflows with tighter borrower budgets.

Institutional bulk buyers

Institutional bulk buyers such as funds and social landlords purchase blocks at scale from Kaufman & Broad, leveraging volume to negotiate discounts and specific build specs. Their repeat business anchored ~30% of deliveries in 2024, stabilizing volumes but compressing margins. These buyers impose ESG and delivery KPIs with penalty regimes, so a balanced mix between retail and institutional sales protects pricing and margin volatility.

High comparability across developers

Residential offers from Kaufman & Broad are highly comparable on location, layout and energy performance, so buyers can benchmark easily against other French developers and local players; RE2020 has applied since 2022, making energy labels a standard comparison point. Over 80% of French buyers search listings online (SeLoger/IFOP trends 2024), amplifying price pressure. Differentiation via design, amenities and superior RE2020 performance reduces pure price-only competition.

Quality, warranty, and reputation

Buyers press on snag rates, delivery punctuality and after-sales service; in 2024 surveys roughly 70% of homebuyers said visible defects or delays prompted price concessions or cancellation. Negative reviews convert quickly into lost deals, while Kaufman & Broads stronger brand lowers return risk and lifts willingness to pay. Proactive customer care and digital handover tools (e-delivery, defect tracking) dilute buyer leverage.

- Snag rates & delivery punctuality drive concessions

- Negative reviews → faster deal losses

- Strong brand reduces returns, raises price tolerance

- Digital handover + proactive care weakens buyer power

Policy-driven expectations

Tax-incentivized affordability and energy-efficiency programs in 2024 have anchored buyer expectations on lower prices and higher performance; when incentives tighten, buyers amplify demands for upfront value and efficiency. Builders face rising compliance costs that cannot always be fully passed to buyers, making lifetime-cost messaging (energy savings, maintenance) vital to defend pricing.

- Policy sensitivity: buyers calibrate willingness-to-pay to incentive levels

- Cost pressure: compliance often compresses margins

- Defense: quantified lifetime savings strengthen price resilience

Tighter affordability: 3.2% rates and 30% institutional buying compress prices

Buyers’ affordability tightened as average new housing loan rates ≈3.2% in 2024, increasing discount pressure and demand for staged payments. Institutional bulk buyers (~30% of deliveries 2024) exert volume-driven price/spec leverage. High comparability and online search (~80% of buyers) intensify price competition; snag/delivery issues drove concessions in ~70% of cases. Strong brand and digital aftercare reduce buyer power.

| Metric | 2024 value |

|---|---|

| Avg mortgage rate | ≈3.2% |

| Institutional share | ~30% |

| Online search | ~80% |

| Concession driver (snags) | ~70% |

Full Version Awaits

Kaufman & Broad Porter's Five Forces Analysis

This preview shows the exact Kaufman & Broad Porter’s Five Forces analysis you’ll receive after purchase—no placeholders. It presents the full, professionally formatted assessment of competitive rivalry, supplier and buyer power, and the threats of new entrants and substitutes. You’ll get this identical file instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Kaufman & Broad faces moderate buyer power, concentrated suppliers in construction inputs, and steady threats from new entrants and substitutes as urban housing evolves. This snapshot highlights strategic pressure points and competitive levers. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Kaufman & Broad’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated materials suppliers

Core inputs like cement, steel, glass and insulation come from a concentrated EU supplier base, giving suppliers pricing leverage and making materials roughly 40% of build costs in France (2024). Energy-linked input swings have driven volatility — material price indices moved about 15% between 2022–2024, often passed to developers. Kaufman & Broad mitigates via framework contracts and vendor diversification, but technical standards and sudden spikes still compress margins.

Scarce specialized subcontractors

MEP, façade and finishing subcontractors are capacity-constrained in busy regions; in 2024 subcontractor bid premiums rose roughly 5–8% and average MEP lead times lengthened by about 4–6 weeks, enabling specialists to cherry-pick higher-margin work or demand tougher payment and warranty terms. This elevates execution risk and scheduling/holding costs for large residential programs. Preferred-partner agreements and steady volumes can temper their pricing power.

Landowners and municipalities

Buildable land is the scarcest supplier, with landowners and municipalities controlling zoning, permits and often extracting premiums; in tight urban markets land can represent 30–50% of total development cost. Competitive tenders for prime plots routinely push prices up and attach design or affordability obligations, increasing acquisition bids by double-digit percentages. Municipal gatekeeping typically lengthens timelines by 6–18 months and raises soft costs (planning, studies, levies) by 5–15%. Early-stage land assembly and strong urban relationships are therefore critical to rebalance supplier power and secure project viability.

Labor costs and regulation

- Wage inflation: ~6% (2024)

- Collective coverage: ~70%

- Safety/training add to baseline costs

- Mitigation: planning, productivity tech

ESG and imported components

ESG-driven demand for low-carbon materials, certified timber and traceable fixtures in 2024 narrows Kaufman & Broad’s supplier pool, raising supplier leverage as import-dependent items face FX swings (≈8–12% intrayear in 2023–24) and logistics cost volatility; institutional sales with ESG clauses (≈60% of large French contracts in 2024) reinforce strict sourcing and pricing power.

- Certified timber limits suppliers

- Imports exposed to FX/logistics

- Institutional ESG boosts supplier leverage

- Dual-sourcing & design-to-value reduce exposure

Suppliers' leverage: materials ≈40%, indices ≈15%, ESG ≈60%

Suppliers hold strong leverage: core materials ≈40% of build cost (France, 2024) with material indices swinging ≈15% (2022–24), subcontractor premiums up 5–8% and MEP lead times +4–6 weeks, land 30–50% of project cost, labor unit costs +6% (2024) with ~70% collective coverage; institutional ESG clauses ≈60% of large contracts heighten certified-supply constraints.

| Metric | 2024 value |

|---|---|

| Materials % of build | ≈40% |

| Material index swing (2022–24) | ≈15% |

| Subcontractor premium | 5–8% |

| Land % of cost | 30–50% |

| Labor inflation | ≈6% |

| Collective coverage | ≈70% |

| Institutional ESG share | ≈60% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Kaufman & Broad, with detailed evaluation of suppliers, buyers, substitutes, and industry rivalry to inform strategic positioning and investment decisions.

A one-sheet Porter’s Five Forces for Kaufman & Broad that maps competitive pressures, lets you tweak inputs for scenario testing, and exports clean visuals for decks—no macros required.

Customers Bargaining Power

Mortgage-rate sensitivity

Individual buyers’ affordability hinges on French mortgage rates and credit criteria; Banque de France data showed average new housing loan rates near 3.2% in 2024, tightening borrower capacity. When rates rise buyers increasingly demand discounts, upgrades or staged payment plans, boosting their bargaining power and slowing sales velocity. Flexible pricing and phased payments help preserve absorption by aligning cashflows with tighter borrower budgets.

Institutional bulk buyers

Institutional bulk buyers such as funds and social landlords purchase blocks at scale from Kaufman & Broad, leveraging volume to negotiate discounts and specific build specs. Their repeat business anchored ~30% of deliveries in 2024, stabilizing volumes but compressing margins. These buyers impose ESG and delivery KPIs with penalty regimes, so a balanced mix between retail and institutional sales protects pricing and margin volatility.

High comparability across developers

Residential offers from Kaufman & Broad are highly comparable on location, layout and energy performance, so buyers can benchmark easily against other French developers and local players; RE2020 has applied since 2022, making energy labels a standard comparison point. Over 80% of French buyers search listings online (SeLoger/IFOP trends 2024), amplifying price pressure. Differentiation via design, amenities and superior RE2020 performance reduces pure price-only competition.

Quality, warranty, and reputation

Buyers press on snag rates, delivery punctuality and after-sales service; in 2024 surveys roughly 70% of homebuyers said visible defects or delays prompted price concessions or cancellation. Negative reviews convert quickly into lost deals, while Kaufman & Broads stronger brand lowers return risk and lifts willingness to pay. Proactive customer care and digital handover tools (e-delivery, defect tracking) dilute buyer leverage.

- Snag rates & delivery punctuality drive concessions

- Negative reviews → faster deal losses

- Strong brand reduces returns, raises price tolerance

- Digital handover + proactive care weakens buyer power

Policy-driven expectations

Tax-incentivized affordability and energy-efficiency programs in 2024 have anchored buyer expectations on lower prices and higher performance; when incentives tighten, buyers amplify demands for upfront value and efficiency. Builders face rising compliance costs that cannot always be fully passed to buyers, making lifetime-cost messaging (energy savings, maintenance) vital to defend pricing.

- Policy sensitivity: buyers calibrate willingness-to-pay to incentive levels

- Cost pressure: compliance often compresses margins

- Defense: quantified lifetime savings strengthen price resilience

Tighter affordability: 3.2% rates and 30% institutional buying compress prices

Buyers’ affordability tightened as average new housing loan rates ≈3.2% in 2024, increasing discount pressure and demand for staged payments. Institutional bulk buyers (~30% of deliveries 2024) exert volume-driven price/spec leverage. High comparability and online search (~80% of buyers) intensify price competition; snag/delivery issues drove concessions in ~70% of cases. Strong brand and digital aftercare reduce buyer power.

| Metric | 2024 value |

|---|---|

| Avg mortgage rate | ≈3.2% |

| Institutional share | ~30% |

| Online search | ~80% |

| Concession driver (snags) | ~70% |

Full Version Awaits

Kaufman & Broad Porter's Five Forces Analysis

This preview shows the exact Kaufman & Broad Porter’s Five Forces analysis you’ll receive after purchase—no placeholders. It presents the full, professionally formatted assessment of competitive rivalry, supplier and buyer power, and the threats of new entrants and substitutes. You’ll get this identical file instantly upon payment.