KB Financial Group Business Model Canvas

Unlock the strategic playbook with our Business Model Canvas—download editable Word & Excel

Unlock KB Financial Group’s strategic playbook with our full Business Model Canvas—three sentences won’t cover it, but this preview shows how value propositions, channels, and revenue streams align to drive growth. Download the complete, editable Word & Excel files to benchmark, strategize, and act with confidence today.

Partnerships

Regulators and industry bodies

Partnership with the Bank of Korea (established 1950), the Financial Services Commission (established 1998) and the Financial Supervisory Service (established 1999) ensures compliance, stability and direct access to monetary and policy guidance. Proactive engagement enables faster approvals and product rollouts and participation in industry associations helps shape standards and risk practices. These ties strengthen trust and operational resilience.

Global banks and correspondent networks

Alliances with international banks and correspondent networks enable KB Financial Group to support cross-border payments, trade finance, and FX for Korean corporates and expatriates, extending reach into key markets through shared platforms that reduce settlement risk and operational costs. These partnerships improve transaction speed and service reliability for international clients, enhancing liquidity management and global trade support.

Fintechs, payment networks, and Open Banking partners

Collaboration with fintechs accelerates KB Financials digital onboarding and UX, helping grow mobile active users to about 18 million in 2024 and reducing onboarding time by roughly 60%. Card schemes and payment rails expand acceptance and merchant solutions, with card payments comprising around 63% of South Korea retail transactions in 2024. Open Banking APIs enable embedded finance with ecosystem players, increasing API-driven revenue streams and partnerships. These alliances drive innovation and customer acquisition at scale.

Technology, cloud, and cybersecurity vendors

Strategic vendors supply KB Financial Group with core banking platforms, cloud infrastructure, and AI toolchains that enable faster product rollout and operational scale; co-development agreements have shortened feature release cycles and improved performance. Cybersecurity partners provide advanced threat detection, incident response, and regulatory-grade controls that underpin resilience and compliance. This integrated tech stack supports scalable growth and audit-ready security.

- core-banking vendors

- cloud-infrastructure

- AI-toolchains

- cyber-threat-detection

- co-development

- regulatory-security

Insurance, asset managers, and distribution alliances

Ties with insurers and KB’s asset management arms enable bancassurance and packaged investment products, expanding lifetime client penetration and fee-based revenue streams. External distributors and brokers widen market access beyond branch networks, increasing reach in wealth and retail segments. Co-branded solutions improve wallet share across life-cycle needs, supporting cross-sell and diversification of fee income.

- Partnerships: bancassurance, asset management

- Distribution: external brokers, third-party channels

- Benefits: higher cross-sell, diversified fees

Regulatory ties + fintech alliances drove 18M users, -60% onboarding, 63% card share

Regulatory partnerships (Bank of Korea, FSC, FSS) ensure compliance and fast product approvals. Fintech alliances drove mobile active users to about 18 million in 2024 and cut onboarding time ~60%. Card & payments integration supports a retail card share ~63% in 2024 while bancassurance and AM ties boost fee income and cross‑sell.

| Metric | Value (2024) |

|---|---|

| Mobile active users | ~18,000,000 |

| Onboarding time | -60% |

| Retail card share | ~63% |

What is included in the product

A comprehensive Business Model Canvas tailored to KB Financial Group, covering customer segments, channels, value propositions and revenue streams across the 9 classic BMC blocks. Includes competitive advantages, SWOT-linked insights and polished narratives—ideal for investor presentations, strategic planning and validation using real-world bank data.

Condenses KB Financial Group’s strategy into a single, editable canvas that quickly identifies core components and pain points for faster decision-making. Shareable and boardroom-ready, it saves hours of structuring and is ideal for team collaboration, comparisons, or executive summaries.

Activities

Retail and corporate lending

Origination and servicing of mortgages, consumer, SME and corporate loans drive KB Financial Group’s core growth, with tailored secured and unsecured products by segment. Rigorous credit assessment, risk-based pricing and active portfolio monitoring balance risk-return and reduce NPL exposure. Continuous repricing and product resets align loan yields with interest rate cycles to protect net interest margin.

Deposit gathering and payments

Attracting low-cost deposits anchors KB Financial Group’s funding stability, with customer deposits reported at about KRW 400 trillion in 2024, keeping loan-to-deposit ratios conservative. Current, savings, and time deposits are actively optimized for mix and duration to manage interest margin and liquidity. Payment processing covers cards, wires, instant transfers and mobile wallets, supporting high transaction volumes. Cash management services sustain SMEs and large corporates’ daily operations.

Wealth, asset management, and insurance

Advisory, brokerage, funds and discretionary mandates cover retail through HNW clients, with KB Financial Group managing diverse AUM across segments (total group assets ~KRW 470 trillion in 2024). Bancassurance and protection products address client risk needs, while portfolio construction blends in-house and third-party solutions; ongoing reviews realign investments to client goals and market shifts.

Risk, compliance, and capital management

Credit, market, liquidity, and operational risk frameworks protect KB Financial Group’s balance sheet through standardized limits, scenario-based monitoring, and recovery plans aligned with 2024 regulatory expectations. AML, KYC, and data privacy controls are embedded across onboarding and transaction monitoring to ensure compliance with Korean and global rules. ICAAP and stress testing drive capital optimization and buffer sizing under adverse scenarios, while analytics refine limits, provisioning, and concentration controls in real time.

- Risk frameworks: credit, market, liquidity, operational

- Compliance controls: AML, KYC, data privacy

- Capital tools: ICAAP, stress testing

- Analytics: limits, provisioning, concentration

Digital transformation and customer experience

KB accelerates product digitization and mobile-first journeys, using automation to cut processing times and boost efficiency; South Korea smartphone penetration reached about 96% in 2024.

Data-driven personalization raises engagement and retention through analytics and real-time signals; open APIs expand distribution via partner ecosystems while continuous UX testing shortens cycles and increases adoption.

- Product digitization: faster launches

- Mobile-first: 96% market reach

- Automation: lower unit costs

- APIs: ecosystem distribution

- UX testing: higher adoption

Lending-led growth with KRW 400T deposits, KRW 470T assets and 96% mobile reach

Origination and servicing of mortgages, consumer, SME and corporate loans drive core growth with risk-based pricing and active monitoring. Low-cost deposits (~KRW 400 trillion in 2024) and diversified payment/cash-management services secure funding and liquidity. Wealth, advisory and bancassurance leverage group scale (total assets ~KRW 470 trillion in 2024) and 96% smartphone penetration to digitize distribution.

| Metric | 2024 |

|---|---|

| Customer deposits | KRW 400 trillion |

| Total group assets | KRW 470 trillion |

| Smartphone penetration (KR) | 96% |

What You See Is What You Get

Business Model Canvas

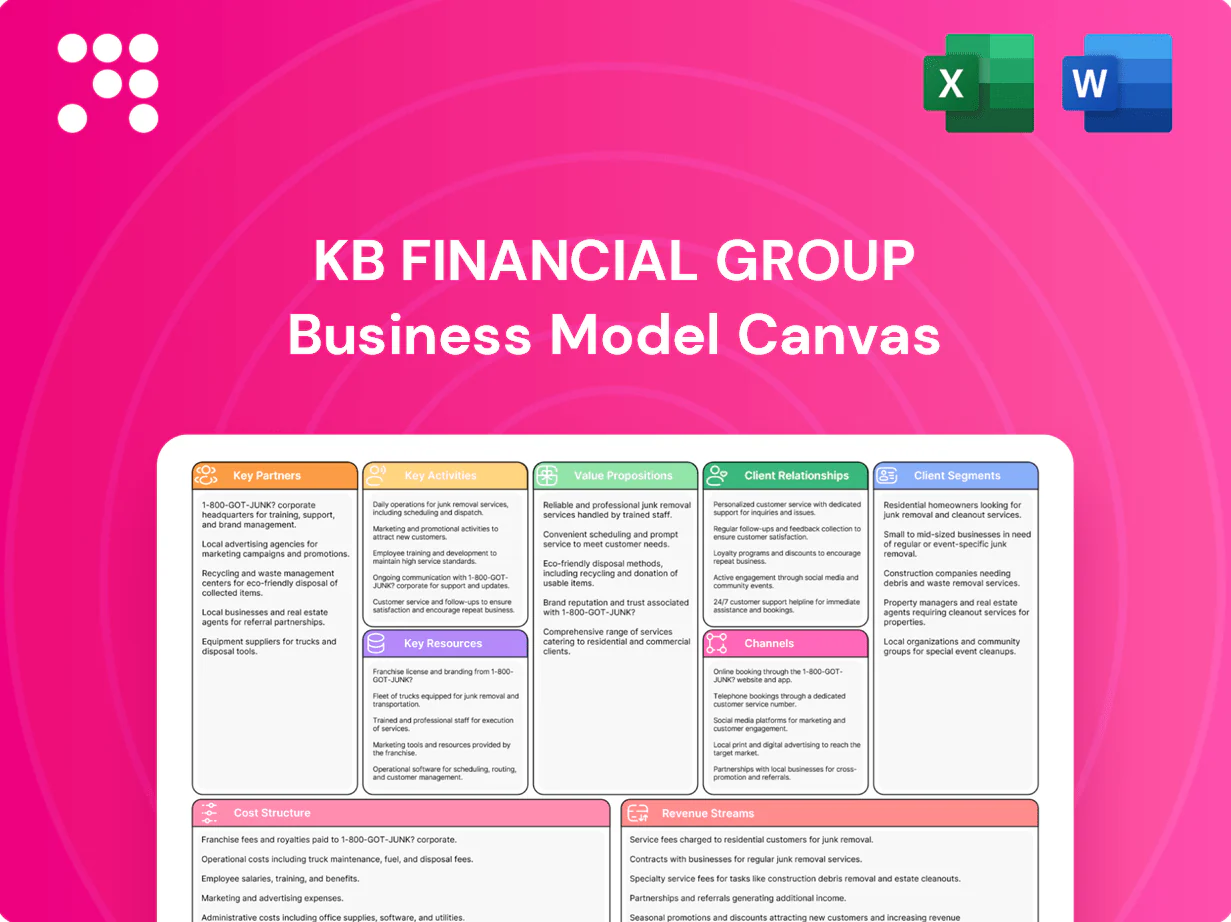

The KB Financial Group Business Model Canvas shown here is the actual deliverable, not a mockup or sample. When you purchase, you’ll receive this same document in full, formatted and ready to edit in Word and Excel. The preview reflects the complete structure, content, and layout you’ll download—no hidden pages or placeholders. Buy with confidence: what you see is exactly what you’ll get.

Unlock the strategic playbook with our Business Model Canvas—download editable Word & Excel

Unlock KB Financial Group’s strategic playbook with our full Business Model Canvas—three sentences won’t cover it, but this preview shows how value propositions, channels, and revenue streams align to drive growth. Download the complete, editable Word & Excel files to benchmark, strategize, and act with confidence today.

Partnerships

Regulators and industry bodies

Partnership with the Bank of Korea (established 1950), the Financial Services Commission (established 1998) and the Financial Supervisory Service (established 1999) ensures compliance, stability and direct access to monetary and policy guidance. Proactive engagement enables faster approvals and product rollouts and participation in industry associations helps shape standards and risk practices. These ties strengthen trust and operational resilience.

Global banks and correspondent networks

Alliances with international banks and correspondent networks enable KB Financial Group to support cross-border payments, trade finance, and FX for Korean corporates and expatriates, extending reach into key markets through shared platforms that reduce settlement risk and operational costs. These partnerships improve transaction speed and service reliability for international clients, enhancing liquidity management and global trade support.

Fintechs, payment networks, and Open Banking partners

Collaboration with fintechs accelerates KB Financials digital onboarding and UX, helping grow mobile active users to about 18 million in 2024 and reducing onboarding time by roughly 60%. Card schemes and payment rails expand acceptance and merchant solutions, with card payments comprising around 63% of South Korea retail transactions in 2024. Open Banking APIs enable embedded finance with ecosystem players, increasing API-driven revenue streams and partnerships. These alliances drive innovation and customer acquisition at scale.

Technology, cloud, and cybersecurity vendors

Strategic vendors supply KB Financial Group with core banking platforms, cloud infrastructure, and AI toolchains that enable faster product rollout and operational scale; co-development agreements have shortened feature release cycles and improved performance. Cybersecurity partners provide advanced threat detection, incident response, and regulatory-grade controls that underpin resilience and compliance. This integrated tech stack supports scalable growth and audit-ready security.

- core-banking vendors

- cloud-infrastructure

- AI-toolchains

- cyber-threat-detection

- co-development

- regulatory-security

Insurance, asset managers, and distribution alliances

Ties with insurers and KB’s asset management arms enable bancassurance and packaged investment products, expanding lifetime client penetration and fee-based revenue streams. External distributors and brokers widen market access beyond branch networks, increasing reach in wealth and retail segments. Co-branded solutions improve wallet share across life-cycle needs, supporting cross-sell and diversification of fee income.

- Partnerships: bancassurance, asset management

- Distribution: external brokers, third-party channels

- Benefits: higher cross-sell, diversified fees

Regulatory ties + fintech alliances drove 18M users, -60% onboarding, 63% card share

Regulatory partnerships (Bank of Korea, FSC, FSS) ensure compliance and fast product approvals. Fintech alliances drove mobile active users to about 18 million in 2024 and cut onboarding time ~60%. Card & payments integration supports a retail card share ~63% in 2024 while bancassurance and AM ties boost fee income and cross‑sell.

| Metric | Value (2024) |

|---|---|

| Mobile active users | ~18,000,000 |

| Onboarding time | -60% |

| Retail card share | ~63% |

What is included in the product

A comprehensive Business Model Canvas tailored to KB Financial Group, covering customer segments, channels, value propositions and revenue streams across the 9 classic BMC blocks. Includes competitive advantages, SWOT-linked insights and polished narratives—ideal for investor presentations, strategic planning and validation using real-world bank data.

Condenses KB Financial Group’s strategy into a single, editable canvas that quickly identifies core components and pain points for faster decision-making. Shareable and boardroom-ready, it saves hours of structuring and is ideal for team collaboration, comparisons, or executive summaries.

Activities

Retail and corporate lending

Origination and servicing of mortgages, consumer, SME and corporate loans drive KB Financial Group’s core growth, with tailored secured and unsecured products by segment. Rigorous credit assessment, risk-based pricing and active portfolio monitoring balance risk-return and reduce NPL exposure. Continuous repricing and product resets align loan yields with interest rate cycles to protect net interest margin.

Deposit gathering and payments

Attracting low-cost deposits anchors KB Financial Group’s funding stability, with customer deposits reported at about KRW 400 trillion in 2024, keeping loan-to-deposit ratios conservative. Current, savings, and time deposits are actively optimized for mix and duration to manage interest margin and liquidity. Payment processing covers cards, wires, instant transfers and mobile wallets, supporting high transaction volumes. Cash management services sustain SMEs and large corporates’ daily operations.

Wealth, asset management, and insurance

Advisory, brokerage, funds and discretionary mandates cover retail through HNW clients, with KB Financial Group managing diverse AUM across segments (total group assets ~KRW 470 trillion in 2024). Bancassurance and protection products address client risk needs, while portfolio construction blends in-house and third-party solutions; ongoing reviews realign investments to client goals and market shifts.

Risk, compliance, and capital management

Credit, market, liquidity, and operational risk frameworks protect KB Financial Group’s balance sheet through standardized limits, scenario-based monitoring, and recovery plans aligned with 2024 regulatory expectations. AML, KYC, and data privacy controls are embedded across onboarding and transaction monitoring to ensure compliance with Korean and global rules. ICAAP and stress testing drive capital optimization and buffer sizing under adverse scenarios, while analytics refine limits, provisioning, and concentration controls in real time.

- Risk frameworks: credit, market, liquidity, operational

- Compliance controls: AML, KYC, data privacy

- Capital tools: ICAAP, stress testing

- Analytics: limits, provisioning, concentration

Digital transformation and customer experience

KB accelerates product digitization and mobile-first journeys, using automation to cut processing times and boost efficiency; South Korea smartphone penetration reached about 96% in 2024.

Data-driven personalization raises engagement and retention through analytics and real-time signals; open APIs expand distribution via partner ecosystems while continuous UX testing shortens cycles and increases adoption.

- Product digitization: faster launches

- Mobile-first: 96% market reach

- Automation: lower unit costs

- APIs: ecosystem distribution

- UX testing: higher adoption

Lending-led growth with KRW 400T deposits, KRW 470T assets and 96% mobile reach

Origination and servicing of mortgages, consumer, SME and corporate loans drive core growth with risk-based pricing and active monitoring. Low-cost deposits (~KRW 400 trillion in 2024) and diversified payment/cash-management services secure funding and liquidity. Wealth, advisory and bancassurance leverage group scale (total assets ~KRW 470 trillion in 2024) and 96% smartphone penetration to digitize distribution.

| Metric | 2024 |

|---|---|

| Customer deposits | KRW 400 trillion |

| Total group assets | KRW 470 trillion |

| Smartphone penetration (KR) | 96% |

What You See Is What You Get

Business Model Canvas

The KB Financial Group Business Model Canvas shown here is the actual deliverable, not a mockup or sample. When you purchase, you’ll receive this same document in full, formatted and ready to edit in Word and Excel. The preview reflects the complete structure, content, and layout you’ll download—no hidden pages or placeholders. Buy with confidence: what you see is exactly what you’ll get.

Original: $10.00

-65%$10.00

$3.50Description

Unlock the strategic playbook with our Business Model Canvas—download editable Word & Excel

Unlock KB Financial Group’s strategic playbook with our full Business Model Canvas—three sentences won’t cover it, but this preview shows how value propositions, channels, and revenue streams align to drive growth. Download the complete, editable Word & Excel files to benchmark, strategize, and act with confidence today.

Partnerships

Regulators and industry bodies

Partnership with the Bank of Korea (established 1950), the Financial Services Commission (established 1998) and the Financial Supervisory Service (established 1999) ensures compliance, stability and direct access to monetary and policy guidance. Proactive engagement enables faster approvals and product rollouts and participation in industry associations helps shape standards and risk practices. These ties strengthen trust and operational resilience.

Global banks and correspondent networks

Alliances with international banks and correspondent networks enable KB Financial Group to support cross-border payments, trade finance, and FX for Korean corporates and expatriates, extending reach into key markets through shared platforms that reduce settlement risk and operational costs. These partnerships improve transaction speed and service reliability for international clients, enhancing liquidity management and global trade support.

Fintechs, payment networks, and Open Banking partners

Collaboration with fintechs accelerates KB Financials digital onboarding and UX, helping grow mobile active users to about 18 million in 2024 and reducing onboarding time by roughly 60%. Card schemes and payment rails expand acceptance and merchant solutions, with card payments comprising around 63% of South Korea retail transactions in 2024. Open Banking APIs enable embedded finance with ecosystem players, increasing API-driven revenue streams and partnerships. These alliances drive innovation and customer acquisition at scale.

Technology, cloud, and cybersecurity vendors

Strategic vendors supply KB Financial Group with core banking platforms, cloud infrastructure, and AI toolchains that enable faster product rollout and operational scale; co-development agreements have shortened feature release cycles and improved performance. Cybersecurity partners provide advanced threat detection, incident response, and regulatory-grade controls that underpin resilience and compliance. This integrated tech stack supports scalable growth and audit-ready security.

- core-banking vendors

- cloud-infrastructure

- AI-toolchains

- cyber-threat-detection

- co-development

- regulatory-security

Insurance, asset managers, and distribution alliances

Ties with insurers and KB’s asset management arms enable bancassurance and packaged investment products, expanding lifetime client penetration and fee-based revenue streams. External distributors and brokers widen market access beyond branch networks, increasing reach in wealth and retail segments. Co-branded solutions improve wallet share across life-cycle needs, supporting cross-sell and diversification of fee income.

- Partnerships: bancassurance, asset management

- Distribution: external brokers, third-party channels

- Benefits: higher cross-sell, diversified fees

Regulatory ties + fintech alliances drove 18M users, -60% onboarding, 63% card share

Regulatory partnerships (Bank of Korea, FSC, FSS) ensure compliance and fast product approvals. Fintech alliances drove mobile active users to about 18 million in 2024 and cut onboarding time ~60%. Card & payments integration supports a retail card share ~63% in 2024 while bancassurance and AM ties boost fee income and cross‑sell.

| Metric | Value (2024) |

|---|---|

| Mobile active users | ~18,000,000 |

| Onboarding time | -60% |

| Retail card share | ~63% |

What is included in the product

A comprehensive Business Model Canvas tailored to KB Financial Group, covering customer segments, channels, value propositions and revenue streams across the 9 classic BMC blocks. Includes competitive advantages, SWOT-linked insights and polished narratives—ideal for investor presentations, strategic planning and validation using real-world bank data.

Condenses KB Financial Group’s strategy into a single, editable canvas that quickly identifies core components and pain points for faster decision-making. Shareable and boardroom-ready, it saves hours of structuring and is ideal for team collaboration, comparisons, or executive summaries.

Activities

Retail and corporate lending

Origination and servicing of mortgages, consumer, SME and corporate loans drive KB Financial Group’s core growth, with tailored secured and unsecured products by segment. Rigorous credit assessment, risk-based pricing and active portfolio monitoring balance risk-return and reduce NPL exposure. Continuous repricing and product resets align loan yields with interest rate cycles to protect net interest margin.

Deposit gathering and payments

Attracting low-cost deposits anchors KB Financial Group’s funding stability, with customer deposits reported at about KRW 400 trillion in 2024, keeping loan-to-deposit ratios conservative. Current, savings, and time deposits are actively optimized for mix and duration to manage interest margin and liquidity. Payment processing covers cards, wires, instant transfers and mobile wallets, supporting high transaction volumes. Cash management services sustain SMEs and large corporates’ daily operations.

Wealth, asset management, and insurance

Advisory, brokerage, funds and discretionary mandates cover retail through HNW clients, with KB Financial Group managing diverse AUM across segments (total group assets ~KRW 470 trillion in 2024). Bancassurance and protection products address client risk needs, while portfolio construction blends in-house and third-party solutions; ongoing reviews realign investments to client goals and market shifts.

Risk, compliance, and capital management

Credit, market, liquidity, and operational risk frameworks protect KB Financial Group’s balance sheet through standardized limits, scenario-based monitoring, and recovery plans aligned with 2024 regulatory expectations. AML, KYC, and data privacy controls are embedded across onboarding and transaction monitoring to ensure compliance with Korean and global rules. ICAAP and stress testing drive capital optimization and buffer sizing under adverse scenarios, while analytics refine limits, provisioning, and concentration controls in real time.

- Risk frameworks: credit, market, liquidity, operational

- Compliance controls: AML, KYC, data privacy

- Capital tools: ICAAP, stress testing

- Analytics: limits, provisioning, concentration

Digital transformation and customer experience

KB accelerates product digitization and mobile-first journeys, using automation to cut processing times and boost efficiency; South Korea smartphone penetration reached about 96% in 2024.

Data-driven personalization raises engagement and retention through analytics and real-time signals; open APIs expand distribution via partner ecosystems while continuous UX testing shortens cycles and increases adoption.

- Product digitization: faster launches

- Mobile-first: 96% market reach

- Automation: lower unit costs

- APIs: ecosystem distribution

- UX testing: higher adoption

Lending-led growth with KRW 400T deposits, KRW 470T assets and 96% mobile reach

Origination and servicing of mortgages, consumer, SME and corporate loans drive core growth with risk-based pricing and active monitoring. Low-cost deposits (~KRW 400 trillion in 2024) and diversified payment/cash-management services secure funding and liquidity. Wealth, advisory and bancassurance leverage group scale (total assets ~KRW 470 trillion in 2024) and 96% smartphone penetration to digitize distribution.

| Metric | 2024 |

|---|---|

| Customer deposits | KRW 400 trillion |

| Total group assets | KRW 470 trillion |

| Smartphone penetration (KR) | 96% |

What You See Is What You Get

Business Model Canvas

The KB Financial Group Business Model Canvas shown here is the actual deliverable, not a mockup or sample. When you purchase, you’ll receive this same document in full, formatted and ready to edit in Word and Excel. The preview reflects the complete structure, content, and layout you’ll download—no hidden pages or placeholders. Buy with confidence: what you see is exactly what you’ll get.