Keller Group PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock strategic clarity with our targeted PESTLE Analysis of Keller Group—examining political, economic, social, technological, legal, and environmental forces shaping its outlook. This concise briefing reveals risks and growth levers you can act on today. Ideal for investors and strategists, it’s ready to deploy in boardrooms and models. Purchase the full report to access the complete, editable analysis instantly.

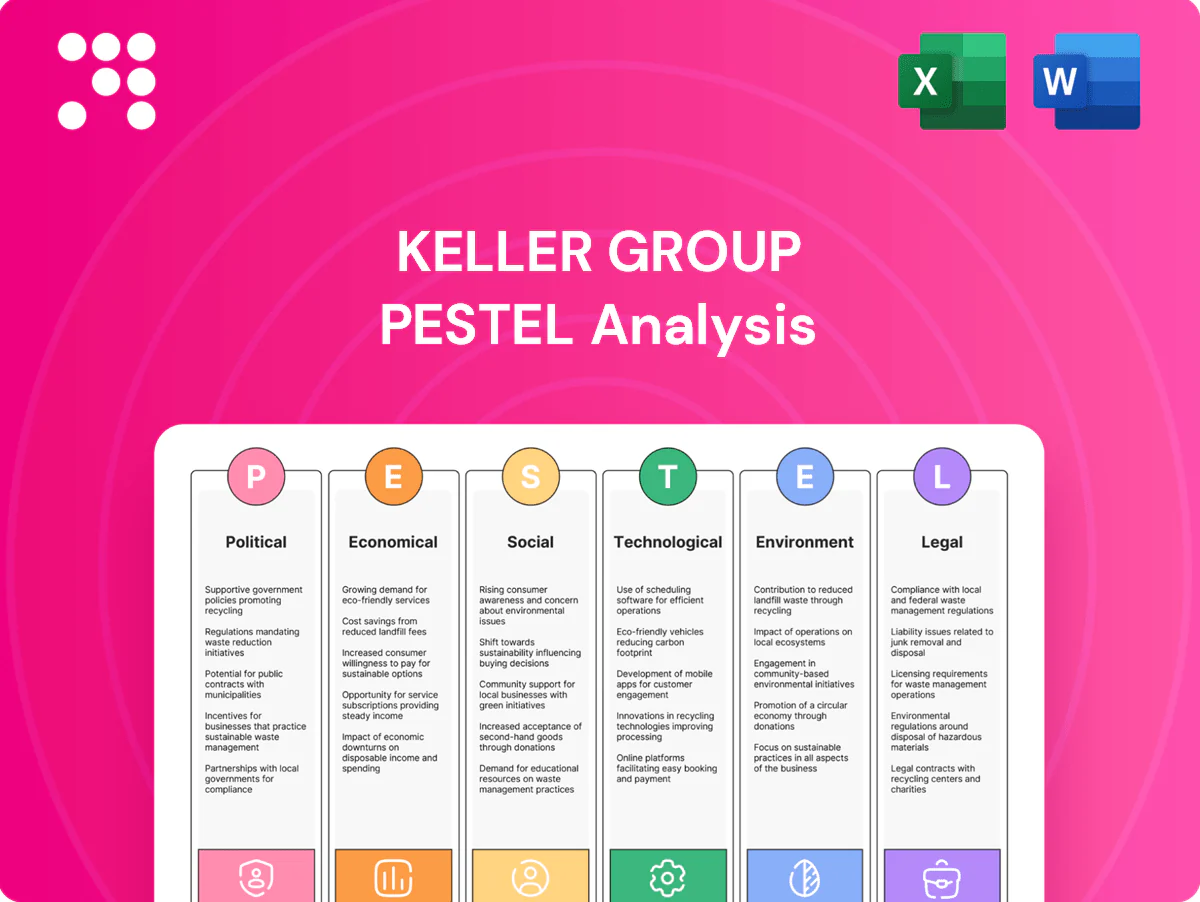

Political factors

Public infrastructure spending priorities

Government budgets and stimulus — notably the US Infrastructure Investment and Jobs Act worth roughly $1.2 trillion and Global Infrastructure Hub estimates of about $94 trillion needed in global infrastructure investment to 2040 — drive demand for transportation, energy, water and flood‑defence projects that are intensive in geotechnical work. Shifts after elections can reallocate capital away from or toward these programmes, creating pipeline volatility despite Keller benefiting from multi‑year contracts. Active geographic diversification helps buffer policy swings and smooth revenue exposure.

Permitting and planning regimes

Complex multilayer approvals in many jurisdictions mean start dates and scope for ground works often slip; in England major planning applications have a statutory 13-week decision target but frequently need longer. Stricter impact assessments and stakeholder consultations can add months to mobilization. Early regulatory engagement de-risks schedules and local expertise is crucial to navigate municipal and national rules.

Geopolitical risk and market access

Sanctions, trade restrictions and regional instability can halt Keller projects and disrupt supply chains, causing delays in materials and specialist plant movement across borders.

Cross-border equipment transfers often encounter customs clearance and visa hurdles for technical crews, increasing mobilisation times and costs.

Balancing a portfolio between OECD and emerging markets, alongside political risk insurance and flexible contracting, helps preserve margins and limit concentrated exposure.

Local content and procurement policies

Governments increasingly mandate domestic sourcing, joint ventures or workforce quotas—in some jurisdictions local content rules demand up to 60% local procurement—forcing Keller to adapt bid structures and delivery models; compliance affects competitiveness while non-compliance risks disqualification or fines. Building local partnerships and training programs strengthens Keller’s licence to operate and long‑term margins.

- Domestic sourcing: up to 60% local content

- Impacts: bid competitiveness, delivery models

- Mitigation: local JV, training programs, partnerships

- Risk: disqualification, financial penalties

Public–private partnership frameworks

PPP structures unlock large, complex geotechnical contracts, directing major civil programmes to specialists and shaping project pipelines for firms like Keller, which operates in 40+ countries with ~11,000 staff (2024).

Risk allocation and payment mechanisms determine cash flow and returns; transparent procurement boosts bid confidence while weak frameworks increase counterparty risk; strong balance sheets support bonding and guarantees.

- PPP access: large technical jobs

- Payments: drive cashflow/returns

- Procurement: transparency = lower risk

- Balance sheet: enables bonds/guarantees

Political shifts and local content rules reshape geotechnical project risk and mobilization

Political shifts (eg US IIJA ~$1.2T, Global Infrastructure Hub $94T to 2040) drive geotechnical demand; election changes create pipeline volatility despite multi‑year contracts. Permitting, sanctions and local content rules (up to 60% local procurement) raise mobilisation costs and compliance risk. Diversification, local JVs and political risk insurance mitigate exposure; Keller: 40+ countries, ~11,000 staff (2024).

| Factor | Metric | Impact | Mitigation |

|---|---|---|---|

| Infrastructure spend | $1.2T (IIJA); $94T to 2040 | Pipeline growth/volatility | Geographic diversification |

| Local content | Up to 60% | Higher costs/qualification risk | Local JV, training |

What is included in the product

Explores how macro-environmental forces uniquely affect the Keller Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, industry-specific examples and forward-looking insights to inform strategic planning, risk mitigation and investor communications.

A concise, visually segmented Keller Group PESTLE summary that simplifies external risk assessment for meetings, is easily editable with region- or line-specific notes, and can be dropped into presentations or shared across teams to speed strategic alignment.

Economic factors

Cyclical construction demand

Cyclical construction demand drives Keller's order intake, with macro growth and housing cycles plus large infrastructure pipelines underpinning wins; the group reported continued healthy activity through 2024 with backlog staying above £1bn mid‑2024. Recessions trim private housing and commercial development, though public works and infrastructure spending have historically partially offset downturns. A diversified sector mix across transport, energy and industrial projects smooths exposure, while backlog quality remains critical to utilization rates and pricing power.

Interest rates and project financing

Higher borrowing costs — Bank of England base rate at 5.25% and 10-year gilt yields near 4.5% in mid‑2025 — lift developer WACC and defer commercial starts, squeezing public issuers' debt capacity. Keller faces higher working‑capital needs and elevated bonding costs that compress margins, though targeted hedging and milestone billing are used to stabilize liquidity and reduce funding spikes.

Input costs and supply chain inflation

Rising input costs—steel averaging about $700/tonne in 2024, cement near £80/tonne and diesel around $1.10/litre—directly inflate Keller job costing and compress margins. Volatile logistics and lead times, with container freight still ~50% below 2021 peaks but spiking intermittently, disrupt scheduling. Use of escalation clauses and forward procurement has preserved margins on major projects. Standardization and long-term supplier agreements boost resilience and lower bid volatility.

Labor availability and wage pressures

Skilled geotechnical crews and engineers remain scarce across key markets, and Keller employed around 11,000 people in 2023–24, concentrating talent in specialist regions.

Wage inflation and rising training costs—industry wage growth near 6% in recent years—can compress margins, though productivity tools and method optimisation improve output per worker and offset some expenses.

Apprenticeships and retention programmes have been expanded to stabilise capability and reduce turnover-related hiring costs.

- Scarcity: specialised crews concentrated regionally

- Workforce: ~11,000 employees (2023–24)

- Wage pressure: ~6% industry wage growth recently

- Mitigation: productivity tools, apprenticeships, retention

Currency fluctuations in global operations

Currency fluctuations across Keller Groups global operations create FX translation and transaction risk as revenues, costs and bids are denominated in multiple currencies; bids fixed in one currency while inputs are paid in another can quickly erode margins. Keller mitigates volatility through natural hedging by aligning regional cost bases to local revenues and selective use of derivatives and forward contracts disclosed in its 2024 annual report. Ongoing monitoring of currency exposures remains central to bid pricing and working capital.

- Multi-currency revenues/costs = translation & transaction risk

- Bids fixed in one currency while inputs in another can erode margin

- Natural hedging + derivatives (forwards) reduce volatility

- Align regional cost bases to revenues to improve protection

Political shifts and local content rules reshape geotechnical project risk and mobilization

Cyclical construction demand drives Keller's order intake; backlog stayed above £1bn mid‑2024 and public infrastructure partly offsets downturns. Higher borrowing costs (BoE 5.25% mid‑2025, 10y gilt ~4.5%) and rising inputs (steel ~$700/t, cement ~£80/t, diesel ~£1.10/l) squeeze margins; mitigation includes escalation clauses, hedging and long‑term supply deals. Workforce ~11,000 with ~6% wage pressure.

| Metric | Value |

|---|---|

| Backlog (mid‑2024) | £>1bn |

| Employees (2023–24) | ~11,000 |

| BoE base rate (mid‑2025) | 5.25% |

| 10y gilt | ~4.5% |

| Steel (2024) | ~$700/t |

| Cement (2024) | ~£80/t |

| Diesel (2024) | ~£1.10/l |

| Wage growth | ~6% |

Preview Before You Purchase

Keller Group PESTLE Analysis

The preview shown here is the exact Keller Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with charts and action points. No placeholders or teasers—download the finished file immediately after checkout.

Skip the Research. Get the Strategy.

Unlock strategic clarity with our targeted PESTLE Analysis of Keller Group—examining political, economic, social, technological, legal, and environmental forces shaping its outlook. This concise briefing reveals risks and growth levers you can act on today. Ideal for investors and strategists, it’s ready to deploy in boardrooms and models. Purchase the full report to access the complete, editable analysis instantly.

Political factors

Public infrastructure spending priorities

Government budgets and stimulus — notably the US Infrastructure Investment and Jobs Act worth roughly $1.2 trillion and Global Infrastructure Hub estimates of about $94 trillion needed in global infrastructure investment to 2040 — drive demand for transportation, energy, water and flood‑defence projects that are intensive in geotechnical work. Shifts after elections can reallocate capital away from or toward these programmes, creating pipeline volatility despite Keller benefiting from multi‑year contracts. Active geographic diversification helps buffer policy swings and smooth revenue exposure.

Permitting and planning regimes

Complex multilayer approvals in many jurisdictions mean start dates and scope for ground works often slip; in England major planning applications have a statutory 13-week decision target but frequently need longer. Stricter impact assessments and stakeholder consultations can add months to mobilization. Early regulatory engagement de-risks schedules and local expertise is crucial to navigate municipal and national rules.

Geopolitical risk and market access

Sanctions, trade restrictions and regional instability can halt Keller projects and disrupt supply chains, causing delays in materials and specialist plant movement across borders.

Cross-border equipment transfers often encounter customs clearance and visa hurdles for technical crews, increasing mobilisation times and costs.

Balancing a portfolio between OECD and emerging markets, alongside political risk insurance and flexible contracting, helps preserve margins and limit concentrated exposure.

Local content and procurement policies

Governments increasingly mandate domestic sourcing, joint ventures or workforce quotas—in some jurisdictions local content rules demand up to 60% local procurement—forcing Keller to adapt bid structures and delivery models; compliance affects competitiveness while non-compliance risks disqualification or fines. Building local partnerships and training programs strengthens Keller’s licence to operate and long‑term margins.

- Domestic sourcing: up to 60% local content

- Impacts: bid competitiveness, delivery models

- Mitigation: local JV, training programs, partnerships

- Risk: disqualification, financial penalties

Public–private partnership frameworks

PPP structures unlock large, complex geotechnical contracts, directing major civil programmes to specialists and shaping project pipelines for firms like Keller, which operates in 40+ countries with ~11,000 staff (2024).

Risk allocation and payment mechanisms determine cash flow and returns; transparent procurement boosts bid confidence while weak frameworks increase counterparty risk; strong balance sheets support bonding and guarantees.

- PPP access: large technical jobs

- Payments: drive cashflow/returns

- Procurement: transparency = lower risk

- Balance sheet: enables bonds/guarantees

Political shifts and local content rules reshape geotechnical project risk and mobilization

Political shifts (eg US IIJA ~$1.2T, Global Infrastructure Hub $94T to 2040) drive geotechnical demand; election changes create pipeline volatility despite multi‑year contracts. Permitting, sanctions and local content rules (up to 60% local procurement) raise mobilisation costs and compliance risk. Diversification, local JVs and political risk insurance mitigate exposure; Keller: 40+ countries, ~11,000 staff (2024).

| Factor | Metric | Impact | Mitigation |

|---|---|---|---|

| Infrastructure spend | $1.2T (IIJA); $94T to 2040 | Pipeline growth/volatility | Geographic diversification |

| Local content | Up to 60% | Higher costs/qualification risk | Local JV, training |

What is included in the product

Explores how macro-environmental forces uniquely affect the Keller Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, industry-specific examples and forward-looking insights to inform strategic planning, risk mitigation and investor communications.

A concise, visually segmented Keller Group PESTLE summary that simplifies external risk assessment for meetings, is easily editable with region- or line-specific notes, and can be dropped into presentations or shared across teams to speed strategic alignment.

Economic factors

Cyclical construction demand

Cyclical construction demand drives Keller's order intake, with macro growth and housing cycles plus large infrastructure pipelines underpinning wins; the group reported continued healthy activity through 2024 with backlog staying above £1bn mid‑2024. Recessions trim private housing and commercial development, though public works and infrastructure spending have historically partially offset downturns. A diversified sector mix across transport, energy and industrial projects smooths exposure, while backlog quality remains critical to utilization rates and pricing power.

Interest rates and project financing

Higher borrowing costs — Bank of England base rate at 5.25% and 10-year gilt yields near 4.5% in mid‑2025 — lift developer WACC and defer commercial starts, squeezing public issuers' debt capacity. Keller faces higher working‑capital needs and elevated bonding costs that compress margins, though targeted hedging and milestone billing are used to stabilize liquidity and reduce funding spikes.

Input costs and supply chain inflation

Rising input costs—steel averaging about $700/tonne in 2024, cement near £80/tonne and diesel around $1.10/litre—directly inflate Keller job costing and compress margins. Volatile logistics and lead times, with container freight still ~50% below 2021 peaks but spiking intermittently, disrupt scheduling. Use of escalation clauses and forward procurement has preserved margins on major projects. Standardization and long-term supplier agreements boost resilience and lower bid volatility.

Labor availability and wage pressures

Skilled geotechnical crews and engineers remain scarce across key markets, and Keller employed around 11,000 people in 2023–24, concentrating talent in specialist regions.

Wage inflation and rising training costs—industry wage growth near 6% in recent years—can compress margins, though productivity tools and method optimisation improve output per worker and offset some expenses.

Apprenticeships and retention programmes have been expanded to stabilise capability and reduce turnover-related hiring costs.

- Scarcity: specialised crews concentrated regionally

- Workforce: ~11,000 employees (2023–24)

- Wage pressure: ~6% industry wage growth recently

- Mitigation: productivity tools, apprenticeships, retention

Currency fluctuations in global operations

Currency fluctuations across Keller Groups global operations create FX translation and transaction risk as revenues, costs and bids are denominated in multiple currencies; bids fixed in one currency while inputs are paid in another can quickly erode margins. Keller mitigates volatility through natural hedging by aligning regional cost bases to local revenues and selective use of derivatives and forward contracts disclosed in its 2024 annual report. Ongoing monitoring of currency exposures remains central to bid pricing and working capital.

- Multi-currency revenues/costs = translation & transaction risk

- Bids fixed in one currency while inputs in another can erode margin

- Natural hedging + derivatives (forwards) reduce volatility

- Align regional cost bases to revenues to improve protection

Political shifts and local content rules reshape geotechnical project risk and mobilization

Cyclical construction demand drives Keller's order intake; backlog stayed above £1bn mid‑2024 and public infrastructure partly offsets downturns. Higher borrowing costs (BoE 5.25% mid‑2025, 10y gilt ~4.5%) and rising inputs (steel ~$700/t, cement ~£80/t, diesel ~£1.10/l) squeeze margins; mitigation includes escalation clauses, hedging and long‑term supply deals. Workforce ~11,000 with ~6% wage pressure.

| Metric | Value |

|---|---|

| Backlog (mid‑2024) | £>1bn |

| Employees (2023–24) | ~11,000 |

| BoE base rate (mid‑2025) | 5.25% |

| 10y gilt | ~4.5% |

| Steel (2024) | ~$700/t |

| Cement (2024) | ~£80/t |

| Diesel (2024) | ~£1.10/l |

| Wage growth | ~6% |

Preview Before You Purchase

Keller Group PESTLE Analysis

The preview shown here is the exact Keller Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with charts and action points. No placeholders or teasers—download the finished file immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our targeted PESTLE Analysis of Keller Group—examining political, economic, social, technological, legal, and environmental forces shaping its outlook. This concise briefing reveals risks and growth levers you can act on today. Ideal for investors and strategists, it’s ready to deploy in boardrooms and models. Purchase the full report to access the complete, editable analysis instantly.

Political factors

Public infrastructure spending priorities

Government budgets and stimulus — notably the US Infrastructure Investment and Jobs Act worth roughly $1.2 trillion and Global Infrastructure Hub estimates of about $94 trillion needed in global infrastructure investment to 2040 — drive demand for transportation, energy, water and flood‑defence projects that are intensive in geotechnical work. Shifts after elections can reallocate capital away from or toward these programmes, creating pipeline volatility despite Keller benefiting from multi‑year contracts. Active geographic diversification helps buffer policy swings and smooth revenue exposure.

Permitting and planning regimes

Complex multilayer approvals in many jurisdictions mean start dates and scope for ground works often slip; in England major planning applications have a statutory 13-week decision target but frequently need longer. Stricter impact assessments and stakeholder consultations can add months to mobilization. Early regulatory engagement de-risks schedules and local expertise is crucial to navigate municipal and national rules.

Geopolitical risk and market access

Sanctions, trade restrictions and regional instability can halt Keller projects and disrupt supply chains, causing delays in materials and specialist plant movement across borders.

Cross-border equipment transfers often encounter customs clearance and visa hurdles for technical crews, increasing mobilisation times and costs.

Balancing a portfolio between OECD and emerging markets, alongside political risk insurance and flexible contracting, helps preserve margins and limit concentrated exposure.

Local content and procurement policies

Governments increasingly mandate domestic sourcing, joint ventures or workforce quotas—in some jurisdictions local content rules demand up to 60% local procurement—forcing Keller to adapt bid structures and delivery models; compliance affects competitiveness while non-compliance risks disqualification or fines. Building local partnerships and training programs strengthens Keller’s licence to operate and long‑term margins.

- Domestic sourcing: up to 60% local content

- Impacts: bid competitiveness, delivery models

- Mitigation: local JV, training programs, partnerships

- Risk: disqualification, financial penalties

Public–private partnership frameworks

PPP structures unlock large, complex geotechnical contracts, directing major civil programmes to specialists and shaping project pipelines for firms like Keller, which operates in 40+ countries with ~11,000 staff (2024).

Risk allocation and payment mechanisms determine cash flow and returns; transparent procurement boosts bid confidence while weak frameworks increase counterparty risk; strong balance sheets support bonding and guarantees.

- PPP access: large technical jobs

- Payments: drive cashflow/returns

- Procurement: transparency = lower risk

- Balance sheet: enables bonds/guarantees

Political shifts and local content rules reshape geotechnical project risk and mobilization

Political shifts (eg US IIJA ~$1.2T, Global Infrastructure Hub $94T to 2040) drive geotechnical demand; election changes create pipeline volatility despite multi‑year contracts. Permitting, sanctions and local content rules (up to 60% local procurement) raise mobilisation costs and compliance risk. Diversification, local JVs and political risk insurance mitigate exposure; Keller: 40+ countries, ~11,000 staff (2024).

| Factor | Metric | Impact | Mitigation |

|---|---|---|---|

| Infrastructure spend | $1.2T (IIJA); $94T to 2040 | Pipeline growth/volatility | Geographic diversification |

| Local content | Up to 60% | Higher costs/qualification risk | Local JV, training |

What is included in the product

Explores how macro-environmental forces uniquely affect the Keller Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, industry-specific examples and forward-looking insights to inform strategic planning, risk mitigation and investor communications.

A concise, visually segmented Keller Group PESTLE summary that simplifies external risk assessment for meetings, is easily editable with region- or line-specific notes, and can be dropped into presentations or shared across teams to speed strategic alignment.

Economic factors

Cyclical construction demand

Cyclical construction demand drives Keller's order intake, with macro growth and housing cycles plus large infrastructure pipelines underpinning wins; the group reported continued healthy activity through 2024 with backlog staying above £1bn mid‑2024. Recessions trim private housing and commercial development, though public works and infrastructure spending have historically partially offset downturns. A diversified sector mix across transport, energy and industrial projects smooths exposure, while backlog quality remains critical to utilization rates and pricing power.

Interest rates and project financing

Higher borrowing costs — Bank of England base rate at 5.25% and 10-year gilt yields near 4.5% in mid‑2025 — lift developer WACC and defer commercial starts, squeezing public issuers' debt capacity. Keller faces higher working‑capital needs and elevated bonding costs that compress margins, though targeted hedging and milestone billing are used to stabilize liquidity and reduce funding spikes.

Input costs and supply chain inflation

Rising input costs—steel averaging about $700/tonne in 2024, cement near £80/tonne and diesel around $1.10/litre—directly inflate Keller job costing and compress margins. Volatile logistics and lead times, with container freight still ~50% below 2021 peaks but spiking intermittently, disrupt scheduling. Use of escalation clauses and forward procurement has preserved margins on major projects. Standardization and long-term supplier agreements boost resilience and lower bid volatility.

Labor availability and wage pressures

Skilled geotechnical crews and engineers remain scarce across key markets, and Keller employed around 11,000 people in 2023–24, concentrating talent in specialist regions.

Wage inflation and rising training costs—industry wage growth near 6% in recent years—can compress margins, though productivity tools and method optimisation improve output per worker and offset some expenses.

Apprenticeships and retention programmes have been expanded to stabilise capability and reduce turnover-related hiring costs.

- Scarcity: specialised crews concentrated regionally

- Workforce: ~11,000 employees (2023–24)

- Wage pressure: ~6% industry wage growth recently

- Mitigation: productivity tools, apprenticeships, retention

Currency fluctuations in global operations

Currency fluctuations across Keller Groups global operations create FX translation and transaction risk as revenues, costs and bids are denominated in multiple currencies; bids fixed in one currency while inputs are paid in another can quickly erode margins. Keller mitigates volatility through natural hedging by aligning regional cost bases to local revenues and selective use of derivatives and forward contracts disclosed in its 2024 annual report. Ongoing monitoring of currency exposures remains central to bid pricing and working capital.

- Multi-currency revenues/costs = translation & transaction risk

- Bids fixed in one currency while inputs in another can erode margin

- Natural hedging + derivatives (forwards) reduce volatility

- Align regional cost bases to revenues to improve protection

Political shifts and local content rules reshape geotechnical project risk and mobilization

Cyclical construction demand drives Keller's order intake; backlog stayed above £1bn mid‑2024 and public infrastructure partly offsets downturns. Higher borrowing costs (BoE 5.25% mid‑2025, 10y gilt ~4.5%) and rising inputs (steel ~$700/t, cement ~£80/t, diesel ~£1.10/l) squeeze margins; mitigation includes escalation clauses, hedging and long‑term supply deals. Workforce ~11,000 with ~6% wage pressure.

| Metric | Value |

|---|---|

| Backlog (mid‑2024) | £>1bn |

| Employees (2023–24) | ~11,000 |

| BoE base rate (mid‑2025) | 5.25% |

| 10y gilt | ~4.5% |

| Steel (2024) | ~$700/t |

| Cement (2024) | ~£80/t |

| Diesel (2024) | ~£1.10/l |

| Wage growth | ~6% |

Preview Before You Purchase

Keller Group PESTLE Analysis

The preview shown here is the exact Keller Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with charts and action points. No placeholders or teasers—download the finished file immediately after checkout.