Keller Group SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Keller Group’s market position blends specialist civil engineering expertise with cyclical exposure—our concise SWOT highlights key strengths, emerging risks, and strategic opportunities. For investors and strategists seeking actionable clarity, the full SWOT delivers deeper financial context, risk scenarios, and practical recommendations. Purchase the complete report to get a professionally formatted Word analysis plus an editable Excel matrix for planning and presentations.

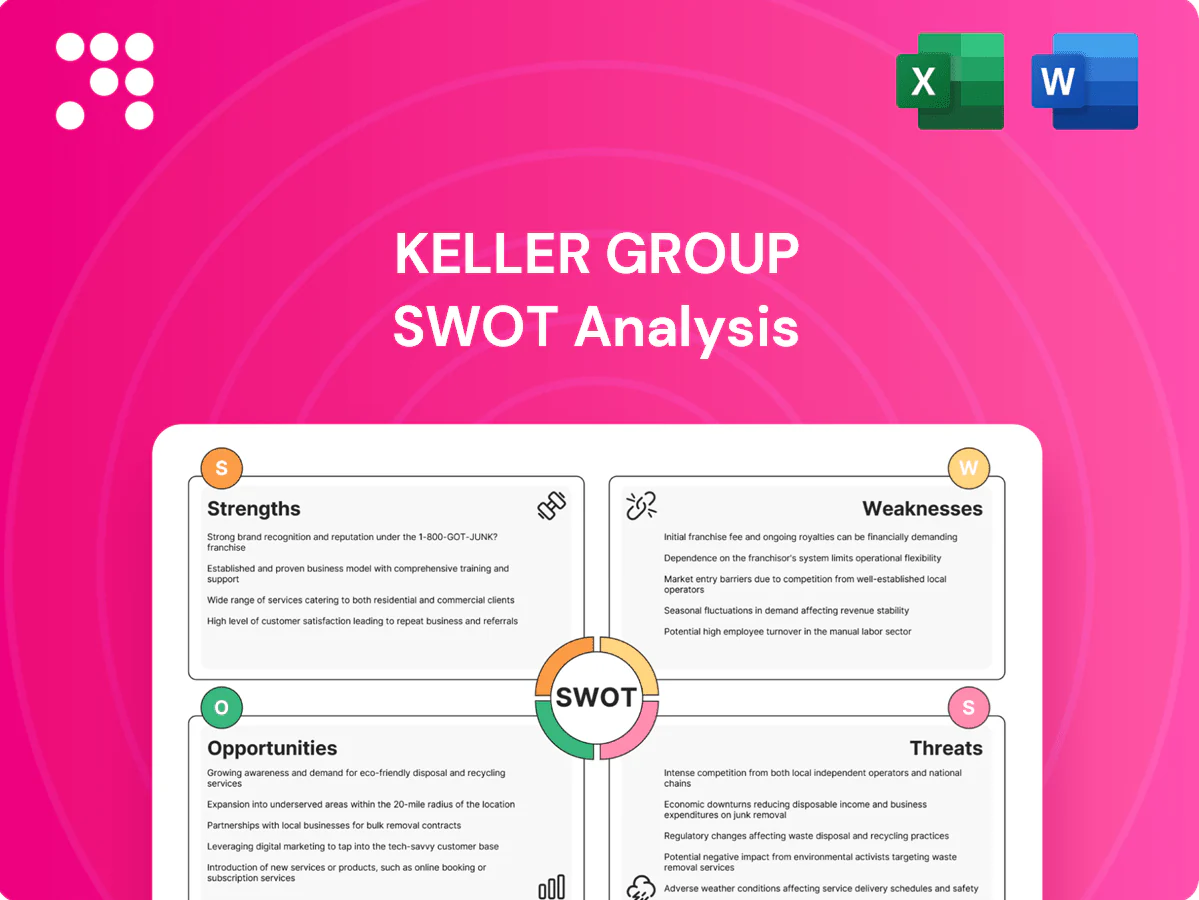

Strengths

Global geotechnical leadership

Recognised as the world’s largest geotechnical specialist, Keller’s scale and focus on ground engineering underpin strong competitive positioning; its operations in 40+ countries enable rapid knowledge transfer and mobilization across regions and sectors. Brand credibility wins complex, high‑value framework contracts and supports pricing power and preferred‑bidder status in technical tenders.

Diverse service portfolio

Keller, the world’s largest geotechnical specialist, offers ground improvement, piling, deep foundations, grouting, anchors and remediation across over 40 countries, enabling integrated solutions that reduce client interface risk. Its cross-selling across techniques lifts project share-of-wallet and improves fleet utilization. Diversification across services and markets buffers cyclicality in end markets and geographies.

Technical expertise and IP

Engineering depth and proprietary methods and specialist equipment enable Keller, the world’s largest geotechnical specialist, to deliver predictable outcomes in difficult ground; proven methodologies lower construction risk and rework. Data from thousands of projects refines design optimization and cost accuracy, while ISO 9001 and ISO 45001-certified safety and quality systems boost client trust and repeat business.

Exposure to infrastructure spend

Exposure to public infrastructure, energy and transport programs drives steady demand for Keller, with FY 2024 group revenue around £2.0bn and a multi-year order book supporting visibility into work pipelines.

- Early-in value chain positioning embeds Keller in project-critical scopes; order book ≈ £1.1bn; resilience vs commercial-only peers

Operational scale and fleet

Large owned equipment fleet and in-house crews allow Keller to mobilize quickly and drive competitive unit costs; procurement scale secures materials and lowers input volatility; standardized processes across regions lift operational efficiency; scale underpins ongoing investment in training, R&D and digital field tools.

- Fleet-led mobilization

- Procurement leverage

- Standardized ops

- Investment capacity

Global geotechnical leader: £2.0bn FY2024 revenue, 40+ countries

Keller is the world’s largest geotechnical specialist, operating in 40+ countries with FY2024 revenue ~£2.0bn and order book ≈£1.1bn.

Scale, owned fleet and standardized ops enable rapid mobilization, procurement leverage and lower unit costs.

Engineering depth, proprietary methods and ISO-certified systems win complex, high-value framework contracts and repeat clients.

| Metric | Value |

|---|---|

| FY2024 revenue | ≈£2.0bn |

| Order book | ≈£1.1bn |

| Operating footprint | 40+ countries |

What is included in the product

Provides a concise SWOT analysis of Keller Group, outlining internal strengths and weaknesses and external opportunities and threats to assess its competitive position, growth drivers, operational gaps, and strategic risks shaping future performance.

Provides a concise, editable SWOT matrix tailored to Keller Group for rapid stakeholder alignment and quick updates to reflect shifting project and market priorities.

Weaknesses

Project risk exposure

Keller (LSE:KLR) faces heightened project risk exposure in fixed-price and design-build work where ground condition variability drives claims, delays and cost overruns that compress margins. Subsurface uncertainty makes contingency setting and disciplined bidding difficult, increasing the likelihood of margin erosion. Mitigating this requires robust risk management and rigorous geotechnical investigation to protect profitability.

Capital intensity

Specialist rigs and ongoing maintenance force Keller to invest heavily in fleet capex, with group revenue of about £2.1bn in FY 2024 and reported capital expenditure near £68m that year, keeping fixed costs high.

Utilisation swings in cyclical markets can quickly dilute returns—ROCE has shown volatility across cycles, stressing margins in downturns.

The balance sheet must fund fleet refreshes and regional redeployments, and high capital requirements constrain operational flexibility and amplify ROCE volatility.

Regional execution variance

Regional execution variance causes Keller units to perform unevenly across markets; FY2024 revenue of £1,896m masked operating margin swings from low single digits in some APAC and Europe territories to double digits in North America, driven by local supply-chain bottlenecks, labour shortages and permitting delays. Integration of recent acquisitions and group-wide standardisation remain work in progress, while management attention is stretched across 30+ geographies.

Reliance on cyclical end-markets

Reliance on cyclical private real estate and industrial projects leaves Keller exposed to swings in developer activity and financing availability, which directly affects near-term awards and tendering.

Mix shifts toward lower-complexity work can compress margins, making backlog quality—not just headline volume—critical for sustaining margin recovery.

Safety and incident sensitivity

Heavy civil operations expose Keller to inherent safety risks where any serious incident can halt projects and damage the firm’s reputation; maintaining zero-harm performance requires sustained investment in training, supervision and safety systems.

- High operational risk

- Reputation-sensitive

- Material insurance/compliance burden

- Ongoing training/culture costs

Subsurface risk, high fleet capex (£68m) and poor regional execution

Keller’s weaknesses include project risk from subsurface uncertainty that compresses margins on fixed-price work, high fleet capex (FY2024 capex ~£68m on revenue £1,896m) raising fixed costs, and uneven regional execution across 30+ geographies causing margin volatility. Dependence on cyclical developer markets and lower-complexity mix further threaten near-term earnings and ROCE.

| Metric | 2024 |

|---|---|

| Revenue | £1,896m |

| Capital expenditure | £68m |

| Geographies | 30+ |

Preview Before You Purchase

Keller Group SWOT Analysis

This is the actual Keller Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering strengths, weaknesses, opportunities and threats. Buy now to download the complete, editable file immediately after checkout.

Make Insightful Decisions Backed by Expert Research

Keller Group’s market position blends specialist civil engineering expertise with cyclical exposure—our concise SWOT highlights key strengths, emerging risks, and strategic opportunities. For investors and strategists seeking actionable clarity, the full SWOT delivers deeper financial context, risk scenarios, and practical recommendations. Purchase the complete report to get a professionally formatted Word analysis plus an editable Excel matrix for planning and presentations.

Strengths

Global geotechnical leadership

Recognised as the world’s largest geotechnical specialist, Keller’s scale and focus on ground engineering underpin strong competitive positioning; its operations in 40+ countries enable rapid knowledge transfer and mobilization across regions and sectors. Brand credibility wins complex, high‑value framework contracts and supports pricing power and preferred‑bidder status in technical tenders.

Diverse service portfolio

Keller, the world’s largest geotechnical specialist, offers ground improvement, piling, deep foundations, grouting, anchors and remediation across over 40 countries, enabling integrated solutions that reduce client interface risk. Its cross-selling across techniques lifts project share-of-wallet and improves fleet utilization. Diversification across services and markets buffers cyclicality in end markets and geographies.

Technical expertise and IP

Engineering depth and proprietary methods and specialist equipment enable Keller, the world’s largest geotechnical specialist, to deliver predictable outcomes in difficult ground; proven methodologies lower construction risk and rework. Data from thousands of projects refines design optimization and cost accuracy, while ISO 9001 and ISO 45001-certified safety and quality systems boost client trust and repeat business.

Exposure to infrastructure spend

Exposure to public infrastructure, energy and transport programs drives steady demand for Keller, with FY 2024 group revenue around £2.0bn and a multi-year order book supporting visibility into work pipelines.

- Early-in value chain positioning embeds Keller in project-critical scopes; order book ≈ £1.1bn; resilience vs commercial-only peers

Operational scale and fleet

Large owned equipment fleet and in-house crews allow Keller to mobilize quickly and drive competitive unit costs; procurement scale secures materials and lowers input volatility; standardized processes across regions lift operational efficiency; scale underpins ongoing investment in training, R&D and digital field tools.

- Fleet-led mobilization

- Procurement leverage

- Standardized ops

- Investment capacity

Global geotechnical leader: £2.0bn FY2024 revenue, 40+ countries

Keller is the world’s largest geotechnical specialist, operating in 40+ countries with FY2024 revenue ~£2.0bn and order book ≈£1.1bn.

Scale, owned fleet and standardized ops enable rapid mobilization, procurement leverage and lower unit costs.

Engineering depth, proprietary methods and ISO-certified systems win complex, high-value framework contracts and repeat clients.

| Metric | Value |

|---|---|

| FY2024 revenue | ≈£2.0bn |

| Order book | ≈£1.1bn |

| Operating footprint | 40+ countries |

What is included in the product

Provides a concise SWOT analysis of Keller Group, outlining internal strengths and weaknesses and external opportunities and threats to assess its competitive position, growth drivers, operational gaps, and strategic risks shaping future performance.

Provides a concise, editable SWOT matrix tailored to Keller Group for rapid stakeholder alignment and quick updates to reflect shifting project and market priorities.

Weaknesses

Project risk exposure

Keller (LSE:KLR) faces heightened project risk exposure in fixed-price and design-build work where ground condition variability drives claims, delays and cost overruns that compress margins. Subsurface uncertainty makes contingency setting and disciplined bidding difficult, increasing the likelihood of margin erosion. Mitigating this requires robust risk management and rigorous geotechnical investigation to protect profitability.

Capital intensity

Specialist rigs and ongoing maintenance force Keller to invest heavily in fleet capex, with group revenue of about £2.1bn in FY 2024 and reported capital expenditure near £68m that year, keeping fixed costs high.

Utilisation swings in cyclical markets can quickly dilute returns—ROCE has shown volatility across cycles, stressing margins in downturns.

The balance sheet must fund fleet refreshes and regional redeployments, and high capital requirements constrain operational flexibility and amplify ROCE volatility.

Regional execution variance

Regional execution variance causes Keller units to perform unevenly across markets; FY2024 revenue of £1,896m masked operating margin swings from low single digits in some APAC and Europe territories to double digits in North America, driven by local supply-chain bottlenecks, labour shortages and permitting delays. Integration of recent acquisitions and group-wide standardisation remain work in progress, while management attention is stretched across 30+ geographies.

Reliance on cyclical end-markets

Reliance on cyclical private real estate and industrial projects leaves Keller exposed to swings in developer activity and financing availability, which directly affects near-term awards and tendering.

Mix shifts toward lower-complexity work can compress margins, making backlog quality—not just headline volume—critical for sustaining margin recovery.

Safety and incident sensitivity

Heavy civil operations expose Keller to inherent safety risks where any serious incident can halt projects and damage the firm’s reputation; maintaining zero-harm performance requires sustained investment in training, supervision and safety systems.

- High operational risk

- Reputation-sensitive

- Material insurance/compliance burden

- Ongoing training/culture costs

Subsurface risk, high fleet capex (£68m) and poor regional execution

Keller’s weaknesses include project risk from subsurface uncertainty that compresses margins on fixed-price work, high fleet capex (FY2024 capex ~£68m on revenue £1,896m) raising fixed costs, and uneven regional execution across 30+ geographies causing margin volatility. Dependence on cyclical developer markets and lower-complexity mix further threaten near-term earnings and ROCE.

| Metric | 2024 |

|---|---|

| Revenue | £1,896m |

| Capital expenditure | £68m |

| Geographies | 30+ |

Preview Before You Purchase

Keller Group SWOT Analysis

This is the actual Keller Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering strengths, weaknesses, opportunities and threats. Buy now to download the complete, editable file immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Keller Group’s market position blends specialist civil engineering expertise with cyclical exposure—our concise SWOT highlights key strengths, emerging risks, and strategic opportunities. For investors and strategists seeking actionable clarity, the full SWOT delivers deeper financial context, risk scenarios, and practical recommendations. Purchase the complete report to get a professionally formatted Word analysis plus an editable Excel matrix for planning and presentations.

Strengths

Global geotechnical leadership

Recognised as the world’s largest geotechnical specialist, Keller’s scale and focus on ground engineering underpin strong competitive positioning; its operations in 40+ countries enable rapid knowledge transfer and mobilization across regions and sectors. Brand credibility wins complex, high‑value framework contracts and supports pricing power and preferred‑bidder status in technical tenders.

Diverse service portfolio

Keller, the world’s largest geotechnical specialist, offers ground improvement, piling, deep foundations, grouting, anchors and remediation across over 40 countries, enabling integrated solutions that reduce client interface risk. Its cross-selling across techniques lifts project share-of-wallet and improves fleet utilization. Diversification across services and markets buffers cyclicality in end markets and geographies.

Technical expertise and IP

Engineering depth and proprietary methods and specialist equipment enable Keller, the world’s largest geotechnical specialist, to deliver predictable outcomes in difficult ground; proven methodologies lower construction risk and rework. Data from thousands of projects refines design optimization and cost accuracy, while ISO 9001 and ISO 45001-certified safety and quality systems boost client trust and repeat business.

Exposure to infrastructure spend

Exposure to public infrastructure, energy and transport programs drives steady demand for Keller, with FY 2024 group revenue around £2.0bn and a multi-year order book supporting visibility into work pipelines.

- Early-in value chain positioning embeds Keller in project-critical scopes; order book ≈ £1.1bn; resilience vs commercial-only peers

Operational scale and fleet

Large owned equipment fleet and in-house crews allow Keller to mobilize quickly and drive competitive unit costs; procurement scale secures materials and lowers input volatility; standardized processes across regions lift operational efficiency; scale underpins ongoing investment in training, R&D and digital field tools.

- Fleet-led mobilization

- Procurement leverage

- Standardized ops

- Investment capacity

Global geotechnical leader: £2.0bn FY2024 revenue, 40+ countries

Keller is the world’s largest geotechnical specialist, operating in 40+ countries with FY2024 revenue ~£2.0bn and order book ≈£1.1bn.

Scale, owned fleet and standardized ops enable rapid mobilization, procurement leverage and lower unit costs.

Engineering depth, proprietary methods and ISO-certified systems win complex, high-value framework contracts and repeat clients.

| Metric | Value |

|---|---|

| FY2024 revenue | ≈£2.0bn |

| Order book | ≈£1.1bn |

| Operating footprint | 40+ countries |

What is included in the product

Provides a concise SWOT analysis of Keller Group, outlining internal strengths and weaknesses and external opportunities and threats to assess its competitive position, growth drivers, operational gaps, and strategic risks shaping future performance.

Provides a concise, editable SWOT matrix tailored to Keller Group for rapid stakeholder alignment and quick updates to reflect shifting project and market priorities.

Weaknesses

Project risk exposure

Keller (LSE:KLR) faces heightened project risk exposure in fixed-price and design-build work where ground condition variability drives claims, delays and cost overruns that compress margins. Subsurface uncertainty makes contingency setting and disciplined bidding difficult, increasing the likelihood of margin erosion. Mitigating this requires robust risk management and rigorous geotechnical investigation to protect profitability.

Capital intensity

Specialist rigs and ongoing maintenance force Keller to invest heavily in fleet capex, with group revenue of about £2.1bn in FY 2024 and reported capital expenditure near £68m that year, keeping fixed costs high.

Utilisation swings in cyclical markets can quickly dilute returns—ROCE has shown volatility across cycles, stressing margins in downturns.

The balance sheet must fund fleet refreshes and regional redeployments, and high capital requirements constrain operational flexibility and amplify ROCE volatility.

Regional execution variance

Regional execution variance causes Keller units to perform unevenly across markets; FY2024 revenue of £1,896m masked operating margin swings from low single digits in some APAC and Europe territories to double digits in North America, driven by local supply-chain bottlenecks, labour shortages and permitting delays. Integration of recent acquisitions and group-wide standardisation remain work in progress, while management attention is stretched across 30+ geographies.

Reliance on cyclical end-markets

Reliance on cyclical private real estate and industrial projects leaves Keller exposed to swings in developer activity and financing availability, which directly affects near-term awards and tendering.

Mix shifts toward lower-complexity work can compress margins, making backlog quality—not just headline volume—critical for sustaining margin recovery.

Safety and incident sensitivity

Heavy civil operations expose Keller to inherent safety risks where any serious incident can halt projects and damage the firm’s reputation; maintaining zero-harm performance requires sustained investment in training, supervision and safety systems.

- High operational risk

- Reputation-sensitive

- Material insurance/compliance burden

- Ongoing training/culture costs

Subsurface risk, high fleet capex (£68m) and poor regional execution

Keller’s weaknesses include project risk from subsurface uncertainty that compresses margins on fixed-price work, high fleet capex (FY2024 capex ~£68m on revenue £1,896m) raising fixed costs, and uneven regional execution across 30+ geographies causing margin volatility. Dependence on cyclical developer markets and lower-complexity mix further threaten near-term earnings and ROCE.

| Metric | 2024 |

|---|---|

| Revenue | £1,896m |

| Capital expenditure | £68m |

| Geographies | 30+ |

Preview Before You Purchase

Keller Group SWOT Analysis

This is the actual Keller Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, covering strengths, weaknesses, opportunities and threats. Buy now to download the complete, editable file immediately after checkout.