Kemira SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Kemira's SWOT highlights strong specialty-chemicals expertise and sustainability leadership, countered by cyclical demand and raw-material sensitivity; opportunities include growing water-treatment and circular-economy demand while competition and input volatility are key threats. Discover the full, editable SWOT report—detailed insights, financial context, and Excel tools—to inform strategy, pitches, and investment decisions.

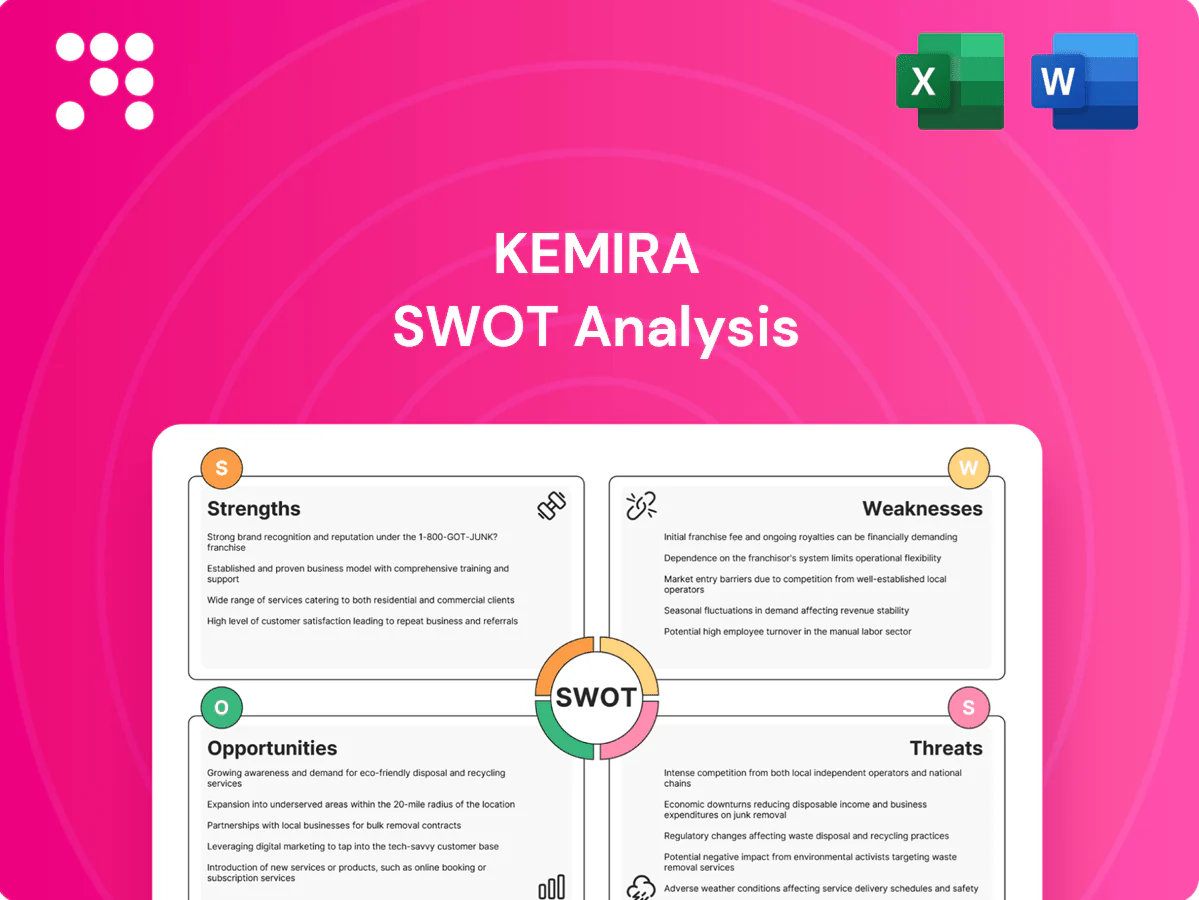

Strengths

Deep water-treatment expertise

Over a century of water-chemistry specialization gives Kemira deep application know-how across coagulation, flocculation and sludge treatment, translating into measurable improvements in quality and throughput for industrial and municipal clients. Its technologies and embedded formulations create high switching costs, reinforced by process integration and field-tested blends used across 40+ countries. Local technical-service teams drive stickiness and upselling through pilots, troubleshooting and dose-optimization support.

Strong position in pulp & paper

Kemira is a partner of choice for retention aids, sizing, bleaching and strength chemicals in pulp and paper, offering integrated solutions that boost fiber yield, machine runnability and end-product properties. Close mill-level collaboration enables continuous optimization and cross-selling across chemical portfolios. Demand is underpinned by resilient tissue and packaging end-markets supporting stable volumes and recurring sales.

Broad, resilient portfolio

Exposure to municipal and industrial water, pulp & paper and energy markets diversifies Kemira’s revenue mix, with the company operating in over 100 countries and reporting net sales around EUR 2.5bn in 2024.

Countercyclical water-treatment volumes help offset softness in cyclical pulp & paper or energy segments, cushioning top-line swings.

A broad product suite enables tailored solutions across customer sizes and geographies, supporting margin stability through cycles.

Regulatory and sustainability alignment

- Regulatory-driven demand

- ESG-aligned product portfolio

- Compliance eases contracting

- Pricing power for premium chemistries

Global footprint and service model

Kemira’s global footprint—over 40 production sites and service centers serving 100+ countries—pairs manufacturing, supply and on-site technical support to secure reliable delivery and shorter lead times for bulky chemicals; 2024 net sales were around EUR 3.0bn, underlining scale. Application labs and pilot projects speed customer value realization, while proximity enables rapid problem-solving and long-term relationships.

- Manufacturing: 40+ sites

- Reach: 100+ countries

- Scale: ~EUR 3.0bn 2024 sales

- Benefits: reduced logistics risk, faster pilots, stronger customer ties

Global water-chemistry platform: 100+ countries, 40+ sites, ~EUR 3.0bn, stable municipal demand

Kemira’s 100+ country reach and 40+ production sites underpin reliable supply and local technical service, driving customer stickiness and upsell. Deep water-chemistry expertise and integrated formulations create high switching costs and regulatory-aligned demand that supports premium pricing. 2024 net sales ~EUR 3.0bn; countercyclical municipal water volumes stabilize revenue versus pulp & paper cycles.

| Metric | Value |

|---|---|

| 2024 net sales | ~EUR 3.0bn |

| Countries | 100+ |

| Production sites | 40+ |

| Core markets | Water, pulp & paper, energy |

What is included in the product

Provides a focused SWOT analysis of Kemira, highlighting its operational strengths and sustainability-driven opportunities alongside internal weaknesses and market threats that will shape the company’s future competitiveness.

Delivers a concise Kemira SWOT matrix for rapid strategic alignment, ideal for executives needing a clear snapshot of competitive positioning, risks, and actionable priorities.

Weaknesses

End-market cyclicality

Volumes and pricing at Kemira are highly sensitive to pulp & paper and oil & gas cycles, so mill downtime, destocking or E&P budget cuts can quickly depress demand. Fixed-cost absorption tightens margins during downturns, amplifying profit volatility. Rapid customer run-rate changes make short-term forecasting and inventory planning notably harder, increasing working-capital strain.

Raw material and energy exposure

Raw material and energy exposure: prices for monomers, caustic and acids and power are volatile—European TTF gas spiked above €300/MWh in 2022 and industrial energy costs remained elevated into 2023–24, compressing margins when pass-through lags. Regional energy shocks weaken European cost competitiveness. Hedging and surcharge mechanisms only partially close timing gaps, leaving short-term margin risk.

Capital and logistics intensity

Bulk chemicals demand heavy capex for plants, storage and handling — Kemira reported revenues of about €3.0bn in 2023, reflecting scale but also capital intensity. Hazardous materials force strict transport, permitting and safety costs that raise operating complexity. High working capital ties cash in inventory and receivables, while optimizing logistics across dispersed customer sites remains technically and economically complex.

Product commoditization risk

Product commoditization exposes Kemira to intense price competition in many water-treatment chemistries. Low-cost producers, especially from Asia, can squeeze margins on standardized SKUs. Differentiation hinges on service, performance data and integrated solutions, so continuous innovation and R&D are required to avoid price erosion; global market ~USD 42B (2023), ~5% CAGR.

- Price pressure from low-cost producers

- Standardized SKUs compress margins

- Need for service/data-driven differentiation

- Ongoing R&D spend required to protect pricing

Limited diversification beyond core

Kemira’s focus on water-intensive end-markets concentrates sector-specific risk: net sales were about EUR 2.0bn in 2024 while a large share of revenue derives from pulp & paper and water-treatment segments, exposing the company to cyclical demand swings. Limited exposure to high-growth adjacencies constrains topline optionality, and a geographic mix with roughly half of sales in mature European markets limits upside versus peers. Portfolio breadth remains narrower than diversified global chemical competitors, reducing resilience.

- Concentration: high reliance on water-intensive verticals

- Growth limits: smaller presence in fast-growing adjacencies

- Geography: ~50% revenue from mature Europe

- Peer gap: narrower product portfolio vs global chemical peers

Cyclical chemicals: energy shocks, margin volatility and low-cost Asian pressure

Kemira is cyclical—volumes and pricing swing with pulp & paper and oil & gas cycles, amplifying margin volatility and working-capital strain. Energy and raw-material price exposure (TTF spiked >€300/MWh in 2022) compresses margins when pass-through lags. Capital intensity and product commoditization (global water-chemicals ~USD 42B in 2023, ~5% CAGR) limit pricing power versus low-cost Asian competitors.

| Metric | Value |

|---|---|

| Revenue (2023) | ≈€3.0bn |

| Net sales (2024) | ≈€2.0bn |

| Europe share | ≈50% |

Preview the Actual Deliverable

Kemira SWOT Analysis

This is the actual Kemira SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the final report; buy to unlock the complete, editable version.

Dive Deeper Into the Company’s Strategic Blueprint

Kemira's SWOT highlights strong specialty-chemicals expertise and sustainability leadership, countered by cyclical demand and raw-material sensitivity; opportunities include growing water-treatment and circular-economy demand while competition and input volatility are key threats. Discover the full, editable SWOT report—detailed insights, financial context, and Excel tools—to inform strategy, pitches, and investment decisions.

Strengths

Deep water-treatment expertise

Over a century of water-chemistry specialization gives Kemira deep application know-how across coagulation, flocculation and sludge treatment, translating into measurable improvements in quality and throughput for industrial and municipal clients. Its technologies and embedded formulations create high switching costs, reinforced by process integration and field-tested blends used across 40+ countries. Local technical-service teams drive stickiness and upselling through pilots, troubleshooting and dose-optimization support.

Strong position in pulp & paper

Kemira is a partner of choice for retention aids, sizing, bleaching and strength chemicals in pulp and paper, offering integrated solutions that boost fiber yield, machine runnability and end-product properties. Close mill-level collaboration enables continuous optimization and cross-selling across chemical portfolios. Demand is underpinned by resilient tissue and packaging end-markets supporting stable volumes and recurring sales.

Broad, resilient portfolio

Exposure to municipal and industrial water, pulp & paper and energy markets diversifies Kemira’s revenue mix, with the company operating in over 100 countries and reporting net sales around EUR 2.5bn in 2024.

Countercyclical water-treatment volumes help offset softness in cyclical pulp & paper or energy segments, cushioning top-line swings.

A broad product suite enables tailored solutions across customer sizes and geographies, supporting margin stability through cycles.

Regulatory and sustainability alignment

- Regulatory-driven demand

- ESG-aligned product portfolio

- Compliance eases contracting

- Pricing power for premium chemistries

Global footprint and service model

Kemira’s global footprint—over 40 production sites and service centers serving 100+ countries—pairs manufacturing, supply and on-site technical support to secure reliable delivery and shorter lead times for bulky chemicals; 2024 net sales were around EUR 3.0bn, underlining scale. Application labs and pilot projects speed customer value realization, while proximity enables rapid problem-solving and long-term relationships.

- Manufacturing: 40+ sites

- Reach: 100+ countries

- Scale: ~EUR 3.0bn 2024 sales

- Benefits: reduced logistics risk, faster pilots, stronger customer ties

Global water-chemistry platform: 100+ countries, 40+ sites, ~EUR 3.0bn, stable municipal demand

Kemira’s 100+ country reach and 40+ production sites underpin reliable supply and local technical service, driving customer stickiness and upsell. Deep water-chemistry expertise and integrated formulations create high switching costs and regulatory-aligned demand that supports premium pricing. 2024 net sales ~EUR 3.0bn; countercyclical municipal water volumes stabilize revenue versus pulp & paper cycles.

| Metric | Value |

|---|---|

| 2024 net sales | ~EUR 3.0bn |

| Countries | 100+ |

| Production sites | 40+ |

| Core markets | Water, pulp & paper, energy |

What is included in the product

Provides a focused SWOT analysis of Kemira, highlighting its operational strengths and sustainability-driven opportunities alongside internal weaknesses and market threats that will shape the company’s future competitiveness.

Delivers a concise Kemira SWOT matrix for rapid strategic alignment, ideal for executives needing a clear snapshot of competitive positioning, risks, and actionable priorities.

Weaknesses

End-market cyclicality

Volumes and pricing at Kemira are highly sensitive to pulp & paper and oil & gas cycles, so mill downtime, destocking or E&P budget cuts can quickly depress demand. Fixed-cost absorption tightens margins during downturns, amplifying profit volatility. Rapid customer run-rate changes make short-term forecasting and inventory planning notably harder, increasing working-capital strain.

Raw material and energy exposure

Raw material and energy exposure: prices for monomers, caustic and acids and power are volatile—European TTF gas spiked above €300/MWh in 2022 and industrial energy costs remained elevated into 2023–24, compressing margins when pass-through lags. Regional energy shocks weaken European cost competitiveness. Hedging and surcharge mechanisms only partially close timing gaps, leaving short-term margin risk.

Capital and logistics intensity

Bulk chemicals demand heavy capex for plants, storage and handling — Kemira reported revenues of about €3.0bn in 2023, reflecting scale but also capital intensity. Hazardous materials force strict transport, permitting and safety costs that raise operating complexity. High working capital ties cash in inventory and receivables, while optimizing logistics across dispersed customer sites remains technically and economically complex.

Product commoditization risk

Product commoditization exposes Kemira to intense price competition in many water-treatment chemistries. Low-cost producers, especially from Asia, can squeeze margins on standardized SKUs. Differentiation hinges on service, performance data and integrated solutions, so continuous innovation and R&D are required to avoid price erosion; global market ~USD 42B (2023), ~5% CAGR.

- Price pressure from low-cost producers

- Standardized SKUs compress margins

- Need for service/data-driven differentiation

- Ongoing R&D spend required to protect pricing

Limited diversification beyond core

Kemira’s focus on water-intensive end-markets concentrates sector-specific risk: net sales were about EUR 2.0bn in 2024 while a large share of revenue derives from pulp & paper and water-treatment segments, exposing the company to cyclical demand swings. Limited exposure to high-growth adjacencies constrains topline optionality, and a geographic mix with roughly half of sales in mature European markets limits upside versus peers. Portfolio breadth remains narrower than diversified global chemical competitors, reducing resilience.

- Concentration: high reliance on water-intensive verticals

- Growth limits: smaller presence in fast-growing adjacencies

- Geography: ~50% revenue from mature Europe

- Peer gap: narrower product portfolio vs global chemical peers

Cyclical chemicals: energy shocks, margin volatility and low-cost Asian pressure

Kemira is cyclical—volumes and pricing swing with pulp & paper and oil & gas cycles, amplifying margin volatility and working-capital strain. Energy and raw-material price exposure (TTF spiked >€300/MWh in 2022) compresses margins when pass-through lags. Capital intensity and product commoditization (global water-chemicals ~USD 42B in 2023, ~5% CAGR) limit pricing power versus low-cost Asian competitors.

| Metric | Value |

|---|---|

| Revenue (2023) | ≈€3.0bn |

| Net sales (2024) | ≈€2.0bn |

| Europe share | ≈50% |

Preview the Actual Deliverable

Kemira SWOT Analysis

This is the actual Kemira SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the final report; buy to unlock the complete, editable version.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Kemira's SWOT highlights strong specialty-chemicals expertise and sustainability leadership, countered by cyclical demand and raw-material sensitivity; opportunities include growing water-treatment and circular-economy demand while competition and input volatility are key threats. Discover the full, editable SWOT report—detailed insights, financial context, and Excel tools—to inform strategy, pitches, and investment decisions.

Strengths

Deep water-treatment expertise

Over a century of water-chemistry specialization gives Kemira deep application know-how across coagulation, flocculation and sludge treatment, translating into measurable improvements in quality and throughput for industrial and municipal clients. Its technologies and embedded formulations create high switching costs, reinforced by process integration and field-tested blends used across 40+ countries. Local technical-service teams drive stickiness and upselling through pilots, troubleshooting and dose-optimization support.

Strong position in pulp & paper

Kemira is a partner of choice for retention aids, sizing, bleaching and strength chemicals in pulp and paper, offering integrated solutions that boost fiber yield, machine runnability and end-product properties. Close mill-level collaboration enables continuous optimization and cross-selling across chemical portfolios. Demand is underpinned by resilient tissue and packaging end-markets supporting stable volumes and recurring sales.

Broad, resilient portfolio

Exposure to municipal and industrial water, pulp & paper and energy markets diversifies Kemira’s revenue mix, with the company operating in over 100 countries and reporting net sales around EUR 2.5bn in 2024.

Countercyclical water-treatment volumes help offset softness in cyclical pulp & paper or energy segments, cushioning top-line swings.

A broad product suite enables tailored solutions across customer sizes and geographies, supporting margin stability through cycles.

Regulatory and sustainability alignment

- Regulatory-driven demand

- ESG-aligned product portfolio

- Compliance eases contracting

- Pricing power for premium chemistries

Global footprint and service model

Kemira’s global footprint—over 40 production sites and service centers serving 100+ countries—pairs manufacturing, supply and on-site technical support to secure reliable delivery and shorter lead times for bulky chemicals; 2024 net sales were around EUR 3.0bn, underlining scale. Application labs and pilot projects speed customer value realization, while proximity enables rapid problem-solving and long-term relationships.

- Manufacturing: 40+ sites

- Reach: 100+ countries

- Scale: ~EUR 3.0bn 2024 sales

- Benefits: reduced logistics risk, faster pilots, stronger customer ties

Global water-chemistry platform: 100+ countries, 40+ sites, ~EUR 3.0bn, stable municipal demand

Kemira’s 100+ country reach and 40+ production sites underpin reliable supply and local technical service, driving customer stickiness and upsell. Deep water-chemistry expertise and integrated formulations create high switching costs and regulatory-aligned demand that supports premium pricing. 2024 net sales ~EUR 3.0bn; countercyclical municipal water volumes stabilize revenue versus pulp & paper cycles.

| Metric | Value |

|---|---|

| 2024 net sales | ~EUR 3.0bn |

| Countries | 100+ |

| Production sites | 40+ |

| Core markets | Water, pulp & paper, energy |

What is included in the product

Provides a focused SWOT analysis of Kemira, highlighting its operational strengths and sustainability-driven opportunities alongside internal weaknesses and market threats that will shape the company’s future competitiveness.

Delivers a concise Kemira SWOT matrix for rapid strategic alignment, ideal for executives needing a clear snapshot of competitive positioning, risks, and actionable priorities.

Weaknesses

End-market cyclicality

Volumes and pricing at Kemira are highly sensitive to pulp & paper and oil & gas cycles, so mill downtime, destocking or E&P budget cuts can quickly depress demand. Fixed-cost absorption tightens margins during downturns, amplifying profit volatility. Rapid customer run-rate changes make short-term forecasting and inventory planning notably harder, increasing working-capital strain.

Raw material and energy exposure

Raw material and energy exposure: prices for monomers, caustic and acids and power are volatile—European TTF gas spiked above €300/MWh in 2022 and industrial energy costs remained elevated into 2023–24, compressing margins when pass-through lags. Regional energy shocks weaken European cost competitiveness. Hedging and surcharge mechanisms only partially close timing gaps, leaving short-term margin risk.

Capital and logistics intensity

Bulk chemicals demand heavy capex for plants, storage and handling — Kemira reported revenues of about €3.0bn in 2023, reflecting scale but also capital intensity. Hazardous materials force strict transport, permitting and safety costs that raise operating complexity. High working capital ties cash in inventory and receivables, while optimizing logistics across dispersed customer sites remains technically and economically complex.

Product commoditization risk

Product commoditization exposes Kemira to intense price competition in many water-treatment chemistries. Low-cost producers, especially from Asia, can squeeze margins on standardized SKUs. Differentiation hinges on service, performance data and integrated solutions, so continuous innovation and R&D are required to avoid price erosion; global market ~USD 42B (2023), ~5% CAGR.

- Price pressure from low-cost producers

- Standardized SKUs compress margins

- Need for service/data-driven differentiation

- Ongoing R&D spend required to protect pricing

Limited diversification beyond core

Kemira’s focus on water-intensive end-markets concentrates sector-specific risk: net sales were about EUR 2.0bn in 2024 while a large share of revenue derives from pulp & paper and water-treatment segments, exposing the company to cyclical demand swings. Limited exposure to high-growth adjacencies constrains topline optionality, and a geographic mix with roughly half of sales in mature European markets limits upside versus peers. Portfolio breadth remains narrower than diversified global chemical competitors, reducing resilience.

- Concentration: high reliance on water-intensive verticals

- Growth limits: smaller presence in fast-growing adjacencies

- Geography: ~50% revenue from mature Europe

- Peer gap: narrower product portfolio vs global chemical peers

Cyclical chemicals: energy shocks, margin volatility and low-cost Asian pressure

Kemira is cyclical—volumes and pricing swing with pulp & paper and oil & gas cycles, amplifying margin volatility and working-capital strain. Energy and raw-material price exposure (TTF spiked >€300/MWh in 2022) compresses margins when pass-through lags. Capital intensity and product commoditization (global water-chemicals ~USD 42B in 2023, ~5% CAGR) limit pricing power versus low-cost Asian competitors.

| Metric | Value |

|---|---|

| Revenue (2023) | ≈€3.0bn |

| Net sales (2024) | ≈€2.0bn |

| Europe share | ≈50% |

Preview the Actual Deliverable

Kemira SWOT Analysis

This is the actual Kemira SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the final report; buy to unlock the complete, editable version.