Kendrion Porter's Five Forces Analysis

From Overview to Strategy Blueprint

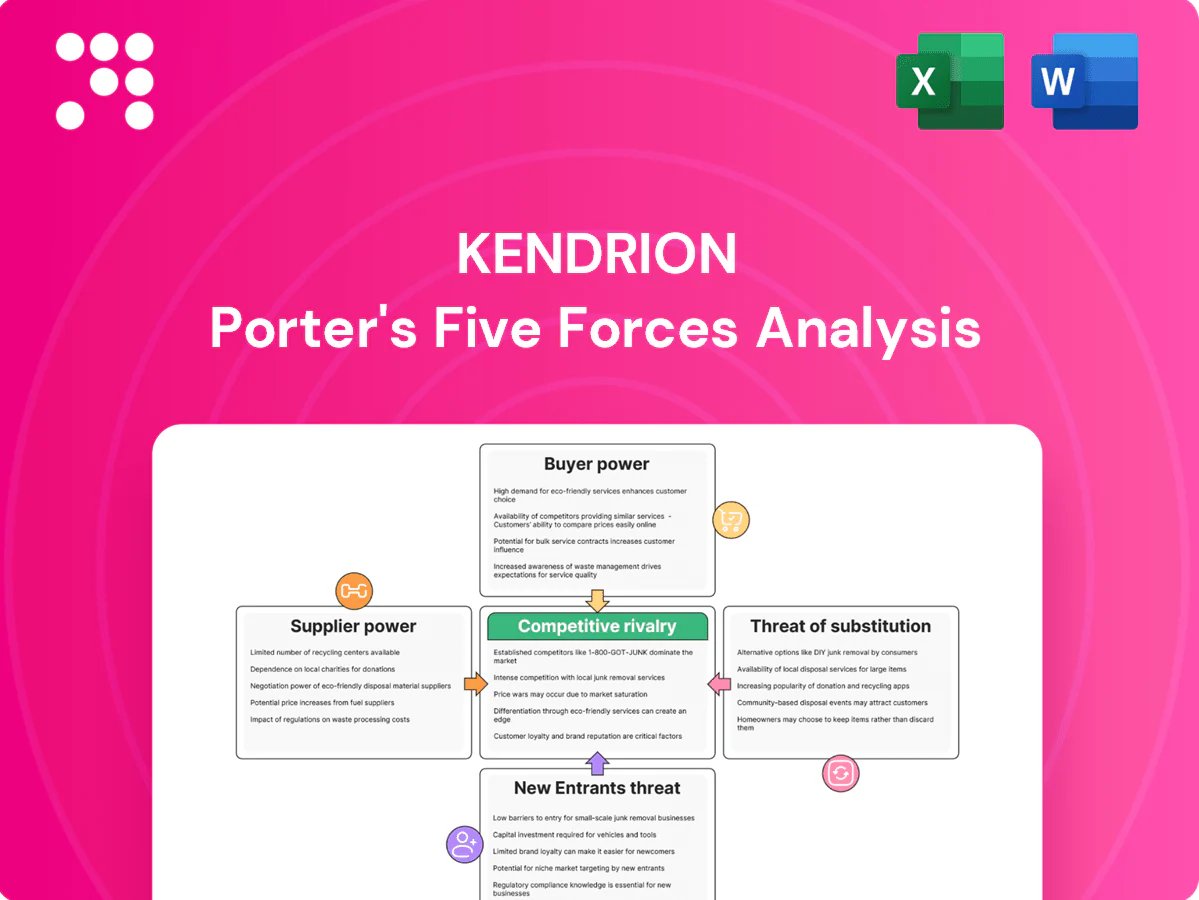

Kendrion’s Porter's Five Forces preview highlights supplier leverage, buyer power, rivalry intensity, threat of substitutes, and barriers to entry, showing where strategic pressure points lie. This snapshot identifies key competitive risks and growth levers for the supplier‑centric electromagnetics niche. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kendrion’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized materials dependency

Dependence on rare-earth magnets, precision steels and copper gives select suppliers leverage; China accounted for about 60% of global rare-earth oxide production in 2024. Limited global sources and price volatility have periodically compressed margins. Long-term supply contracts and commodity hedging partially mitigate exposure. Qualification of alternate suppliers and materials typically requires many months to years.

Custom components and tooling

Engineered-to-order coils, rotors and housings raise supplier stickiness by embedding unique specs and tooling into production, creating significant switching frictions; tooling amortization and qualified tooling specs often lock buyers to vendors. Dual-tooling and modular component designs can materially reduce single-supplier dependence, while systematic vendor development programs and shared engineering timelines rebalance supplier power.

Semiconductor and electronics supply

Controls require chips, sensors and power electronics that faced cyclical shortages, with average semiconductor lead times around 18 weeks in 2024, elevating allocation risk and supplier power in tight markets.

Strategic inventory (safety stock covering 3–6 months of demand) and second-source designs materially reduce exposure, while closer forecasts and vendor-managed inventory (VMI) have cut emergency buys by up to 20% in analogous OEMs.

Geographic concentration and logistics

Compliance and sustainability demands

Automotive and medical end-markets demand IATF/ISO quality and rising ESG compliance, elevating supplier entry barriers and bargaining power. In 2024 CSRD extended formal ESG reporting to roughly 50,000 EU firms, concentrating the pool of certified vendors. Kendrion and OEMs use audits, scorecards and joint sustainability roadmaps to enforce terms and align incentives.

- IATF/ISO + ESG prerequisites raise supplier influence

- CSRD 2024: ~50,000 EU firms now in ESG reporting scope

- Audits and scorecards enforce compliance

- Collaborative sustainability roadmaps align incentives

Supply squeeze: rare-earths ~60%, chips lead time ~18w

Supplier power is elevated by concentration in rare-earths (China ~60% of oxide production in 2024) and semiconductors (avg lead times ~18 weeks in 2024), compressing margins. Engineered, tool-locked components and IATF/ISO + ESG requisites (CSRD ~50,000 EU firms in scope 2024) increase stickiness. Mitigants: 3–6 months safety stock, nearshoring, dual-sourcing and VMI.

| Metric | 2024 Value |

|---|---|

| Rare-earth share (China) | ~60% |

| Semiconductor lead time | ~18 weeks |

| Safety stock | 3–6 months |

| CSRD scope (EU) | ~50,000 firms |

What is included in the product

Tailored Five Forces analysis for Kendrion that uncovers competitive intensity, supplier and buyer leverage, threat of substitutes and new entrants, and highlights disruptive risks and strategic levers to protect margins and market share.

A compact Kendrion Porter's Five Forces one-sheet highlighting supplier, buyer, competitor, entrant and substitute pressures—ideal for quick strategic decisions, board slides and swapping in your own data to reflect evolving market conditions.

Customers Bargaining Power

Large OEM and Tier-1 concentration

Large automotive, industrial automation and medical OEMs buy at scale and can negotiate aggressively; the top 10 OEMs accounted for roughly half of global light-vehicle production in 2024, concentrating purchasing power. Their volume, certification control and multi-year framework agreements compress pricing and terms, often squeezing supplier margins. Deep technical relationships and qualification cycles limit churn risk despite tight margins.

High switching costs from design-in

Once Kendrion brakes and controls are design-in validated, requalification typically exceeds 12 months and can incur costs in the hundreds of thousands of euros, making post-award buyer renegotiation difficult. This stickiness materially reduces buyer power after contract award, while pre-award buyers still extract leverage through competitive bidding. Lifecycle service agreements and spare parts sales further lock customers in, supporting recurring revenue and raising effective switching costs.

Customization reduces comparability

Engineered solutions reduce apples-to-apples price comparisons as bespoke Kendrion modules emphasize performance specs and integration support, shifting buyer focus from unit price to total system value. This differentiation tempers pure price pressure and enables value-in-use selling, which Kendrion highlighted in 2024 as central to customer retention and margin protection. As a result, procurement decisions weigh lifecycle performance and integration services alongside upfront cost.

Cyclical demand and budget scrutiny

Cyclical auto and industrial swings drive volume volatility for Kendrion, with global light-vehicle production estimated at 79.5 million units in 2024 (OICA), amplifying buyer pressure in downturns. In weak phases customers commonly push for price concessions and extended payment terms, compressing margins. Kendrion defends margins via flexible capacity, variable cost structures and diversified end-markets that smooth demand swings.

- Volume volatility: auto cycles (79.5m vehicles, 2024)

- Buyer leverage: price cuts and longer terms in downturns

- Defense: flexible capacity, variable costs

- Diversification: industrial end-markets smooth swings

Quality, delivery, and support expectations

- OTIF: >95–98%

- PPAP: level 3/4

- Zero-defect: mandatory for safety parts

- Digital monitoring: reduces inspection disputes

Top10 OEMs ≈50%, 95–98% OTIF shift buying to system value

Large OEMs concentrate purchasing (top 10 ≈50%) and exert strong pre-award leverage via volume and framework contracts, but post-award switching costs—requalification >12 months and high validation costs—reduce buyer power. Kendrion’s engineered differentiation, OTIF 95–98% and lifecycle service contracts shift decisions from price to total system value, softening pure price pressure.

| Metric | 2024 |

|---|---|

| Global light-vehicle production | 79.5m |

| Top10 OEM share | ≈50% |

| OTIF requirement | 95–98% |

| Requalification time | >12 months |

Same Document Delivered

Kendrion Porter's Five Forces Analysis

This preview shows the exact Kendrion Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the full, professionally written analysis, fully formatted and ready to download. Once you buy, you'll get instant access to this same file for immediate use.

From Overview to Strategy Blueprint

Kendrion’s Porter's Five Forces preview highlights supplier leverage, buyer power, rivalry intensity, threat of substitutes, and barriers to entry, showing where strategic pressure points lie. This snapshot identifies key competitive risks and growth levers for the supplier‑centric electromagnetics niche. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kendrion’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized materials dependency

Dependence on rare-earth magnets, precision steels and copper gives select suppliers leverage; China accounted for about 60% of global rare-earth oxide production in 2024. Limited global sources and price volatility have periodically compressed margins. Long-term supply contracts and commodity hedging partially mitigate exposure. Qualification of alternate suppliers and materials typically requires many months to years.

Custom components and tooling

Engineered-to-order coils, rotors and housings raise supplier stickiness by embedding unique specs and tooling into production, creating significant switching frictions; tooling amortization and qualified tooling specs often lock buyers to vendors. Dual-tooling and modular component designs can materially reduce single-supplier dependence, while systematic vendor development programs and shared engineering timelines rebalance supplier power.

Semiconductor and electronics supply

Controls require chips, sensors and power electronics that faced cyclical shortages, with average semiconductor lead times around 18 weeks in 2024, elevating allocation risk and supplier power in tight markets.

Strategic inventory (safety stock covering 3–6 months of demand) and second-source designs materially reduce exposure, while closer forecasts and vendor-managed inventory (VMI) have cut emergency buys by up to 20% in analogous OEMs.

Geographic concentration and logistics

Compliance and sustainability demands

Automotive and medical end-markets demand IATF/ISO quality and rising ESG compliance, elevating supplier entry barriers and bargaining power. In 2024 CSRD extended formal ESG reporting to roughly 50,000 EU firms, concentrating the pool of certified vendors. Kendrion and OEMs use audits, scorecards and joint sustainability roadmaps to enforce terms and align incentives.

- IATF/ISO + ESG prerequisites raise supplier influence

- CSRD 2024: ~50,000 EU firms now in ESG reporting scope

- Audits and scorecards enforce compliance

- Collaborative sustainability roadmaps align incentives

Supply squeeze: rare-earths ~60%, chips lead time ~18w

Supplier power is elevated by concentration in rare-earths (China ~60% of oxide production in 2024) and semiconductors (avg lead times ~18 weeks in 2024), compressing margins. Engineered, tool-locked components and IATF/ISO + ESG requisites (CSRD ~50,000 EU firms in scope 2024) increase stickiness. Mitigants: 3–6 months safety stock, nearshoring, dual-sourcing and VMI.

| Metric | 2024 Value |

|---|---|

| Rare-earth share (China) | ~60% |

| Semiconductor lead time | ~18 weeks |

| Safety stock | 3–6 months |

| CSRD scope (EU) | ~50,000 firms |

What is included in the product

Tailored Five Forces analysis for Kendrion that uncovers competitive intensity, supplier and buyer leverage, threat of substitutes and new entrants, and highlights disruptive risks and strategic levers to protect margins and market share.

A compact Kendrion Porter's Five Forces one-sheet highlighting supplier, buyer, competitor, entrant and substitute pressures—ideal for quick strategic decisions, board slides and swapping in your own data to reflect evolving market conditions.

Customers Bargaining Power

Large OEM and Tier-1 concentration

Large automotive, industrial automation and medical OEMs buy at scale and can negotiate aggressively; the top 10 OEMs accounted for roughly half of global light-vehicle production in 2024, concentrating purchasing power. Their volume, certification control and multi-year framework agreements compress pricing and terms, often squeezing supplier margins. Deep technical relationships and qualification cycles limit churn risk despite tight margins.

High switching costs from design-in

Once Kendrion brakes and controls are design-in validated, requalification typically exceeds 12 months and can incur costs in the hundreds of thousands of euros, making post-award buyer renegotiation difficult. This stickiness materially reduces buyer power after contract award, while pre-award buyers still extract leverage through competitive bidding. Lifecycle service agreements and spare parts sales further lock customers in, supporting recurring revenue and raising effective switching costs.

Customization reduces comparability

Engineered solutions reduce apples-to-apples price comparisons as bespoke Kendrion modules emphasize performance specs and integration support, shifting buyer focus from unit price to total system value. This differentiation tempers pure price pressure and enables value-in-use selling, which Kendrion highlighted in 2024 as central to customer retention and margin protection. As a result, procurement decisions weigh lifecycle performance and integration services alongside upfront cost.

Cyclical demand and budget scrutiny

Cyclical auto and industrial swings drive volume volatility for Kendrion, with global light-vehicle production estimated at 79.5 million units in 2024 (OICA), amplifying buyer pressure in downturns. In weak phases customers commonly push for price concessions and extended payment terms, compressing margins. Kendrion defends margins via flexible capacity, variable cost structures and diversified end-markets that smooth demand swings.

- Volume volatility: auto cycles (79.5m vehicles, 2024)

- Buyer leverage: price cuts and longer terms in downturns

- Defense: flexible capacity, variable costs

- Diversification: industrial end-markets smooth swings

Quality, delivery, and support expectations

- OTIF: >95–98%

- PPAP: level 3/4

- Zero-defect: mandatory for safety parts

- Digital monitoring: reduces inspection disputes

Top10 OEMs ≈50%, 95–98% OTIF shift buying to system value

Large OEMs concentrate purchasing (top 10 ≈50%) and exert strong pre-award leverage via volume and framework contracts, but post-award switching costs—requalification >12 months and high validation costs—reduce buyer power. Kendrion’s engineered differentiation, OTIF 95–98% and lifecycle service contracts shift decisions from price to total system value, softening pure price pressure.

| Metric | 2024 |

|---|---|

| Global light-vehicle production | 79.5m |

| Top10 OEM share | ≈50% |

| OTIF requirement | 95–98% |

| Requalification time | >12 months |

Same Document Delivered

Kendrion Porter's Five Forces Analysis

This preview shows the exact Kendrion Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the full, professionally written analysis, fully formatted and ready to download. Once you buy, you'll get instant access to this same file for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Kendrion’s Porter's Five Forces preview highlights supplier leverage, buyer power, rivalry intensity, threat of substitutes, and barriers to entry, showing where strategic pressure points lie. This snapshot identifies key competitive risks and growth levers for the supplier‑centric electromagnetics niche. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kendrion’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized materials dependency

Dependence on rare-earth magnets, precision steels and copper gives select suppliers leverage; China accounted for about 60% of global rare-earth oxide production in 2024. Limited global sources and price volatility have periodically compressed margins. Long-term supply contracts and commodity hedging partially mitigate exposure. Qualification of alternate suppliers and materials typically requires many months to years.

Custom components and tooling

Engineered-to-order coils, rotors and housings raise supplier stickiness by embedding unique specs and tooling into production, creating significant switching frictions; tooling amortization and qualified tooling specs often lock buyers to vendors. Dual-tooling and modular component designs can materially reduce single-supplier dependence, while systematic vendor development programs and shared engineering timelines rebalance supplier power.

Semiconductor and electronics supply

Controls require chips, sensors and power electronics that faced cyclical shortages, with average semiconductor lead times around 18 weeks in 2024, elevating allocation risk and supplier power in tight markets.

Strategic inventory (safety stock covering 3–6 months of demand) and second-source designs materially reduce exposure, while closer forecasts and vendor-managed inventory (VMI) have cut emergency buys by up to 20% in analogous OEMs.

Geographic concentration and logistics

Compliance and sustainability demands

Automotive and medical end-markets demand IATF/ISO quality and rising ESG compliance, elevating supplier entry barriers and bargaining power. In 2024 CSRD extended formal ESG reporting to roughly 50,000 EU firms, concentrating the pool of certified vendors. Kendrion and OEMs use audits, scorecards and joint sustainability roadmaps to enforce terms and align incentives.

- IATF/ISO + ESG prerequisites raise supplier influence

- CSRD 2024: ~50,000 EU firms now in ESG reporting scope

- Audits and scorecards enforce compliance

- Collaborative sustainability roadmaps align incentives

Supply squeeze: rare-earths ~60%, chips lead time ~18w

Supplier power is elevated by concentration in rare-earths (China ~60% of oxide production in 2024) and semiconductors (avg lead times ~18 weeks in 2024), compressing margins. Engineered, tool-locked components and IATF/ISO + ESG requisites (CSRD ~50,000 EU firms in scope 2024) increase stickiness. Mitigants: 3–6 months safety stock, nearshoring, dual-sourcing and VMI.

| Metric | 2024 Value |

|---|---|

| Rare-earth share (China) | ~60% |

| Semiconductor lead time | ~18 weeks |

| Safety stock | 3–6 months |

| CSRD scope (EU) | ~50,000 firms |

What is included in the product

Tailored Five Forces analysis for Kendrion that uncovers competitive intensity, supplier and buyer leverage, threat of substitutes and new entrants, and highlights disruptive risks and strategic levers to protect margins and market share.

A compact Kendrion Porter's Five Forces one-sheet highlighting supplier, buyer, competitor, entrant and substitute pressures—ideal for quick strategic decisions, board slides and swapping in your own data to reflect evolving market conditions.

Customers Bargaining Power

Large OEM and Tier-1 concentration

Large automotive, industrial automation and medical OEMs buy at scale and can negotiate aggressively; the top 10 OEMs accounted for roughly half of global light-vehicle production in 2024, concentrating purchasing power. Their volume, certification control and multi-year framework agreements compress pricing and terms, often squeezing supplier margins. Deep technical relationships and qualification cycles limit churn risk despite tight margins.

High switching costs from design-in

Once Kendrion brakes and controls are design-in validated, requalification typically exceeds 12 months and can incur costs in the hundreds of thousands of euros, making post-award buyer renegotiation difficult. This stickiness materially reduces buyer power after contract award, while pre-award buyers still extract leverage through competitive bidding. Lifecycle service agreements and spare parts sales further lock customers in, supporting recurring revenue and raising effective switching costs.

Customization reduces comparability

Engineered solutions reduce apples-to-apples price comparisons as bespoke Kendrion modules emphasize performance specs and integration support, shifting buyer focus from unit price to total system value. This differentiation tempers pure price pressure and enables value-in-use selling, which Kendrion highlighted in 2024 as central to customer retention and margin protection. As a result, procurement decisions weigh lifecycle performance and integration services alongside upfront cost.

Cyclical demand and budget scrutiny

Cyclical auto and industrial swings drive volume volatility for Kendrion, with global light-vehicle production estimated at 79.5 million units in 2024 (OICA), amplifying buyer pressure in downturns. In weak phases customers commonly push for price concessions and extended payment terms, compressing margins. Kendrion defends margins via flexible capacity, variable cost structures and diversified end-markets that smooth demand swings.

- Volume volatility: auto cycles (79.5m vehicles, 2024)

- Buyer leverage: price cuts and longer terms in downturns

- Defense: flexible capacity, variable costs

- Diversification: industrial end-markets smooth swings

Quality, delivery, and support expectations

- OTIF: >95–98%

- PPAP: level 3/4

- Zero-defect: mandatory for safety parts

- Digital monitoring: reduces inspection disputes

Top10 OEMs ≈50%, 95–98% OTIF shift buying to system value

Large OEMs concentrate purchasing (top 10 ≈50%) and exert strong pre-award leverage via volume and framework contracts, but post-award switching costs—requalification >12 months and high validation costs—reduce buyer power. Kendrion’s engineered differentiation, OTIF 95–98% and lifecycle service contracts shift decisions from price to total system value, softening pure price pressure.

| Metric | 2024 |

|---|---|

| Global light-vehicle production | 79.5m |

| Top10 OEM share | ≈50% |

| OTIF requirement | 95–98% |

| Requalification time | >12 months |

Same Document Delivered

Kendrion Porter's Five Forces Analysis

This preview shows the exact Kendrion Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the full, professionally written analysis, fully formatted and ready to download. Once you buy, you'll get instant access to this same file for immediate use.