Keppel Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

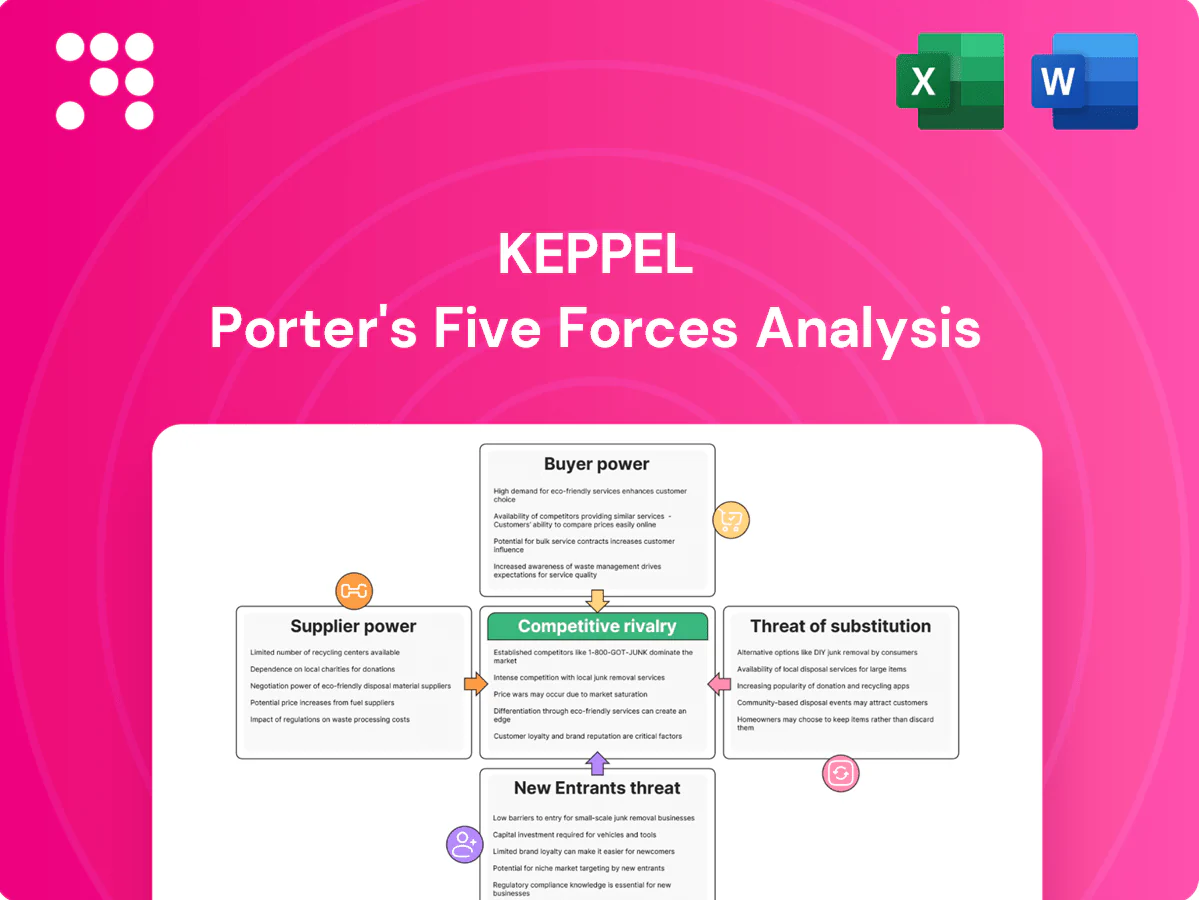

Keppel’s Porter's Five Forces snapshot highlights supplier and buyer power, competitive rivalry, substitutes, and entry threats shaping its port and maritime businesses. This concise view identifies strategic pressures and opportunities investors should watch. The full analysis unlocks force-by-force ratings, visuals, and actionable insight—get the complete report to inform decisions.

Suppliers Bargaining Power

Concentrated critical equipment

As of 2024 waste-to-energy boilers, grid-scale turbines and desalination modules are supplied mainly by a handful of global OEMs (GE, Siemens Energy, Mitsubishi Power; Valmet, Babcock & Wilcox; IDE, Acciona), giving suppliers strong leverage. Switching suppliers incurs lengthy qualification delays and performance risk. Keppel mitigates this via multi-vendor frameworks and long-term service agreements. Scale secures volume discounts but heavy customization can create supplier lock-in.

Specialized tech and IP

Process technology, digital infrastructure designs and control systems often rely on licensed IP and industry standards (eg SCADA/OT, 3GPP), creating supplier leverage. Proprietary data center and WtE specifications further tighten dependence, while co-development deals and adoption of open standards such as Open Compute and Open RAN reduce hold-up risk. Strong in-house engineering capability curbs one-way supplier power by enabling reverse integration and specification control.

Construction and EPC capacity

Tight regional EPC and skilled labor markets inflate costs and timelines, with mega-projects concentrating demand on a limited contractor pool and driving schedule risk; framework contracts and modularization are increasingly used to smooth volatility and lock rates, while diversified sourcing across geographies reduces exposure to single-market capacity shortages.

Energy and commodity inputs

Steel, cement, cable and semiconductor inputs show cyclical price swings (often up to 30%), but indexed contracts and financial hedges implemented by ports and EPC partners have cut realised volatility materially in 2024. Localising supply chains has reduced lead-time and logistics risk by 25–40% for major operators. Stricter sustainability criteria in 2024 shrank eligible supplier pools, tightening negotiation leverage for qualified vendors.

- Price swing up to 30%

- Lead-time/logistics cut 25–40%

- Smaller supplier pool via sustainability rules

Land and permitting gatekeepers

Land, grid interconnection and environmental approvals in 2024 remain controlled by governments and utilities, giving these suppliers high leverage through timelines and conditional permits; typical major-port permitting delays commonly extend 12–24 months. Early engagement and public–private partnerships reduce timing uncertainty, while a proven compliance track record accelerates approvals.

High supplier power: Top 6 OEMs, ±30% price swings, permits 12–24 months

Supplier power in 2024 is high: a handful of OEMs dominate WtE, turbines and desalination, price swings reach up to 30% and permitting delays run 12–24 months. Keppel mitigates via multi-vendor frameworks, long-term service agreements and in-house engineering; localization cut lead-times 25–40%.

| Factor | 2024 metric | Impact |

|---|---|---|

| OEM concentration | Top 6 global | High leverage |

| Price volatility | ±30% | Cost risk |

| Lead-time | -25–40% (localization) | Lowered risk |

| Permits | 12–24 months | Schedule risk |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and entry risks tailored to Keppel, identifying disruptive threats, substitutes, and strategic levers to protect market share.

A concise one-sheet Five Forces for Keppel Porter—instantly visualizes competitive pressure and strategic risks for quick board decisions. Swap in your own data, duplicate scenarios, and export to pitch decks without macros or finance expertise.

Customers Bargaining Power

Government and utility buyers

Government and utility buyers issue competitive tenders with strict KPIs, driving heavy emphasis on uptime and penalty clauses; in 2024 procurement frameworks tightened further in many markets. Their scale creates significant price pressure and enforceable performance penalties, while long-term offtake structures like PPAs and availability payments provide cashflow stability but lock margins. Political cycles in 2024 continued to re-prioritise terms and project selection, increasing regulatory and contract risk for operators.

Hyperscalers and carriers

Hyperscalers and carriers exert strong buyer power: the top three cloud providers held about 66% of the global cloud market in 2024, demanding 99.99% uptime and PUE targets near 1.1, enabling them to push aggressive price and SLA terms; multi-region footprints let providers bundle capacity but force concessions often in low-single-digit to mid-teens percent; green power sourcing is now a critical deal lever.

Industrial and commercial users

Industrial and commercial users exert strong bargaining power in behind-the-meter energy and urban solutions, with the global C&I BTM market valued at about USD 18.6 billion in 2024 and numerous alternative vendors available. Keppel defends value via tiered service tiers and outcomes-based pricing, while cross-selling integrated urban solutions raises switching costs and deepens customer ties. Performance guarantees transfer operational risk back to Keppel, limiting buyer leverage when guarantees are credible.

Price transparency in auctions

Price transparency in renewables and WtE auctions is compressing margins as clearing prices — in some 2024 tenders falling below 30 USD/MWh in parts of Asia and the Middle East — become public, while differentiation through lower LCOE, higher reliability and demonstrable ESG value cushions buyer power; data-rich developers improve bid accuracy, but overbidding risk demands disciplined capital allocation and strict bid caps.

- Price visibility: 2024 clears <30 USD/MWh in regions

- Differentiation: LCOE, reliability, ESG

- Data edge: better site and resource modeling

- Risk: overbidding → enforce capital discipline

Long contract tenors

Long-term port concessions (commonly 20–30 years) reduce churn but hardwire escalation formulas; buyers push indexation caps and step-downs to limit tariff escalation. Renegotiation risk rises in volatile markets as throughput swings; strong 2024 operational performance and service delivery bolster Keppel Ports' renewal leverage.

- Concession length: 20–30 years

- Buyer demands: indexation caps, step-downs

- Risk: renegotiation in downturns

- Mitigation: strong service delivery, KPIs

Buyers dominate: hyperscalers (~66%) demand 99.99% uptime; renewables <30 USD/MWh squeeze margins

Buyers wield strong power: govt tenders tighten KPIs and penalties, hyperscalers (top‑3 ~66% share) demand 99.99% uptime and push prices down. C&I BTM market ~USD18.6bn boosts switching options; long port concessions (20–30 yrs) limit churn but invite renegotiation in downturns. Renewables price visibility (some 2024 clears <30 USD/MWh) compresses margins while LCOE, reliability and ESG enable differentiation.

| Metric | 2024 value |

|---|---|

| Top‑3 cloud share | ~66% |

| C&I BTM market | USD18.6bn |

| Renewables auction clears | <30 USD/MWh |

| Port concession length | 20–30 yrs |

Full Version Awaits

Keppel Porter's Five Forces Analysis

This preview shows the exact Keppel Porter Five Forces analysis you'll receive after purchase—no placeholders or samples. The document is the professionally formatted, ready-to-use file covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with evidence-backed insights. You'll get instant access to this identical document once payment completes.

Go Beyond the Preview—Access the Full Strategic Report

Keppel’s Porter's Five Forces snapshot highlights supplier and buyer power, competitive rivalry, substitutes, and entry threats shaping its port and maritime businesses. This concise view identifies strategic pressures and opportunities investors should watch. The full analysis unlocks force-by-force ratings, visuals, and actionable insight—get the complete report to inform decisions.

Suppliers Bargaining Power

Concentrated critical equipment

As of 2024 waste-to-energy boilers, grid-scale turbines and desalination modules are supplied mainly by a handful of global OEMs (GE, Siemens Energy, Mitsubishi Power; Valmet, Babcock & Wilcox; IDE, Acciona), giving suppliers strong leverage. Switching suppliers incurs lengthy qualification delays and performance risk. Keppel mitigates this via multi-vendor frameworks and long-term service agreements. Scale secures volume discounts but heavy customization can create supplier lock-in.

Specialized tech and IP

Process technology, digital infrastructure designs and control systems often rely on licensed IP and industry standards (eg SCADA/OT, 3GPP), creating supplier leverage. Proprietary data center and WtE specifications further tighten dependence, while co-development deals and adoption of open standards such as Open Compute and Open RAN reduce hold-up risk. Strong in-house engineering capability curbs one-way supplier power by enabling reverse integration and specification control.

Construction and EPC capacity

Tight regional EPC and skilled labor markets inflate costs and timelines, with mega-projects concentrating demand on a limited contractor pool and driving schedule risk; framework contracts and modularization are increasingly used to smooth volatility and lock rates, while diversified sourcing across geographies reduces exposure to single-market capacity shortages.

Energy and commodity inputs

Steel, cement, cable and semiconductor inputs show cyclical price swings (often up to 30%), but indexed contracts and financial hedges implemented by ports and EPC partners have cut realised volatility materially in 2024. Localising supply chains has reduced lead-time and logistics risk by 25–40% for major operators. Stricter sustainability criteria in 2024 shrank eligible supplier pools, tightening negotiation leverage for qualified vendors.

- Price swing up to 30%

- Lead-time/logistics cut 25–40%

- Smaller supplier pool via sustainability rules

Land and permitting gatekeepers

Land, grid interconnection and environmental approvals in 2024 remain controlled by governments and utilities, giving these suppliers high leverage through timelines and conditional permits; typical major-port permitting delays commonly extend 12–24 months. Early engagement and public–private partnerships reduce timing uncertainty, while a proven compliance track record accelerates approvals.

High supplier power: Top 6 OEMs, ±30% price swings, permits 12–24 months

Supplier power in 2024 is high: a handful of OEMs dominate WtE, turbines and desalination, price swings reach up to 30% and permitting delays run 12–24 months. Keppel mitigates via multi-vendor frameworks, long-term service agreements and in-house engineering; localization cut lead-times 25–40%.

| Factor | 2024 metric | Impact |

|---|---|---|

| OEM concentration | Top 6 global | High leverage |

| Price volatility | ±30% | Cost risk |

| Lead-time | -25–40% (localization) | Lowered risk |

| Permits | 12–24 months | Schedule risk |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and entry risks tailored to Keppel, identifying disruptive threats, substitutes, and strategic levers to protect market share.

A concise one-sheet Five Forces for Keppel Porter—instantly visualizes competitive pressure and strategic risks for quick board decisions. Swap in your own data, duplicate scenarios, and export to pitch decks without macros or finance expertise.

Customers Bargaining Power

Government and utility buyers

Government and utility buyers issue competitive tenders with strict KPIs, driving heavy emphasis on uptime and penalty clauses; in 2024 procurement frameworks tightened further in many markets. Their scale creates significant price pressure and enforceable performance penalties, while long-term offtake structures like PPAs and availability payments provide cashflow stability but lock margins. Political cycles in 2024 continued to re-prioritise terms and project selection, increasing regulatory and contract risk for operators.

Hyperscalers and carriers

Hyperscalers and carriers exert strong buyer power: the top three cloud providers held about 66% of the global cloud market in 2024, demanding 99.99% uptime and PUE targets near 1.1, enabling them to push aggressive price and SLA terms; multi-region footprints let providers bundle capacity but force concessions often in low-single-digit to mid-teens percent; green power sourcing is now a critical deal lever.

Industrial and commercial users

Industrial and commercial users exert strong bargaining power in behind-the-meter energy and urban solutions, with the global C&I BTM market valued at about USD 18.6 billion in 2024 and numerous alternative vendors available. Keppel defends value via tiered service tiers and outcomes-based pricing, while cross-selling integrated urban solutions raises switching costs and deepens customer ties. Performance guarantees transfer operational risk back to Keppel, limiting buyer leverage when guarantees are credible.

Price transparency in auctions

Price transparency in renewables and WtE auctions is compressing margins as clearing prices — in some 2024 tenders falling below 30 USD/MWh in parts of Asia and the Middle East — become public, while differentiation through lower LCOE, higher reliability and demonstrable ESG value cushions buyer power; data-rich developers improve bid accuracy, but overbidding risk demands disciplined capital allocation and strict bid caps.

- Price visibility: 2024 clears <30 USD/MWh in regions

- Differentiation: LCOE, reliability, ESG

- Data edge: better site and resource modeling

- Risk: overbidding → enforce capital discipline

Long contract tenors

Long-term port concessions (commonly 20–30 years) reduce churn but hardwire escalation formulas; buyers push indexation caps and step-downs to limit tariff escalation. Renegotiation risk rises in volatile markets as throughput swings; strong 2024 operational performance and service delivery bolster Keppel Ports' renewal leverage.

- Concession length: 20–30 years

- Buyer demands: indexation caps, step-downs

- Risk: renegotiation in downturns

- Mitigation: strong service delivery, KPIs

Buyers dominate: hyperscalers (~66%) demand 99.99% uptime; renewables <30 USD/MWh squeeze margins

Buyers wield strong power: govt tenders tighten KPIs and penalties, hyperscalers (top‑3 ~66% share) demand 99.99% uptime and push prices down. C&I BTM market ~USD18.6bn boosts switching options; long port concessions (20–30 yrs) limit churn but invite renegotiation in downturns. Renewables price visibility (some 2024 clears <30 USD/MWh) compresses margins while LCOE, reliability and ESG enable differentiation.

| Metric | 2024 value |

|---|---|

| Top‑3 cloud share | ~66% |

| C&I BTM market | USD18.6bn |

| Renewables auction clears | <30 USD/MWh |

| Port concession length | 20–30 yrs |

Full Version Awaits

Keppel Porter's Five Forces Analysis

This preview shows the exact Keppel Porter Five Forces analysis you'll receive after purchase—no placeholders or samples. The document is the professionally formatted, ready-to-use file covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with evidence-backed insights. You'll get instant access to this identical document once payment completes.

Description

Go Beyond the Preview—Access the Full Strategic Report

Keppel’s Porter's Five Forces snapshot highlights supplier and buyer power, competitive rivalry, substitutes, and entry threats shaping its port and maritime businesses. This concise view identifies strategic pressures and opportunities investors should watch. The full analysis unlocks force-by-force ratings, visuals, and actionable insight—get the complete report to inform decisions.

Suppliers Bargaining Power

Concentrated critical equipment

As of 2024 waste-to-energy boilers, grid-scale turbines and desalination modules are supplied mainly by a handful of global OEMs (GE, Siemens Energy, Mitsubishi Power; Valmet, Babcock & Wilcox; IDE, Acciona), giving suppliers strong leverage. Switching suppliers incurs lengthy qualification delays and performance risk. Keppel mitigates this via multi-vendor frameworks and long-term service agreements. Scale secures volume discounts but heavy customization can create supplier lock-in.

Specialized tech and IP

Process technology, digital infrastructure designs and control systems often rely on licensed IP and industry standards (eg SCADA/OT, 3GPP), creating supplier leverage. Proprietary data center and WtE specifications further tighten dependence, while co-development deals and adoption of open standards such as Open Compute and Open RAN reduce hold-up risk. Strong in-house engineering capability curbs one-way supplier power by enabling reverse integration and specification control.

Construction and EPC capacity

Tight regional EPC and skilled labor markets inflate costs and timelines, with mega-projects concentrating demand on a limited contractor pool and driving schedule risk; framework contracts and modularization are increasingly used to smooth volatility and lock rates, while diversified sourcing across geographies reduces exposure to single-market capacity shortages.

Energy and commodity inputs

Steel, cement, cable and semiconductor inputs show cyclical price swings (often up to 30%), but indexed contracts and financial hedges implemented by ports and EPC partners have cut realised volatility materially in 2024. Localising supply chains has reduced lead-time and logistics risk by 25–40% for major operators. Stricter sustainability criteria in 2024 shrank eligible supplier pools, tightening negotiation leverage for qualified vendors.

- Price swing up to 30%

- Lead-time/logistics cut 25–40%

- Smaller supplier pool via sustainability rules

Land and permitting gatekeepers

Land, grid interconnection and environmental approvals in 2024 remain controlled by governments and utilities, giving these suppliers high leverage through timelines and conditional permits; typical major-port permitting delays commonly extend 12–24 months. Early engagement and public–private partnerships reduce timing uncertainty, while a proven compliance track record accelerates approvals.

High supplier power: Top 6 OEMs, ±30% price swings, permits 12–24 months

Supplier power in 2024 is high: a handful of OEMs dominate WtE, turbines and desalination, price swings reach up to 30% and permitting delays run 12–24 months. Keppel mitigates via multi-vendor frameworks, long-term service agreements and in-house engineering; localization cut lead-times 25–40%.

| Factor | 2024 metric | Impact |

|---|---|---|

| OEM concentration | Top 6 global | High leverage |

| Price volatility | ±30% | Cost risk |

| Lead-time | -25–40% (localization) | Lowered risk |

| Permits | 12–24 months | Schedule risk |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and entry risks tailored to Keppel, identifying disruptive threats, substitutes, and strategic levers to protect market share.

A concise one-sheet Five Forces for Keppel Porter—instantly visualizes competitive pressure and strategic risks for quick board decisions. Swap in your own data, duplicate scenarios, and export to pitch decks without macros or finance expertise.

Customers Bargaining Power

Government and utility buyers

Government and utility buyers issue competitive tenders with strict KPIs, driving heavy emphasis on uptime and penalty clauses; in 2024 procurement frameworks tightened further in many markets. Their scale creates significant price pressure and enforceable performance penalties, while long-term offtake structures like PPAs and availability payments provide cashflow stability but lock margins. Political cycles in 2024 continued to re-prioritise terms and project selection, increasing regulatory and contract risk for operators.

Hyperscalers and carriers

Hyperscalers and carriers exert strong buyer power: the top three cloud providers held about 66% of the global cloud market in 2024, demanding 99.99% uptime and PUE targets near 1.1, enabling them to push aggressive price and SLA terms; multi-region footprints let providers bundle capacity but force concessions often in low-single-digit to mid-teens percent; green power sourcing is now a critical deal lever.

Industrial and commercial users

Industrial and commercial users exert strong bargaining power in behind-the-meter energy and urban solutions, with the global C&I BTM market valued at about USD 18.6 billion in 2024 and numerous alternative vendors available. Keppel defends value via tiered service tiers and outcomes-based pricing, while cross-selling integrated urban solutions raises switching costs and deepens customer ties. Performance guarantees transfer operational risk back to Keppel, limiting buyer leverage when guarantees are credible.

Price transparency in auctions

Price transparency in renewables and WtE auctions is compressing margins as clearing prices — in some 2024 tenders falling below 30 USD/MWh in parts of Asia and the Middle East — become public, while differentiation through lower LCOE, higher reliability and demonstrable ESG value cushions buyer power; data-rich developers improve bid accuracy, but overbidding risk demands disciplined capital allocation and strict bid caps.

- Price visibility: 2024 clears <30 USD/MWh in regions

- Differentiation: LCOE, reliability, ESG

- Data edge: better site and resource modeling

- Risk: overbidding → enforce capital discipline

Long contract tenors

Long-term port concessions (commonly 20–30 years) reduce churn but hardwire escalation formulas; buyers push indexation caps and step-downs to limit tariff escalation. Renegotiation risk rises in volatile markets as throughput swings; strong 2024 operational performance and service delivery bolster Keppel Ports' renewal leverage.

- Concession length: 20–30 years

- Buyer demands: indexation caps, step-downs

- Risk: renegotiation in downturns

- Mitigation: strong service delivery, KPIs

Buyers dominate: hyperscalers (~66%) demand 99.99% uptime; renewables <30 USD/MWh squeeze margins

Buyers wield strong power: govt tenders tighten KPIs and penalties, hyperscalers (top‑3 ~66% share) demand 99.99% uptime and push prices down. C&I BTM market ~USD18.6bn boosts switching options; long port concessions (20–30 yrs) limit churn but invite renegotiation in downturns. Renewables price visibility (some 2024 clears <30 USD/MWh) compresses margins while LCOE, reliability and ESG enable differentiation.

| Metric | 2024 value |

|---|---|

| Top‑3 cloud share | ~66% |

| C&I BTM market | USD18.6bn |

| Renewables auction clears | <30 USD/MWh |

| Port concession length | 20–30 yrs |

Full Version Awaits

Keppel Porter's Five Forces Analysis

This preview shows the exact Keppel Porter Five Forces analysis you'll receive after purchase—no placeholders or samples. The document is the professionally formatted, ready-to-use file covering competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with evidence-backed insights. You'll get instant access to this identical document once payment completes.