Kering Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

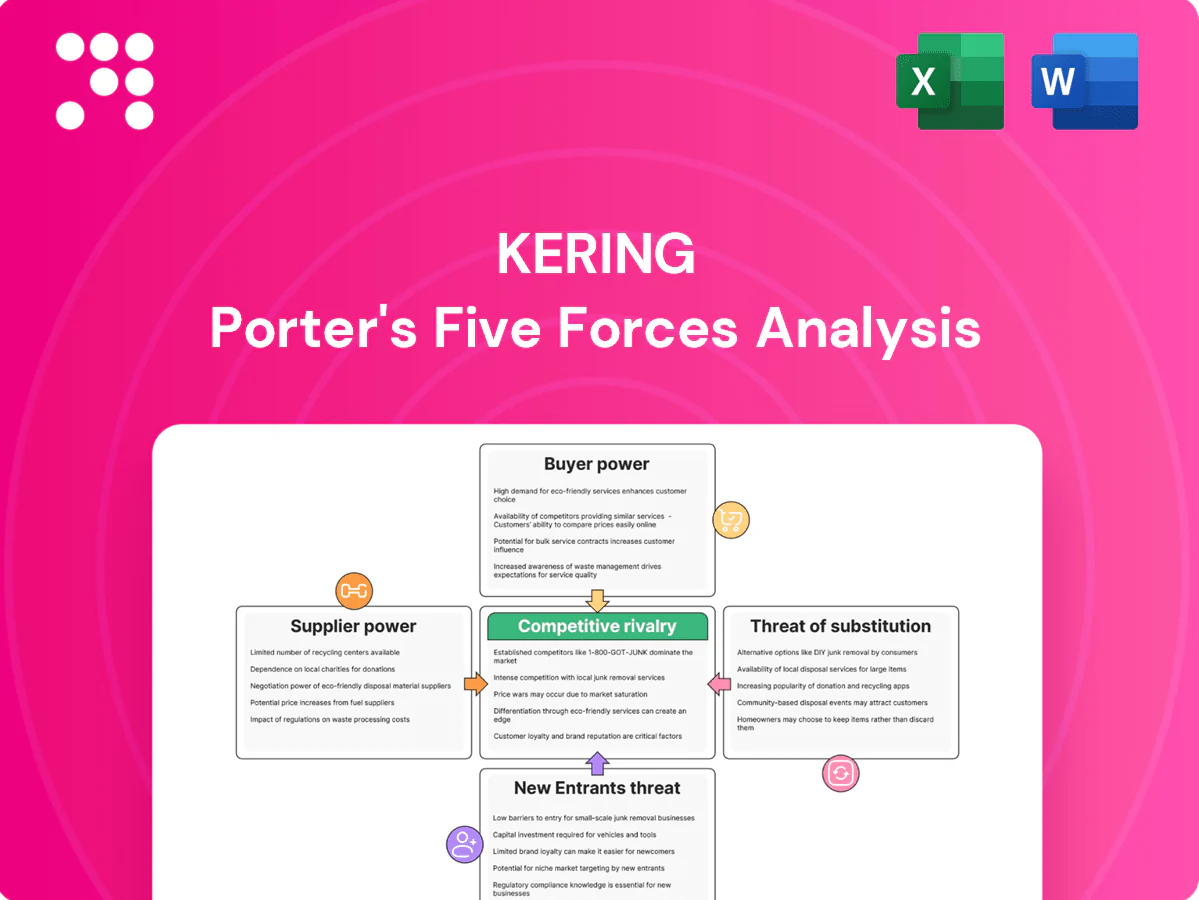

Kering enjoys strong brand power and high entry barriers, limiting new rivals, while buyer pressure is moderate and supplier influence is muted by scale; substitute threats persist from affordable luxury and fast-fashion. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kering’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Rare materials scarcity

High-grade leather, precious metals and gemstones remain finite and tightly controlled, giving upstream suppliers strong leverage; as of 2024 tightened ethical sourcing and traceability policies further narrow certified suppliers. Kering offsets risk through multi-sourcing and vertical integration and reports ongoing programs to increase traceability, yet scarcity sustains supplier power. Price volatility and rising certification costs continue to pressure margins.

Artisanal craftsmanship

Specialized ateliers and limited master craftsmen give suppliers high bargaining power for Kering, as switching adds time and cost; Bain 2024 notes the personal luxury goods market's scale increases pressure on scarce artisanal capacity. Capacity constraints in high-skill workshops create seasonal bottlenecks, while long-term partnerships and training raise dependency. Strict quality standards further shrink the eligible supplier pool.

Sustainability compliance

Strict ESG commitments limit Kering to suppliers meeting high environmental and social criteria, narrowing the pool and increasing bargaining power among certified vendors. Compliance costs and audits raise entry barriers, concentrating leverage with audited suppliers. Kering’s traceability push improves control but reduces alternatives; non-compliance risks reputational damage and supply disruption for a group with €18.4bn revenue (2023).

Brand-critical inputs

Signature hardware, premium fabrics and innovative materials form core brand codes that limit supplier substitution; Gucci accounted for about 60% of Kering group sales in 2024, concentrating the impact of any supply disruption. Co‑developed inputs embed supplier know‑how and long lead times for bespoke components raise switching costs, while IP and exclusivity clauses lower competitive risk but constrain operational flexibility.

- Signature hardware: low substitutability

- Co‑development: higher switching costs

- Lead times: extended dependency cycles

- IP/exclusivity: risk reduction vs operational constraints

Logistics concentration

Luxury house operations depend on timely, secure logistics and specialized finishing; in 2024 concentrated providers in key regions (Italy, France, Switzerland) can amplify supplier leverage when disruptions occur, as seen during regional strikes and port congestion.

Nearshoring and dual-sourcing reduce lead times and risk but do not eliminate niche craftsmanship and temperature-controlled transport dependencies; freight-rate volatility and episodic capacity constraints continue to boost upstream bargaining power.

- Logistics concentration: high

- Regional risk hotspots: Italy/France/Switzerland

- Mitigants: nearshoring, dual-sourcing (partial)

- Upstream pressure: freight volatility, capacity limits

Finite inputs and ESG rules boost supplier leverage; core label ~60%

Finite high‑grade inputs, scarce artisanal ateliers and strict 2024 ESG/traceability rules concentrate supplier leverage; Kering (group revenue €18.4bn in 2023) mitigates via multi‑sourcing, nearshoring and vertical programs, yet Gucci’s ~60% share of 2024 sales amplifies exposure. Freight volatility, certification costs and long lead times sustain upstream pricing power and switching costs.

| Metric | Value/Note |

|---|---|

| Group revenue (2023) | €18.4bn |

| Gucci share (2024) | ~60% of group sales |

| Source on artisanal capacity | Bain 2024: tight |

What is included in the product

Analyzes competitive rivalry, buyer and supplier power, threats from new entrants and substitutes for Kering, highlighting disruptive trends, pricing pressures and barriers that shape its luxury market position.

A concise one-sheet Porter's Five Forces for Kering—clarifying supplier, buyer, entrant, substitute, and rivalry pressures to speed strategic decision-making and boardroom briefing.

Customers Bargaining Power

Affluent but discerning

Affluent but discerning: High-net-worth clients are largely price-insensitive yet extremely quality-sensitive, shifting power as they demand exclusivity, sustainability and flawless service; the global personal luxury goods market reached about €360 billion in 2024, concentrating buying power among HNW segments. Negative experiences trigger swift switching to rival maisons—luxury churn rises sharply after one poor service event. Kering's brand equity (group revenue ~€20.5bn in 2024) tempers buyer power but raises service expectations.

Wholesale and retail mix

Direct-to-consumer expansion — over 1,000 directly operated boutiques in 2024 — reduces intermediary bargaining power, yet select department stores and e-tail partners still negotiate terms and returns. Wholesale partners continue to influence shelf space and seasonal buys, representing roughly 35% of distribution in 2024. Kering’s growing retail footprint improves margin control, while omnichannel data sharply enhances pricing and assortment decisions.

Digital transparency

Online communities and resale platforms fuel instant price and quality comparisons amid a resale market projected to reach $77bn by 2025, increasing pressure on Kering for consistent pricing and airtight authenticity guarantees. Customers expect seamless digital experiences and fast resolutions, often demanding responses within 24 hours. About 5bn social media users amplify voices, magnifying reputational risk from missteps.

Resale market options

Pre-owned luxury offers lower entry prices and greater liquidity—the global pre-owned luxury market was about $36 billion in 2024 (≈10% of the market), giving buyers clear alternatives and bargaining levers. Certified resale pathways often delay full-price purchases as consumers wait for authenticated stock. Kering’s partnerships and authentication initiatives aim to capture resale value and retain control, but resale still modestly increases buyer leverage.

- Market size: ~$36B in 2024 (≈10% of luxury)

- Buyer leverage: increased via lower-entry and liquidity

- Kering response: partnerships + authentication to capture value

- Effect: certified resale can defer full-price buys

Cultural and trend shifts

Rapid pivots from streetwear to quiet luxury or fine jewelry shift Kering’s customer bargaining power as culturally relevant, sustainable labels capture spending; Kering reported ~€20.1bn revenue in 2023, highlighting scale at stake if trends flip.

- Buyers reward cultural relevance & sustainability

- Slow response risks demand erosion

- Data-led merchandising cuts markdowns and anticipates preferences

Affluent buyers gain leverage as omnichannel, resale and boutiques reshape luxury market

Affluent buyers are quality- and service-driven, limiting price sensitivity while raising expectations; global luxury ≈€360bn and Kering rev ≈€20.5bn in 2024. Direct retail (>1,000 boutiques in 2024) reduces intermediary leverage but online/resale (pre-owned ≈$36bn in 2024) increases buyer alternatives and switching risk. Omnichannel data and authentication partially reclaim power but buyers retain growing leverage.

| Metric | 2024 | Implication |

|---|---|---|

| Global luxury | ≈€360bn | High buyer concentration |

| Kering revenue | ≈€20.5bn | Brand strength mitigates price pressure |

| Direct boutiques | >1,000 | Less intermediary power |

| Pre-owned market | ≈$36bn (~10%) | More buyer alternatives |

Preview Before You Purchase

Kering Porter's Five Forces Analysis

This preview shows the exact Kering Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The document presents a full assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, with conclusions tailored to Kering's luxury fashion context. Once you buy, you'll get instant access to this same professionally formatted file, ready to download and use.

Go Beyond the Preview—Access the Full Strategic Report

Kering enjoys strong brand power and high entry barriers, limiting new rivals, while buyer pressure is moderate and supplier influence is muted by scale; substitute threats persist from affordable luxury and fast-fashion. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kering’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Rare materials scarcity

High-grade leather, precious metals and gemstones remain finite and tightly controlled, giving upstream suppliers strong leverage; as of 2024 tightened ethical sourcing and traceability policies further narrow certified suppliers. Kering offsets risk through multi-sourcing and vertical integration and reports ongoing programs to increase traceability, yet scarcity sustains supplier power. Price volatility and rising certification costs continue to pressure margins.

Artisanal craftsmanship

Specialized ateliers and limited master craftsmen give suppliers high bargaining power for Kering, as switching adds time and cost; Bain 2024 notes the personal luxury goods market's scale increases pressure on scarce artisanal capacity. Capacity constraints in high-skill workshops create seasonal bottlenecks, while long-term partnerships and training raise dependency. Strict quality standards further shrink the eligible supplier pool.

Sustainability compliance

Strict ESG commitments limit Kering to suppliers meeting high environmental and social criteria, narrowing the pool and increasing bargaining power among certified vendors. Compliance costs and audits raise entry barriers, concentrating leverage with audited suppliers. Kering’s traceability push improves control but reduces alternatives; non-compliance risks reputational damage and supply disruption for a group with €18.4bn revenue (2023).

Brand-critical inputs

Signature hardware, premium fabrics and innovative materials form core brand codes that limit supplier substitution; Gucci accounted for about 60% of Kering group sales in 2024, concentrating the impact of any supply disruption. Co‑developed inputs embed supplier know‑how and long lead times for bespoke components raise switching costs, while IP and exclusivity clauses lower competitive risk but constrain operational flexibility.

- Signature hardware: low substitutability

- Co‑development: higher switching costs

- Lead times: extended dependency cycles

- IP/exclusivity: risk reduction vs operational constraints

Logistics concentration

Luxury house operations depend on timely, secure logistics and specialized finishing; in 2024 concentrated providers in key regions (Italy, France, Switzerland) can amplify supplier leverage when disruptions occur, as seen during regional strikes and port congestion.

Nearshoring and dual-sourcing reduce lead times and risk but do not eliminate niche craftsmanship and temperature-controlled transport dependencies; freight-rate volatility and episodic capacity constraints continue to boost upstream bargaining power.

- Logistics concentration: high

- Regional risk hotspots: Italy/France/Switzerland

- Mitigants: nearshoring, dual-sourcing (partial)

- Upstream pressure: freight volatility, capacity limits

Finite inputs and ESG rules boost supplier leverage; core label ~60%

Finite high‑grade inputs, scarce artisanal ateliers and strict 2024 ESG/traceability rules concentrate supplier leverage; Kering (group revenue €18.4bn in 2023) mitigates via multi‑sourcing, nearshoring and vertical programs, yet Gucci’s ~60% share of 2024 sales amplifies exposure. Freight volatility, certification costs and long lead times sustain upstream pricing power and switching costs.

| Metric | Value/Note |

|---|---|

| Group revenue (2023) | €18.4bn |

| Gucci share (2024) | ~60% of group sales |

| Source on artisanal capacity | Bain 2024: tight |

What is included in the product

Analyzes competitive rivalry, buyer and supplier power, threats from new entrants and substitutes for Kering, highlighting disruptive trends, pricing pressures and barriers that shape its luxury market position.

A concise one-sheet Porter's Five Forces for Kering—clarifying supplier, buyer, entrant, substitute, and rivalry pressures to speed strategic decision-making and boardroom briefing.

Customers Bargaining Power

Affluent but discerning

Affluent but discerning: High-net-worth clients are largely price-insensitive yet extremely quality-sensitive, shifting power as they demand exclusivity, sustainability and flawless service; the global personal luxury goods market reached about €360 billion in 2024, concentrating buying power among HNW segments. Negative experiences trigger swift switching to rival maisons—luxury churn rises sharply after one poor service event. Kering's brand equity (group revenue ~€20.5bn in 2024) tempers buyer power but raises service expectations.

Wholesale and retail mix

Direct-to-consumer expansion — over 1,000 directly operated boutiques in 2024 — reduces intermediary bargaining power, yet select department stores and e-tail partners still negotiate terms and returns. Wholesale partners continue to influence shelf space and seasonal buys, representing roughly 35% of distribution in 2024. Kering’s growing retail footprint improves margin control, while omnichannel data sharply enhances pricing and assortment decisions.

Digital transparency

Online communities and resale platforms fuel instant price and quality comparisons amid a resale market projected to reach $77bn by 2025, increasing pressure on Kering for consistent pricing and airtight authenticity guarantees. Customers expect seamless digital experiences and fast resolutions, often demanding responses within 24 hours. About 5bn social media users amplify voices, magnifying reputational risk from missteps.

Resale market options

Pre-owned luxury offers lower entry prices and greater liquidity—the global pre-owned luxury market was about $36 billion in 2024 (≈10% of the market), giving buyers clear alternatives and bargaining levers. Certified resale pathways often delay full-price purchases as consumers wait for authenticated stock. Kering’s partnerships and authentication initiatives aim to capture resale value and retain control, but resale still modestly increases buyer leverage.

- Market size: ~$36B in 2024 (≈10% of luxury)

- Buyer leverage: increased via lower-entry and liquidity

- Kering response: partnerships + authentication to capture value

- Effect: certified resale can defer full-price buys

Cultural and trend shifts

Rapid pivots from streetwear to quiet luxury or fine jewelry shift Kering’s customer bargaining power as culturally relevant, sustainable labels capture spending; Kering reported ~€20.1bn revenue in 2023, highlighting scale at stake if trends flip.

- Buyers reward cultural relevance & sustainability

- Slow response risks demand erosion

- Data-led merchandising cuts markdowns and anticipates preferences

Affluent buyers gain leverage as omnichannel, resale and boutiques reshape luxury market

Affluent buyers are quality- and service-driven, limiting price sensitivity while raising expectations; global luxury ≈€360bn and Kering rev ≈€20.5bn in 2024. Direct retail (>1,000 boutiques in 2024) reduces intermediary leverage but online/resale (pre-owned ≈$36bn in 2024) increases buyer alternatives and switching risk. Omnichannel data and authentication partially reclaim power but buyers retain growing leverage.

| Metric | 2024 | Implication |

|---|---|---|

| Global luxury | ≈€360bn | High buyer concentration |

| Kering revenue | ≈€20.5bn | Brand strength mitigates price pressure |

| Direct boutiques | >1,000 | Less intermediary power |

| Pre-owned market | ≈$36bn (~10%) | More buyer alternatives |

Preview Before You Purchase

Kering Porter's Five Forces Analysis

This preview shows the exact Kering Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The document presents a full assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, with conclusions tailored to Kering's luxury fashion context. Once you buy, you'll get instant access to this same professionally formatted file, ready to download and use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Kering enjoys strong brand power and high entry barriers, limiting new rivals, while buyer pressure is moderate and supplier influence is muted by scale; substitute threats persist from affordable luxury and fast-fashion. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kering’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Rare materials scarcity

High-grade leather, precious metals and gemstones remain finite and tightly controlled, giving upstream suppliers strong leverage; as of 2024 tightened ethical sourcing and traceability policies further narrow certified suppliers. Kering offsets risk through multi-sourcing and vertical integration and reports ongoing programs to increase traceability, yet scarcity sustains supplier power. Price volatility and rising certification costs continue to pressure margins.

Artisanal craftsmanship

Specialized ateliers and limited master craftsmen give suppliers high bargaining power for Kering, as switching adds time and cost; Bain 2024 notes the personal luxury goods market's scale increases pressure on scarce artisanal capacity. Capacity constraints in high-skill workshops create seasonal bottlenecks, while long-term partnerships and training raise dependency. Strict quality standards further shrink the eligible supplier pool.

Sustainability compliance

Strict ESG commitments limit Kering to suppliers meeting high environmental and social criteria, narrowing the pool and increasing bargaining power among certified vendors. Compliance costs and audits raise entry barriers, concentrating leverage with audited suppliers. Kering’s traceability push improves control but reduces alternatives; non-compliance risks reputational damage and supply disruption for a group with €18.4bn revenue (2023).

Brand-critical inputs

Signature hardware, premium fabrics and innovative materials form core brand codes that limit supplier substitution; Gucci accounted for about 60% of Kering group sales in 2024, concentrating the impact of any supply disruption. Co‑developed inputs embed supplier know‑how and long lead times for bespoke components raise switching costs, while IP and exclusivity clauses lower competitive risk but constrain operational flexibility.

- Signature hardware: low substitutability

- Co‑development: higher switching costs

- Lead times: extended dependency cycles

- IP/exclusivity: risk reduction vs operational constraints

Logistics concentration

Luxury house operations depend on timely, secure logistics and specialized finishing; in 2024 concentrated providers in key regions (Italy, France, Switzerland) can amplify supplier leverage when disruptions occur, as seen during regional strikes and port congestion.

Nearshoring and dual-sourcing reduce lead times and risk but do not eliminate niche craftsmanship and temperature-controlled transport dependencies; freight-rate volatility and episodic capacity constraints continue to boost upstream bargaining power.

- Logistics concentration: high

- Regional risk hotspots: Italy/France/Switzerland

- Mitigants: nearshoring, dual-sourcing (partial)

- Upstream pressure: freight volatility, capacity limits

Finite inputs and ESG rules boost supplier leverage; core label ~60%

Finite high‑grade inputs, scarce artisanal ateliers and strict 2024 ESG/traceability rules concentrate supplier leverage; Kering (group revenue €18.4bn in 2023) mitigates via multi‑sourcing, nearshoring and vertical programs, yet Gucci’s ~60% share of 2024 sales amplifies exposure. Freight volatility, certification costs and long lead times sustain upstream pricing power and switching costs.

| Metric | Value/Note |

|---|---|

| Group revenue (2023) | €18.4bn |

| Gucci share (2024) | ~60% of group sales |

| Source on artisanal capacity | Bain 2024: tight |

What is included in the product

Analyzes competitive rivalry, buyer and supplier power, threats from new entrants and substitutes for Kering, highlighting disruptive trends, pricing pressures and barriers that shape its luxury market position.

A concise one-sheet Porter's Five Forces for Kering—clarifying supplier, buyer, entrant, substitute, and rivalry pressures to speed strategic decision-making and boardroom briefing.

Customers Bargaining Power

Affluent but discerning

Affluent but discerning: High-net-worth clients are largely price-insensitive yet extremely quality-sensitive, shifting power as they demand exclusivity, sustainability and flawless service; the global personal luxury goods market reached about €360 billion in 2024, concentrating buying power among HNW segments. Negative experiences trigger swift switching to rival maisons—luxury churn rises sharply after one poor service event. Kering's brand equity (group revenue ~€20.5bn in 2024) tempers buyer power but raises service expectations.

Wholesale and retail mix

Direct-to-consumer expansion — over 1,000 directly operated boutiques in 2024 — reduces intermediary bargaining power, yet select department stores and e-tail partners still negotiate terms and returns. Wholesale partners continue to influence shelf space and seasonal buys, representing roughly 35% of distribution in 2024. Kering’s growing retail footprint improves margin control, while omnichannel data sharply enhances pricing and assortment decisions.

Digital transparency

Online communities and resale platforms fuel instant price and quality comparisons amid a resale market projected to reach $77bn by 2025, increasing pressure on Kering for consistent pricing and airtight authenticity guarantees. Customers expect seamless digital experiences and fast resolutions, often demanding responses within 24 hours. About 5bn social media users amplify voices, magnifying reputational risk from missteps.

Resale market options

Pre-owned luxury offers lower entry prices and greater liquidity—the global pre-owned luxury market was about $36 billion in 2024 (≈10% of the market), giving buyers clear alternatives and bargaining levers. Certified resale pathways often delay full-price purchases as consumers wait for authenticated stock. Kering’s partnerships and authentication initiatives aim to capture resale value and retain control, but resale still modestly increases buyer leverage.

- Market size: ~$36B in 2024 (≈10% of luxury)

- Buyer leverage: increased via lower-entry and liquidity

- Kering response: partnerships + authentication to capture value

- Effect: certified resale can defer full-price buys

Cultural and trend shifts

Rapid pivots from streetwear to quiet luxury or fine jewelry shift Kering’s customer bargaining power as culturally relevant, sustainable labels capture spending; Kering reported ~€20.1bn revenue in 2023, highlighting scale at stake if trends flip.

- Buyers reward cultural relevance & sustainability

- Slow response risks demand erosion

- Data-led merchandising cuts markdowns and anticipates preferences

Affluent buyers gain leverage as omnichannel, resale and boutiques reshape luxury market

Affluent buyers are quality- and service-driven, limiting price sensitivity while raising expectations; global luxury ≈€360bn and Kering rev ≈€20.5bn in 2024. Direct retail (>1,000 boutiques in 2024) reduces intermediary leverage but online/resale (pre-owned ≈$36bn in 2024) increases buyer alternatives and switching risk. Omnichannel data and authentication partially reclaim power but buyers retain growing leverage.

| Metric | 2024 | Implication |

|---|---|---|

| Global luxury | ≈€360bn | High buyer concentration |

| Kering revenue | ≈€20.5bn | Brand strength mitigates price pressure |

| Direct boutiques | >1,000 | Less intermediary power |

| Pre-owned market | ≈$36bn (~10%) | More buyer alternatives |

Preview Before You Purchase

Kering Porter's Five Forces Analysis

This preview shows the exact Kering Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The document presents a full assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, with conclusions tailored to Kering's luxury fashion context. Once you buy, you'll get instant access to this same professionally formatted file, ready to download and use.