Kerry Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

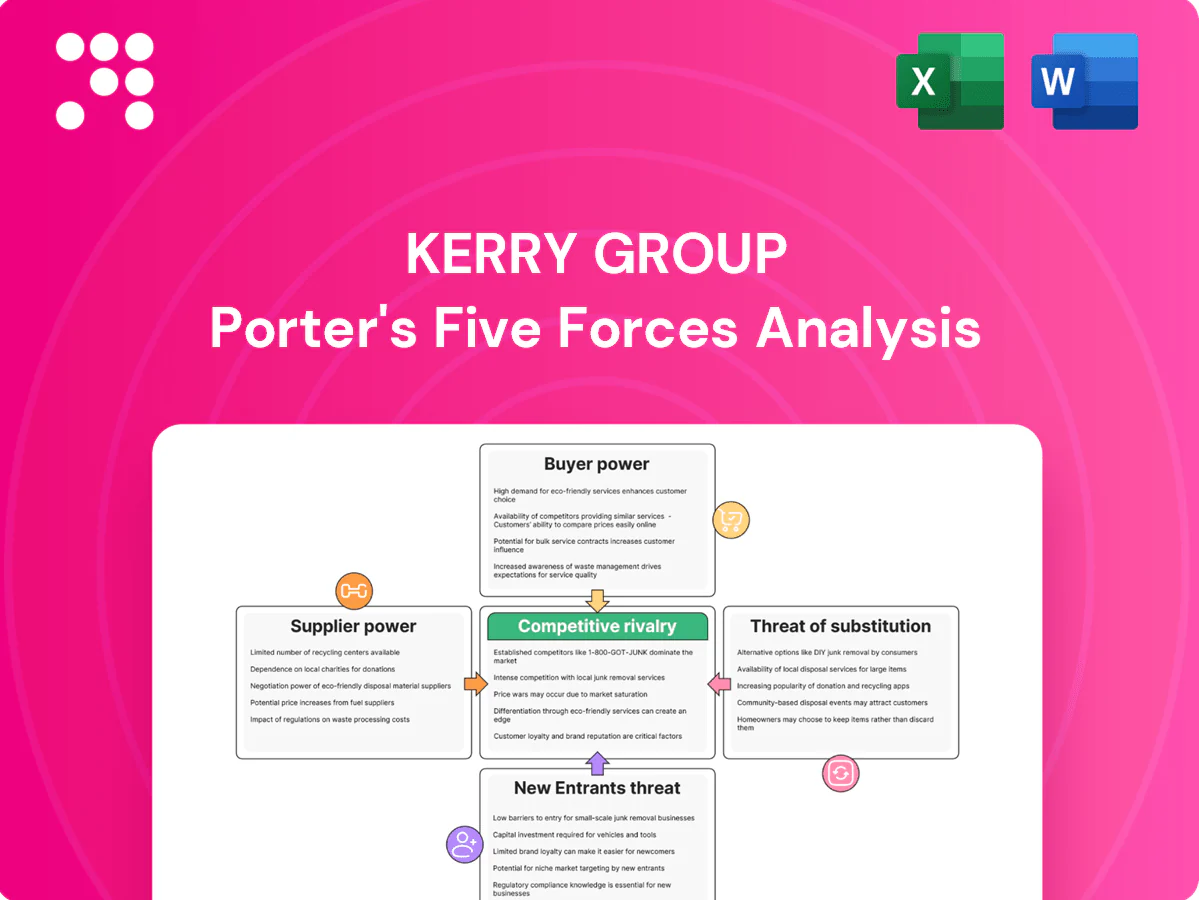

This snapshot highlights Kerry Group’s competitive pressures—supplier and buyer power, substitute threats, entry barriers and industry rivalry—showing where margins and growth may be challenged. Ready to go deeper? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals and actionable strategy.

Suppliers Bargaining Power

Concentrated specialty inputs

Many critical inputs are region-concentrated—Madagascar supplies about 80% of global vanilla and Ivory Coast plus Ghana account for roughly 60% of cocoa—giving suppliers pricing and allocation leverage. Kerry mitigates via multi-sourcing and hedging, but scarcity cycles still compress margins. Climate shocks and geopolitical disruptions amplify episodic supplier power.

Quality, compliance, and certification hurdles

Suppliers meeting food safety, pharma-grade and sustainability standards are scarce, boosting their bargaining power and contributing to months-long qualification and audit lead times (typically 3–12 months) that raise switching costs. Kerry Group, with 2024 revenue around €8.4bn, relies on global QA systems that reduce supply risk but effectively lock in approved vendors. Premium certifications (BRC, SQF, ISO) allow suppliers to command higher input prices.

Commodity volatility and pass-through

Volatile dairy, sugar and vegetable oil markets materially drive cost swings across Kerry Group’s Taste & Nutrition and Consumer Foods, and while long-term contracts and pass-through clauses mitigate exposure, timing gaps in pass-throughs can compress margins. Suppliers with storage or timing advantages can extract value during short-term spikes, and currency moves, particularly a weaker euro versus USD, further amplify supplier leverage and input cost volatility.

Process/IP-embedded inputs

- Proprietary inputs: high supplier power

- Co-development: increases switching costs

- Limited substitutes: sustained price pressure

- Scale (€9.6bn FY24): enables long-term leverage

Sustainability and traceability requirements

Rising demands for traceability (deforestation-free, fair-trade) narrow Kerry’s eligible supplier pool, enabling compliant suppliers to command premiums and reducing price flexibility for buyers.

Kerry’s public sustainability commitments constrain switching to cheaper non-compliant sources, and ongoing supplier consolidation around ESG standards risks raising structural input costs over time.

- Traceability narrows supplier pool

- Compliant suppliers command premiums

- Sustainability commitments limit switching

- ESG-driven consolidation can raise input costs

Supplier power high; concentration, climate risk vs FY24 revenue €9.6bn

Suppliers exert moderate–high power: geographic concentration (Madagascar ~80% vanilla; Ghana+Ivory Coast ~60% cocoa), proprietary inputs and scarce certified vendors raise switching costs and premiums. Kerry FY24 revenue €9.6bn gives renegotiation leverage, but climate, ESG and commodity volatility keep short-term supplier pricing power elevated.

| Metric | Value |

|---|---|

| FY24 revenue | €9.6bn |

| Vanilla supply (Madagascar) | ~80% |

| Cocoa (Ivory Coast+Ghana) | ~60% |

| Qualification lead time | 3–12 months |

What is included in the product

Tailored exclusively for Kerry Group, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer influence, and market entry risks, identifying disruptive substitutes and emerging threats to market share. Detailed strategic commentary evaluates pricing power and protective market dynamics to inform investor materials and strategic planning.

One-sheet Porter's Five Forces for Kerry Group—clear, customizable pressure levels and instant spider/radar visuals to pinpoint strategic risks and opportunities; copy-ready for pitch decks or board slides, swap in your own data and integrate with Excel or the paired Word report without macros for fast, practical decision-making.

Customers Bargaining Power

Consolidated global CPG and QSR customers

Large multinationals and QSR chains, such as McDonald’s with over 40,000 restaurants worldwide, buy at scale and run competitive tenders, enabling dual-sourcing and aggressive price negotiation. Price transparency in commoditized ingredients amplifies margin pressure across supply chains. Kerry, with operations in 150+ countries and 2023 revenue ~€8.9bn, offsets this through differentiated solutions and multi-year agreements.

Switching costs from formulation lock-in

In 2024 reformulation, sensory revalidation and regulatory re-approvals create tangible switching costs for Kerry customers, reducing pure price-driven churn in complex applications. Buyers still use pilot trials and scale-down testing to extract concessions during contract negotiations. Co-created IP with Kerry both anchors relationships through bespoke formulations and invites heightened price scrutiny when value attribution is contested. Pilot-stage concessions remain a key leveraging point.

Private label and retailer influence

Retailers and private-label buyers push strong price pressure in Consumer Foods, with private-label share rising and major grocers driving frequent promotions that squeeze margins across categories; Kerry reported FY2024 group revenue of about €8.8bn and sustained ~26,000 employees, reflecting scale to negotiate. Buyers can switch brands or contracts rapidly, raising churn risk. Kerry offsets pressure through manufacturing efficiency, premium branding and SKU mix improvement, targeting higher-margin solutions and customer co-development.

Demand for clean label and sustainability

Buyers increasingly specify natural, non-GMO and traceable solutions, with 48% of global consumers prioritizing clean-label ingredients in 2024 (Innova Market Insights), narrowing Kerry’s raw-material pool and raising sourcing costs that can compress margins if not passed on. These specs enable value-based pricing for advanced, traceable systems when Kerry can demonstrate measurable consumer impact—purchase intent or willingness to pay uplift—so negotiation outcomes hinge on proven end-consumer benefits.

- Buyers: higher specification, limited suppliers, cost pressure

- Pricing: risk of margin compression vs value-based premium

- Negotiation: depends on demonstrated consumer impact and willingness to pay

Short lead times and service expectations

Customers demand rapid prototyping (often within 2–4 weeks) and global delivery; OTIF targets around 95% and service-level penalties commonly reach up to 2% of contract value, giving buyers leverage. Kerry’s applications network of over 60 global centres increases stickiness and reduces buyer power, but missed OTIF/service targets frequently trigger price or term concessions.

- OTIF target: 95%

- Penalty range: up to 2%

- Applications centres: >60

Buyers squeeze prices; supplier uses €8.8bn, 60+ centers, multi-year deals

Large global buyers use scale and tenders to force dual-sourcing and price pressure; Kerry’s ~€8.8bn 2024 revenue and 60+ applications centres mitigate this via differentiated solutions and multi-year contracts. Clean-label demand (48% of consumers, 2024) raises sourcing cost but permits premium pricing when impact is proven. OTIF ~95% and penalties up to 2% give customers leverage.

| Metric | Value |

|---|---|

| Revenue (2024) | ~€8.8bn |

| Applications centres | >60 |

| Clean-label priority (2024) | 48% |

| OTIF target | ~95% |

| Penalty range | up to 2% |

Full Version Awaits

Kerry Group Porter's Five Forces Analysis

This preview shows the exact Kerry Group Porter's Five Forces Analysis you'll receive after purchase—no placeholders or excerpts. The full document is professionally formatted and ready for immediate download and use. What you see here is precisely what will be delivered upon payment.

From Overview to Strategy Blueprint

This snapshot highlights Kerry Group’s competitive pressures—supplier and buyer power, substitute threats, entry barriers and industry rivalry—showing where margins and growth may be challenged. Ready to go deeper? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals and actionable strategy.

Suppliers Bargaining Power

Concentrated specialty inputs

Many critical inputs are region-concentrated—Madagascar supplies about 80% of global vanilla and Ivory Coast plus Ghana account for roughly 60% of cocoa—giving suppliers pricing and allocation leverage. Kerry mitigates via multi-sourcing and hedging, but scarcity cycles still compress margins. Climate shocks and geopolitical disruptions amplify episodic supplier power.

Quality, compliance, and certification hurdles

Suppliers meeting food safety, pharma-grade and sustainability standards are scarce, boosting their bargaining power and contributing to months-long qualification and audit lead times (typically 3–12 months) that raise switching costs. Kerry Group, with 2024 revenue around €8.4bn, relies on global QA systems that reduce supply risk but effectively lock in approved vendors. Premium certifications (BRC, SQF, ISO) allow suppliers to command higher input prices.

Commodity volatility and pass-through

Volatile dairy, sugar and vegetable oil markets materially drive cost swings across Kerry Group’s Taste & Nutrition and Consumer Foods, and while long-term contracts and pass-through clauses mitigate exposure, timing gaps in pass-throughs can compress margins. Suppliers with storage or timing advantages can extract value during short-term spikes, and currency moves, particularly a weaker euro versus USD, further amplify supplier leverage and input cost volatility.

Process/IP-embedded inputs

- Proprietary inputs: high supplier power

- Co-development: increases switching costs

- Limited substitutes: sustained price pressure

- Scale (€9.6bn FY24): enables long-term leverage

Sustainability and traceability requirements

Rising demands for traceability (deforestation-free, fair-trade) narrow Kerry’s eligible supplier pool, enabling compliant suppliers to command premiums and reducing price flexibility for buyers.

Kerry’s public sustainability commitments constrain switching to cheaper non-compliant sources, and ongoing supplier consolidation around ESG standards risks raising structural input costs over time.

- Traceability narrows supplier pool

- Compliant suppliers command premiums

- Sustainability commitments limit switching

- ESG-driven consolidation can raise input costs

Supplier power high; concentration, climate risk vs FY24 revenue €9.6bn

Suppliers exert moderate–high power: geographic concentration (Madagascar ~80% vanilla; Ghana+Ivory Coast ~60% cocoa), proprietary inputs and scarce certified vendors raise switching costs and premiums. Kerry FY24 revenue €9.6bn gives renegotiation leverage, but climate, ESG and commodity volatility keep short-term supplier pricing power elevated.

| Metric | Value |

|---|---|

| FY24 revenue | €9.6bn |

| Vanilla supply (Madagascar) | ~80% |

| Cocoa (Ivory Coast+Ghana) | ~60% |

| Qualification lead time | 3–12 months |

What is included in the product

Tailored exclusively for Kerry Group, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer influence, and market entry risks, identifying disruptive substitutes and emerging threats to market share. Detailed strategic commentary evaluates pricing power and protective market dynamics to inform investor materials and strategic planning.

One-sheet Porter's Five Forces for Kerry Group—clear, customizable pressure levels and instant spider/radar visuals to pinpoint strategic risks and opportunities; copy-ready for pitch decks or board slides, swap in your own data and integrate with Excel or the paired Word report without macros for fast, practical decision-making.

Customers Bargaining Power

Consolidated global CPG and QSR customers

Large multinationals and QSR chains, such as McDonald’s with over 40,000 restaurants worldwide, buy at scale and run competitive tenders, enabling dual-sourcing and aggressive price negotiation. Price transparency in commoditized ingredients amplifies margin pressure across supply chains. Kerry, with operations in 150+ countries and 2023 revenue ~€8.9bn, offsets this through differentiated solutions and multi-year agreements.

Switching costs from formulation lock-in

In 2024 reformulation, sensory revalidation and regulatory re-approvals create tangible switching costs for Kerry customers, reducing pure price-driven churn in complex applications. Buyers still use pilot trials and scale-down testing to extract concessions during contract negotiations. Co-created IP with Kerry both anchors relationships through bespoke formulations and invites heightened price scrutiny when value attribution is contested. Pilot-stage concessions remain a key leveraging point.

Private label and retailer influence

Retailers and private-label buyers push strong price pressure in Consumer Foods, with private-label share rising and major grocers driving frequent promotions that squeeze margins across categories; Kerry reported FY2024 group revenue of about €8.8bn and sustained ~26,000 employees, reflecting scale to negotiate. Buyers can switch brands or contracts rapidly, raising churn risk. Kerry offsets pressure through manufacturing efficiency, premium branding and SKU mix improvement, targeting higher-margin solutions and customer co-development.

Demand for clean label and sustainability

Buyers increasingly specify natural, non-GMO and traceable solutions, with 48% of global consumers prioritizing clean-label ingredients in 2024 (Innova Market Insights), narrowing Kerry’s raw-material pool and raising sourcing costs that can compress margins if not passed on. These specs enable value-based pricing for advanced, traceable systems when Kerry can demonstrate measurable consumer impact—purchase intent or willingness to pay uplift—so negotiation outcomes hinge on proven end-consumer benefits.

- Buyers: higher specification, limited suppliers, cost pressure

- Pricing: risk of margin compression vs value-based premium

- Negotiation: depends on demonstrated consumer impact and willingness to pay

Short lead times and service expectations

Customers demand rapid prototyping (often within 2–4 weeks) and global delivery; OTIF targets around 95% and service-level penalties commonly reach up to 2% of contract value, giving buyers leverage. Kerry’s applications network of over 60 global centres increases stickiness and reduces buyer power, but missed OTIF/service targets frequently trigger price or term concessions.

- OTIF target: 95%

- Penalty range: up to 2%

- Applications centres: >60

Buyers squeeze prices; supplier uses €8.8bn, 60+ centers, multi-year deals

Large global buyers use scale and tenders to force dual-sourcing and price pressure; Kerry’s ~€8.8bn 2024 revenue and 60+ applications centres mitigate this via differentiated solutions and multi-year contracts. Clean-label demand (48% of consumers, 2024) raises sourcing cost but permits premium pricing when impact is proven. OTIF ~95% and penalties up to 2% give customers leverage.

| Metric | Value |

|---|---|

| Revenue (2024) | ~€8.8bn |

| Applications centres | >60 |

| Clean-label priority (2024) | 48% |

| OTIF target | ~95% |

| Penalty range | up to 2% |

Full Version Awaits

Kerry Group Porter's Five Forces Analysis

This preview shows the exact Kerry Group Porter's Five Forces Analysis you'll receive after purchase—no placeholders or excerpts. The full document is professionally formatted and ready for immediate download and use. What you see here is precisely what will be delivered upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

This snapshot highlights Kerry Group’s competitive pressures—supplier and buyer power, substitute threats, entry barriers and industry rivalry—showing where margins and growth may be challenged. Ready to go deeper? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals and actionable strategy.

Suppliers Bargaining Power

Concentrated specialty inputs

Many critical inputs are region-concentrated—Madagascar supplies about 80% of global vanilla and Ivory Coast plus Ghana account for roughly 60% of cocoa—giving suppliers pricing and allocation leverage. Kerry mitigates via multi-sourcing and hedging, but scarcity cycles still compress margins. Climate shocks and geopolitical disruptions amplify episodic supplier power.

Quality, compliance, and certification hurdles

Suppliers meeting food safety, pharma-grade and sustainability standards are scarce, boosting their bargaining power and contributing to months-long qualification and audit lead times (typically 3–12 months) that raise switching costs. Kerry Group, with 2024 revenue around €8.4bn, relies on global QA systems that reduce supply risk but effectively lock in approved vendors. Premium certifications (BRC, SQF, ISO) allow suppliers to command higher input prices.

Commodity volatility and pass-through

Volatile dairy, sugar and vegetable oil markets materially drive cost swings across Kerry Group’s Taste & Nutrition and Consumer Foods, and while long-term contracts and pass-through clauses mitigate exposure, timing gaps in pass-throughs can compress margins. Suppliers with storage or timing advantages can extract value during short-term spikes, and currency moves, particularly a weaker euro versus USD, further amplify supplier leverage and input cost volatility.

Process/IP-embedded inputs

- Proprietary inputs: high supplier power

- Co-development: increases switching costs

- Limited substitutes: sustained price pressure

- Scale (€9.6bn FY24): enables long-term leverage

Sustainability and traceability requirements

Rising demands for traceability (deforestation-free, fair-trade) narrow Kerry’s eligible supplier pool, enabling compliant suppliers to command premiums and reducing price flexibility for buyers.

Kerry’s public sustainability commitments constrain switching to cheaper non-compliant sources, and ongoing supplier consolidation around ESG standards risks raising structural input costs over time.

- Traceability narrows supplier pool

- Compliant suppliers command premiums

- Sustainability commitments limit switching

- ESG-driven consolidation can raise input costs

Supplier power high; concentration, climate risk vs FY24 revenue €9.6bn

Suppliers exert moderate–high power: geographic concentration (Madagascar ~80% vanilla; Ghana+Ivory Coast ~60% cocoa), proprietary inputs and scarce certified vendors raise switching costs and premiums. Kerry FY24 revenue €9.6bn gives renegotiation leverage, but climate, ESG and commodity volatility keep short-term supplier pricing power elevated.

| Metric | Value |

|---|---|

| FY24 revenue | €9.6bn |

| Vanilla supply (Madagascar) | ~80% |

| Cocoa (Ivory Coast+Ghana) | ~60% |

| Qualification lead time | 3–12 months |

What is included in the product

Tailored exclusively for Kerry Group, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer influence, and market entry risks, identifying disruptive substitutes and emerging threats to market share. Detailed strategic commentary evaluates pricing power and protective market dynamics to inform investor materials and strategic planning.

One-sheet Porter's Five Forces for Kerry Group—clear, customizable pressure levels and instant spider/radar visuals to pinpoint strategic risks and opportunities; copy-ready for pitch decks or board slides, swap in your own data and integrate with Excel or the paired Word report without macros for fast, practical decision-making.

Customers Bargaining Power

Consolidated global CPG and QSR customers

Large multinationals and QSR chains, such as McDonald’s with over 40,000 restaurants worldwide, buy at scale and run competitive tenders, enabling dual-sourcing and aggressive price negotiation. Price transparency in commoditized ingredients amplifies margin pressure across supply chains. Kerry, with operations in 150+ countries and 2023 revenue ~€8.9bn, offsets this through differentiated solutions and multi-year agreements.

Switching costs from formulation lock-in

In 2024 reformulation, sensory revalidation and regulatory re-approvals create tangible switching costs for Kerry customers, reducing pure price-driven churn in complex applications. Buyers still use pilot trials and scale-down testing to extract concessions during contract negotiations. Co-created IP with Kerry both anchors relationships through bespoke formulations and invites heightened price scrutiny when value attribution is contested. Pilot-stage concessions remain a key leveraging point.

Private label and retailer influence

Retailers and private-label buyers push strong price pressure in Consumer Foods, with private-label share rising and major grocers driving frequent promotions that squeeze margins across categories; Kerry reported FY2024 group revenue of about €8.8bn and sustained ~26,000 employees, reflecting scale to negotiate. Buyers can switch brands or contracts rapidly, raising churn risk. Kerry offsets pressure through manufacturing efficiency, premium branding and SKU mix improvement, targeting higher-margin solutions and customer co-development.

Demand for clean label and sustainability

Buyers increasingly specify natural, non-GMO and traceable solutions, with 48% of global consumers prioritizing clean-label ingredients in 2024 (Innova Market Insights), narrowing Kerry’s raw-material pool and raising sourcing costs that can compress margins if not passed on. These specs enable value-based pricing for advanced, traceable systems when Kerry can demonstrate measurable consumer impact—purchase intent or willingness to pay uplift—so negotiation outcomes hinge on proven end-consumer benefits.

- Buyers: higher specification, limited suppliers, cost pressure

- Pricing: risk of margin compression vs value-based premium

- Negotiation: depends on demonstrated consumer impact and willingness to pay

Short lead times and service expectations

Customers demand rapid prototyping (often within 2–4 weeks) and global delivery; OTIF targets around 95% and service-level penalties commonly reach up to 2% of contract value, giving buyers leverage. Kerry’s applications network of over 60 global centres increases stickiness and reduces buyer power, but missed OTIF/service targets frequently trigger price or term concessions.

- OTIF target: 95%

- Penalty range: up to 2%

- Applications centres: >60

Buyers squeeze prices; supplier uses €8.8bn, 60+ centers, multi-year deals

Large global buyers use scale and tenders to force dual-sourcing and price pressure; Kerry’s ~€8.8bn 2024 revenue and 60+ applications centres mitigate this via differentiated solutions and multi-year contracts. Clean-label demand (48% of consumers, 2024) raises sourcing cost but permits premium pricing when impact is proven. OTIF ~95% and penalties up to 2% give customers leverage.

| Metric | Value |

|---|---|

| Revenue (2024) | ~€8.8bn |

| Applications centres | >60 |

| Clean-label priority (2024) | 48% |

| OTIF target | ~95% |

| Penalty range | up to 2% |

Full Version Awaits

Kerry Group Porter's Five Forces Analysis

This preview shows the exact Kerry Group Porter's Five Forces Analysis you'll receive after purchase—no placeholders or excerpts. The full document is professionally formatted and ready for immediate download and use. What you see here is precisely what will be delivered upon payment.