Kerry Properties Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

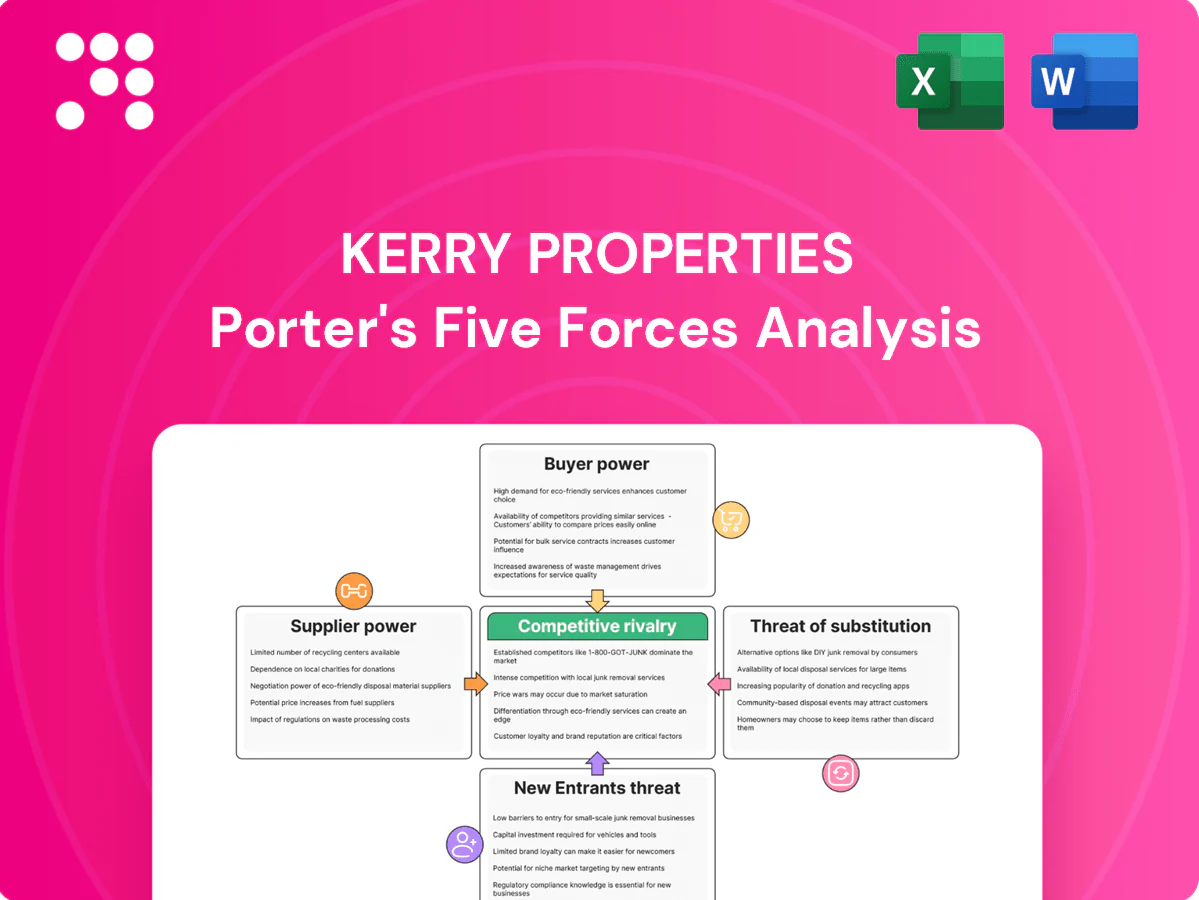

Kerry Properties faces moderate buyer power, tight land and supplier constraints, and intense rivalry across Hong Kong and mainland markets. Regulatory shifts and capital cycles raise risks from substitutes and new entrants. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore Kerry Properties’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Construction materials concentration

Core inputs like steel, cement, glass and HVAC show strong cyclicality—steel and cement prices swung roughly 30–40% and 15–25% respectively between 2020–2024—while a few large regional suppliers often dominate supply. In Hong Kong and tier‑1 Mainland cities strict quality and compliance shrink approved vendor lists to a handful, raising switching costs and timelines. Supplier concentration can therefore lift procurement risk and pass-through costs. Kerry’s scale and long-term relationships partially mitigate this pressure.

Specialist contractors and labor

MEP, façade and fit-out specialists are often capacity-constrained in building booms with utilization commonly cited at 85–95% in 2024; top-tier contractors command schedule priority and can extract 5–12% price premiums due to skilled labor scarcity and stricter safety compliance. Project delays from specialist shortages routinely cascade across GCC development schedules, and Kerry uses multi-year framework agreements and performance-based contracts to secure priority delivery.

Land as a “supplier” via auctions

Government land auctions and tenders in Hong Kong and Mainland cities act as a quasi-monopoly input, with land-transfer fees historically accounting for roughly 20–30% of local government revenue. Limited prime plots and policy-driven release cadence push acquisition costs higher, while competition from state-owned and private developers intensifies bidding. Strategic land banking and JV partnerships are used by Kerry Properties to smooth price volatility and secure supply.

Technology and building systems vendors

Smart-building, ESG and green-certification systems are concentrated among a handful of certified vendors; proprietary platforms increase lock-in and lifecycle costs, while standards like BACnet, Matter and KNX are improving interoperability. The global smart-building market was about USD 41 billion in 2024 and smart systems can cut energy use up to 30%, but Kerry’s premium positioning demands higher-spec systems, moderating supplier leverage.

- Concentration: few certified providers

- Cost: proprietary platforms raise lifecycle costs

- Standards: BACnet/Matter/KNX improving interoperability

- Numbers: USD 41B market (2024); energy savings up to 30%

- Kerry: premium specs reduce supplier bargaining power

Logistics and infrastructure tie-ins

Utility hookups, transport access and municipal approvals effectively supply project viability; delays or conditional hookups can stall cash flows and hand negotiating leverage to authorities. Coordination with state entities often creates bottlenecks as permitting bodies hold structural power over timelines and conditions. Kerry Properties, founded 1978 and active in Hong Kong and Mainland China, uses long operating history and infrastructure affiliations to accelerate interfaces.

- Permitting bodies exert structural power

- Utility/transport access = critical input

- State coordination can create bottlenecks

- Long history (founded 1978) aids faster interfaces

Supplier pressure: steel +30–40%, cement +15–25%

Supplier power is moderate-high: raw-materials volatile (steel +30–40%, cement +15–25% 2020–24) and specialist contractors ran 85–95% utilization in 2024, extracting 5–12% premiums. Land release cadence and land-transfer fees (≈20–30% of local govt revenue) tighten acquisition power. Smart-building vendors concentrate in a USD 41B market (2024), but Kerry’s scale and long agreements mitigate risks.

| Factor | 2024 metric | Impact on Kerry |

|---|---|---|

| Raw materials | Steel +30–40%, Cement +15–25% | Raises procurement risk |

| Specialist contractors | Utilization 85–95%; premiums 5–12% | Schedule/price pressure |

| Land supply | Land fees ≈20–30% govt revenue | Higher acquisition costs |

| Smart systems | Market USD 41B; energy saving up to 30% | Vendor concentration, moderate leverage |

What is included in the product

Tailored Porter’s Five Forces analysis of Kerry Properties uncovering competitive intensity, buyer/supplier power, entry barriers and substitution risks, with strategic implications for pricing, margins and market positioning.

A concise one-sheet Porter's Five Forces for Kerry Properties that distills competitive pressures, supplier/buyer dynamics and regulatory risks—perfect for quick boardroom decisions and investor notes.

Customers Bargaining Power

Diverse buyer segments

End-buyers in 2024 span luxury residential purchasers, corporate commercial tenants, and mixed-use patrons, creating varied bargaining dynamics. Corporate tenants negotiating longer leases and larger footprints exert greater leverage versus individual luxury buyers, who remain less price-sensitive due to brand and location preferences. Kerry Properties’ premium positioning in 2024 reduces but does not eliminate customer bargaining power.

Information transparency

Comparable sales, vacancy data and online listings — CBRE reported Hong Kong Grade A office vacancy at about 9.0% in 2024 — have boosted buyer knowledge, compressing transaction windows and sharpening price discovery. Greater transparency intensifies price competition in commoditized suburban and mid-market submarkets. For prime waterfront and mixed-use assets, scarcity still limits direct comparability. Robust disclosure of NOI, tenant covenants and superior amenities continue to justify 10–25% transaction premiums.

Institutional tenants’ negotiation

Anchor institutional tenants routinely extract fit-out allowances, rent-free periods and favourable escalation clauses, but their draw boosts footfall and strengthens financing metrics, helping offset concessions; Kerry Properties reported steady leasing activity in 2024 that reinforced asset performance. Renewal options sustain tenant leverage over time, yet proactive curation of a balanced tenant mix preserves overall pricing power and mitigates dependency on any single anchor.

Alternative housing and leasing options

- Co-living/service-apartments up 18% (2024)

- Downsizing to periphery increases switching

- Prime location + amenities lowers churn

Post-sale service and reputation

Defect rectification and property management directly shape perceived value, reducing refund demands and price concessions when issues are resolved swiftly; strong after-sales lowers refund disputes and discounting. Negative resident experiences spread rapidly online, amplifying bargaining power of buyers. Kerry Properties (03883.HK) leverages its integrated management arm in 2024 to support satisfaction and retention.

- After-sales reduces disputes

- Online negatives amplify bargaining

- Kerry 03883.HK integrated management 2024

HK: 9.0% Grade A vacancy, +18% supply shifts tenant leverage

End-buyers in 2024 span luxury residential purchasers, corporate tenants and mixed-use patrons, producing varied bargaining dynamics. HK Grade A office vacancy ~9.0% (CBRE 2024) and co-living/service-apartments supply +18% y/y raise tenant leverage in non-prime markets. Kerry Properties 03883.HK premium positioning, integrated management and steady leasing activity in 2024 limit but do not eliminate customer power.

| Metric | 2024 Value | Implication |

|---|---|---|

| HK Grade A vacancy | ~9.0% | Higher tenant leverage |

| Co-living/serviced supply | +18% y/y | More switching options |

| Transaction premium (prime) | 10–25% | Price insulation for Kerry |

Preview the Actual Deliverable

Kerry Properties Porter's Five Forces Analysis

This preview shows the exact Kerry Properties Porter's Five Forces Analysis you'll receive upon purchase—fully completed, professionally formatted, and ready to use. The content here is the final deliverable, not a mockup or excerpt. Buy with confidence: instant access to this identical file is provided immediately after payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Kerry Properties faces moderate buyer power, tight land and supplier constraints, and intense rivalry across Hong Kong and mainland markets. Regulatory shifts and capital cycles raise risks from substitutes and new entrants. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore Kerry Properties’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Construction materials concentration

Core inputs like steel, cement, glass and HVAC show strong cyclicality—steel and cement prices swung roughly 30–40% and 15–25% respectively between 2020–2024—while a few large regional suppliers often dominate supply. In Hong Kong and tier‑1 Mainland cities strict quality and compliance shrink approved vendor lists to a handful, raising switching costs and timelines. Supplier concentration can therefore lift procurement risk and pass-through costs. Kerry’s scale and long-term relationships partially mitigate this pressure.

Specialist contractors and labor

MEP, façade and fit-out specialists are often capacity-constrained in building booms with utilization commonly cited at 85–95% in 2024; top-tier contractors command schedule priority and can extract 5–12% price premiums due to skilled labor scarcity and stricter safety compliance. Project delays from specialist shortages routinely cascade across GCC development schedules, and Kerry uses multi-year framework agreements and performance-based contracts to secure priority delivery.

Land as a “supplier” via auctions

Government land auctions and tenders in Hong Kong and Mainland cities act as a quasi-monopoly input, with land-transfer fees historically accounting for roughly 20–30% of local government revenue. Limited prime plots and policy-driven release cadence push acquisition costs higher, while competition from state-owned and private developers intensifies bidding. Strategic land banking and JV partnerships are used by Kerry Properties to smooth price volatility and secure supply.

Technology and building systems vendors

Smart-building, ESG and green-certification systems are concentrated among a handful of certified vendors; proprietary platforms increase lock-in and lifecycle costs, while standards like BACnet, Matter and KNX are improving interoperability. The global smart-building market was about USD 41 billion in 2024 and smart systems can cut energy use up to 30%, but Kerry’s premium positioning demands higher-spec systems, moderating supplier leverage.

- Concentration: few certified providers

- Cost: proprietary platforms raise lifecycle costs

- Standards: BACnet/Matter/KNX improving interoperability

- Numbers: USD 41B market (2024); energy savings up to 30%

- Kerry: premium specs reduce supplier bargaining power

Logistics and infrastructure tie-ins

Utility hookups, transport access and municipal approvals effectively supply project viability; delays or conditional hookups can stall cash flows and hand negotiating leverage to authorities. Coordination with state entities often creates bottlenecks as permitting bodies hold structural power over timelines and conditions. Kerry Properties, founded 1978 and active in Hong Kong and Mainland China, uses long operating history and infrastructure affiliations to accelerate interfaces.

- Permitting bodies exert structural power

- Utility/transport access = critical input

- State coordination can create bottlenecks

- Long history (founded 1978) aids faster interfaces

Supplier pressure: steel +30–40%, cement +15–25%

Supplier power is moderate-high: raw-materials volatile (steel +30–40%, cement +15–25% 2020–24) and specialist contractors ran 85–95% utilization in 2024, extracting 5–12% premiums. Land release cadence and land-transfer fees (≈20–30% of local govt revenue) tighten acquisition power. Smart-building vendors concentrate in a USD 41B market (2024), but Kerry’s scale and long agreements mitigate risks.

| Factor | 2024 metric | Impact on Kerry |

|---|---|---|

| Raw materials | Steel +30–40%, Cement +15–25% | Raises procurement risk |

| Specialist contractors | Utilization 85–95%; premiums 5–12% | Schedule/price pressure |

| Land supply | Land fees ≈20–30% govt revenue | Higher acquisition costs |

| Smart systems | Market USD 41B; energy saving up to 30% | Vendor concentration, moderate leverage |

What is included in the product

Tailored Porter’s Five Forces analysis of Kerry Properties uncovering competitive intensity, buyer/supplier power, entry barriers and substitution risks, with strategic implications for pricing, margins and market positioning.

A concise one-sheet Porter's Five Forces for Kerry Properties that distills competitive pressures, supplier/buyer dynamics and regulatory risks—perfect for quick boardroom decisions and investor notes.

Customers Bargaining Power

Diverse buyer segments

End-buyers in 2024 span luxury residential purchasers, corporate commercial tenants, and mixed-use patrons, creating varied bargaining dynamics. Corporate tenants negotiating longer leases and larger footprints exert greater leverage versus individual luxury buyers, who remain less price-sensitive due to brand and location preferences. Kerry Properties’ premium positioning in 2024 reduces but does not eliminate customer bargaining power.

Information transparency

Comparable sales, vacancy data and online listings — CBRE reported Hong Kong Grade A office vacancy at about 9.0% in 2024 — have boosted buyer knowledge, compressing transaction windows and sharpening price discovery. Greater transparency intensifies price competition in commoditized suburban and mid-market submarkets. For prime waterfront and mixed-use assets, scarcity still limits direct comparability. Robust disclosure of NOI, tenant covenants and superior amenities continue to justify 10–25% transaction premiums.

Institutional tenants’ negotiation

Anchor institutional tenants routinely extract fit-out allowances, rent-free periods and favourable escalation clauses, but their draw boosts footfall and strengthens financing metrics, helping offset concessions; Kerry Properties reported steady leasing activity in 2024 that reinforced asset performance. Renewal options sustain tenant leverage over time, yet proactive curation of a balanced tenant mix preserves overall pricing power and mitigates dependency on any single anchor.

Alternative housing and leasing options

- Co-living/service-apartments up 18% (2024)

- Downsizing to periphery increases switching

- Prime location + amenities lowers churn

Post-sale service and reputation

Defect rectification and property management directly shape perceived value, reducing refund demands and price concessions when issues are resolved swiftly; strong after-sales lowers refund disputes and discounting. Negative resident experiences spread rapidly online, amplifying bargaining power of buyers. Kerry Properties (03883.HK) leverages its integrated management arm in 2024 to support satisfaction and retention.

- After-sales reduces disputes

- Online negatives amplify bargaining

- Kerry 03883.HK integrated management 2024

HK: 9.0% Grade A vacancy, +18% supply shifts tenant leverage

End-buyers in 2024 span luxury residential purchasers, corporate tenants and mixed-use patrons, producing varied bargaining dynamics. HK Grade A office vacancy ~9.0% (CBRE 2024) and co-living/service-apartments supply +18% y/y raise tenant leverage in non-prime markets. Kerry Properties 03883.HK premium positioning, integrated management and steady leasing activity in 2024 limit but do not eliminate customer power.

| Metric | 2024 Value | Implication |

|---|---|---|

| HK Grade A vacancy | ~9.0% | Higher tenant leverage |

| Co-living/serviced supply | +18% y/y | More switching options |

| Transaction premium (prime) | 10–25% | Price insulation for Kerry |

Preview the Actual Deliverable

Kerry Properties Porter's Five Forces Analysis

This preview shows the exact Kerry Properties Porter's Five Forces Analysis you'll receive upon purchase—fully completed, professionally formatted, and ready to use. The content here is the final deliverable, not a mockup or excerpt. Buy with confidence: instant access to this identical file is provided immediately after payment.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Kerry Properties faces moderate buyer power, tight land and supplier constraints, and intense rivalry across Hong Kong and mainland markets. Regulatory shifts and capital cycles raise risks from substitutes and new entrants. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore Kerry Properties’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Construction materials concentration

Core inputs like steel, cement, glass and HVAC show strong cyclicality—steel and cement prices swung roughly 30–40% and 15–25% respectively between 2020–2024—while a few large regional suppliers often dominate supply. In Hong Kong and tier‑1 Mainland cities strict quality and compliance shrink approved vendor lists to a handful, raising switching costs and timelines. Supplier concentration can therefore lift procurement risk and pass-through costs. Kerry’s scale and long-term relationships partially mitigate this pressure.

Specialist contractors and labor

MEP, façade and fit-out specialists are often capacity-constrained in building booms with utilization commonly cited at 85–95% in 2024; top-tier contractors command schedule priority and can extract 5–12% price premiums due to skilled labor scarcity and stricter safety compliance. Project delays from specialist shortages routinely cascade across GCC development schedules, and Kerry uses multi-year framework agreements and performance-based contracts to secure priority delivery.

Land as a “supplier” via auctions

Government land auctions and tenders in Hong Kong and Mainland cities act as a quasi-monopoly input, with land-transfer fees historically accounting for roughly 20–30% of local government revenue. Limited prime plots and policy-driven release cadence push acquisition costs higher, while competition from state-owned and private developers intensifies bidding. Strategic land banking and JV partnerships are used by Kerry Properties to smooth price volatility and secure supply.

Technology and building systems vendors

Smart-building, ESG and green-certification systems are concentrated among a handful of certified vendors; proprietary platforms increase lock-in and lifecycle costs, while standards like BACnet, Matter and KNX are improving interoperability. The global smart-building market was about USD 41 billion in 2024 and smart systems can cut energy use up to 30%, but Kerry’s premium positioning demands higher-spec systems, moderating supplier leverage.

- Concentration: few certified providers

- Cost: proprietary platforms raise lifecycle costs

- Standards: BACnet/Matter/KNX improving interoperability

- Numbers: USD 41B market (2024); energy savings up to 30%

- Kerry: premium specs reduce supplier bargaining power

Logistics and infrastructure tie-ins

Utility hookups, transport access and municipal approvals effectively supply project viability; delays or conditional hookups can stall cash flows and hand negotiating leverage to authorities. Coordination with state entities often creates bottlenecks as permitting bodies hold structural power over timelines and conditions. Kerry Properties, founded 1978 and active in Hong Kong and Mainland China, uses long operating history and infrastructure affiliations to accelerate interfaces.

- Permitting bodies exert structural power

- Utility/transport access = critical input

- State coordination can create bottlenecks

- Long history (founded 1978) aids faster interfaces

Supplier pressure: steel +30–40%, cement +15–25%

Supplier power is moderate-high: raw-materials volatile (steel +30–40%, cement +15–25% 2020–24) and specialist contractors ran 85–95% utilization in 2024, extracting 5–12% premiums. Land release cadence and land-transfer fees (≈20–30% of local govt revenue) tighten acquisition power. Smart-building vendors concentrate in a USD 41B market (2024), but Kerry’s scale and long agreements mitigate risks.

| Factor | 2024 metric | Impact on Kerry |

|---|---|---|

| Raw materials | Steel +30–40%, Cement +15–25% | Raises procurement risk |

| Specialist contractors | Utilization 85–95%; premiums 5–12% | Schedule/price pressure |

| Land supply | Land fees ≈20–30% govt revenue | Higher acquisition costs |

| Smart systems | Market USD 41B; energy saving up to 30% | Vendor concentration, moderate leverage |

What is included in the product

Tailored Porter’s Five Forces analysis of Kerry Properties uncovering competitive intensity, buyer/supplier power, entry barriers and substitution risks, with strategic implications for pricing, margins and market positioning.

A concise one-sheet Porter's Five Forces for Kerry Properties that distills competitive pressures, supplier/buyer dynamics and regulatory risks—perfect for quick boardroom decisions and investor notes.

Customers Bargaining Power

Diverse buyer segments

End-buyers in 2024 span luxury residential purchasers, corporate commercial tenants, and mixed-use patrons, creating varied bargaining dynamics. Corporate tenants negotiating longer leases and larger footprints exert greater leverage versus individual luxury buyers, who remain less price-sensitive due to brand and location preferences. Kerry Properties’ premium positioning in 2024 reduces but does not eliminate customer bargaining power.

Information transparency

Comparable sales, vacancy data and online listings — CBRE reported Hong Kong Grade A office vacancy at about 9.0% in 2024 — have boosted buyer knowledge, compressing transaction windows and sharpening price discovery. Greater transparency intensifies price competition in commoditized suburban and mid-market submarkets. For prime waterfront and mixed-use assets, scarcity still limits direct comparability. Robust disclosure of NOI, tenant covenants and superior amenities continue to justify 10–25% transaction premiums.

Institutional tenants’ negotiation

Anchor institutional tenants routinely extract fit-out allowances, rent-free periods and favourable escalation clauses, but their draw boosts footfall and strengthens financing metrics, helping offset concessions; Kerry Properties reported steady leasing activity in 2024 that reinforced asset performance. Renewal options sustain tenant leverage over time, yet proactive curation of a balanced tenant mix preserves overall pricing power and mitigates dependency on any single anchor.

Alternative housing and leasing options

- Co-living/service-apartments up 18% (2024)

- Downsizing to periphery increases switching

- Prime location + amenities lowers churn

Post-sale service and reputation

Defect rectification and property management directly shape perceived value, reducing refund demands and price concessions when issues are resolved swiftly; strong after-sales lowers refund disputes and discounting. Negative resident experiences spread rapidly online, amplifying bargaining power of buyers. Kerry Properties (03883.HK) leverages its integrated management arm in 2024 to support satisfaction and retention.

- After-sales reduces disputes

- Online negatives amplify bargaining

- Kerry 03883.HK integrated management 2024

HK: 9.0% Grade A vacancy, +18% supply shifts tenant leverage

End-buyers in 2024 span luxury residential purchasers, corporate tenants and mixed-use patrons, producing varied bargaining dynamics. HK Grade A office vacancy ~9.0% (CBRE 2024) and co-living/service-apartments supply +18% y/y raise tenant leverage in non-prime markets. Kerry Properties 03883.HK premium positioning, integrated management and steady leasing activity in 2024 limit but do not eliminate customer power.

| Metric | 2024 Value | Implication |

|---|---|---|

| HK Grade A vacancy | ~9.0% | Higher tenant leverage |

| Co-living/serviced supply | +18% y/y | More switching options |

| Transaction premium (prime) | 10–25% | Price insulation for Kerry |

Preview the Actual Deliverable

Kerry Properties Porter's Five Forces Analysis

This preview shows the exact Kerry Properties Porter's Five Forces Analysis you'll receive upon purchase—fully completed, professionally formatted, and ready to use. The content here is the final deliverable, not a mockup or excerpt. Buy with confidence: instant access to this identical file is provided immediately after payment.