Keurig Dr Pepper Boston Consulting Group Matrix

See the Bigger Picture

Keurig Dr Pepper’s product mix sits at an interesting crossroads — some brands are clear Stars, others steady Cash Cows, and a few need a hard look. This snapshot scratches the surface; buy the full BCG Matrix to see exact quadrant placements, revenue and market-share data, and practical moves you can act on. Get the ready-to-use Word report + high-level Excel summary for board-ready slides and quick strategy shifts. Purchase now and stop guessing which brands to back or prune.

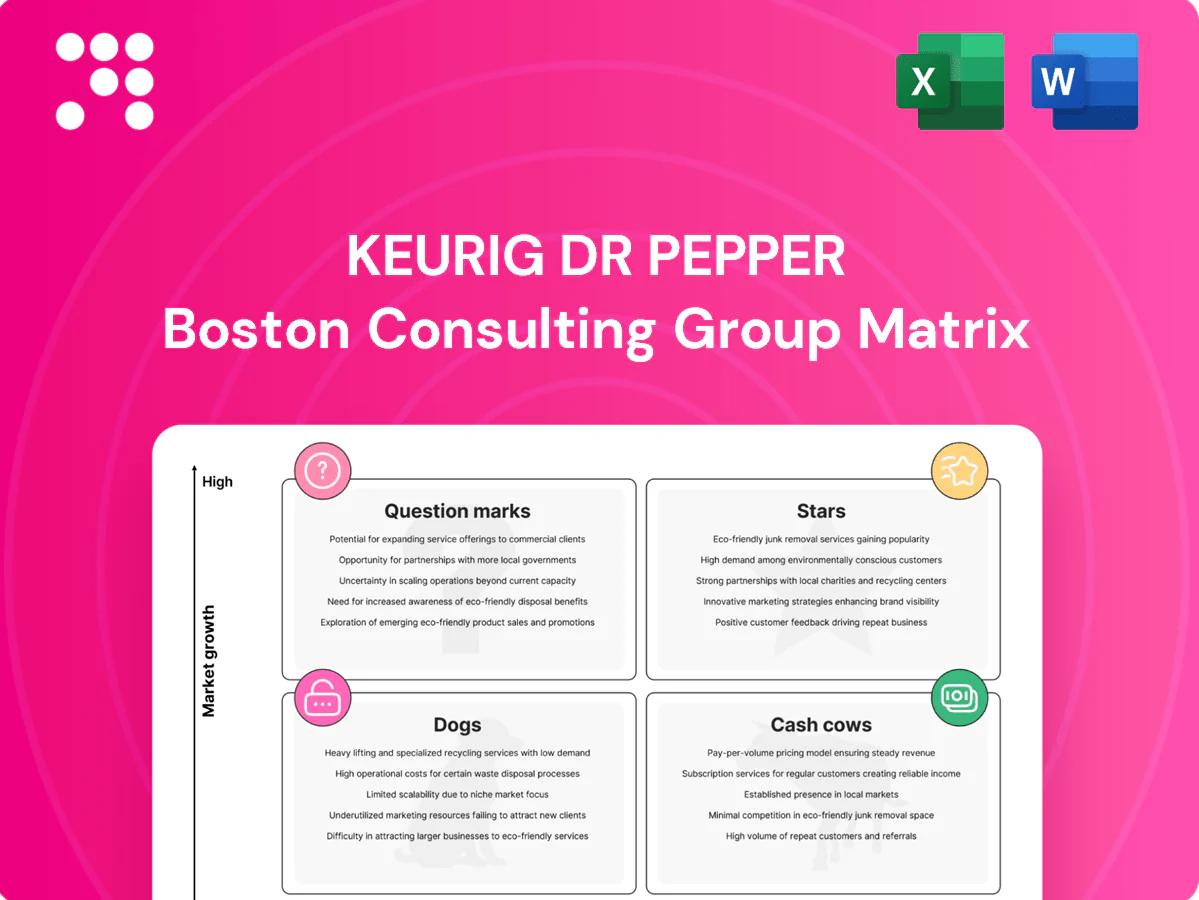

Stars

Dr Pepper brand momentum

Dr Pepper sits in Stars with high share and category tailwinds, helping KDP report roughly $12.4B in 2024 net sales; the brand keeps stealing sips from competitors. It must sustain promo and placement to hold the lead while the market expands. Keep feeding media, new flavors and multipacks to convert trial into habit. Maintain share now and it can graduate into pure cash mode.

K-Cup pods ecosystem

Single-serve at-home coffee continues expanding (segment ~3% annual growth in 2023–24) and KDP owns the shelf with roughly 70% K-Cup pod share and Keurig penetration above 60% of U.S. households. Volume turns fast, requiring sustained marketing to defend share and onboard users while driving high attach rates and flavor expansion. The flywheel—more households, more attach, more SKUs—can convert K-Cup dominance into long-term cash flow for KDP (company revenue ~$14.5B in 2023).

CORE Hydration premium water

Trading-up in bottled water continues and CORE Hydration holds a strong lane in premium after Keurig Dr Pepper paid about 525 million dollars to acquire CORE in 2021; velocity is solid but awareness and cold-space come at recurring promotional and CAPEX cost, so continued investment is required. Line extensions (electrolytes, flavors) deepen the moat and, if executed, can transition CORE from a high-growth Star into a steady Cash Cow within KDP’s portfolio.

C4 Energy distribution play

C4 Energy is a rocket ship in KDP’s portfolio, with KDP’s extensive route-to-market providing the throttle; share climbs in dense distribution but growth requires heavy sampling and shelf investment, and converting trial to repeat is key. Push broad availability, multipack trials, and cold placements to lock repeat purchase and prioritize short-term share wins to monetize later.

- Distribution-led growth

- Sampling-heavy burn

- Drive cold availability

- Multipack trials to convert

- Win now, milk later

Dr Pepper Zero Sugar

Zero-sugar CSDs remain one of the few clear growth seams in soda in 2024, and Dr Pepper Zero Sugar delivers taste parity and strong repeat purchase behavior that helps Keurig Dr Pepper defend share versus Coke and Pepsi.

- Keep media share high to outpace Coke/Pepsi zeros

- Prioritize flavor innovation and sports moments

- Maintain lead to convert into annuity-like cash

Portfolio fuels ~12.4B sales; pods rise, zero-sugar CSDs expand

Dr Pepper, Keurig K-Cups, CORE and C4 sit as Stars for KDP—Dr Pepper drove brand strength into KDP’s ~12.4B net sales in 2024; single-serve pods grew ~3% in 2023–24 with K-Cup ~70% share and >60% U.S. household penetration; CORE (acquired for ~$525M in 2021) and C4 need distribution and sampling to convert trial to repeat; zero-sugar CSDs remain a key growth seam in 2024.

| Brand | 2024 metric | note |

|---|---|---|

| Dr Pepper | $12.4B contrib | High share |

| K-Cup | ~70% share | >60% HH |

| CORE | Acq $525M | Premium water |

What is included in the product

BCG Matrix review of Keurig Dr Pepper’s portfolio: stars, cash cows, question marks, dogs with investment and divestment guidance.

One-page BCG matrix placing Keurig Dr Pepper units in quadrants to spot growth vs cash cows - clarity for fast, strategic decisions.

Cash Cows

Canada Dry & Schweppes mixers

Canada Dry and Schweppes sit as mature, high-share cash cows for Keurig Dr Pepper, driving predictable margins; in 2024 they delivered low-single-digit category growth while representing roughly 12% of KDP beverage revenue. Low growth implies modest promotional spend keeps velocity steady; focus is on pack-price architecture and DSD efficiency to protect margin. KDP uses this cash flow to fund new growth bets and innovation.

7UP/A&W/Sunkist core CSDs

7UP/A&W/Sunkist are established household CSDs delivering stable velocities and scale-driven margins; Keurig Dr Pepper reported fiscal 2024 net sales of about $13.5 billion, with CSDs a core contributor. Category growth is tepid—US CSD volume was flat to low-single-digit decline in 2024—so marketing spend stays tight. Strategy: defend shelf space, optimize pricing, and trim tail SKUs to protect margin and free reliable cash that powers the portfolio.

Keurig brewers installed base

Keurig brewers boast an installed base of over 30 million households, producing steady accessory and replacement-parts sales that carry higher margins and recurring cash flow. Hardware unit growth has slowed, but service parts and pod ecosystem revenues remain resilient, supporting mid-single-digit organic growth for the beverage segment. Seasonal promos and strict compatibility keep ecosystem stickiness high, preserving lifetime value. Efficient operations and supply-chain discipline boost flow-through, helping KDP sustain operating leverage against a ~12.1 billion dollar 2024 revenue base.

Mott’s juice and applesauce

Mott’s juice and applesauce sit squarely as Keurig Dr Pepper cash cows: trusted pantry staples with low marketing churn that deliver steady margins and help KDP (net sales ~14.6 billion in 2024) fund higher-growth bets. Promotional spend is surgical—trade and pack-size mix plus school/channel penetration drive incremental volume. Bank the cash and redeploy into innovations and expanding faster-growing categories.

- Trusted pantry brand — steady demand

- Surgical promo — efficient ROI

- Pack-size and school/channel focus

- Cash generator — funds growth investments

Snapple teas (core SKUs)

Snapple teas (core SKUs) remain an iconic, multi-decade brand with a loyal buyer base even as US RTD tea growth cooled to low single digits in 2024; focus on high-velocity flavors and profitable pack formats preserves SKU economics. Maintain broad off- and on-premise distribution with limited incremental media spend to protect margins and steady cash generation for Keurig Dr Pepper.

- Brand strength: high loyalty, enduring awareness

- Category trend: RTD tea growth low single digits (2024)

- Assortment: concentrate on top-selling flavors and pack sizes

- Go-to-market: wide distribution, minimal incremental media

- Financials: solid margins, reliable cash-out for reinvestment

Beverage cash cows: steady margins, pack-price, SKU pruning and targeted promos

KDP cash cows (Canada Dry/Schweppes, 7UP/A&W/Sunkist, Mott’s, Snapple, Keurig accessories) deliver predictable margins and cash to fund growth; 2024 net sales ~14.6B, beverage revenue ~12.1B, CSDs core contributor. Category growth in 2024 was low-single-digits; priorities: pack-price, SKU pruning, DSD efficiency and targeted promos to preserve margin.

| Brand | Role | 2024 metric | Growth 2024 | Key action |

|---|---|---|---|---|

| Canada Dry/Schweppes | Cash cow | ~12% beverage rev | low SD | price/pack mix |

| 7UP/A&W/Sunkist | Cash cow | core CSD | flat to -SD | defend shelf |

| Mott’s | Cash cow | stable pantry rev | low SD | school/channel mix |

| Snapple | Cash cow | RTD tea scale | low SD | SKU focus |

| Keurig brewers | Hardware cashflow | 30M installed base | mid SD rev | ecosystem stickiness |

Full Transparency, Always

Keurig Dr Pepper BCG Matrix

The Keurig Dr Pepper BCG Matrix you're previewing is the exact file you'll receive after purchase. No watermarks, no placeholder content—just a fully formatted strategic report built for clarity. Buy once and download the ready-to-edit, print-ready matrix, crafted for immediate use in planning or investor decks. What you see is what you get.

See the Bigger Picture

Keurig Dr Pepper’s product mix sits at an interesting crossroads — some brands are clear Stars, others steady Cash Cows, and a few need a hard look. This snapshot scratches the surface; buy the full BCG Matrix to see exact quadrant placements, revenue and market-share data, and practical moves you can act on. Get the ready-to-use Word report + high-level Excel summary for board-ready slides and quick strategy shifts. Purchase now and stop guessing which brands to back or prune.

Stars

Dr Pepper brand momentum

Dr Pepper sits in Stars with high share and category tailwinds, helping KDP report roughly $12.4B in 2024 net sales; the brand keeps stealing sips from competitors. It must sustain promo and placement to hold the lead while the market expands. Keep feeding media, new flavors and multipacks to convert trial into habit. Maintain share now and it can graduate into pure cash mode.

K-Cup pods ecosystem

Single-serve at-home coffee continues expanding (segment ~3% annual growth in 2023–24) and KDP owns the shelf with roughly 70% K-Cup pod share and Keurig penetration above 60% of U.S. households. Volume turns fast, requiring sustained marketing to defend share and onboard users while driving high attach rates and flavor expansion. The flywheel—more households, more attach, more SKUs—can convert K-Cup dominance into long-term cash flow for KDP (company revenue ~$14.5B in 2023).

CORE Hydration premium water

Trading-up in bottled water continues and CORE Hydration holds a strong lane in premium after Keurig Dr Pepper paid about 525 million dollars to acquire CORE in 2021; velocity is solid but awareness and cold-space come at recurring promotional and CAPEX cost, so continued investment is required. Line extensions (electrolytes, flavors) deepen the moat and, if executed, can transition CORE from a high-growth Star into a steady Cash Cow within KDP’s portfolio.

C4 Energy distribution play

C4 Energy is a rocket ship in KDP’s portfolio, with KDP’s extensive route-to-market providing the throttle; share climbs in dense distribution but growth requires heavy sampling and shelf investment, and converting trial to repeat is key. Push broad availability, multipack trials, and cold placements to lock repeat purchase and prioritize short-term share wins to monetize later.

- Distribution-led growth

- Sampling-heavy burn

- Drive cold availability

- Multipack trials to convert

- Win now, milk later

Dr Pepper Zero Sugar

Zero-sugar CSDs remain one of the few clear growth seams in soda in 2024, and Dr Pepper Zero Sugar delivers taste parity and strong repeat purchase behavior that helps Keurig Dr Pepper defend share versus Coke and Pepsi.

- Keep media share high to outpace Coke/Pepsi zeros

- Prioritize flavor innovation and sports moments

- Maintain lead to convert into annuity-like cash

Portfolio fuels ~12.4B sales; pods rise, zero-sugar CSDs expand

Dr Pepper, Keurig K-Cups, CORE and C4 sit as Stars for KDP—Dr Pepper drove brand strength into KDP’s ~12.4B net sales in 2024; single-serve pods grew ~3% in 2023–24 with K-Cup ~70% share and >60% U.S. household penetration; CORE (acquired for ~$525M in 2021) and C4 need distribution and sampling to convert trial to repeat; zero-sugar CSDs remain a key growth seam in 2024.

| Brand | 2024 metric | note |

|---|---|---|

| Dr Pepper | $12.4B contrib | High share |

| K-Cup | ~70% share | >60% HH |

| CORE | Acq $525M | Premium water |

What is included in the product

BCG Matrix review of Keurig Dr Pepper’s portfolio: stars, cash cows, question marks, dogs with investment and divestment guidance.

One-page BCG matrix placing Keurig Dr Pepper units in quadrants to spot growth vs cash cows - clarity for fast, strategic decisions.

Cash Cows

Canada Dry & Schweppes mixers

Canada Dry and Schweppes sit as mature, high-share cash cows for Keurig Dr Pepper, driving predictable margins; in 2024 they delivered low-single-digit category growth while representing roughly 12% of KDP beverage revenue. Low growth implies modest promotional spend keeps velocity steady; focus is on pack-price architecture and DSD efficiency to protect margin. KDP uses this cash flow to fund new growth bets and innovation.

7UP/A&W/Sunkist core CSDs

7UP/A&W/Sunkist are established household CSDs delivering stable velocities and scale-driven margins; Keurig Dr Pepper reported fiscal 2024 net sales of about $13.5 billion, with CSDs a core contributor. Category growth is tepid—US CSD volume was flat to low-single-digit decline in 2024—so marketing spend stays tight. Strategy: defend shelf space, optimize pricing, and trim tail SKUs to protect margin and free reliable cash that powers the portfolio.

Keurig brewers installed base

Keurig brewers boast an installed base of over 30 million households, producing steady accessory and replacement-parts sales that carry higher margins and recurring cash flow. Hardware unit growth has slowed, but service parts and pod ecosystem revenues remain resilient, supporting mid-single-digit organic growth for the beverage segment. Seasonal promos and strict compatibility keep ecosystem stickiness high, preserving lifetime value. Efficient operations and supply-chain discipline boost flow-through, helping KDP sustain operating leverage against a ~12.1 billion dollar 2024 revenue base.

Mott’s juice and applesauce

Mott’s juice and applesauce sit squarely as Keurig Dr Pepper cash cows: trusted pantry staples with low marketing churn that deliver steady margins and help KDP (net sales ~14.6 billion in 2024) fund higher-growth bets. Promotional spend is surgical—trade and pack-size mix plus school/channel penetration drive incremental volume. Bank the cash and redeploy into innovations and expanding faster-growing categories.

- Trusted pantry brand — steady demand

- Surgical promo — efficient ROI

- Pack-size and school/channel focus

- Cash generator — funds growth investments

Snapple teas (core SKUs)

Snapple teas (core SKUs) remain an iconic, multi-decade brand with a loyal buyer base even as US RTD tea growth cooled to low single digits in 2024; focus on high-velocity flavors and profitable pack formats preserves SKU economics. Maintain broad off- and on-premise distribution with limited incremental media spend to protect margins and steady cash generation for Keurig Dr Pepper.

- Brand strength: high loyalty, enduring awareness

- Category trend: RTD tea growth low single digits (2024)

- Assortment: concentrate on top-selling flavors and pack sizes

- Go-to-market: wide distribution, minimal incremental media

- Financials: solid margins, reliable cash-out for reinvestment

Beverage cash cows: steady margins, pack-price, SKU pruning and targeted promos

KDP cash cows (Canada Dry/Schweppes, 7UP/A&W/Sunkist, Mott’s, Snapple, Keurig accessories) deliver predictable margins and cash to fund growth; 2024 net sales ~14.6B, beverage revenue ~12.1B, CSDs core contributor. Category growth in 2024 was low-single-digits; priorities: pack-price, SKU pruning, DSD efficiency and targeted promos to preserve margin.

| Brand | Role | 2024 metric | Growth 2024 | Key action |

|---|---|---|---|---|

| Canada Dry/Schweppes | Cash cow | ~12% beverage rev | low SD | price/pack mix |

| 7UP/A&W/Sunkist | Cash cow | core CSD | flat to -SD | defend shelf |

| Mott’s | Cash cow | stable pantry rev | low SD | school/channel mix |

| Snapple | Cash cow | RTD tea scale | low SD | SKU focus |

| Keurig brewers | Hardware cashflow | 30M installed base | mid SD rev | ecosystem stickiness |

Full Transparency, Always

Keurig Dr Pepper BCG Matrix

The Keurig Dr Pepper BCG Matrix you're previewing is the exact file you'll receive after purchase. No watermarks, no placeholder content—just a fully formatted strategic report built for clarity. Buy once and download the ready-to-edit, print-ready matrix, crafted for immediate use in planning or investor decks. What you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

See the Bigger Picture

Keurig Dr Pepper’s product mix sits at an interesting crossroads — some brands are clear Stars, others steady Cash Cows, and a few need a hard look. This snapshot scratches the surface; buy the full BCG Matrix to see exact quadrant placements, revenue and market-share data, and practical moves you can act on. Get the ready-to-use Word report + high-level Excel summary for board-ready slides and quick strategy shifts. Purchase now and stop guessing which brands to back or prune.

Stars

Dr Pepper brand momentum

Dr Pepper sits in Stars with high share and category tailwinds, helping KDP report roughly $12.4B in 2024 net sales; the brand keeps stealing sips from competitors. It must sustain promo and placement to hold the lead while the market expands. Keep feeding media, new flavors and multipacks to convert trial into habit. Maintain share now and it can graduate into pure cash mode.

K-Cup pods ecosystem

Single-serve at-home coffee continues expanding (segment ~3% annual growth in 2023–24) and KDP owns the shelf with roughly 70% K-Cup pod share and Keurig penetration above 60% of U.S. households. Volume turns fast, requiring sustained marketing to defend share and onboard users while driving high attach rates and flavor expansion. The flywheel—more households, more attach, more SKUs—can convert K-Cup dominance into long-term cash flow for KDP (company revenue ~$14.5B in 2023).

CORE Hydration premium water

Trading-up in bottled water continues and CORE Hydration holds a strong lane in premium after Keurig Dr Pepper paid about 525 million dollars to acquire CORE in 2021; velocity is solid but awareness and cold-space come at recurring promotional and CAPEX cost, so continued investment is required. Line extensions (electrolytes, flavors) deepen the moat and, if executed, can transition CORE from a high-growth Star into a steady Cash Cow within KDP’s portfolio.

C4 Energy distribution play

C4 Energy is a rocket ship in KDP’s portfolio, with KDP’s extensive route-to-market providing the throttle; share climbs in dense distribution but growth requires heavy sampling and shelf investment, and converting trial to repeat is key. Push broad availability, multipack trials, and cold placements to lock repeat purchase and prioritize short-term share wins to monetize later.

- Distribution-led growth

- Sampling-heavy burn

- Drive cold availability

- Multipack trials to convert

- Win now, milk later

Dr Pepper Zero Sugar

Zero-sugar CSDs remain one of the few clear growth seams in soda in 2024, and Dr Pepper Zero Sugar delivers taste parity and strong repeat purchase behavior that helps Keurig Dr Pepper defend share versus Coke and Pepsi.

- Keep media share high to outpace Coke/Pepsi zeros

- Prioritize flavor innovation and sports moments

- Maintain lead to convert into annuity-like cash

Portfolio fuels ~12.4B sales; pods rise, zero-sugar CSDs expand

Dr Pepper, Keurig K-Cups, CORE and C4 sit as Stars for KDP—Dr Pepper drove brand strength into KDP’s ~12.4B net sales in 2024; single-serve pods grew ~3% in 2023–24 with K-Cup ~70% share and >60% U.S. household penetration; CORE (acquired for ~$525M in 2021) and C4 need distribution and sampling to convert trial to repeat; zero-sugar CSDs remain a key growth seam in 2024.

| Brand | 2024 metric | note |

|---|---|---|

| Dr Pepper | $12.4B contrib | High share |

| K-Cup | ~70% share | >60% HH |

| CORE | Acq $525M | Premium water |

What is included in the product

BCG Matrix review of Keurig Dr Pepper’s portfolio: stars, cash cows, question marks, dogs with investment and divestment guidance.

One-page BCG matrix placing Keurig Dr Pepper units in quadrants to spot growth vs cash cows - clarity for fast, strategic decisions.

Cash Cows

Canada Dry & Schweppes mixers

Canada Dry and Schweppes sit as mature, high-share cash cows for Keurig Dr Pepper, driving predictable margins; in 2024 they delivered low-single-digit category growth while representing roughly 12% of KDP beverage revenue. Low growth implies modest promotional spend keeps velocity steady; focus is on pack-price architecture and DSD efficiency to protect margin. KDP uses this cash flow to fund new growth bets and innovation.

7UP/A&W/Sunkist core CSDs

7UP/A&W/Sunkist are established household CSDs delivering stable velocities and scale-driven margins; Keurig Dr Pepper reported fiscal 2024 net sales of about $13.5 billion, with CSDs a core contributor. Category growth is tepid—US CSD volume was flat to low-single-digit decline in 2024—so marketing spend stays tight. Strategy: defend shelf space, optimize pricing, and trim tail SKUs to protect margin and free reliable cash that powers the portfolio.

Keurig brewers installed base

Keurig brewers boast an installed base of over 30 million households, producing steady accessory and replacement-parts sales that carry higher margins and recurring cash flow. Hardware unit growth has slowed, but service parts and pod ecosystem revenues remain resilient, supporting mid-single-digit organic growth for the beverage segment. Seasonal promos and strict compatibility keep ecosystem stickiness high, preserving lifetime value. Efficient operations and supply-chain discipline boost flow-through, helping KDP sustain operating leverage against a ~12.1 billion dollar 2024 revenue base.

Mott’s juice and applesauce

Mott’s juice and applesauce sit squarely as Keurig Dr Pepper cash cows: trusted pantry staples with low marketing churn that deliver steady margins and help KDP (net sales ~14.6 billion in 2024) fund higher-growth bets. Promotional spend is surgical—trade and pack-size mix plus school/channel penetration drive incremental volume. Bank the cash and redeploy into innovations and expanding faster-growing categories.

- Trusted pantry brand — steady demand

- Surgical promo — efficient ROI

- Pack-size and school/channel focus

- Cash generator — funds growth investments

Snapple teas (core SKUs)

Snapple teas (core SKUs) remain an iconic, multi-decade brand with a loyal buyer base even as US RTD tea growth cooled to low single digits in 2024; focus on high-velocity flavors and profitable pack formats preserves SKU economics. Maintain broad off- and on-premise distribution with limited incremental media spend to protect margins and steady cash generation for Keurig Dr Pepper.

- Brand strength: high loyalty, enduring awareness

- Category trend: RTD tea growth low single digits (2024)

- Assortment: concentrate on top-selling flavors and pack sizes

- Go-to-market: wide distribution, minimal incremental media

- Financials: solid margins, reliable cash-out for reinvestment

Beverage cash cows: steady margins, pack-price, SKU pruning and targeted promos

KDP cash cows (Canada Dry/Schweppes, 7UP/A&W/Sunkist, Mott’s, Snapple, Keurig accessories) deliver predictable margins and cash to fund growth; 2024 net sales ~14.6B, beverage revenue ~12.1B, CSDs core contributor. Category growth in 2024 was low-single-digits; priorities: pack-price, SKU pruning, DSD efficiency and targeted promos to preserve margin.

| Brand | Role | 2024 metric | Growth 2024 | Key action |

|---|---|---|---|---|

| Canada Dry/Schweppes | Cash cow | ~12% beverage rev | low SD | price/pack mix |

| 7UP/A&W/Sunkist | Cash cow | core CSD | flat to -SD | defend shelf |

| Mott’s | Cash cow | stable pantry rev | low SD | school/channel mix |

| Snapple | Cash cow | RTD tea scale | low SD | SKU focus |

| Keurig brewers | Hardware cashflow | 30M installed base | mid SD rev | ecosystem stickiness |

Full Transparency, Always

Keurig Dr Pepper BCG Matrix

The Keurig Dr Pepper BCG Matrix you're previewing is the exact file you'll receive after purchase. No watermarks, no placeholder content—just a fully formatted strategic report built for clarity. Buy once and download the ready-to-edit, print-ready matrix, crafted for immediate use in planning or investor decks. What you see is what you get.