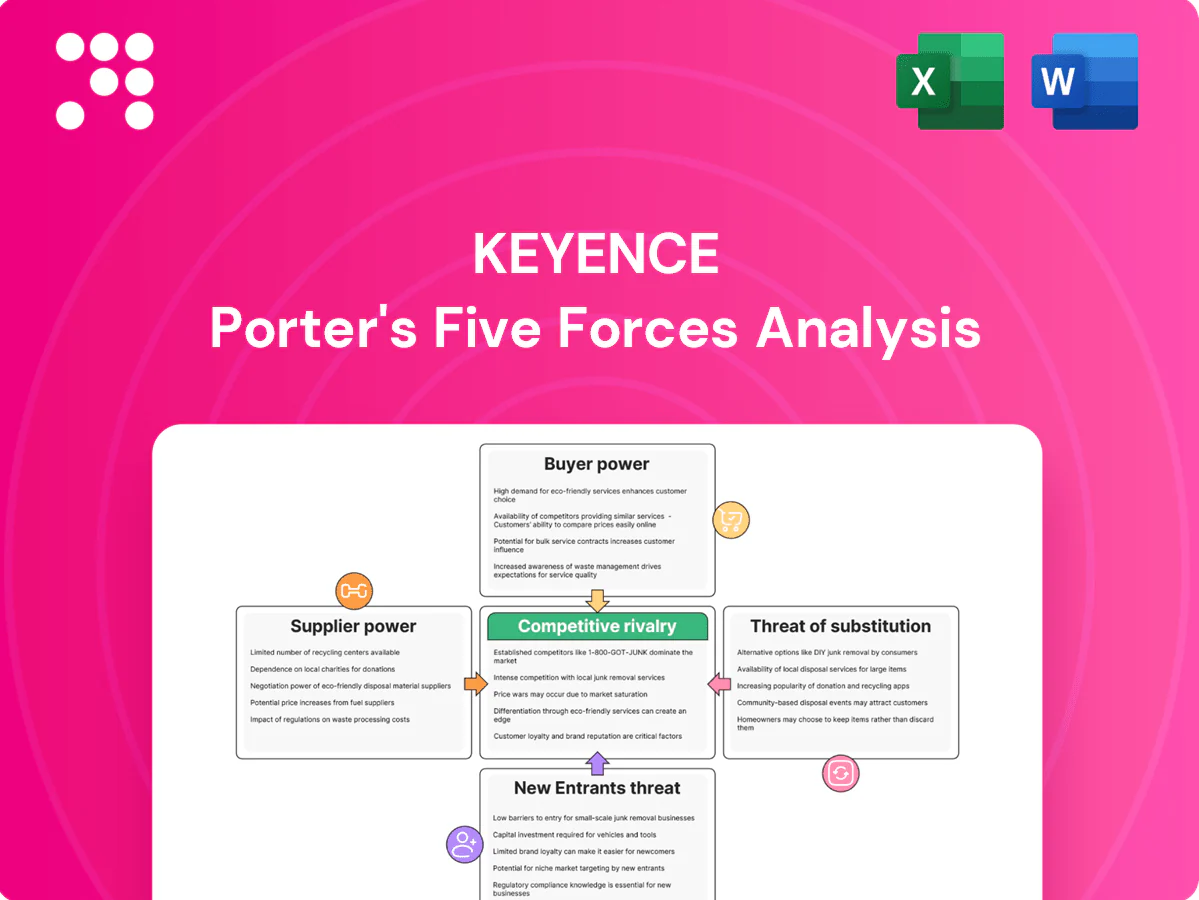

Keyence Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Keyence faces intense rivalry from automation and sensor makers, moderate supplier power, and growing buyer sophistication that pressures margins; threats from new entrants and substitutes remain manageable due to high technical barriers. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or competitive decisions.

Suppliers Bargaining Power

Specialized components concentration

High-precision optics, laser diodes, image sensors and custom ASICs are sourced from a relatively concentrated supplier pool, raising switching costs and lead-time risk for Keyence; however, Keyence’s scale (revenues exceeded ¥700 billion in FY2024) and engineering depth enable dual-sourcing and rigorous vendor qualification to mitigate supplier power, while long-term agreements and modular design further reduce supplier leverage.

Customization and co-development

Keyence’s reliance on custom modules to meet tight performance specs concentrates supplier power toward a limited set of partners, while co-development arrangements create lock‑in even as they let Keyence steer supplier roadmaps. Strong IP ownership and stringent technical specs limit single‑vendor dependency, and joint testing/qualification typically cuts changeover time by up to 30%, reducing switching friction.

Supply chain resilience and geopolitics

Semiconductor cycles, export controls and regional disruptions tightened component availability in 2024, pushing optics/laser lead times beyond six months in some cases. Keyence offsets with diversified sourcing and inventory buffers—holding roughly 1–2 months of critical parts—and premium pricing with an operating margin near 40% (FY2024) helps absorb input-cost swings. Strategic safety stock for long-lead optics/lasers reduces disruption risk.

Manufacturing outsourcing flexibility

Keyence’s fabless, light-asset model in 2024 lets it shift production among EMS partners, reducing supplier bargaining power on assembly and test by keeping suppliers replaceable and subject to competitive bids. Standardized DFM and strict quality systems sustain reliability while enabling price competition. Vendor scorecards plus volume commitments lock in favorable terms and continuity.

- fabless model: 2024 strategic core

- standardized DFM: enables competitive bidding

- vendor scorecards: performance + pricing leverage

- volume commitments: secure lead times and discounts

Brand pull and volume leverage

Keyence’s global demand and rapid product turns, supported by a direct sales network spanning 47 countries (2024), deliver meaningful order volumes that earn suppliers pull-through incentives and priority allocation in tight markets; preferred-customer status often secures better pricing and shorter lead times, while Keyence’s high-end brand makes suppliers eager to be reference partners.

- 47 countries (2024)

- High order volumes → priority allocation

- Preferred-customer pricing & lead-time benefits

- Brand = attractive reference partner

Moderate supplier power vs ¥700bn scale, ~40% margin

Keyence faces moderate supplier power: critical optics/lasers and ASICs come from a concentrated pool, with lead times >6 months in 2024. Scale (revenue >¥700bn FY2024) and fabless model enable dual-sourcing, vendor scorecards and 1–2 months safety stock, reducing leverage. Strong IP and margin (~40% operating margin FY2024) increase supplier incentives to prioritize Keyence.

| Metric | 2024 |

|---|---|

| Revenue | ¥>700bn |

| Operating margin | ~40% |

| Inventory (critical parts) | 1–2 months |

| Lead times (optics/lasers) | >6 months |

| Sales footprint | 47 countries |

What is included in the product

Tailored Porter's Five Forces analysis for Keyence uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, plus disruptive risks and strategic levers to protect margins; delivered in editable Word format for integration into investor decks, strategy reports, or academic work.

A concise one-sheet Porter's Five Forces for Keyence that visualizes competitive pressures and relieves analysis bottlenecks; customizable force levels and clean charts ready to drop into decks or executive reports.

Customers Bargaining Power

Large OEMs vs. SMBs

Automotive, electronics and life‑sciences OEMs buy sensors and vision systems at scale and exert strong price/service leverage; Keyence served this demand as part of FY2024 sales of roughly JPY 753 billion with gross margins near 60%. Smaller manufacturers lack bargaining power and are highly price sensitive, limiting margin pressure on low‑volume SKUs. Keyence mitigates OEM power through tiered pricing, value‑based selling, rapid ROI proofs and volume discounts plus bundled solutions.

High switching costs in production

Validation, PLC/MES integration and operator training create meaningful switching costs for buyers, with 68% of manufacturers citing requalification as a primary barrier to vendor change in 2024. Downtime risk and requalification timelines—often weeks—deter switching given average production losses measured in tens of thousands per hour. Keyence’s ease-of-use, application engineering support and post-sale service, plus firmware continuity and global field engineers in 25+ countries, increase customer lock-in and reduce churn.

Performance-critical applications

In performance-critical metrology and vision applications, accuracy, repeatability and uptime outweigh unit price, weakening pure price bargaining; Keyence leverages on-site demos and trials to quantify yield and scrap reductions. Documented ROI from trials supports premium pricing and drives procurement decisions; the global machine vision market was about USD 13.5 billion in 2024, underscoring strong demand for high-performance solutions.

Direct sales and technical support

Keyence’s direct sales and technical support model limits distributor power and delivers fast application engineering, giving buyers tailored solutions while Keyence controls pricing and the sales narrative. On-site trials compress decision cycles and reduce competitive-quote pressure; continuous follow-up increases lifecycle revenue capture; Keyence (6861.T) sustains ~40% operating margin.

- Direct model: limits distributor leverage

- On-site trials: shorter decision cycles

- Pricing control: higher margin capture

- Follow-up: increased aftermarket revenue

Cyclicality and budget constraints

In downturns buyers tighten capex and demand tougher price and payment terms; Keyence in 2024 mitigated this via leasing, staged rollouts and retrofit kits to preserve order flow and shorten sales cycles.

Product breadth enables cross-selling to defend ASPs while quick-pay discounts and service bundles align with constrained budgets; Keyence sustained strong margins in 2024, supporting flexibility without broad price cuts.

- 2024 tactic: leasing and staged deployment

- Retrofit kits reduce upfront capex

- Cross-selling defends ASPs

- Quick-pay discounts + service bundles

OEMs wield price/service leverage; top vision supplier: JPY 753B, ~60% GM

OEMs exert strong price/service leverage despite Keyence FY2024 sales of JPY 753 billion and ~60% gross margin; high-value apps reduce pure price bargaining. 68% of manufacturers cite requalification as primary switching barrier in 2024, raising churn costs. Machine vision market ≈ USD 13.5B (2024); Keyence sustains ~40% operating margin via direct sales and trials.

| Metric | 2024 |

|---|---|

| Sales | JPY 753B |

| Gross margin | ~60% |

| Op margin | ~40% |

| Requalification barrier | 68% |

| Market size (vision) | USD 13.5B |

Full Version Awaits

Keyence Porter's Five Forces Analysis

This preview shows the exact Keyence Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file is the full, professionally formatted document covering rivalry, supplier and buyer power, threat of substitutes and new entry, plus strategic implications, ready for download. Purchase grants instant access to this identical deliverable.

Don't Miss the Bigger Picture

Keyence faces intense rivalry from automation and sensor makers, moderate supplier power, and growing buyer sophistication that pressures margins; threats from new entrants and substitutes remain manageable due to high technical barriers. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or competitive decisions.

Suppliers Bargaining Power

Specialized components concentration

High-precision optics, laser diodes, image sensors and custom ASICs are sourced from a relatively concentrated supplier pool, raising switching costs and lead-time risk for Keyence; however, Keyence’s scale (revenues exceeded ¥700 billion in FY2024) and engineering depth enable dual-sourcing and rigorous vendor qualification to mitigate supplier power, while long-term agreements and modular design further reduce supplier leverage.

Customization and co-development

Keyence’s reliance on custom modules to meet tight performance specs concentrates supplier power toward a limited set of partners, while co-development arrangements create lock‑in even as they let Keyence steer supplier roadmaps. Strong IP ownership and stringent technical specs limit single‑vendor dependency, and joint testing/qualification typically cuts changeover time by up to 30%, reducing switching friction.

Supply chain resilience and geopolitics

Semiconductor cycles, export controls and regional disruptions tightened component availability in 2024, pushing optics/laser lead times beyond six months in some cases. Keyence offsets with diversified sourcing and inventory buffers—holding roughly 1–2 months of critical parts—and premium pricing with an operating margin near 40% (FY2024) helps absorb input-cost swings. Strategic safety stock for long-lead optics/lasers reduces disruption risk.

Manufacturing outsourcing flexibility

Keyence’s fabless, light-asset model in 2024 lets it shift production among EMS partners, reducing supplier bargaining power on assembly and test by keeping suppliers replaceable and subject to competitive bids. Standardized DFM and strict quality systems sustain reliability while enabling price competition. Vendor scorecards plus volume commitments lock in favorable terms and continuity.

- fabless model: 2024 strategic core

- standardized DFM: enables competitive bidding

- vendor scorecards: performance + pricing leverage

- volume commitments: secure lead times and discounts

Brand pull and volume leverage

Keyence’s global demand and rapid product turns, supported by a direct sales network spanning 47 countries (2024), deliver meaningful order volumes that earn suppliers pull-through incentives and priority allocation in tight markets; preferred-customer status often secures better pricing and shorter lead times, while Keyence’s high-end brand makes suppliers eager to be reference partners.

- 47 countries (2024)

- High order volumes → priority allocation

- Preferred-customer pricing & lead-time benefits

- Brand = attractive reference partner

Moderate supplier power vs ¥700bn scale, ~40% margin

Keyence faces moderate supplier power: critical optics/lasers and ASICs come from a concentrated pool, with lead times >6 months in 2024. Scale (revenue >¥700bn FY2024) and fabless model enable dual-sourcing, vendor scorecards and 1–2 months safety stock, reducing leverage. Strong IP and margin (~40% operating margin FY2024) increase supplier incentives to prioritize Keyence.

| Metric | 2024 |

|---|---|

| Revenue | ¥>700bn |

| Operating margin | ~40% |

| Inventory (critical parts) | 1–2 months |

| Lead times (optics/lasers) | >6 months |

| Sales footprint | 47 countries |

What is included in the product

Tailored Porter's Five Forces analysis for Keyence uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, plus disruptive risks and strategic levers to protect margins; delivered in editable Word format for integration into investor decks, strategy reports, or academic work.

A concise one-sheet Porter's Five Forces for Keyence that visualizes competitive pressures and relieves analysis bottlenecks; customizable force levels and clean charts ready to drop into decks or executive reports.

Customers Bargaining Power

Large OEMs vs. SMBs

Automotive, electronics and life‑sciences OEMs buy sensors and vision systems at scale and exert strong price/service leverage; Keyence served this demand as part of FY2024 sales of roughly JPY 753 billion with gross margins near 60%. Smaller manufacturers lack bargaining power and are highly price sensitive, limiting margin pressure on low‑volume SKUs. Keyence mitigates OEM power through tiered pricing, value‑based selling, rapid ROI proofs and volume discounts plus bundled solutions.

High switching costs in production

Validation, PLC/MES integration and operator training create meaningful switching costs for buyers, with 68% of manufacturers citing requalification as a primary barrier to vendor change in 2024. Downtime risk and requalification timelines—often weeks—deter switching given average production losses measured in tens of thousands per hour. Keyence’s ease-of-use, application engineering support and post-sale service, plus firmware continuity and global field engineers in 25+ countries, increase customer lock-in and reduce churn.

Performance-critical applications

In performance-critical metrology and vision applications, accuracy, repeatability and uptime outweigh unit price, weakening pure price bargaining; Keyence leverages on-site demos and trials to quantify yield and scrap reductions. Documented ROI from trials supports premium pricing and drives procurement decisions; the global machine vision market was about USD 13.5 billion in 2024, underscoring strong demand for high-performance solutions.

Direct sales and technical support

Keyence’s direct sales and technical support model limits distributor power and delivers fast application engineering, giving buyers tailored solutions while Keyence controls pricing and the sales narrative. On-site trials compress decision cycles and reduce competitive-quote pressure; continuous follow-up increases lifecycle revenue capture; Keyence (6861.T) sustains ~40% operating margin.

- Direct model: limits distributor leverage

- On-site trials: shorter decision cycles

- Pricing control: higher margin capture

- Follow-up: increased aftermarket revenue

Cyclicality and budget constraints

In downturns buyers tighten capex and demand tougher price and payment terms; Keyence in 2024 mitigated this via leasing, staged rollouts and retrofit kits to preserve order flow and shorten sales cycles.

Product breadth enables cross-selling to defend ASPs while quick-pay discounts and service bundles align with constrained budgets; Keyence sustained strong margins in 2024, supporting flexibility without broad price cuts.

- 2024 tactic: leasing and staged deployment

- Retrofit kits reduce upfront capex

- Cross-selling defends ASPs

- Quick-pay discounts + service bundles

OEMs wield price/service leverage; top vision supplier: JPY 753B, ~60% GM

OEMs exert strong price/service leverage despite Keyence FY2024 sales of JPY 753 billion and ~60% gross margin; high-value apps reduce pure price bargaining. 68% of manufacturers cite requalification as primary switching barrier in 2024, raising churn costs. Machine vision market ≈ USD 13.5B (2024); Keyence sustains ~40% operating margin via direct sales and trials.

| Metric | 2024 |

|---|---|

| Sales | JPY 753B |

| Gross margin | ~60% |

| Op margin | ~40% |

| Requalification barrier | 68% |

| Market size (vision) | USD 13.5B |

Full Version Awaits

Keyence Porter's Five Forces Analysis

This preview shows the exact Keyence Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file is the full, professionally formatted document covering rivalry, supplier and buyer power, threat of substitutes and new entry, plus strategic implications, ready for download. Purchase grants instant access to this identical deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Keyence faces intense rivalry from automation and sensor makers, moderate supplier power, and growing buyer sophistication that pressures margins; threats from new entrants and substitutes remain manageable due to high technical barriers. This snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or competitive decisions.

Suppliers Bargaining Power

Specialized components concentration

High-precision optics, laser diodes, image sensors and custom ASICs are sourced from a relatively concentrated supplier pool, raising switching costs and lead-time risk for Keyence; however, Keyence’s scale (revenues exceeded ¥700 billion in FY2024) and engineering depth enable dual-sourcing and rigorous vendor qualification to mitigate supplier power, while long-term agreements and modular design further reduce supplier leverage.

Customization and co-development

Keyence’s reliance on custom modules to meet tight performance specs concentrates supplier power toward a limited set of partners, while co-development arrangements create lock‑in even as they let Keyence steer supplier roadmaps. Strong IP ownership and stringent technical specs limit single‑vendor dependency, and joint testing/qualification typically cuts changeover time by up to 30%, reducing switching friction.

Supply chain resilience and geopolitics

Semiconductor cycles, export controls and regional disruptions tightened component availability in 2024, pushing optics/laser lead times beyond six months in some cases. Keyence offsets with diversified sourcing and inventory buffers—holding roughly 1–2 months of critical parts—and premium pricing with an operating margin near 40% (FY2024) helps absorb input-cost swings. Strategic safety stock for long-lead optics/lasers reduces disruption risk.

Manufacturing outsourcing flexibility

Keyence’s fabless, light-asset model in 2024 lets it shift production among EMS partners, reducing supplier bargaining power on assembly and test by keeping suppliers replaceable and subject to competitive bids. Standardized DFM and strict quality systems sustain reliability while enabling price competition. Vendor scorecards plus volume commitments lock in favorable terms and continuity.

- fabless model: 2024 strategic core

- standardized DFM: enables competitive bidding

- vendor scorecards: performance + pricing leverage

- volume commitments: secure lead times and discounts

Brand pull and volume leverage

Keyence’s global demand and rapid product turns, supported by a direct sales network spanning 47 countries (2024), deliver meaningful order volumes that earn suppliers pull-through incentives and priority allocation in tight markets; preferred-customer status often secures better pricing and shorter lead times, while Keyence’s high-end brand makes suppliers eager to be reference partners.

- 47 countries (2024)

- High order volumes → priority allocation

- Preferred-customer pricing & lead-time benefits

- Brand = attractive reference partner

Moderate supplier power vs ¥700bn scale, ~40% margin

Keyence faces moderate supplier power: critical optics/lasers and ASICs come from a concentrated pool, with lead times >6 months in 2024. Scale (revenue >¥700bn FY2024) and fabless model enable dual-sourcing, vendor scorecards and 1–2 months safety stock, reducing leverage. Strong IP and margin (~40% operating margin FY2024) increase supplier incentives to prioritize Keyence.

| Metric | 2024 |

|---|---|

| Revenue | ¥>700bn |

| Operating margin | ~40% |

| Inventory (critical parts) | 1–2 months |

| Lead times (optics/lasers) | >6 months |

| Sales footprint | 47 countries |

What is included in the product

Tailored Porter's Five Forces analysis for Keyence uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, plus disruptive risks and strategic levers to protect margins; delivered in editable Word format for integration into investor decks, strategy reports, or academic work.

A concise one-sheet Porter's Five Forces for Keyence that visualizes competitive pressures and relieves analysis bottlenecks; customizable force levels and clean charts ready to drop into decks or executive reports.

Customers Bargaining Power

Large OEMs vs. SMBs

Automotive, electronics and life‑sciences OEMs buy sensors and vision systems at scale and exert strong price/service leverage; Keyence served this demand as part of FY2024 sales of roughly JPY 753 billion with gross margins near 60%. Smaller manufacturers lack bargaining power and are highly price sensitive, limiting margin pressure on low‑volume SKUs. Keyence mitigates OEM power through tiered pricing, value‑based selling, rapid ROI proofs and volume discounts plus bundled solutions.

High switching costs in production

Validation, PLC/MES integration and operator training create meaningful switching costs for buyers, with 68% of manufacturers citing requalification as a primary barrier to vendor change in 2024. Downtime risk and requalification timelines—often weeks—deter switching given average production losses measured in tens of thousands per hour. Keyence’s ease-of-use, application engineering support and post-sale service, plus firmware continuity and global field engineers in 25+ countries, increase customer lock-in and reduce churn.

Performance-critical applications

In performance-critical metrology and vision applications, accuracy, repeatability and uptime outweigh unit price, weakening pure price bargaining; Keyence leverages on-site demos and trials to quantify yield and scrap reductions. Documented ROI from trials supports premium pricing and drives procurement decisions; the global machine vision market was about USD 13.5 billion in 2024, underscoring strong demand for high-performance solutions.

Direct sales and technical support

Keyence’s direct sales and technical support model limits distributor power and delivers fast application engineering, giving buyers tailored solutions while Keyence controls pricing and the sales narrative. On-site trials compress decision cycles and reduce competitive-quote pressure; continuous follow-up increases lifecycle revenue capture; Keyence (6861.T) sustains ~40% operating margin.

- Direct model: limits distributor leverage

- On-site trials: shorter decision cycles

- Pricing control: higher margin capture

- Follow-up: increased aftermarket revenue

Cyclicality and budget constraints

In downturns buyers tighten capex and demand tougher price and payment terms; Keyence in 2024 mitigated this via leasing, staged rollouts and retrofit kits to preserve order flow and shorten sales cycles.

Product breadth enables cross-selling to defend ASPs while quick-pay discounts and service bundles align with constrained budgets; Keyence sustained strong margins in 2024, supporting flexibility without broad price cuts.

- 2024 tactic: leasing and staged deployment

- Retrofit kits reduce upfront capex

- Cross-selling defends ASPs

- Quick-pay discounts + service bundles

OEMs wield price/service leverage; top vision supplier: JPY 753B, ~60% GM

OEMs exert strong price/service leverage despite Keyence FY2024 sales of JPY 753 billion and ~60% gross margin; high-value apps reduce pure price bargaining. 68% of manufacturers cite requalification as primary switching barrier in 2024, raising churn costs. Machine vision market ≈ USD 13.5B (2024); Keyence sustains ~40% operating margin via direct sales and trials.

| Metric | 2024 |

|---|---|

| Sales | JPY 753B |

| Gross margin | ~60% |

| Op margin | ~40% |

| Requalification barrier | 68% |

| Market size (vision) | USD 13.5B |

Full Version Awaits

Keyence Porter's Five Forces Analysis

This preview shows the exact Keyence Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file is the full, professionally formatted document covering rivalry, supplier and buyer power, threat of substitutes and new entry, plus strategic implications, ready for download. Purchase grants instant access to this identical deliverable.