Kawasaki Heavy Industries Porter's Five Forces Analysis

Don't Miss the Bigger Picture

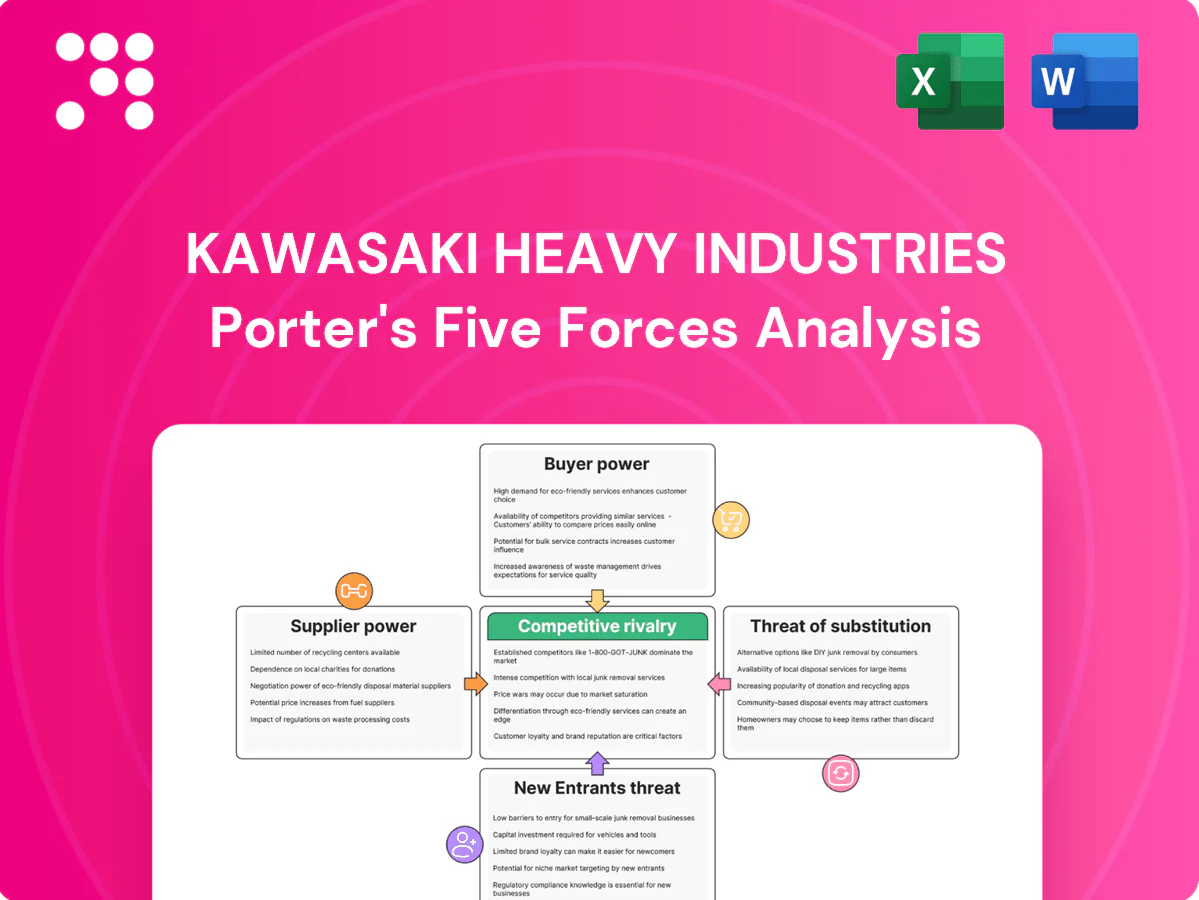

Kawasaki Heavy Industries faces intense rivalry, high capital and regulatory barriers, moderated supplier power thanks to scale, and evolving substitute threats from electrification and alternative transport technologies. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kawasaki Heavy Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized materials

Advanced steels, composites and specialty alloys for Kawasaki come from a concentrated base of fewer than 10 qualified global sources, giving suppliers high leverage. Aerospace-grade and marine-class certifications further shrink the pool, and long lead times for forgings and castings — often up to 52 weeks — create intermittent bottlenecks. Kawasaki reduces risk through multisourcing and selective in-house metallurgy capacity expansion.

High-tech components

Semiconductors, sensors, batteries and control systems are concentrated: TSMC held ~56% foundry share in 2024 and CATL ~33% of EV battery capacity, giving suppliers pricing power; 2021–24 chip shocks led to multi-month rationing and 10–20% repricing in some modules. Proprietary design-in raises switching costs, while long-term framework agreements and co-development (joint R&D, multi-year offtakes) have been used to stabilize supply.

Capital equipment vendors

Shipyards and rolling-stock plants at Kawasaki Heavy Industries depend on large machinery and tooling from dominant OEMs such as Mitsubishi Heavy Industries and Siemens Mobility, creating supplier leverage.

Proprietary maintenance parts and spares tie Kawasaki to those vendors, while upgrades and calibrations sustain ongoing dependence.

Negotiated service-level contracts with OEMs partially mitigate cost and downtime risk by securing prioritized support and lead times.

Logistics and yard services

Heavy-lift, dry-dock and specialized transport capacity tightened in 2024 with heavy-lift fleet utilization around 83%, elevating supplier leverage; global port congestion rose, increasing average vessel delay days by about 14% year-on-year and strengthening logistics providers’ bargaining power. Project-level scheduling magnifies exposure to cascading delays, while Kawasaki’s forward booking and captive yard options can cut disruption risk roughly 50%.

- Capacity utilization ~83% (2024)

- Vessel delays +14% YoY (2024)

- Project scheduling = higher delay exposure

- Forward booking/captive yards ≈50% disruption reduction

Energy and utilities

Energy-intensive forging, welding and testing make Kawasaki highly exposed to power suppliers; in 2024 Japan industrial electricity hovered near ¥22–24/kWh and LNG spot markets eased versus 2022–23 peaks, pushing energy to represent roughly 5–12% of heavy-manufacturing OPEX for comparable firms.

- Volatility: electricity/gas price swings drive cost-baseline risk

- Green premiums: renewables procurement can raise input cost but meet customer ESG mandates

- Mitigation: hedging and on-site generation reduce price exposure

Supplier leverage, scarce chips & batteries, logistics tight; multisourcing cuts risk 50%

Supplier power is high: <10 qualified sources for advanced alloys and long lead times (up to 52 weeks) concentrate leverage. Semiconductors (TSMC ~56% foundry share, 2024) and batteries (CATL ~33% capacity, 2024) add pricing power and switching costs. Logistics and heavy-lift tightness (utilization ~83%, 2024) and energy costs (Japan industrial ¥22–24/kWh, 2024) raise input risk; multisourcing, long-term offtakes and forward booking cut disruption ~50%.

| Input | 2024 metric |

|---|---|

| Advanced alloys sources | <10 |

| TSMC foundry share | ~56% |

| CATL EV capacity | ~33% |

| Heavy-lift util. | ~83% |

| Japan ind. electricity | ¥22–24/kWh |

What is included in the product

Tailored Porter's Five Forces analysis of Kawasaki Heavy Industries, assessing competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, and disruptive forces across its transportation, aerospace, and energy segments to inform strategic decisions.

A clear one-sheet Porter's Five Forces summary for Kawasaki Heavy Industries—ideal for quick strategic decisions and boardroom slides. Customize pressure levels with latest market data and view competitive intensity instantly via a spider chart.

Customers Bargaining Power

Government procurement

Rail operators, defense and public agencies buy via tightly specified tenders, and Japan's defense budget reached about 6.9 trillion JPY in 2024, concentrating buyer power and price leverage. Large contract sizes and a small buyer base give customers outsized bargaining power, forcing suppliers to compete on lifecycle cost and localization requirements that squeeze margins. Performance-based contracts commonly extend maintenance and liability obligations for years to decades, locking in after-sales costs and reducing pricing flexibility.

Fleet and OEM customers

Airframe primes and fleet owners, representing a global commercial jet fleet of about 25,000 aircraft in 2024, use volume discounts and design influence to press suppliers like Kawasaki on price and specs. Dual-sourcing norms and multi-year OEM contracts (commonly 5–15 years) keep pricing competitive. Technical certification raises switching costs, but buyers emphasize total cost of ownership and long relationships often trade lower price for proven reliability and support.

Dealer networks

Motorcycle dealers shape retail mix, incentives and inventory turns by choosing which Kawasaki models to prioritize and pressing for floor-plan support and marketing co‑funding; they can demand better terms to protect margins. Dealers' ability to switch to rival brands gives them negotiating leverage, especially in regions with strong multi-brand networks. Kawasaki counters through brand pull, captive finance via Kawasaki Motors Finance and expanded digital retail tools and dealer portals to boost turn and reduce channel friction.

End-user price sensitivity

End-user demand for consumer motorcycles is price-elastic with frequent cross-shopping; global two-wheeler sales were roughly 50 million in 2024, amplifying sensitivity to small price moves. Economic cycles and higher credit costs in 2024 reduced willingness to pay, while features/performance support premiums only within segment limits. Financing offers and after-sales bundles (warranty, service plans) preserve value and close sales.

- Elastic demand

- Credit-driven swings

- Feature-premium cap

- Financing/after-sales

Service and parts leverage

Industrial buyers push Kawasaki for uptime guarantees and predictable spares pricing, turning multi-year service contracts into negotiation focal points; access to diagnostics/data becomes a bargaining chip as customers seek remote-troubleshoot rights and capex predictability. Kawasaki’s extensive installed base strengthens bargaining position on parts volume but obligates long-term support commitments and margin pressure.

- Service contracts: negotiation focal point

- Data access: customer leverage

- Installed base: strength and obligation

Buyers Hold Leverage: Tenders, Fleet Demands and Dealer Pressure Shape Lifecycle Costs

Buyers exert high leverage via large, specified tenders (Japan defense budget ~6.9 trillion JPY in 2024), forcing bids on lifecycle cost and localization. Airframe primes (global fleet ~25,000 aircraft in 2024) drive price and spec demands; certification raises switching cost. Dealers and end-users (global two‑wheeler sales ~50M in 2024) press pricing, financing and after-sales terms.

| Segment | Buyer power | 2024 metric |

|---|---|---|

| Defense/Rail | Very high | 6.9T JPY |

| Aerospace | High | ~25,000 fleet |

| Motorcycles | Medium | ~50M units |

Preview Before You Purchase

Kawasaki Heavy Industries Porter's Five Forces Analysis

This Kawasaki Heavy Industries Porter's Five Forces analysis is the full, professionally formatted report you see in preview—no placeholders or excerpts. It includes supplier, buyer, rivalry, entrant, and substitute assessments and strategic implications. Purchase grants instant access to this exact file, ready to download and use immediately.

Don't Miss the Bigger Picture

Kawasaki Heavy Industries faces intense rivalry, high capital and regulatory barriers, moderated supplier power thanks to scale, and evolving substitute threats from electrification and alternative transport technologies. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kawasaki Heavy Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized materials

Advanced steels, composites and specialty alloys for Kawasaki come from a concentrated base of fewer than 10 qualified global sources, giving suppliers high leverage. Aerospace-grade and marine-class certifications further shrink the pool, and long lead times for forgings and castings — often up to 52 weeks — create intermittent bottlenecks. Kawasaki reduces risk through multisourcing and selective in-house metallurgy capacity expansion.

High-tech components

Semiconductors, sensors, batteries and control systems are concentrated: TSMC held ~56% foundry share in 2024 and CATL ~33% of EV battery capacity, giving suppliers pricing power; 2021–24 chip shocks led to multi-month rationing and 10–20% repricing in some modules. Proprietary design-in raises switching costs, while long-term framework agreements and co-development (joint R&D, multi-year offtakes) have been used to stabilize supply.

Capital equipment vendors

Shipyards and rolling-stock plants at Kawasaki Heavy Industries depend on large machinery and tooling from dominant OEMs such as Mitsubishi Heavy Industries and Siemens Mobility, creating supplier leverage.

Proprietary maintenance parts and spares tie Kawasaki to those vendors, while upgrades and calibrations sustain ongoing dependence.

Negotiated service-level contracts with OEMs partially mitigate cost and downtime risk by securing prioritized support and lead times.

Logistics and yard services

Heavy-lift, dry-dock and specialized transport capacity tightened in 2024 with heavy-lift fleet utilization around 83%, elevating supplier leverage; global port congestion rose, increasing average vessel delay days by about 14% year-on-year and strengthening logistics providers’ bargaining power. Project-level scheduling magnifies exposure to cascading delays, while Kawasaki’s forward booking and captive yard options can cut disruption risk roughly 50%.

- Capacity utilization ~83% (2024)

- Vessel delays +14% YoY (2024)

- Project scheduling = higher delay exposure

- Forward booking/captive yards ≈50% disruption reduction

Energy and utilities

Energy-intensive forging, welding and testing make Kawasaki highly exposed to power suppliers; in 2024 Japan industrial electricity hovered near ¥22–24/kWh and LNG spot markets eased versus 2022–23 peaks, pushing energy to represent roughly 5–12% of heavy-manufacturing OPEX for comparable firms.

- Volatility: electricity/gas price swings drive cost-baseline risk

- Green premiums: renewables procurement can raise input cost but meet customer ESG mandates

- Mitigation: hedging and on-site generation reduce price exposure

Supplier leverage, scarce chips & batteries, logistics tight; multisourcing cuts risk 50%

Supplier power is high: <10 qualified sources for advanced alloys and long lead times (up to 52 weeks) concentrate leverage. Semiconductors (TSMC ~56% foundry share, 2024) and batteries (CATL ~33% capacity, 2024) add pricing power and switching costs. Logistics and heavy-lift tightness (utilization ~83%, 2024) and energy costs (Japan industrial ¥22–24/kWh, 2024) raise input risk; multisourcing, long-term offtakes and forward booking cut disruption ~50%.

| Input | 2024 metric |

|---|---|

| Advanced alloys sources | <10 |

| TSMC foundry share | ~56% |

| CATL EV capacity | ~33% |

| Heavy-lift util. | ~83% |

| Japan ind. electricity | ¥22–24/kWh |

What is included in the product

Tailored Porter's Five Forces analysis of Kawasaki Heavy Industries, assessing competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, and disruptive forces across its transportation, aerospace, and energy segments to inform strategic decisions.

A clear one-sheet Porter's Five Forces summary for Kawasaki Heavy Industries—ideal for quick strategic decisions and boardroom slides. Customize pressure levels with latest market data and view competitive intensity instantly via a spider chart.

Customers Bargaining Power

Government procurement

Rail operators, defense and public agencies buy via tightly specified tenders, and Japan's defense budget reached about 6.9 trillion JPY in 2024, concentrating buyer power and price leverage. Large contract sizes and a small buyer base give customers outsized bargaining power, forcing suppliers to compete on lifecycle cost and localization requirements that squeeze margins. Performance-based contracts commonly extend maintenance and liability obligations for years to decades, locking in after-sales costs and reducing pricing flexibility.

Fleet and OEM customers

Airframe primes and fleet owners, representing a global commercial jet fleet of about 25,000 aircraft in 2024, use volume discounts and design influence to press suppliers like Kawasaki on price and specs. Dual-sourcing norms and multi-year OEM contracts (commonly 5–15 years) keep pricing competitive. Technical certification raises switching costs, but buyers emphasize total cost of ownership and long relationships often trade lower price for proven reliability and support.

Dealer networks

Motorcycle dealers shape retail mix, incentives and inventory turns by choosing which Kawasaki models to prioritize and pressing for floor-plan support and marketing co‑funding; they can demand better terms to protect margins. Dealers' ability to switch to rival brands gives them negotiating leverage, especially in regions with strong multi-brand networks. Kawasaki counters through brand pull, captive finance via Kawasaki Motors Finance and expanded digital retail tools and dealer portals to boost turn and reduce channel friction.

End-user price sensitivity

End-user demand for consumer motorcycles is price-elastic with frequent cross-shopping; global two-wheeler sales were roughly 50 million in 2024, amplifying sensitivity to small price moves. Economic cycles and higher credit costs in 2024 reduced willingness to pay, while features/performance support premiums only within segment limits. Financing offers and after-sales bundles (warranty, service plans) preserve value and close sales.

- Elastic demand

- Credit-driven swings

- Feature-premium cap

- Financing/after-sales

Service and parts leverage

Industrial buyers push Kawasaki for uptime guarantees and predictable spares pricing, turning multi-year service contracts into negotiation focal points; access to diagnostics/data becomes a bargaining chip as customers seek remote-troubleshoot rights and capex predictability. Kawasaki’s extensive installed base strengthens bargaining position on parts volume but obligates long-term support commitments and margin pressure.

- Service contracts: negotiation focal point

- Data access: customer leverage

- Installed base: strength and obligation

Buyers Hold Leverage: Tenders, Fleet Demands and Dealer Pressure Shape Lifecycle Costs

Buyers exert high leverage via large, specified tenders (Japan defense budget ~6.9 trillion JPY in 2024), forcing bids on lifecycle cost and localization. Airframe primes (global fleet ~25,000 aircraft in 2024) drive price and spec demands; certification raises switching cost. Dealers and end-users (global two‑wheeler sales ~50M in 2024) press pricing, financing and after-sales terms.

| Segment | Buyer power | 2024 metric |

|---|---|---|

| Defense/Rail | Very high | 6.9T JPY |

| Aerospace | High | ~25,000 fleet |

| Motorcycles | Medium | ~50M units |

Preview Before You Purchase

Kawasaki Heavy Industries Porter's Five Forces Analysis

This Kawasaki Heavy Industries Porter's Five Forces analysis is the full, professionally formatted report you see in preview—no placeholders or excerpts. It includes supplier, buyer, rivalry, entrant, and substitute assessments and strategic implications. Purchase grants instant access to this exact file, ready to download and use immediately.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Kawasaki Heavy Industries faces intense rivalry, high capital and regulatory barriers, moderated supplier power thanks to scale, and evolving substitute threats from electrification and alternative transport technologies. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kawasaki Heavy Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized materials

Advanced steels, composites and specialty alloys for Kawasaki come from a concentrated base of fewer than 10 qualified global sources, giving suppliers high leverage. Aerospace-grade and marine-class certifications further shrink the pool, and long lead times for forgings and castings — often up to 52 weeks — create intermittent bottlenecks. Kawasaki reduces risk through multisourcing and selective in-house metallurgy capacity expansion.

High-tech components

Semiconductors, sensors, batteries and control systems are concentrated: TSMC held ~56% foundry share in 2024 and CATL ~33% of EV battery capacity, giving suppliers pricing power; 2021–24 chip shocks led to multi-month rationing and 10–20% repricing in some modules. Proprietary design-in raises switching costs, while long-term framework agreements and co-development (joint R&D, multi-year offtakes) have been used to stabilize supply.

Capital equipment vendors

Shipyards and rolling-stock plants at Kawasaki Heavy Industries depend on large machinery and tooling from dominant OEMs such as Mitsubishi Heavy Industries and Siemens Mobility, creating supplier leverage.

Proprietary maintenance parts and spares tie Kawasaki to those vendors, while upgrades and calibrations sustain ongoing dependence.

Negotiated service-level contracts with OEMs partially mitigate cost and downtime risk by securing prioritized support and lead times.

Logistics and yard services

Heavy-lift, dry-dock and specialized transport capacity tightened in 2024 with heavy-lift fleet utilization around 83%, elevating supplier leverage; global port congestion rose, increasing average vessel delay days by about 14% year-on-year and strengthening logistics providers’ bargaining power. Project-level scheduling magnifies exposure to cascading delays, while Kawasaki’s forward booking and captive yard options can cut disruption risk roughly 50%.

- Capacity utilization ~83% (2024)

- Vessel delays +14% YoY (2024)

- Project scheduling = higher delay exposure

- Forward booking/captive yards ≈50% disruption reduction

Energy and utilities

Energy-intensive forging, welding and testing make Kawasaki highly exposed to power suppliers; in 2024 Japan industrial electricity hovered near ¥22–24/kWh and LNG spot markets eased versus 2022–23 peaks, pushing energy to represent roughly 5–12% of heavy-manufacturing OPEX for comparable firms.

- Volatility: electricity/gas price swings drive cost-baseline risk

- Green premiums: renewables procurement can raise input cost but meet customer ESG mandates

- Mitigation: hedging and on-site generation reduce price exposure

Supplier leverage, scarce chips & batteries, logistics tight; multisourcing cuts risk 50%

Supplier power is high: <10 qualified sources for advanced alloys and long lead times (up to 52 weeks) concentrate leverage. Semiconductors (TSMC ~56% foundry share, 2024) and batteries (CATL ~33% capacity, 2024) add pricing power and switching costs. Logistics and heavy-lift tightness (utilization ~83%, 2024) and energy costs (Japan industrial ¥22–24/kWh, 2024) raise input risk; multisourcing, long-term offtakes and forward booking cut disruption ~50%.

| Input | 2024 metric |

|---|---|

| Advanced alloys sources | <10 |

| TSMC foundry share | ~56% |

| CATL EV capacity | ~33% |

| Heavy-lift util. | ~83% |

| Japan ind. electricity | ¥22–24/kWh |

What is included in the product

Tailored Porter's Five Forces analysis of Kawasaki Heavy Industries, assessing competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, and disruptive forces across its transportation, aerospace, and energy segments to inform strategic decisions.

A clear one-sheet Porter's Five Forces summary for Kawasaki Heavy Industries—ideal for quick strategic decisions and boardroom slides. Customize pressure levels with latest market data and view competitive intensity instantly via a spider chart.

Customers Bargaining Power

Government procurement

Rail operators, defense and public agencies buy via tightly specified tenders, and Japan's defense budget reached about 6.9 trillion JPY in 2024, concentrating buyer power and price leverage. Large contract sizes and a small buyer base give customers outsized bargaining power, forcing suppliers to compete on lifecycle cost and localization requirements that squeeze margins. Performance-based contracts commonly extend maintenance and liability obligations for years to decades, locking in after-sales costs and reducing pricing flexibility.

Fleet and OEM customers

Airframe primes and fleet owners, representing a global commercial jet fleet of about 25,000 aircraft in 2024, use volume discounts and design influence to press suppliers like Kawasaki on price and specs. Dual-sourcing norms and multi-year OEM contracts (commonly 5–15 years) keep pricing competitive. Technical certification raises switching costs, but buyers emphasize total cost of ownership and long relationships often trade lower price for proven reliability and support.

Dealer networks

Motorcycle dealers shape retail mix, incentives and inventory turns by choosing which Kawasaki models to prioritize and pressing for floor-plan support and marketing co‑funding; they can demand better terms to protect margins. Dealers' ability to switch to rival brands gives them negotiating leverage, especially in regions with strong multi-brand networks. Kawasaki counters through brand pull, captive finance via Kawasaki Motors Finance and expanded digital retail tools and dealer portals to boost turn and reduce channel friction.

End-user price sensitivity

End-user demand for consumer motorcycles is price-elastic with frequent cross-shopping; global two-wheeler sales were roughly 50 million in 2024, amplifying sensitivity to small price moves. Economic cycles and higher credit costs in 2024 reduced willingness to pay, while features/performance support premiums only within segment limits. Financing offers and after-sales bundles (warranty, service plans) preserve value and close sales.

- Elastic demand

- Credit-driven swings

- Feature-premium cap

- Financing/after-sales

Service and parts leverage

Industrial buyers push Kawasaki for uptime guarantees and predictable spares pricing, turning multi-year service contracts into negotiation focal points; access to diagnostics/data becomes a bargaining chip as customers seek remote-troubleshoot rights and capex predictability. Kawasaki’s extensive installed base strengthens bargaining position on parts volume but obligates long-term support commitments and margin pressure.

- Service contracts: negotiation focal point

- Data access: customer leverage

- Installed base: strength and obligation

Buyers Hold Leverage: Tenders, Fleet Demands and Dealer Pressure Shape Lifecycle Costs

Buyers exert high leverage via large, specified tenders (Japan defense budget ~6.9 trillion JPY in 2024), forcing bids on lifecycle cost and localization. Airframe primes (global fleet ~25,000 aircraft in 2024) drive price and spec demands; certification raises switching cost. Dealers and end-users (global two‑wheeler sales ~50M in 2024) press pricing, financing and after-sales terms.

| Segment | Buyer power | 2024 metric |

|---|---|---|

| Defense/Rail | Very high | 6.9T JPY |

| Aerospace | High | ~25,000 fleet |

| Motorcycles | Medium | ~50M units |

Preview Before You Purchase

Kawasaki Heavy Industries Porter's Five Forces Analysis

This Kawasaki Heavy Industries Porter's Five Forces analysis is the full, professionally formatted report you see in preview—no placeholders or excerpts. It includes supplier, buyer, rivalry, entrant, and substitute assessments and strategic implications. Purchase grants instant access to this exact file, ready to download and use immediately.