KHovnanian Homes Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

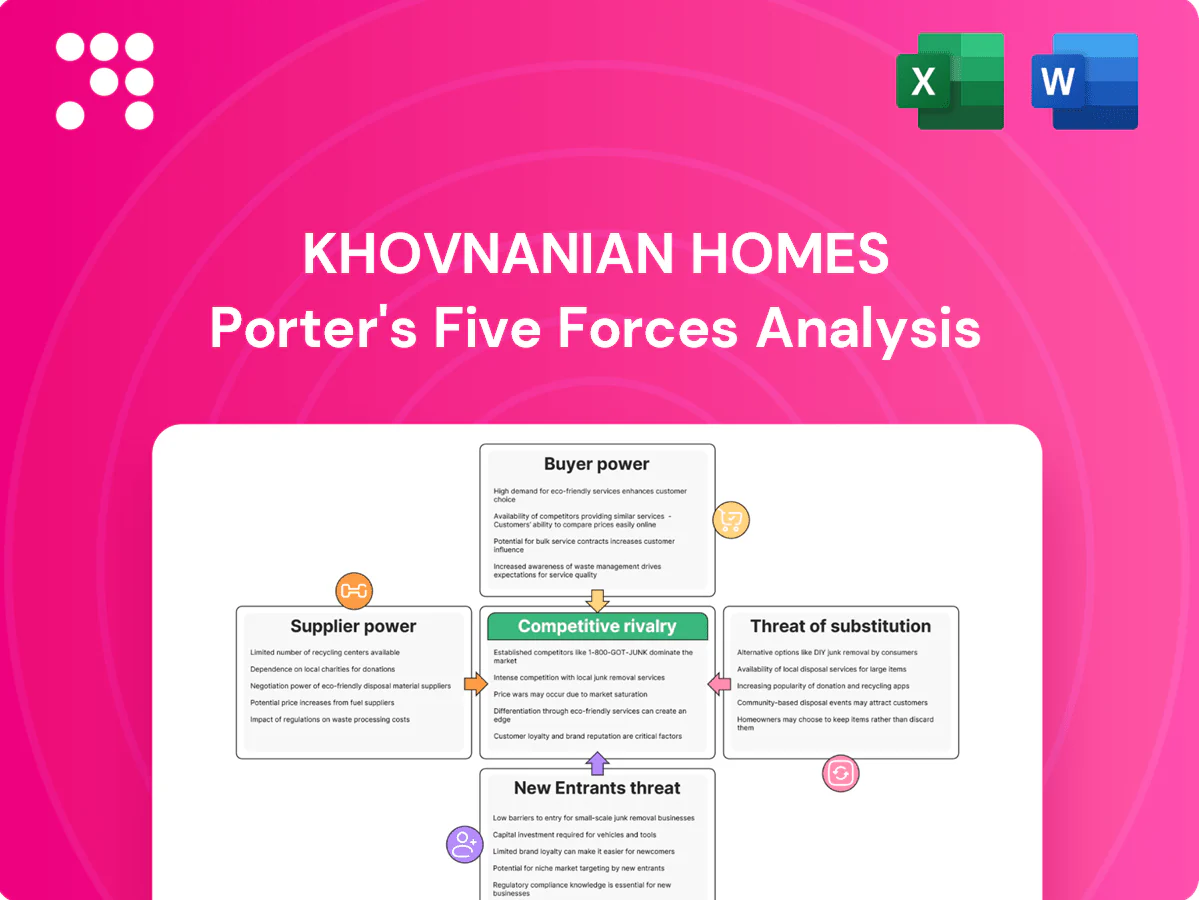

KHovnanian Homes faces moderate buyer power, strong supplier influence on materials, and rising competitive pressure from national and regional builders, while regulatory hurdles and substitute housing models reshape margins. This snapshot highlights key strategic pressures and opportunity areas. Unlock the full Porter's Five Forces Analysis to explore KHovnanian Homes’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated land sellers

In many desirable submarkets buildable lots are controlled by a handful of landowners or entitled land funds, giving sellers leverage to push higher pricing and restrictive terms.

K Hovnanian often competes early for options, increasing deposits and adding escalation clauses to secure parcels while long entitlement timelines extend sellers’ influence.

Diversifying markets and using option structures mitigate but do not eliminate concentrated-seller power.

Material price volatility

Lumber, concrete, steel, roofing and HVAC are sourced from national suppliers with cyclical pricing; commodity swings in 2024 ranged roughly 5–20% across these inputs, with freight adds often compressing mid-build margins. Volume contracts and value engineering mitigate but do not eliminate timing risk. Substitution across SKUs is limited by codes and fixed plans, keeping supplier power elevated.

Subcontractor and labor capacity

Trades like framers, electricians and plumbers remain fragmented but capacity-constrained in hot markets; a 2024 NAHB survey found roughly 86% of builders report subcontractor shortages. Wage inflation and crew availability drive cycle times and costs, while KHov’s multi-community pipeline helps attract crews yet peak demand shifts bargaining power to subs; quality-control needs further limit switching.

Municipalities and utilities

Municipalities and utilities function as quasi-suppliers with gatekeeper power: permanent power, water taps, inspections and permits can dictate start-to-close timing and add carrying costs when schedules slip.

Fee schedules and local timelines often delay closings; strong relationships and proactive scheduling reduce friction but cannot eliminate backlog or sudden regulatory shifts that instantly raise costs.

- Gatekeeper functions: permits, inspections, taps

- Impact: delayed closings → higher carrying costs

- Mitigation: relationships, proactive scheduling

- Residual risk: local backlog and regulatory shocks

Specialty inputs and lead times

Windows, doors, appliances and cabinetry create plan-level micro-monopolies for K. Hovnanian as brand/spec constraints limit substitution; 2024 lead-time spikes—often 8–12+ weeks for windows—force redesigns or buyer incentives to close. Multi-vendor qualification and spec flexibility reduce exposure, but buyer finish expectations cap substitution and margin recovery.

- Brand/spec lock-in

- 8–12+ week lead times (2024)

- Multi-vendor mitigation

- Finish-driven substitution limits

Supplier power tightens: commodity swings 5–20%, subs shortage ~86%

Supplier power is elevated: land concentration and option competition tighten parcel access, commodity inputs swung roughly 5–20% in 2024, and specialized finish lead times (windows) ran 8–12+ weeks. Subcontractor capacity is constrained—NAHB 2024 found ~86% of builders report shortages—while permits/utilities act as gatekeepers that add timing/carry costs.

| Metric | 2024 |

|---|---|

| Commodity input swings | 5–20% |

| Subcontractor shortage (NAHB) | ~86% |

| Window lead times | 8–12+ weeks |

What is included in the product

Tailored Porter's Five Forces analysis for KHovnanian Homes that uncovers competitive intensity, buyer and supplier power, entry barriers, substitutes, and disruptive threats, with strategic commentary on pricing leverage, market positioning, and risks to profitability.

A one-sheet Porter’s Five Forces for K. Hovnanian that distills competitive pressure into an actionable radar chart—customize force levels, swap your data, and drop it straight into decks to quickly relieve strategic uncertainty and guide execution.

Customers Bargaining Power

High price sensitivity

Homebuyers compare monthly payments across builders and resale options; with the 30-year fixed averaging about 6.8% in 2024 (Freddie Mac), small rate moves materially change affordability. A 1 percentage-point rise increases payments roughly $250/month on a $400,000 mortgage, shifting buyer choices. KHovnanian must calibrate incentives to clear inventory without eroding brand, while value messaging and energy-efficiency features soften pure price comparisons.

Mortgage rate dependence

Mortgage-rate swings materially increase buyer leverage as payment shock is tangible—each 1% rise boosts monthly payments on a $400,000 mortgage by roughly $240, so buyers push harder on price and concessions. Rate buydowns and closing-cost credits have become negotiation norms, while captive or preferred lenders help K. Hovnanian streamline approvals and lock rates for buyers. Prolonged high rates in 2024 widened buyer concession expectations across markets.

Information transparency

Online listings, MLS data and reviews drive transparency—NAR 2024 reports about 97% of buyers used the internet to search homes—letting shoppers cross-shop specs, lot sizes and HOA fees instantly. KHovnanian’s digital sales tools and virtual tours increase lead conversion and time-on-listing. However, this transparency compresses pricing dispersion across nearby comps, narrowing margins and limiting localized price flexibility.

Low switching costs pre-contract

Until earnest money and design selections are locked—earnest deposits commonly 1–3% of purchase price—buyers switch readily, so pre-qual funnels must accelerate to secure contracts; personalization and community amenities increase emotional switching costs, yet cancellable options and standard contingencies (inspection, finance) keep leverage with buyers.

- Low switching costs pre-contract

- Earnest money 1–3%

- Fast pre-qual to contract

- Personalization raises emotional cost

- Contingencies preserve buyer leverage

Segment heterogeneity

First-time, move-up, luxury and active-adult buyers exert varying bargaining power; first-time buyers are most rate- and incentive-sensitive with first-time purchasers at 31% of buyers in 2024 and 30-year rates near 7% in 2024, while luxury buyers trade price for customization and strict timelines; tailored product-series and curated upgrade packages help KHovnanian rebalance negotiating leverage across segments.

- first-time: 31% share in 2024

- rate context: ~7% 30-year mortgage (2024)

- luxury: customization > price

- strategy: product-series + curated upgrades

Buyers leverage: 30y 6.8%, 1pp ≈ $250/mo on $400k

Buyers have strong leverage: 30-year avg 6.8% in 2024, where a 1pp rise adds ≈$250/month on a $400k mortgage, increasing demand for buydowns and credits. Online search (97% buyers, NAR 2024) and low pre-contract switching (earnest 1–3%) compress margins; segmentation (first-time 31%) shifts bargaining dynamics.

| Metric | 2024 |

|---|---|

| 30y rate | 6.8% |

| First-time share | 31% |

| Online search | 97% |

| Earnest | 1–3% |

What You See Is What You Get

KHovnanian Homes Porter's Five Forces Analysis

This preview displays the exact K. Hovnanian Homes Porter’s Five Forces analysis you’ll receive upon purchase—no placeholders or samples. The full document is professionally formatted, ready for immediate download and use, and contains a complete, actionable assessment of competitive forces affecting the business. Purchase grants instant access to this identical file.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

KHovnanian Homes faces moderate buyer power, strong supplier influence on materials, and rising competitive pressure from national and regional builders, while regulatory hurdles and substitute housing models reshape margins. This snapshot highlights key strategic pressures and opportunity areas. Unlock the full Porter's Five Forces Analysis to explore KHovnanian Homes’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated land sellers

In many desirable submarkets buildable lots are controlled by a handful of landowners or entitled land funds, giving sellers leverage to push higher pricing and restrictive terms.

K Hovnanian often competes early for options, increasing deposits and adding escalation clauses to secure parcels while long entitlement timelines extend sellers’ influence.

Diversifying markets and using option structures mitigate but do not eliminate concentrated-seller power.

Material price volatility

Lumber, concrete, steel, roofing and HVAC are sourced from national suppliers with cyclical pricing; commodity swings in 2024 ranged roughly 5–20% across these inputs, with freight adds often compressing mid-build margins. Volume contracts and value engineering mitigate but do not eliminate timing risk. Substitution across SKUs is limited by codes and fixed plans, keeping supplier power elevated.

Subcontractor and labor capacity

Trades like framers, electricians and plumbers remain fragmented but capacity-constrained in hot markets; a 2024 NAHB survey found roughly 86% of builders report subcontractor shortages. Wage inflation and crew availability drive cycle times and costs, while KHov’s multi-community pipeline helps attract crews yet peak demand shifts bargaining power to subs; quality-control needs further limit switching.

Municipalities and utilities

Municipalities and utilities function as quasi-suppliers with gatekeeper power: permanent power, water taps, inspections and permits can dictate start-to-close timing and add carrying costs when schedules slip.

Fee schedules and local timelines often delay closings; strong relationships and proactive scheduling reduce friction but cannot eliminate backlog or sudden regulatory shifts that instantly raise costs.

- Gatekeeper functions: permits, inspections, taps

- Impact: delayed closings → higher carrying costs

- Mitigation: relationships, proactive scheduling

- Residual risk: local backlog and regulatory shocks

Specialty inputs and lead times

Windows, doors, appliances and cabinetry create plan-level micro-monopolies for K. Hovnanian as brand/spec constraints limit substitution; 2024 lead-time spikes—often 8–12+ weeks for windows—force redesigns or buyer incentives to close. Multi-vendor qualification and spec flexibility reduce exposure, but buyer finish expectations cap substitution and margin recovery.

- Brand/spec lock-in

- 8–12+ week lead times (2024)

- Multi-vendor mitigation

- Finish-driven substitution limits

Supplier power tightens: commodity swings 5–20%, subs shortage ~86%

Supplier power is elevated: land concentration and option competition tighten parcel access, commodity inputs swung roughly 5–20% in 2024, and specialized finish lead times (windows) ran 8–12+ weeks. Subcontractor capacity is constrained—NAHB 2024 found ~86% of builders report shortages—while permits/utilities act as gatekeepers that add timing/carry costs.

| Metric | 2024 |

|---|---|

| Commodity input swings | 5–20% |

| Subcontractor shortage (NAHB) | ~86% |

| Window lead times | 8–12+ weeks |

What is included in the product

Tailored Porter's Five Forces analysis for KHovnanian Homes that uncovers competitive intensity, buyer and supplier power, entry barriers, substitutes, and disruptive threats, with strategic commentary on pricing leverage, market positioning, and risks to profitability.

A one-sheet Porter’s Five Forces for K. Hovnanian that distills competitive pressure into an actionable radar chart—customize force levels, swap your data, and drop it straight into decks to quickly relieve strategic uncertainty and guide execution.

Customers Bargaining Power

High price sensitivity

Homebuyers compare monthly payments across builders and resale options; with the 30-year fixed averaging about 6.8% in 2024 (Freddie Mac), small rate moves materially change affordability. A 1 percentage-point rise increases payments roughly $250/month on a $400,000 mortgage, shifting buyer choices. KHovnanian must calibrate incentives to clear inventory without eroding brand, while value messaging and energy-efficiency features soften pure price comparisons.

Mortgage rate dependence

Mortgage-rate swings materially increase buyer leverage as payment shock is tangible—each 1% rise boosts monthly payments on a $400,000 mortgage by roughly $240, so buyers push harder on price and concessions. Rate buydowns and closing-cost credits have become negotiation norms, while captive or preferred lenders help K. Hovnanian streamline approvals and lock rates for buyers. Prolonged high rates in 2024 widened buyer concession expectations across markets.

Information transparency

Online listings, MLS data and reviews drive transparency—NAR 2024 reports about 97% of buyers used the internet to search homes—letting shoppers cross-shop specs, lot sizes and HOA fees instantly. KHovnanian’s digital sales tools and virtual tours increase lead conversion and time-on-listing. However, this transparency compresses pricing dispersion across nearby comps, narrowing margins and limiting localized price flexibility.

Low switching costs pre-contract

Until earnest money and design selections are locked—earnest deposits commonly 1–3% of purchase price—buyers switch readily, so pre-qual funnels must accelerate to secure contracts; personalization and community amenities increase emotional switching costs, yet cancellable options and standard contingencies (inspection, finance) keep leverage with buyers.

- Low switching costs pre-contract

- Earnest money 1–3%

- Fast pre-qual to contract

- Personalization raises emotional cost

- Contingencies preserve buyer leverage

Segment heterogeneity

First-time, move-up, luxury and active-adult buyers exert varying bargaining power; first-time buyers are most rate- and incentive-sensitive with first-time purchasers at 31% of buyers in 2024 and 30-year rates near 7% in 2024, while luxury buyers trade price for customization and strict timelines; tailored product-series and curated upgrade packages help KHovnanian rebalance negotiating leverage across segments.

- first-time: 31% share in 2024

- rate context: ~7% 30-year mortgage (2024)

- luxury: customization > price

- strategy: product-series + curated upgrades

Buyers leverage: 30y 6.8%, 1pp ≈ $250/mo on $400k

Buyers have strong leverage: 30-year avg 6.8% in 2024, where a 1pp rise adds ≈$250/month on a $400k mortgage, increasing demand for buydowns and credits. Online search (97% buyers, NAR 2024) and low pre-contract switching (earnest 1–3%) compress margins; segmentation (first-time 31%) shifts bargaining dynamics.

| Metric | 2024 |

|---|---|

| 30y rate | 6.8% |

| First-time share | 31% |

| Online search | 97% |

| Earnest | 1–3% |

What You See Is What You Get

KHovnanian Homes Porter's Five Forces Analysis

This preview displays the exact K. Hovnanian Homes Porter’s Five Forces analysis you’ll receive upon purchase—no placeholders or samples. The full document is professionally formatted, ready for immediate download and use, and contains a complete, actionable assessment of competitive forces affecting the business. Purchase grants instant access to this identical file.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

KHovnanian Homes faces moderate buyer power, strong supplier influence on materials, and rising competitive pressure from national and regional builders, while regulatory hurdles and substitute housing models reshape margins. This snapshot highlights key strategic pressures and opportunity areas. Unlock the full Porter's Five Forces Analysis to explore KHovnanian Homes’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated land sellers

In many desirable submarkets buildable lots are controlled by a handful of landowners or entitled land funds, giving sellers leverage to push higher pricing and restrictive terms.

K Hovnanian often competes early for options, increasing deposits and adding escalation clauses to secure parcels while long entitlement timelines extend sellers’ influence.

Diversifying markets and using option structures mitigate but do not eliminate concentrated-seller power.

Material price volatility

Lumber, concrete, steel, roofing and HVAC are sourced from national suppliers with cyclical pricing; commodity swings in 2024 ranged roughly 5–20% across these inputs, with freight adds often compressing mid-build margins. Volume contracts and value engineering mitigate but do not eliminate timing risk. Substitution across SKUs is limited by codes and fixed plans, keeping supplier power elevated.

Subcontractor and labor capacity

Trades like framers, electricians and plumbers remain fragmented but capacity-constrained in hot markets; a 2024 NAHB survey found roughly 86% of builders report subcontractor shortages. Wage inflation and crew availability drive cycle times and costs, while KHov’s multi-community pipeline helps attract crews yet peak demand shifts bargaining power to subs; quality-control needs further limit switching.

Municipalities and utilities

Municipalities and utilities function as quasi-suppliers with gatekeeper power: permanent power, water taps, inspections and permits can dictate start-to-close timing and add carrying costs when schedules slip.

Fee schedules and local timelines often delay closings; strong relationships and proactive scheduling reduce friction but cannot eliminate backlog or sudden regulatory shifts that instantly raise costs.

- Gatekeeper functions: permits, inspections, taps

- Impact: delayed closings → higher carrying costs

- Mitigation: relationships, proactive scheduling

- Residual risk: local backlog and regulatory shocks

Specialty inputs and lead times

Windows, doors, appliances and cabinetry create plan-level micro-monopolies for K. Hovnanian as brand/spec constraints limit substitution; 2024 lead-time spikes—often 8–12+ weeks for windows—force redesigns or buyer incentives to close. Multi-vendor qualification and spec flexibility reduce exposure, but buyer finish expectations cap substitution and margin recovery.

- Brand/spec lock-in

- 8–12+ week lead times (2024)

- Multi-vendor mitigation

- Finish-driven substitution limits

Supplier power tightens: commodity swings 5–20%, subs shortage ~86%

Supplier power is elevated: land concentration and option competition tighten parcel access, commodity inputs swung roughly 5–20% in 2024, and specialized finish lead times (windows) ran 8–12+ weeks. Subcontractor capacity is constrained—NAHB 2024 found ~86% of builders report shortages—while permits/utilities act as gatekeepers that add timing/carry costs.

| Metric | 2024 |

|---|---|

| Commodity input swings | 5–20% |

| Subcontractor shortage (NAHB) | ~86% |

| Window lead times | 8–12+ weeks |

What is included in the product

Tailored Porter's Five Forces analysis for KHovnanian Homes that uncovers competitive intensity, buyer and supplier power, entry barriers, substitutes, and disruptive threats, with strategic commentary on pricing leverage, market positioning, and risks to profitability.

A one-sheet Porter’s Five Forces for K. Hovnanian that distills competitive pressure into an actionable radar chart—customize force levels, swap your data, and drop it straight into decks to quickly relieve strategic uncertainty and guide execution.

Customers Bargaining Power

High price sensitivity

Homebuyers compare monthly payments across builders and resale options; with the 30-year fixed averaging about 6.8% in 2024 (Freddie Mac), small rate moves materially change affordability. A 1 percentage-point rise increases payments roughly $250/month on a $400,000 mortgage, shifting buyer choices. KHovnanian must calibrate incentives to clear inventory without eroding brand, while value messaging and energy-efficiency features soften pure price comparisons.

Mortgage rate dependence

Mortgage-rate swings materially increase buyer leverage as payment shock is tangible—each 1% rise boosts monthly payments on a $400,000 mortgage by roughly $240, so buyers push harder on price and concessions. Rate buydowns and closing-cost credits have become negotiation norms, while captive or preferred lenders help K. Hovnanian streamline approvals and lock rates for buyers. Prolonged high rates in 2024 widened buyer concession expectations across markets.

Information transparency

Online listings, MLS data and reviews drive transparency—NAR 2024 reports about 97% of buyers used the internet to search homes—letting shoppers cross-shop specs, lot sizes and HOA fees instantly. KHovnanian’s digital sales tools and virtual tours increase lead conversion and time-on-listing. However, this transparency compresses pricing dispersion across nearby comps, narrowing margins and limiting localized price flexibility.

Low switching costs pre-contract

Until earnest money and design selections are locked—earnest deposits commonly 1–3% of purchase price—buyers switch readily, so pre-qual funnels must accelerate to secure contracts; personalization and community amenities increase emotional switching costs, yet cancellable options and standard contingencies (inspection, finance) keep leverage with buyers.

- Low switching costs pre-contract

- Earnest money 1–3%

- Fast pre-qual to contract

- Personalization raises emotional cost

- Contingencies preserve buyer leverage

Segment heterogeneity

First-time, move-up, luxury and active-adult buyers exert varying bargaining power; first-time buyers are most rate- and incentive-sensitive with first-time purchasers at 31% of buyers in 2024 and 30-year rates near 7% in 2024, while luxury buyers trade price for customization and strict timelines; tailored product-series and curated upgrade packages help KHovnanian rebalance negotiating leverage across segments.

- first-time: 31% share in 2024

- rate context: ~7% 30-year mortgage (2024)

- luxury: customization > price

- strategy: product-series + curated upgrades

Buyers leverage: 30y 6.8%, 1pp ≈ $250/mo on $400k

Buyers have strong leverage: 30-year avg 6.8% in 2024, where a 1pp rise adds ≈$250/month on a $400k mortgage, increasing demand for buydowns and credits. Online search (97% buyers, NAR 2024) and low pre-contract switching (earnest 1–3%) compress margins; segmentation (first-time 31%) shifts bargaining dynamics.

| Metric | 2024 |

|---|---|

| 30y rate | 6.8% |

| First-time share | 31% |

| Online search | 97% |

| Earnest | 1–3% |

What You See Is What You Get

KHovnanian Homes Porter's Five Forces Analysis

This preview displays the exact K. Hovnanian Homes Porter’s Five Forces analysis you’ll receive upon purchase—no placeholders or samples. The full document is professionally formatted, ready for immediate download and use, and contains a complete, actionable assessment of competitive forces affecting the business. Purchase grants instant access to this identical file.