Kier Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Kier Group’s Porter’s Five Forces snapshot highlights supplier leverage, buyer pressure, substitute risks and barriers to entry shaping its construction and services markets. This brief overview signals strategic vulnerabilities and opportunities but omits force-by-force ratings and visuals. Unlock the full Porter’s Five Forces Analysis for a consultant-grade, data-driven breakdown tailored to Kier Group to inform strategy and investment decisions.

Suppliers Bargaining Power

Specialist subcontractor dependence

Complex Kier projects depend on niche trades (M&E, rail systems, signalling) that remain capacity constrained, concentrating bargaining power with top-tier specialists. High switching costs and qualification timelines often lock suppliers mid-project, with specialist lead times commonly stretching several months in 2024. Supplier delays or price rises cascade through programme schedules, amplifying cost and timeline risk for Kier.

Volatile input costs and commodities

Steel, cement, asphalt, aggregates and energy drive input-cost risk for Kier; Brent crude averaged about $87/barrel in 2024, keeping fuel and asphalt costs elevated and enabling suppliers to pass inflation through index-linked clauses that tighten margins. Hedging and long-term framework pricing reduce exposure but cannot eliminate sudden commodity spikes. Prolonged volatility forces stricter bid discipline and larger contingency allowances, pressuring tender competitiveness and profitability.

Plant, equipment, and OEM parts

Access to heavy plant and proprietary components creates bottlenecks for Kier, with 2024 industry reports noting TBM lead times of 18–24 months and signalling/ITS OEM windows of 12–36 months. OEM lead times give equipment suppliers leverage over scheduling and pricing. Maintenance and spares contracts embed vendor lock-in, and availability constraints can force costly resequencing and idle plant on multi‑site projects.

Digital, BIM, and data platform vendors

Digital, BIM and data platform vendors are concentrated around Autodesk, Bentley and Trimble as of 2024, creating high switching costs on live programmes due to limited interoperability and entrenched toolchains. Licensing, bespoke integrations and vendor support materially raise total cost of ownership, while cyber obligations and uptime SLAs are frequent negotiation choke points.

- Vendor concentration: Autodesk, Bentley, Trimble (2024)

- High switching barriers: limited interoperability

- TCO drivers: licensing + integration support

- Risk focus: cyber liability and uptime SLAs

Sustainability and low-carbon materials

- BES 6001: fewer compliant vendors

- 2024: low-carbon premium up to 15%

- Smaller pools = higher supplier leverage

- Fixed-price contracts vulnerable to margin squeeze

M&E/rail supply squeeze: lead times 3–24m, Brent $87/bbl, low-carbon 15%

Complex Kier projects rely on niche M&E/rail specialists with 2024 lead times of 3–24 months, concentrating supplier leverage. Commodity pressure (Brent ~$87/bbl in 2024) and low‑carbon premiums (~15%) squeeze margins on fixed‑price work. OEM/plant bottlenecks (TBM 18–24m) and concentrated software vendors raise switching costs and schedule risk.

| Metric | 2024 |

|---|---|

| Brent | $87/bbl |

| Low‑carbon premium | up to 15% |

| TBM lead time | 18–24 months |

| Signalling OEM | 12–36 months |

What is included in the product

Tailored Porter’s Five Forces analysis of Kier Group uncovering key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging disruptive threats to its market position, with strategic commentary for stakeholders.

A concise Porter's Five Forces one-sheet for Kier Group that visualizes competitive pressures, supplier/customer leverage and regulatory risk—streamlining boardroom decisions and strategic scenario planning.

Customers Bargaining Power

Public sector buyer concentration

Central government, agencies and local authorities control large frameworks representing over 50% of Kier’s order book in 2024, giving buyers strong leverage on price and contract terms. High spend concentration drives aggressive competitive tenders and multi-lot frameworks, intensifying price pressure and compressing margins with typical bid discounts often exceeding 5%. Payment terms (commonly 30–60 days) and social value weightings—frequently up to 20%— materially shape bid economics and contractor cashflow.

Frameworks and performance gating

Framework reappointment for Kier increasingly hinges on 2024 KPIs covering time, cost, safety and carbon, with buyers using performance scorecards to extract commercial concessions and change orders. Poor scorecard outcomes can restrict access to future public and private pipelines, amplifying buyer bargaining power. Gainshare/painshare clauses adopted in 2024 shift upside and downside risk onto contractors, compressing margins and negotiating leverage.

Technical specifications and design control

Clients dictate design standards and approvals on regulated assets, squeezing Kier’s margins as tight oversight increased; Kier reported 2024 revenue of about £4.0bn with continued focus on regulated sectors. Scope creep and change control compress margins on projects where client-approved variations rose materially in 2024. Value-engineering wins are often client-approved, limiting contractor capture of savings. Design-and-build shifts delivery risk to Kier while clients retain strong oversight.

Transparent market pricing

Transparent market pricing has strengthened buyer leverage over Kier as benchmarking and industry cost databases make supplier rates comparable, while should-cost models in 2024 narrowed information asymmetry and drove tougher negotiations. Open-book contracts cap supplier upside and expose line-item costs, and public-sector buyers increasingly reserve the right to re-tender packages when pricing diverges from benchmarks; Kier’s 2024 revenue of £4.2bn increases the stakes of such pressures.

- Benchmarks: faster price discovery

- Should-cost models: reduced asymmetry

- Open-book: capped margins, exposed costs

- Re-tendering: enforces market-aligned pricing

ESG and community outcomes

Buyers now insist on measurable social value, apprenticeships and credible net-zero pathways, expanding scope without proportional price uplift; UK law sets a net-zero target by 2050 and the Social Value Act 2012 requires public buyers to consider social value. Failure to meet these non-price criteria can disqualify bids and reduce future pipeline, forcing contractors to invest upfront to remain eligible.

- Buyers: social value, apprenticeships, net-zero

- Impact: expanded deliverables, limited price uplift

- Risk: disqualification, lost future work

- Action: upfront investment to retain eligibility

Public sector >50% of 2024 order book; £4.0bn revenue; >5% bid discounts

Public sector accounts for >50% of Kier’s 2024 order book, giving buyers strong leverage on price and terms; typical bid discounts exceed 5% and payment terms are 30–60 days. KPI/social value weightings (often up to 20%) and open-book/should-cost models compress margins and shift risk to contractors. Kier reported ~£4.0bn revenue in 2024, raising stakes of re-tendering and performance clauses.

| Metric | 2024 | Impact |

|---|---|---|

| Public share | >50% | High buyer leverage |

| Revenue | £4.0bn | Scale risk exposure |

| Bid discount | >5% | Margin compression |

Full Version Awaits

Kier Group Porter's Five Forces Analysis

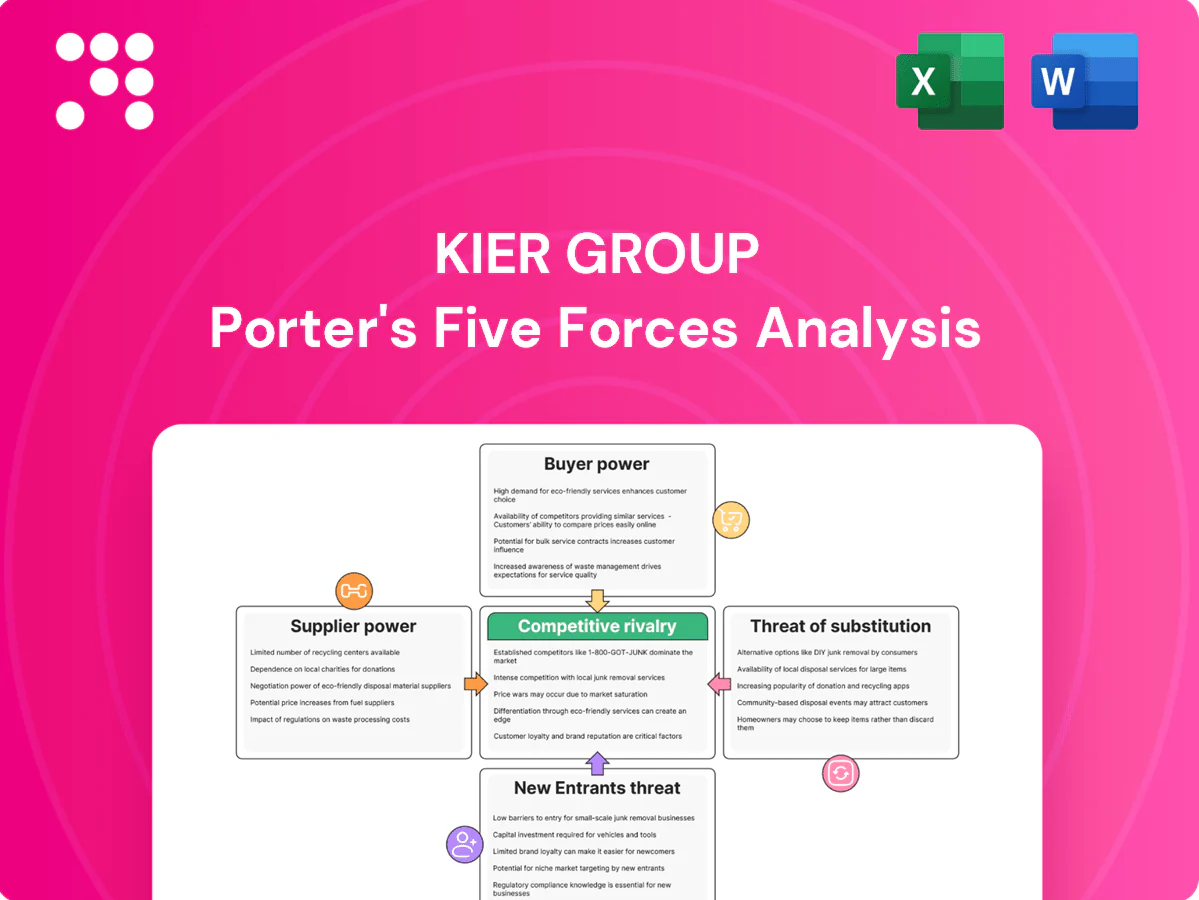

This Porter's Five Forces analysis of Kier Group examines supplier power, buyer power, competitive rivalry, threat of substitutes and barriers to entry to assess the firm's strategic position. You're previewing the final version—precisely the same document that will be available to you instantly after buying. Fully formatted and ready to use for decision-making or reporting.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Kier Group’s Porter’s Five Forces snapshot highlights supplier leverage, buyer pressure, substitute risks and barriers to entry shaping its construction and services markets. This brief overview signals strategic vulnerabilities and opportunities but omits force-by-force ratings and visuals. Unlock the full Porter’s Five Forces Analysis for a consultant-grade, data-driven breakdown tailored to Kier Group to inform strategy and investment decisions.

Suppliers Bargaining Power

Specialist subcontractor dependence

Complex Kier projects depend on niche trades (M&E, rail systems, signalling) that remain capacity constrained, concentrating bargaining power with top-tier specialists. High switching costs and qualification timelines often lock suppliers mid-project, with specialist lead times commonly stretching several months in 2024. Supplier delays or price rises cascade through programme schedules, amplifying cost and timeline risk for Kier.

Volatile input costs and commodities

Steel, cement, asphalt, aggregates and energy drive input-cost risk for Kier; Brent crude averaged about $87/barrel in 2024, keeping fuel and asphalt costs elevated and enabling suppliers to pass inflation through index-linked clauses that tighten margins. Hedging and long-term framework pricing reduce exposure but cannot eliminate sudden commodity spikes. Prolonged volatility forces stricter bid discipline and larger contingency allowances, pressuring tender competitiveness and profitability.

Plant, equipment, and OEM parts

Access to heavy plant and proprietary components creates bottlenecks for Kier, with 2024 industry reports noting TBM lead times of 18–24 months and signalling/ITS OEM windows of 12–36 months. OEM lead times give equipment suppliers leverage over scheduling and pricing. Maintenance and spares contracts embed vendor lock-in, and availability constraints can force costly resequencing and idle plant on multi‑site projects.

Digital, BIM, and data platform vendors

Digital, BIM and data platform vendors are concentrated around Autodesk, Bentley and Trimble as of 2024, creating high switching costs on live programmes due to limited interoperability and entrenched toolchains. Licensing, bespoke integrations and vendor support materially raise total cost of ownership, while cyber obligations and uptime SLAs are frequent negotiation choke points.

- Vendor concentration: Autodesk, Bentley, Trimble (2024)

- High switching barriers: limited interoperability

- TCO drivers: licensing + integration support

- Risk focus: cyber liability and uptime SLAs

Sustainability and low-carbon materials

- BES 6001: fewer compliant vendors

- 2024: low-carbon premium up to 15%

- Smaller pools = higher supplier leverage

- Fixed-price contracts vulnerable to margin squeeze

M&E/rail supply squeeze: lead times 3–24m, Brent $87/bbl, low-carbon 15%

Complex Kier projects rely on niche M&E/rail specialists with 2024 lead times of 3–24 months, concentrating supplier leverage. Commodity pressure (Brent ~$87/bbl in 2024) and low‑carbon premiums (~15%) squeeze margins on fixed‑price work. OEM/plant bottlenecks (TBM 18–24m) and concentrated software vendors raise switching costs and schedule risk.

| Metric | 2024 |

|---|---|

| Brent | $87/bbl |

| Low‑carbon premium | up to 15% |

| TBM lead time | 18–24 months |

| Signalling OEM | 12–36 months |

What is included in the product

Tailored Porter’s Five Forces analysis of Kier Group uncovering key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging disruptive threats to its market position, with strategic commentary for stakeholders.

A concise Porter's Five Forces one-sheet for Kier Group that visualizes competitive pressures, supplier/customer leverage and regulatory risk—streamlining boardroom decisions and strategic scenario planning.

Customers Bargaining Power

Public sector buyer concentration

Central government, agencies and local authorities control large frameworks representing over 50% of Kier’s order book in 2024, giving buyers strong leverage on price and contract terms. High spend concentration drives aggressive competitive tenders and multi-lot frameworks, intensifying price pressure and compressing margins with typical bid discounts often exceeding 5%. Payment terms (commonly 30–60 days) and social value weightings—frequently up to 20%— materially shape bid economics and contractor cashflow.

Frameworks and performance gating

Framework reappointment for Kier increasingly hinges on 2024 KPIs covering time, cost, safety and carbon, with buyers using performance scorecards to extract commercial concessions and change orders. Poor scorecard outcomes can restrict access to future public and private pipelines, amplifying buyer bargaining power. Gainshare/painshare clauses adopted in 2024 shift upside and downside risk onto contractors, compressing margins and negotiating leverage.

Technical specifications and design control

Clients dictate design standards and approvals on regulated assets, squeezing Kier’s margins as tight oversight increased; Kier reported 2024 revenue of about £4.0bn with continued focus on regulated sectors. Scope creep and change control compress margins on projects where client-approved variations rose materially in 2024. Value-engineering wins are often client-approved, limiting contractor capture of savings. Design-and-build shifts delivery risk to Kier while clients retain strong oversight.

Transparent market pricing

Transparent market pricing has strengthened buyer leverage over Kier as benchmarking and industry cost databases make supplier rates comparable, while should-cost models in 2024 narrowed information asymmetry and drove tougher negotiations. Open-book contracts cap supplier upside and expose line-item costs, and public-sector buyers increasingly reserve the right to re-tender packages when pricing diverges from benchmarks; Kier’s 2024 revenue of £4.2bn increases the stakes of such pressures.

- Benchmarks: faster price discovery

- Should-cost models: reduced asymmetry

- Open-book: capped margins, exposed costs

- Re-tendering: enforces market-aligned pricing

ESG and community outcomes

Buyers now insist on measurable social value, apprenticeships and credible net-zero pathways, expanding scope without proportional price uplift; UK law sets a net-zero target by 2050 and the Social Value Act 2012 requires public buyers to consider social value. Failure to meet these non-price criteria can disqualify bids and reduce future pipeline, forcing contractors to invest upfront to remain eligible.

- Buyers: social value, apprenticeships, net-zero

- Impact: expanded deliverables, limited price uplift

- Risk: disqualification, lost future work

- Action: upfront investment to retain eligibility

Public sector >50% of 2024 order book; £4.0bn revenue; >5% bid discounts

Public sector accounts for >50% of Kier’s 2024 order book, giving buyers strong leverage on price and terms; typical bid discounts exceed 5% and payment terms are 30–60 days. KPI/social value weightings (often up to 20%) and open-book/should-cost models compress margins and shift risk to contractors. Kier reported ~£4.0bn revenue in 2024, raising stakes of re-tendering and performance clauses.

| Metric | 2024 | Impact |

|---|---|---|

| Public share | >50% | High buyer leverage |

| Revenue | £4.0bn | Scale risk exposure |

| Bid discount | >5% | Margin compression |

Full Version Awaits

Kier Group Porter's Five Forces Analysis

This Porter's Five Forces analysis of Kier Group examines supplier power, buyer power, competitive rivalry, threat of substitutes and barriers to entry to assess the firm's strategic position. You're previewing the final version—precisely the same document that will be available to you instantly after buying. Fully formatted and ready to use for decision-making or reporting.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Kier Group’s Porter’s Five Forces snapshot highlights supplier leverage, buyer pressure, substitute risks and barriers to entry shaping its construction and services markets. This brief overview signals strategic vulnerabilities and opportunities but omits force-by-force ratings and visuals. Unlock the full Porter’s Five Forces Analysis for a consultant-grade, data-driven breakdown tailored to Kier Group to inform strategy and investment decisions.

Suppliers Bargaining Power

Specialist subcontractor dependence

Complex Kier projects depend on niche trades (M&E, rail systems, signalling) that remain capacity constrained, concentrating bargaining power with top-tier specialists. High switching costs and qualification timelines often lock suppliers mid-project, with specialist lead times commonly stretching several months in 2024. Supplier delays or price rises cascade through programme schedules, amplifying cost and timeline risk for Kier.

Volatile input costs and commodities

Steel, cement, asphalt, aggregates and energy drive input-cost risk for Kier; Brent crude averaged about $87/barrel in 2024, keeping fuel and asphalt costs elevated and enabling suppliers to pass inflation through index-linked clauses that tighten margins. Hedging and long-term framework pricing reduce exposure but cannot eliminate sudden commodity spikes. Prolonged volatility forces stricter bid discipline and larger contingency allowances, pressuring tender competitiveness and profitability.

Plant, equipment, and OEM parts

Access to heavy plant and proprietary components creates bottlenecks for Kier, with 2024 industry reports noting TBM lead times of 18–24 months and signalling/ITS OEM windows of 12–36 months. OEM lead times give equipment suppliers leverage over scheduling and pricing. Maintenance and spares contracts embed vendor lock-in, and availability constraints can force costly resequencing and idle plant on multi‑site projects.

Digital, BIM, and data platform vendors

Digital, BIM and data platform vendors are concentrated around Autodesk, Bentley and Trimble as of 2024, creating high switching costs on live programmes due to limited interoperability and entrenched toolchains. Licensing, bespoke integrations and vendor support materially raise total cost of ownership, while cyber obligations and uptime SLAs are frequent negotiation choke points.

- Vendor concentration: Autodesk, Bentley, Trimble (2024)

- High switching barriers: limited interoperability

- TCO drivers: licensing + integration support

- Risk focus: cyber liability and uptime SLAs

Sustainability and low-carbon materials

- BES 6001: fewer compliant vendors

- 2024: low-carbon premium up to 15%

- Smaller pools = higher supplier leverage

- Fixed-price contracts vulnerable to margin squeeze

M&E/rail supply squeeze: lead times 3–24m, Brent $87/bbl, low-carbon 15%

Complex Kier projects rely on niche M&E/rail specialists with 2024 lead times of 3–24 months, concentrating supplier leverage. Commodity pressure (Brent ~$87/bbl in 2024) and low‑carbon premiums (~15%) squeeze margins on fixed‑price work. OEM/plant bottlenecks (TBM 18–24m) and concentrated software vendors raise switching costs and schedule risk.

| Metric | 2024 |

|---|---|

| Brent | $87/bbl |

| Low‑carbon premium | up to 15% |

| TBM lead time | 18–24 months |

| Signalling OEM | 12–36 months |

What is included in the product

Tailored Porter’s Five Forces analysis of Kier Group uncovering key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging disruptive threats to its market position, with strategic commentary for stakeholders.

A concise Porter's Five Forces one-sheet for Kier Group that visualizes competitive pressures, supplier/customer leverage and regulatory risk—streamlining boardroom decisions and strategic scenario planning.

Customers Bargaining Power

Public sector buyer concentration

Central government, agencies and local authorities control large frameworks representing over 50% of Kier’s order book in 2024, giving buyers strong leverage on price and contract terms. High spend concentration drives aggressive competitive tenders and multi-lot frameworks, intensifying price pressure and compressing margins with typical bid discounts often exceeding 5%. Payment terms (commonly 30–60 days) and social value weightings—frequently up to 20%— materially shape bid economics and contractor cashflow.

Frameworks and performance gating

Framework reappointment for Kier increasingly hinges on 2024 KPIs covering time, cost, safety and carbon, with buyers using performance scorecards to extract commercial concessions and change orders. Poor scorecard outcomes can restrict access to future public and private pipelines, amplifying buyer bargaining power. Gainshare/painshare clauses adopted in 2024 shift upside and downside risk onto contractors, compressing margins and negotiating leverage.

Technical specifications and design control

Clients dictate design standards and approvals on regulated assets, squeezing Kier’s margins as tight oversight increased; Kier reported 2024 revenue of about £4.0bn with continued focus on regulated sectors. Scope creep and change control compress margins on projects where client-approved variations rose materially in 2024. Value-engineering wins are often client-approved, limiting contractor capture of savings. Design-and-build shifts delivery risk to Kier while clients retain strong oversight.

Transparent market pricing

Transparent market pricing has strengthened buyer leverage over Kier as benchmarking and industry cost databases make supplier rates comparable, while should-cost models in 2024 narrowed information asymmetry and drove tougher negotiations. Open-book contracts cap supplier upside and expose line-item costs, and public-sector buyers increasingly reserve the right to re-tender packages when pricing diverges from benchmarks; Kier’s 2024 revenue of £4.2bn increases the stakes of such pressures.

- Benchmarks: faster price discovery

- Should-cost models: reduced asymmetry

- Open-book: capped margins, exposed costs

- Re-tendering: enforces market-aligned pricing

ESG and community outcomes

Buyers now insist on measurable social value, apprenticeships and credible net-zero pathways, expanding scope without proportional price uplift; UK law sets a net-zero target by 2050 and the Social Value Act 2012 requires public buyers to consider social value. Failure to meet these non-price criteria can disqualify bids and reduce future pipeline, forcing contractors to invest upfront to remain eligible.

- Buyers: social value, apprenticeships, net-zero

- Impact: expanded deliverables, limited price uplift

- Risk: disqualification, lost future work

- Action: upfront investment to retain eligibility

Public sector >50% of 2024 order book; £4.0bn revenue; >5% bid discounts

Public sector accounts for >50% of Kier’s 2024 order book, giving buyers strong leverage on price and terms; typical bid discounts exceed 5% and payment terms are 30–60 days. KPI/social value weightings (often up to 20%) and open-book/should-cost models compress margins and shift risk to contractors. Kier reported ~£4.0bn revenue in 2024, raising stakes of re-tendering and performance clauses.

| Metric | 2024 | Impact |

|---|---|---|

| Public share | >50% | High buyer leverage |

| Revenue | £4.0bn | Scale risk exposure |

| Bid discount | >5% | Margin compression |

Full Version Awaits

Kier Group Porter's Five Forces Analysis

This Porter's Five Forces analysis of Kier Group examines supplier power, buyer power, competitive rivalry, threat of substitutes and barriers to entry to assess the firm's strategic position. You're previewing the final version—precisely the same document that will be available to you instantly after buying. Fully formatted and ready to use for decision-making or reporting.