Kier Group SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Kier Group’s SWOT highlights resilient infrastructure expertise, project diversification, and recent balance-sheet improvements, tempered by contract risk and sector cyclicality. Our full SWOT unpacks financial metrics, competitive positioning, and strategic options in a ready-to-use Word and Excel package. Purchase the complete report to plan, pitch, or invest with confidence.

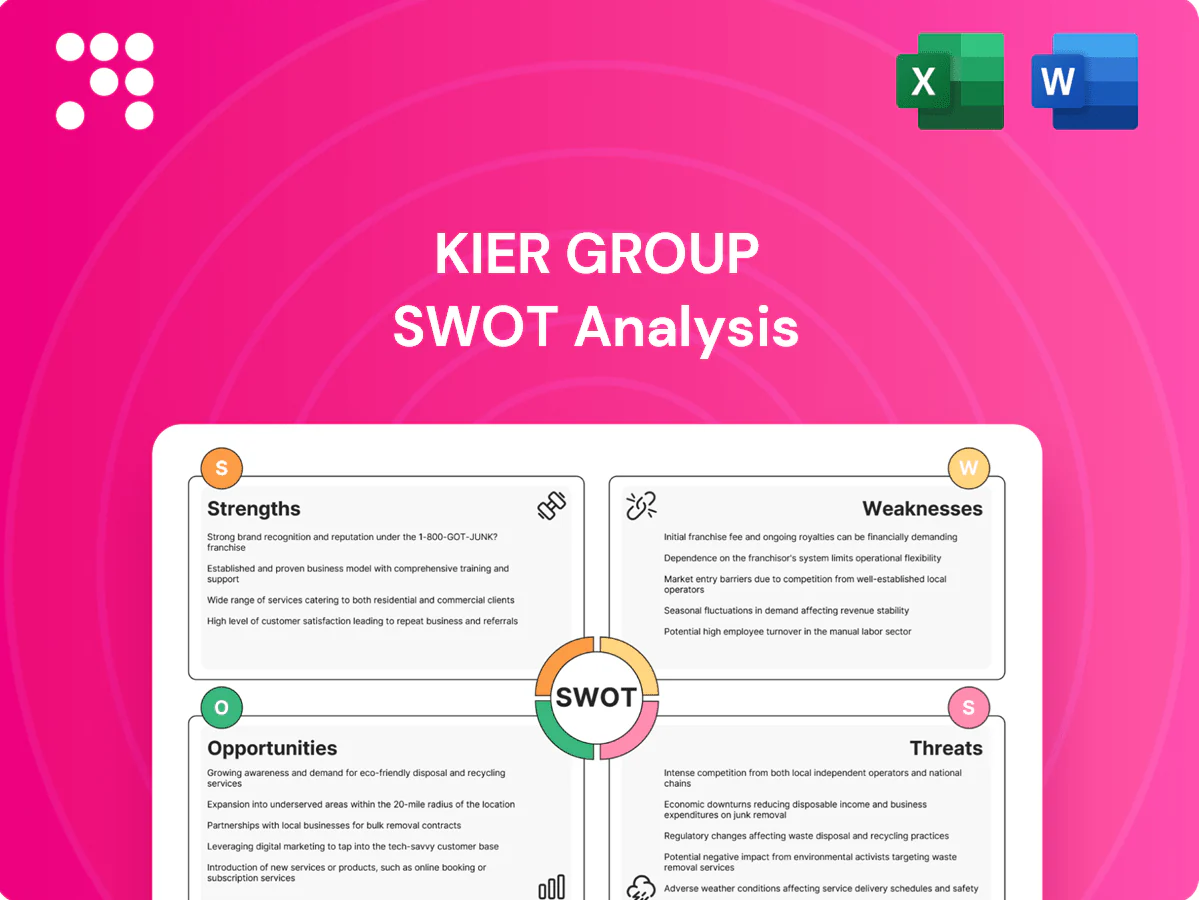

Strengths

Diversified infrastructure portfolio

Kier’s coverage across highways, rail, education, healthcare and justice reduces single‑sector dependence and supported group revenue of c.£4bn in FY2023. This diversification helps smooth revenue through economic cycles and policy shifts, while enabling rapid reallocation of resources to more resilient end‑markets. Cross‑sector learning from public sector frameworks improves delivery standards and operational efficiency.

Public-sector framework access

Participation in UK government and regional frameworks gives Kier steady bid flow linked to the UK infrastructure pipeline of c.£600bn to 2030, lowering sales costs and improving visibility of future work. Prequalification advantages on frameworks typically raise win rates and utilisation by concentrating repeat opportunities. Strong client relationships from framework delivery enhance repeat business and pipeline resilience.

End-to-end delivery capability

Integrated construction, infrastructure services and property development give Kier end-to-end lifecycle solutions, supporting a reported order book above £4bn in 2024 and diversified revenue streams. Clients gain single-point accountability and coordinated delivery, which compresses timelines and lowers interface risk across projects. Bundled offerings and asset recycling widen margin opportunities and improve capital efficiency for the group.

Sustainability and social value focus

Kier's emphasis on sustainable solutions aligns with client ESG priorities, improving competitiveness on contracts requiring carbon reduction. Community legacy programmes bolster licence to operate and public-sector differentiation. Adoption of low-carbon materials and methods helps win tenders with green weighting, while strong ESG credentials support access to sustainability-linked finance and attract ESG-focused talent.

- ESG-aligned bidding advantage

- Community programmes = stronger licence to operate

- Low-carbon procurement boosts tender success

- ESG credentials aid financing and talent attraction

Nationwide execution scale

Nationwide execution scale gives Kier a UK-wide footprint enabling rapid mobilization across regions, supporting procurement leverage and stronger supply-chain resilience while standardized processes boost quality and safety performance and align with decentralized public spending programs.

- Nationwide footprint

- Procurement leverage

- Supply-chain resilience

- Standardized quality & safety

- Aligned with decentralized public spending

UK infra group: c.£4.0bn rev, >£4bn OB; pipeline c.£600bn

Kier’s diversified UK-focused portfolio (highways, rail, education, healthcare, justice) supported group revenue of c.£4.0bn in FY2023 and an order book above £4bn in 2024, reducing single‑sector exposure and smoothing cyclicality. Framework participation ties Kier to a c.£600bn UK infrastructure pipeline to 2030, improving bid visibility and win rates. Integrated construction, services and development plus strong ESG credentials enhance margin mix, finance access and client retention.

| Metric | Value |

|---|---|

| Revenue (FY2023) | c.£4.0bn |

| Order book (2024) | >£4.0bn |

| UK infra pipeline to 2030 | c.£600bn |

| ESG-linked finance / tender advantage | Material (improves win rates) |

What is included in the product

Delivers a strategic overview of Kier Group’s internal and external business factors. Highlights strengths, weaknesses, opportunities, and threats shaping its competitive position and prospects for growth.

Provides a concise Kier Group SWOT matrix for fast, visual alignment of strategic priorities and risk mitigation, enabling quick stakeholder briefings and responsive decision-making.

Weaknesses

Low-margin, fixed-price exposure

Construction commonly runs on thin margins—UK construction operating margins averaged about 3.5% in 2023 (ONS), so cost shocks quickly wipe profits; Kier has repeatedly highlighted fixed-price contract exposure in its filings. Fixed-price work erodes profitability when input costs rise and contracts rarely allow mid-project repricing. Small estimating errors compound over long, complex builds, increasing downside risk.

Project delivery volatility

Large infrastructure jobs expose Kier to schedule and interface risks that have led to delays, liquidated damages and working-capital strain; Kier employs around 12,000 staff and generates circa £3bn revenue, so mid-project cash pressure is material. Rework and variations have compressed margins and eroded client trust, weakening framework positioning and reducing likelihood of future awards.

Working-capital intensity

Upfront labour and materials outlays precede cash receipts, with construction retentions commonly ~3–5% of contract value and payment terms often stretching 60–120 days. Retentions and long terms depress cash conversion, elevating reliance on committed bank facilities and tight treasury controls. Slower cycle turns can rapidly expose liquidity if collections lag beyond expected receivable days.

Public-sector revenue concentration

Kier’s revenue remains heavily skewed to the public sector, with roughly 55% of group revenue tied to government contracts in FY2024, exposing demand to UK fiscal policy and spending resets; election cycles and spending reviews caused multi-year project deferrals in 2024–25. Changes to public procurement frameworks in 2024 reduced framework awards and pipeline visibility, constraining pricing power versus diversified private-sector peers.

- Public exposure ~55% (FY2024)

- Election/fiscal cycles → project deferrals 2024–25

- Procurement reform reduced framework access in 2024

- Concentration limits pricing leverage vs private clients

Legacy liabilities and reputation drag

Historic projects leave open claims, defects and provisions that divert cash and absorb management time into dispute resolution rather than bidding and growth; negative headlines from contract failures erode client and investor confidence, while insurance excesses and mounting legal fees compress earnings quality.

- Legacy claims divert management focus

- Reputation risk hurts stakeholder trust

- Insurance excesses and legal costs reduce margins

Thin margins, long payment terms and heavy public-sector exposure increase profit and cash risk

Thin sector margins (UK construction operating margin ~3.5% in 2023, ONS) and fixed-price contract exposure leave Kier highly profit-sensitive to input-cost shocks. Cash conversion is weak—retentions ~3–5% and payment terms 60–120 days—while public-sector dependence (~55% of revenue in FY2024) concentrates demand and pricing risk.

| Metric | Value |

|---|---|

| Operating margin | ~3.5% (ONS 2023) |

| Public revenue | ~55% (FY2024) |

| Retentions | 3–5% |

| Payment terms | 60–120 days |

| Staff / Revenue | ~12,000 / ~£3bn |

What You See Is What You Get

Kier Group SWOT Analysis

This is a real excerpt from the complete Kier Group SWOT analysis you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable document included in your download. Buy now to unlock the entire in-depth version immediately after checkout.

Elevate Your Analysis with the Complete SWOT Report

Kier Group’s SWOT highlights resilient infrastructure expertise, project diversification, and recent balance-sheet improvements, tempered by contract risk and sector cyclicality. Our full SWOT unpacks financial metrics, competitive positioning, and strategic options in a ready-to-use Word and Excel package. Purchase the complete report to plan, pitch, or invest with confidence.

Strengths

Diversified infrastructure portfolio

Kier’s coverage across highways, rail, education, healthcare and justice reduces single‑sector dependence and supported group revenue of c.£4bn in FY2023. This diversification helps smooth revenue through economic cycles and policy shifts, while enabling rapid reallocation of resources to more resilient end‑markets. Cross‑sector learning from public sector frameworks improves delivery standards and operational efficiency.

Public-sector framework access

Participation in UK government and regional frameworks gives Kier steady bid flow linked to the UK infrastructure pipeline of c.£600bn to 2030, lowering sales costs and improving visibility of future work. Prequalification advantages on frameworks typically raise win rates and utilisation by concentrating repeat opportunities. Strong client relationships from framework delivery enhance repeat business and pipeline resilience.

End-to-end delivery capability

Integrated construction, infrastructure services and property development give Kier end-to-end lifecycle solutions, supporting a reported order book above £4bn in 2024 and diversified revenue streams. Clients gain single-point accountability and coordinated delivery, which compresses timelines and lowers interface risk across projects. Bundled offerings and asset recycling widen margin opportunities and improve capital efficiency for the group.

Sustainability and social value focus

Kier's emphasis on sustainable solutions aligns with client ESG priorities, improving competitiveness on contracts requiring carbon reduction. Community legacy programmes bolster licence to operate and public-sector differentiation. Adoption of low-carbon materials and methods helps win tenders with green weighting, while strong ESG credentials support access to sustainability-linked finance and attract ESG-focused talent.

- ESG-aligned bidding advantage

- Community programmes = stronger licence to operate

- Low-carbon procurement boosts tender success

- ESG credentials aid financing and talent attraction

Nationwide execution scale

Nationwide execution scale gives Kier a UK-wide footprint enabling rapid mobilization across regions, supporting procurement leverage and stronger supply-chain resilience while standardized processes boost quality and safety performance and align with decentralized public spending programs.

- Nationwide footprint

- Procurement leverage

- Supply-chain resilience

- Standardized quality & safety

- Aligned with decentralized public spending

UK infra group: c.£4.0bn rev, >£4bn OB; pipeline c.£600bn

Kier’s diversified UK-focused portfolio (highways, rail, education, healthcare, justice) supported group revenue of c.£4.0bn in FY2023 and an order book above £4bn in 2024, reducing single‑sector exposure and smoothing cyclicality. Framework participation ties Kier to a c.£600bn UK infrastructure pipeline to 2030, improving bid visibility and win rates. Integrated construction, services and development plus strong ESG credentials enhance margin mix, finance access and client retention.

| Metric | Value |

|---|---|

| Revenue (FY2023) | c.£4.0bn |

| Order book (2024) | >£4.0bn |

| UK infra pipeline to 2030 | c.£600bn |

| ESG-linked finance / tender advantage | Material (improves win rates) |

What is included in the product

Delivers a strategic overview of Kier Group’s internal and external business factors. Highlights strengths, weaknesses, opportunities, and threats shaping its competitive position and prospects for growth.

Provides a concise Kier Group SWOT matrix for fast, visual alignment of strategic priorities and risk mitigation, enabling quick stakeholder briefings and responsive decision-making.

Weaknesses

Low-margin, fixed-price exposure

Construction commonly runs on thin margins—UK construction operating margins averaged about 3.5% in 2023 (ONS), so cost shocks quickly wipe profits; Kier has repeatedly highlighted fixed-price contract exposure in its filings. Fixed-price work erodes profitability when input costs rise and contracts rarely allow mid-project repricing. Small estimating errors compound over long, complex builds, increasing downside risk.

Project delivery volatility

Large infrastructure jobs expose Kier to schedule and interface risks that have led to delays, liquidated damages and working-capital strain; Kier employs around 12,000 staff and generates circa £3bn revenue, so mid-project cash pressure is material. Rework and variations have compressed margins and eroded client trust, weakening framework positioning and reducing likelihood of future awards.

Working-capital intensity

Upfront labour and materials outlays precede cash receipts, with construction retentions commonly ~3–5% of contract value and payment terms often stretching 60–120 days. Retentions and long terms depress cash conversion, elevating reliance on committed bank facilities and tight treasury controls. Slower cycle turns can rapidly expose liquidity if collections lag beyond expected receivable days.

Public-sector revenue concentration

Kier’s revenue remains heavily skewed to the public sector, with roughly 55% of group revenue tied to government contracts in FY2024, exposing demand to UK fiscal policy and spending resets; election cycles and spending reviews caused multi-year project deferrals in 2024–25. Changes to public procurement frameworks in 2024 reduced framework awards and pipeline visibility, constraining pricing power versus diversified private-sector peers.

- Public exposure ~55% (FY2024)

- Election/fiscal cycles → project deferrals 2024–25

- Procurement reform reduced framework access in 2024

- Concentration limits pricing leverage vs private clients

Legacy liabilities and reputation drag

Historic projects leave open claims, defects and provisions that divert cash and absorb management time into dispute resolution rather than bidding and growth; negative headlines from contract failures erode client and investor confidence, while insurance excesses and mounting legal fees compress earnings quality.

- Legacy claims divert management focus

- Reputation risk hurts stakeholder trust

- Insurance excesses and legal costs reduce margins

Thin margins, long payment terms and heavy public-sector exposure increase profit and cash risk

Thin sector margins (UK construction operating margin ~3.5% in 2023, ONS) and fixed-price contract exposure leave Kier highly profit-sensitive to input-cost shocks. Cash conversion is weak—retentions ~3–5% and payment terms 60–120 days—while public-sector dependence (~55% of revenue in FY2024) concentrates demand and pricing risk.

| Metric | Value |

|---|---|

| Operating margin | ~3.5% (ONS 2023) |

| Public revenue | ~55% (FY2024) |

| Retentions | 3–5% |

| Payment terms | 60–120 days |

| Staff / Revenue | ~12,000 / ~£3bn |

What You See Is What You Get

Kier Group SWOT Analysis

This is a real excerpt from the complete Kier Group SWOT analysis you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable document included in your download. Buy now to unlock the entire in-depth version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

Kier Group’s SWOT highlights resilient infrastructure expertise, project diversification, and recent balance-sheet improvements, tempered by contract risk and sector cyclicality. Our full SWOT unpacks financial metrics, competitive positioning, and strategic options in a ready-to-use Word and Excel package. Purchase the complete report to plan, pitch, or invest with confidence.

Strengths

Diversified infrastructure portfolio

Kier’s coverage across highways, rail, education, healthcare and justice reduces single‑sector dependence and supported group revenue of c.£4bn in FY2023. This diversification helps smooth revenue through economic cycles and policy shifts, while enabling rapid reallocation of resources to more resilient end‑markets. Cross‑sector learning from public sector frameworks improves delivery standards and operational efficiency.

Public-sector framework access

Participation in UK government and regional frameworks gives Kier steady bid flow linked to the UK infrastructure pipeline of c.£600bn to 2030, lowering sales costs and improving visibility of future work. Prequalification advantages on frameworks typically raise win rates and utilisation by concentrating repeat opportunities. Strong client relationships from framework delivery enhance repeat business and pipeline resilience.

End-to-end delivery capability

Integrated construction, infrastructure services and property development give Kier end-to-end lifecycle solutions, supporting a reported order book above £4bn in 2024 and diversified revenue streams. Clients gain single-point accountability and coordinated delivery, which compresses timelines and lowers interface risk across projects. Bundled offerings and asset recycling widen margin opportunities and improve capital efficiency for the group.

Sustainability and social value focus

Kier's emphasis on sustainable solutions aligns with client ESG priorities, improving competitiveness on contracts requiring carbon reduction. Community legacy programmes bolster licence to operate and public-sector differentiation. Adoption of low-carbon materials and methods helps win tenders with green weighting, while strong ESG credentials support access to sustainability-linked finance and attract ESG-focused talent.

- ESG-aligned bidding advantage

- Community programmes = stronger licence to operate

- Low-carbon procurement boosts tender success

- ESG credentials aid financing and talent attraction

Nationwide execution scale

Nationwide execution scale gives Kier a UK-wide footprint enabling rapid mobilization across regions, supporting procurement leverage and stronger supply-chain resilience while standardized processes boost quality and safety performance and align with decentralized public spending programs.

- Nationwide footprint

- Procurement leverage

- Supply-chain resilience

- Standardized quality & safety

- Aligned with decentralized public spending

UK infra group: c.£4.0bn rev, >£4bn OB; pipeline c.£600bn

Kier’s diversified UK-focused portfolio (highways, rail, education, healthcare, justice) supported group revenue of c.£4.0bn in FY2023 and an order book above £4bn in 2024, reducing single‑sector exposure and smoothing cyclicality. Framework participation ties Kier to a c.£600bn UK infrastructure pipeline to 2030, improving bid visibility and win rates. Integrated construction, services and development plus strong ESG credentials enhance margin mix, finance access and client retention.

| Metric | Value |

|---|---|

| Revenue (FY2023) | c.£4.0bn |

| Order book (2024) | >£4.0bn |

| UK infra pipeline to 2030 | c.£600bn |

| ESG-linked finance / tender advantage | Material (improves win rates) |

What is included in the product

Delivers a strategic overview of Kier Group’s internal and external business factors. Highlights strengths, weaknesses, opportunities, and threats shaping its competitive position and prospects for growth.

Provides a concise Kier Group SWOT matrix for fast, visual alignment of strategic priorities and risk mitigation, enabling quick stakeholder briefings and responsive decision-making.

Weaknesses

Low-margin, fixed-price exposure

Construction commonly runs on thin margins—UK construction operating margins averaged about 3.5% in 2023 (ONS), so cost shocks quickly wipe profits; Kier has repeatedly highlighted fixed-price contract exposure in its filings. Fixed-price work erodes profitability when input costs rise and contracts rarely allow mid-project repricing. Small estimating errors compound over long, complex builds, increasing downside risk.

Project delivery volatility

Large infrastructure jobs expose Kier to schedule and interface risks that have led to delays, liquidated damages and working-capital strain; Kier employs around 12,000 staff and generates circa £3bn revenue, so mid-project cash pressure is material. Rework and variations have compressed margins and eroded client trust, weakening framework positioning and reducing likelihood of future awards.

Working-capital intensity

Upfront labour and materials outlays precede cash receipts, with construction retentions commonly ~3–5% of contract value and payment terms often stretching 60–120 days. Retentions and long terms depress cash conversion, elevating reliance on committed bank facilities and tight treasury controls. Slower cycle turns can rapidly expose liquidity if collections lag beyond expected receivable days.

Public-sector revenue concentration

Kier’s revenue remains heavily skewed to the public sector, with roughly 55% of group revenue tied to government contracts in FY2024, exposing demand to UK fiscal policy and spending resets; election cycles and spending reviews caused multi-year project deferrals in 2024–25. Changes to public procurement frameworks in 2024 reduced framework awards and pipeline visibility, constraining pricing power versus diversified private-sector peers.

- Public exposure ~55% (FY2024)

- Election/fiscal cycles → project deferrals 2024–25

- Procurement reform reduced framework access in 2024

- Concentration limits pricing leverage vs private clients

Legacy liabilities and reputation drag

Historic projects leave open claims, defects and provisions that divert cash and absorb management time into dispute resolution rather than bidding and growth; negative headlines from contract failures erode client and investor confidence, while insurance excesses and mounting legal fees compress earnings quality.

- Legacy claims divert management focus

- Reputation risk hurts stakeholder trust

- Insurance excesses and legal costs reduce margins

Thin margins, long payment terms and heavy public-sector exposure increase profit and cash risk

Thin sector margins (UK construction operating margin ~3.5% in 2023, ONS) and fixed-price contract exposure leave Kier highly profit-sensitive to input-cost shocks. Cash conversion is weak—retentions ~3–5% and payment terms 60–120 days—while public-sector dependence (~55% of revenue in FY2024) concentrates demand and pricing risk.

| Metric | Value |

|---|---|

| Operating margin | ~3.5% (ONS 2023) |

| Public revenue | ~55% (FY2024) |

| Retentions | 3–5% |

| Payment terms | 60–120 days |

| Staff / Revenue | ~12,000 / ~£3bn |

What You See Is What You Get

Kier Group SWOT Analysis

This is a real excerpt from the complete Kier Group SWOT analysis you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable document included in your download. Buy now to unlock the entire in-depth version immediately after checkout.