Kiewit Porter's Five Forces Analysis

From Overview to Strategy Blueprint

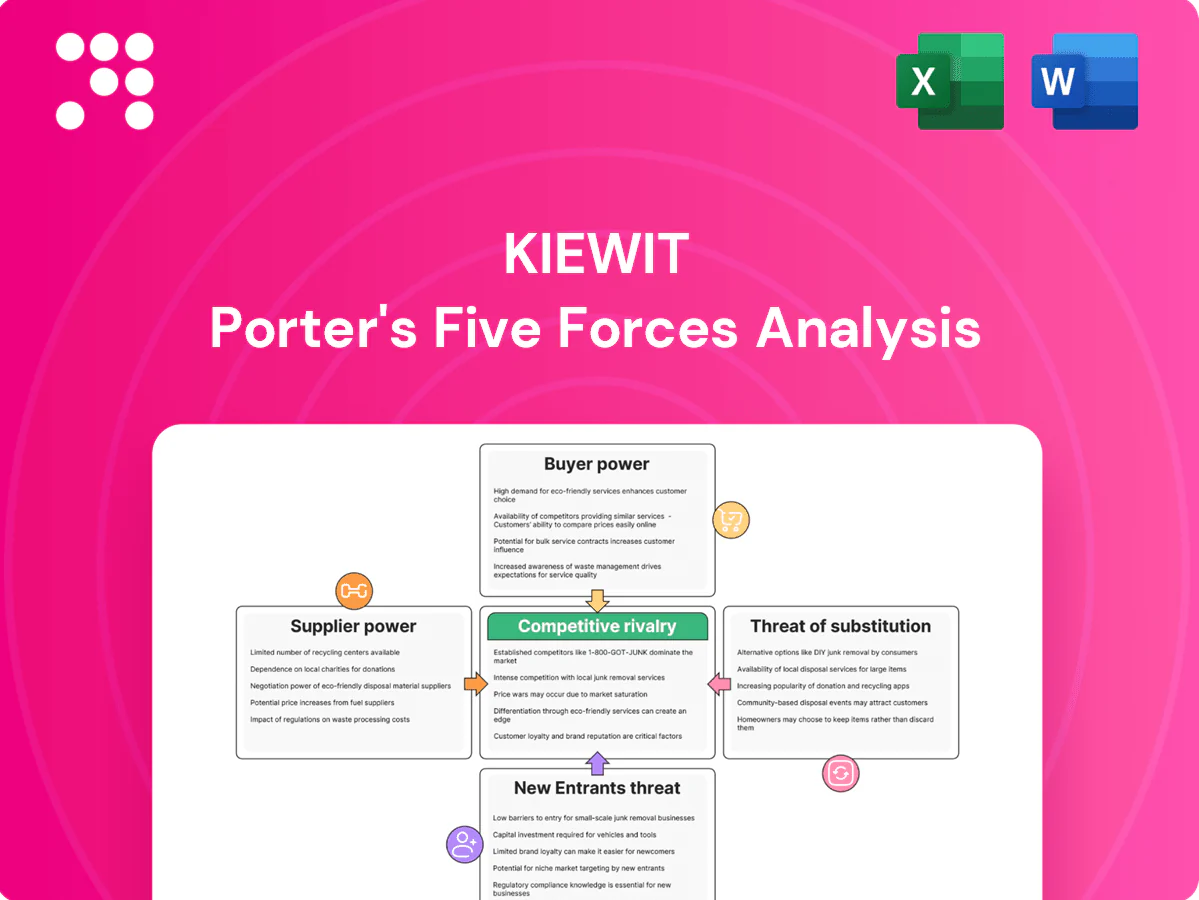

Kiewit's Porter's Five Forces snapshot highlights strong supplier relationships, moderate buyer power, high rivalry in construction and engineering, barriers limiting new entrants, and limited substitute threats. This brief view teases key strategic pressures and competitive levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Kiewit.

Suppliers Bargaining Power

Specialized inputs

Large Kiewit projects rely on cement, steel, turbines, pipe and heavy equipment from concentrated global suppliers — China produced about 54% of world steel in 2024, reinforcing supplier concentration. Multiple vendors exist but rigorous qualification and 12–24 month turbine/equipment lead times limit substitution. Bulk commodity price swings have shifted leverage mid-project; Kiewit offsets risk via multi-sourcing and hedging where feasible.

Subcontractors & trades

Skilled subs in electrical, instrumentation and tunneling became bottlenecks in the 2024 market, pushing specialty trade wage growth and leading to project delays. Unionization in construction is around 13% (BLS 2023–24), which elevates regional supplier leverage and wage baselines. Tight capacity increases performance risk; Kiewit’s self-perform model materially reduces dependence on high-power subcontractors.

Technology vendors

BIM/CAD, survey and project-controls platforms create switching costs and training dependencies—firms often face 3–5 year contract terms and onboarding costs commonly in the $50k–$200k range. Certification and data-integration requirements limit rapid provider changes, letting vendors exert moderate power via licensing and support terms, while long-term enterprise agreements partially temper pricing exposure.

Logistics & lead times

Overseas fabrication, port congestion and volatile freight rates undermine delivery certainty for Kiewit; the Drewry World Container Index fell over 80% from 2021 peaks to 2024 but schedule risk remains and lead-time variability rose in Red Sea and Suez-area disruptions. Schedule sensitivity increases supplier leverage when expediting is needed; geopolitical constraints narrow alternative sources. Early procurement and buffer stock reduce pressure.

- Overseas fabrication: long lead times

- Port congestion: increases variability

- Freight rates: Drewry WCI down >80% vs 2021

- Geopolitics: limits redirection

- Mitigants: early buy, buffer stock

Vertical integration

Kiewit’s vertical integration—self-performing civil, structural and select MEP scopes—internalizes value and captures margin that would otherwise flow to subcontractors. Owning extensive equipment fleets reduces dependence on rental suppliers, blunting supplier pricing power and schedule risk while strengthening negotiation leverage with remaining vendors.

- 2024: Kiewit remains privately held; exact 2024 revenue and backlog are not publicly disclosed

Supply pressure: China steel 54%, turbines 12–24mo, onboarding $50k–$200k

Suppliers wield moderate-to-high power on materials (steel: China 54% of 2024 output) and long-lead turbines (12–24mo), while specialty subs and 13% construction unionization (BLS 2023–24) raise labor leverage. Kiewit’s self-perform, equipment fleets, multi-sourcing and hedging mitigate pricing and schedule risk; BIM/contracts add switching costs ($50k–$200k onboarding).

| Metric | 2024 value |

|---|---|

| China share of steel | 54% |

| Turbine/equipment lead time | 12–24 months |

| Construction unionization | 13% (BLS 2023–24) |

| Drewry WCI change vs 2021 | down >80% |

| Onboarding cost (BIM/tools) | $50k–$200k |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Kiewit's construction and engineering operations, evaluating supplier and buyer power, threat of substitutes, intensity of rivalry, and barriers that protect incumbents.

One-sheet Porter's Five Forces tailored for Kiewit—instantly highlights contractor-specific risks and bargaining pressures for faster, board-ready decisions. Swap in updated project data or scenarios to see strategic pressure shift and relieve analysis bottlenecks.

Customers Bargaining Power

Large institutional buyers

Public agencies, utilities and energy majors procure at scale under professional processes, supported by federal programs such as the Bipartisan Infrastructure Law which authorized about 550 billion dollars in new infrastructure funding. Their sophistication and volume give them strong negotiating leverage to dictate contract terms, risk allocation and compliance. Kiewit counters with a long track record and documented capability to deliver complex EPC scopes, and is regularly ranked among ENR’s top contractors.

Competitive tendering

Competitive tendering—driven by low-bid and best-value RFPs—compresses margins as owners increasingly prize price and measurable value, often forcing 5–15% bid concessions in contested heavy-civil projects. Pre-bid transparency tools let owners compare apples-to-apples, amplifying buyer power and favoring fixed-price, lump-sum EPC structures that shift cost and schedule risk to contractors. Kiewit, reporting roughly $13 billion revenue in 2024, counters with rigorous estimating, standardized contingency governance and disciplined risk allocation to protect margins.

Risk transfer clauses

Owners push liquidated damages, performance guarantees, and onerous change terms, elevating buyer leverage over cost, schedule, and quality; Flyvbjerg et al. show large projects average ~28% cost overruns, underscoring this pressure. Contractors must price or negotiate these risks effectively, shifting or pricing contingencies. Kiewit’s legal and project controls discipline materially helps balance exposures on high-stakes bids and change management.

Frameworks & alliances

Long-term master agreements and partnering models reduce transactional pressure by locking in multi-year workstreams, while buyers demand continuous improvement and periodic cost-downs as contract conditions. Relationship capital from repeat engagements lowers switching frequency and supports predictable backlog that can offset lower unit margins.

- Long-term agreements: stabilize volume

- Buyer demands: continuous improvement, cost-downs

- Relationship capital: reduces churn

- Predictable backlog: offsets margin pressure

End-market diversity

End-market exposure across six sectors—transportation, water, power, OGC, buildings, and mining—limits Kiewit’s dependence on any single buyer and reduces buyer concentration risk through cycle diversification. This sector mix lets management reallocate resources toward higher-margin or faster-growing projects when markets diverge, lowering aggregate buyer power over time. Operational scale across those markets strengthens bargaining leverage with large public and private clients.

- sectors: 6 (transportation, water, power, OGC, buildings, mining)

- effect: lowers buyer concentration risk

- benefit: flexibility to prioritize attractive opportunities

Scale and BIL $550B back contractors amid 28% overruns

Public agencies and energy majors wield strong leverage via scale and federal programs (BIL ~550 billion), while Kiewit reported ~13 billion revenue in 2024 and leverages reputation to negotiate. Competitive tendering compresses margins (typical bid concessions 5–15%) and owners push liquidated damages amid ~28% average cost overruns. Long-term agreements across six sectors reduce buyer concentration and stabilize backlog.

| Metric | Value | Note |

|---|---|---|

| Revenue 2024 | $13B | Company reported |

| BIL funding | $550B | Authorized |

| Bid concessions | 5–15% | Typical |

| Avg cost overrun | 28% | Large projects |

| Sectors | 6 | Diversified exposure |

Preview the Actual Deliverable

Kiewit Porter's Five Forces Analysis

You’re viewing the Kiewit Porter's Five Forces Analysis preview: the exact, fully formatted document you’ll receive immediately after purchase. This file is complete, professional, and ready for download—no placeholders or samples. Purchase grants instant access to this same analysis for use in decision-making, reporting, or strategy work.

From Overview to Strategy Blueprint

Kiewit's Porter's Five Forces snapshot highlights strong supplier relationships, moderate buyer power, high rivalry in construction and engineering, barriers limiting new entrants, and limited substitute threats. This brief view teases key strategic pressures and competitive levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Kiewit.

Suppliers Bargaining Power

Specialized inputs

Large Kiewit projects rely on cement, steel, turbines, pipe and heavy equipment from concentrated global suppliers — China produced about 54% of world steel in 2024, reinforcing supplier concentration. Multiple vendors exist but rigorous qualification and 12–24 month turbine/equipment lead times limit substitution. Bulk commodity price swings have shifted leverage mid-project; Kiewit offsets risk via multi-sourcing and hedging where feasible.

Subcontractors & trades

Skilled subs in electrical, instrumentation and tunneling became bottlenecks in the 2024 market, pushing specialty trade wage growth and leading to project delays. Unionization in construction is around 13% (BLS 2023–24), which elevates regional supplier leverage and wage baselines. Tight capacity increases performance risk; Kiewit’s self-perform model materially reduces dependence on high-power subcontractors.

Technology vendors

BIM/CAD, survey and project-controls platforms create switching costs and training dependencies—firms often face 3–5 year contract terms and onboarding costs commonly in the $50k–$200k range. Certification and data-integration requirements limit rapid provider changes, letting vendors exert moderate power via licensing and support terms, while long-term enterprise agreements partially temper pricing exposure.

Logistics & lead times

Overseas fabrication, port congestion and volatile freight rates undermine delivery certainty for Kiewit; the Drewry World Container Index fell over 80% from 2021 peaks to 2024 but schedule risk remains and lead-time variability rose in Red Sea and Suez-area disruptions. Schedule sensitivity increases supplier leverage when expediting is needed; geopolitical constraints narrow alternative sources. Early procurement and buffer stock reduce pressure.

- Overseas fabrication: long lead times

- Port congestion: increases variability

- Freight rates: Drewry WCI down >80% vs 2021

- Geopolitics: limits redirection

- Mitigants: early buy, buffer stock

Vertical integration

Kiewit’s vertical integration—self-performing civil, structural and select MEP scopes—internalizes value and captures margin that would otherwise flow to subcontractors. Owning extensive equipment fleets reduces dependence on rental suppliers, blunting supplier pricing power and schedule risk while strengthening negotiation leverage with remaining vendors.

- 2024: Kiewit remains privately held; exact 2024 revenue and backlog are not publicly disclosed

Supply pressure: China steel 54%, turbines 12–24mo, onboarding $50k–$200k

Suppliers wield moderate-to-high power on materials (steel: China 54% of 2024 output) and long-lead turbines (12–24mo), while specialty subs and 13% construction unionization (BLS 2023–24) raise labor leverage. Kiewit’s self-perform, equipment fleets, multi-sourcing and hedging mitigate pricing and schedule risk; BIM/contracts add switching costs ($50k–$200k onboarding).

| Metric | 2024 value |

|---|---|

| China share of steel | 54% |

| Turbine/equipment lead time | 12–24 months |

| Construction unionization | 13% (BLS 2023–24) |

| Drewry WCI change vs 2021 | down >80% |

| Onboarding cost (BIM/tools) | $50k–$200k |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Kiewit's construction and engineering operations, evaluating supplier and buyer power, threat of substitutes, intensity of rivalry, and barriers that protect incumbents.

One-sheet Porter's Five Forces tailored for Kiewit—instantly highlights contractor-specific risks and bargaining pressures for faster, board-ready decisions. Swap in updated project data or scenarios to see strategic pressure shift and relieve analysis bottlenecks.

Customers Bargaining Power

Large institutional buyers

Public agencies, utilities and energy majors procure at scale under professional processes, supported by federal programs such as the Bipartisan Infrastructure Law which authorized about 550 billion dollars in new infrastructure funding. Their sophistication and volume give them strong negotiating leverage to dictate contract terms, risk allocation and compliance. Kiewit counters with a long track record and documented capability to deliver complex EPC scopes, and is regularly ranked among ENR’s top contractors.

Competitive tendering

Competitive tendering—driven by low-bid and best-value RFPs—compresses margins as owners increasingly prize price and measurable value, often forcing 5–15% bid concessions in contested heavy-civil projects. Pre-bid transparency tools let owners compare apples-to-apples, amplifying buyer power and favoring fixed-price, lump-sum EPC structures that shift cost and schedule risk to contractors. Kiewit, reporting roughly $13 billion revenue in 2024, counters with rigorous estimating, standardized contingency governance and disciplined risk allocation to protect margins.

Risk transfer clauses

Owners push liquidated damages, performance guarantees, and onerous change terms, elevating buyer leverage over cost, schedule, and quality; Flyvbjerg et al. show large projects average ~28% cost overruns, underscoring this pressure. Contractors must price or negotiate these risks effectively, shifting or pricing contingencies. Kiewit’s legal and project controls discipline materially helps balance exposures on high-stakes bids and change management.

Frameworks & alliances

Long-term master agreements and partnering models reduce transactional pressure by locking in multi-year workstreams, while buyers demand continuous improvement and periodic cost-downs as contract conditions. Relationship capital from repeat engagements lowers switching frequency and supports predictable backlog that can offset lower unit margins.

- Long-term agreements: stabilize volume

- Buyer demands: continuous improvement, cost-downs

- Relationship capital: reduces churn

- Predictable backlog: offsets margin pressure

End-market diversity

End-market exposure across six sectors—transportation, water, power, OGC, buildings, and mining—limits Kiewit’s dependence on any single buyer and reduces buyer concentration risk through cycle diversification. This sector mix lets management reallocate resources toward higher-margin or faster-growing projects when markets diverge, lowering aggregate buyer power over time. Operational scale across those markets strengthens bargaining leverage with large public and private clients.

- sectors: 6 (transportation, water, power, OGC, buildings, mining)

- effect: lowers buyer concentration risk

- benefit: flexibility to prioritize attractive opportunities

Scale and BIL $550B back contractors amid 28% overruns

Public agencies and energy majors wield strong leverage via scale and federal programs (BIL ~550 billion), while Kiewit reported ~13 billion revenue in 2024 and leverages reputation to negotiate. Competitive tendering compresses margins (typical bid concessions 5–15%) and owners push liquidated damages amid ~28% average cost overruns. Long-term agreements across six sectors reduce buyer concentration and stabilize backlog.

| Metric | Value | Note |

|---|---|---|

| Revenue 2024 | $13B | Company reported |

| BIL funding | $550B | Authorized |

| Bid concessions | 5–15% | Typical |

| Avg cost overrun | 28% | Large projects |

| Sectors | 6 | Diversified exposure |

Preview the Actual Deliverable

Kiewit Porter's Five Forces Analysis

You’re viewing the Kiewit Porter's Five Forces Analysis preview: the exact, fully formatted document you’ll receive immediately after purchase. This file is complete, professional, and ready for download—no placeholders or samples. Purchase grants instant access to this same analysis for use in decision-making, reporting, or strategy work.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Kiewit's Porter's Five Forces snapshot highlights strong supplier relationships, moderate buyer power, high rivalry in construction and engineering, barriers limiting new entrants, and limited substitute threats. This brief view teases key strategic pressures and competitive levers. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Kiewit.

Suppliers Bargaining Power

Specialized inputs

Large Kiewit projects rely on cement, steel, turbines, pipe and heavy equipment from concentrated global suppliers — China produced about 54% of world steel in 2024, reinforcing supplier concentration. Multiple vendors exist but rigorous qualification and 12–24 month turbine/equipment lead times limit substitution. Bulk commodity price swings have shifted leverage mid-project; Kiewit offsets risk via multi-sourcing and hedging where feasible.

Subcontractors & trades

Skilled subs in electrical, instrumentation and tunneling became bottlenecks in the 2024 market, pushing specialty trade wage growth and leading to project delays. Unionization in construction is around 13% (BLS 2023–24), which elevates regional supplier leverage and wage baselines. Tight capacity increases performance risk; Kiewit’s self-perform model materially reduces dependence on high-power subcontractors.

Technology vendors

BIM/CAD, survey and project-controls platforms create switching costs and training dependencies—firms often face 3–5 year contract terms and onboarding costs commonly in the $50k–$200k range. Certification and data-integration requirements limit rapid provider changes, letting vendors exert moderate power via licensing and support terms, while long-term enterprise agreements partially temper pricing exposure.

Logistics & lead times

Overseas fabrication, port congestion and volatile freight rates undermine delivery certainty for Kiewit; the Drewry World Container Index fell over 80% from 2021 peaks to 2024 but schedule risk remains and lead-time variability rose in Red Sea and Suez-area disruptions. Schedule sensitivity increases supplier leverage when expediting is needed; geopolitical constraints narrow alternative sources. Early procurement and buffer stock reduce pressure.

- Overseas fabrication: long lead times

- Port congestion: increases variability

- Freight rates: Drewry WCI down >80% vs 2021

- Geopolitics: limits redirection

- Mitigants: early buy, buffer stock

Vertical integration

Kiewit’s vertical integration—self-performing civil, structural and select MEP scopes—internalizes value and captures margin that would otherwise flow to subcontractors. Owning extensive equipment fleets reduces dependence on rental suppliers, blunting supplier pricing power and schedule risk while strengthening negotiation leverage with remaining vendors.

- 2024: Kiewit remains privately held; exact 2024 revenue and backlog are not publicly disclosed

Supply pressure: China steel 54%, turbines 12–24mo, onboarding $50k–$200k

Suppliers wield moderate-to-high power on materials (steel: China 54% of 2024 output) and long-lead turbines (12–24mo), while specialty subs and 13% construction unionization (BLS 2023–24) raise labor leverage. Kiewit’s self-perform, equipment fleets, multi-sourcing and hedging mitigate pricing and schedule risk; BIM/contracts add switching costs ($50k–$200k onboarding).

| Metric | 2024 value |

|---|---|

| China share of steel | 54% |

| Turbine/equipment lead time | 12–24 months |

| Construction unionization | 13% (BLS 2023–24) |

| Drewry WCI change vs 2021 | down >80% |

| Onboarding cost (BIM/tools) | $50k–$200k |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Kiewit's construction and engineering operations, evaluating supplier and buyer power, threat of substitutes, intensity of rivalry, and barriers that protect incumbents.

One-sheet Porter's Five Forces tailored for Kiewit—instantly highlights contractor-specific risks and bargaining pressures for faster, board-ready decisions. Swap in updated project data or scenarios to see strategic pressure shift and relieve analysis bottlenecks.

Customers Bargaining Power

Large institutional buyers

Public agencies, utilities and energy majors procure at scale under professional processes, supported by federal programs such as the Bipartisan Infrastructure Law which authorized about 550 billion dollars in new infrastructure funding. Their sophistication and volume give them strong negotiating leverage to dictate contract terms, risk allocation and compliance. Kiewit counters with a long track record and documented capability to deliver complex EPC scopes, and is regularly ranked among ENR’s top contractors.

Competitive tendering

Competitive tendering—driven by low-bid and best-value RFPs—compresses margins as owners increasingly prize price and measurable value, often forcing 5–15% bid concessions in contested heavy-civil projects. Pre-bid transparency tools let owners compare apples-to-apples, amplifying buyer power and favoring fixed-price, lump-sum EPC structures that shift cost and schedule risk to contractors. Kiewit, reporting roughly $13 billion revenue in 2024, counters with rigorous estimating, standardized contingency governance and disciplined risk allocation to protect margins.

Risk transfer clauses

Owners push liquidated damages, performance guarantees, and onerous change terms, elevating buyer leverage over cost, schedule, and quality; Flyvbjerg et al. show large projects average ~28% cost overruns, underscoring this pressure. Contractors must price or negotiate these risks effectively, shifting or pricing contingencies. Kiewit’s legal and project controls discipline materially helps balance exposures on high-stakes bids and change management.

Frameworks & alliances

Long-term master agreements and partnering models reduce transactional pressure by locking in multi-year workstreams, while buyers demand continuous improvement and periodic cost-downs as contract conditions. Relationship capital from repeat engagements lowers switching frequency and supports predictable backlog that can offset lower unit margins.

- Long-term agreements: stabilize volume

- Buyer demands: continuous improvement, cost-downs

- Relationship capital: reduces churn

- Predictable backlog: offsets margin pressure

End-market diversity

End-market exposure across six sectors—transportation, water, power, OGC, buildings, and mining—limits Kiewit’s dependence on any single buyer and reduces buyer concentration risk through cycle diversification. This sector mix lets management reallocate resources toward higher-margin or faster-growing projects when markets diverge, lowering aggregate buyer power over time. Operational scale across those markets strengthens bargaining leverage with large public and private clients.

- sectors: 6 (transportation, water, power, OGC, buildings, mining)

- effect: lowers buyer concentration risk

- benefit: flexibility to prioritize attractive opportunities

Scale and BIL $550B back contractors amid 28% overruns

Public agencies and energy majors wield strong leverage via scale and federal programs (BIL ~550 billion), while Kiewit reported ~13 billion revenue in 2024 and leverages reputation to negotiate. Competitive tendering compresses margins (typical bid concessions 5–15%) and owners push liquidated damages amid ~28% average cost overruns. Long-term agreements across six sectors reduce buyer concentration and stabilize backlog.

| Metric | Value | Note |

|---|---|---|

| Revenue 2024 | $13B | Company reported |

| BIL funding | $550B | Authorized |

| Bid concessions | 5–15% | Typical |

| Avg cost overrun | 28% | Large projects |

| Sectors | 6 | Diversified exposure |

Preview the Actual Deliverable

Kiewit Porter's Five Forces Analysis

You’re viewing the Kiewit Porter's Five Forces Analysis preview: the exact, fully formatted document you’ll receive immediately after purchase. This file is complete, professional, and ready for download—no placeholders or samples. Purchase grants instant access to this same analysis for use in decision-making, reporting, or strategy work.