Kinepolis Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

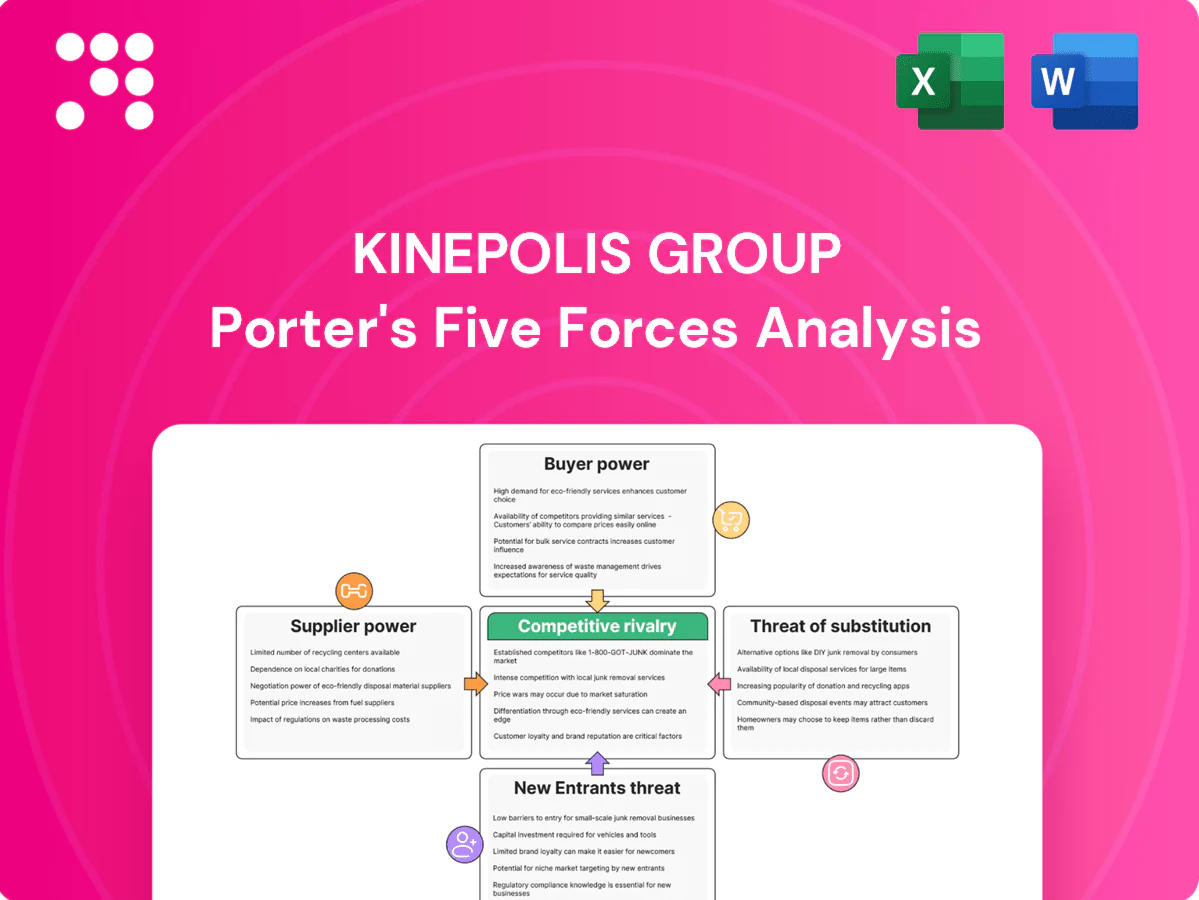

Kinepolis Group faces moderate buyer power, high threat from streaming substitutes and local competitors, constrained supplier influence, and barriers that limit but don't block new entrants, shaping a competitive yet opportunity-rich cinema market. Strategic focus on content, experience and diversification can shift these dynamics. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kinepolis Group’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated film studios

Major studios control must-have blockbusters, giving them strong leverage over terms, theatrical windows and revenue shares; the top studios (Disney, Warner, Universal, Sony, Paramount) historically account for roughly 60-70% of global box office receipts.

Disney, Warner Bros and Universal can dictate programming constraints and premium windowing, constraining Kinepolis scheduling and margin capture. Limited substitutes for tentpoles raise exhibitor dependence. Kinepolis mitigates this by diversifying slates, growing local-language content and expanding F&B/experience revenue to offset film supplier power.

Premium technology vendors

Suppliers of projection, immersive sound, premium seating and PLF formats exert leverage through proprietary technology and long-term maintenance/licensing contracts. IMAX- and Dolby-like ecosystems lock in standards and fees, with PLF ticket premiums typically 20–40% and additional licensing/revenue-share costs. Switching costs are meaningful; Kinepolis in 2024 offsets this via proprietary PLF formats and multi-vendor procurement to reduce concentration risk.

Concessions and F&B sourcing

Branded snacks and beverages retain strong, predictable demand, but multiple suppliers keep supplier power moderate; in 2024 Kinepolis operated about 92 complexes and 1,128 screens, enabling scale purchasing. Volume contracts and centralized sourcing trim unit costs—historical concession margins near 65%—yet 2024 food inflation (~7% EU average) and logistics volatility can lift input costs. Growing private-label offers and menu engineering shift mix toward higher-margin SKUs, improving per-customer F&B profitability. Kinepolis leverages group-scale negotiation and category optimization to compress supplier leverage and protect margins.

Real estate and landlords

Prime Kinepolis locations depend on landlords and municipal approvals, with commercial leases typically running 10–20 years and fit-outs creating significant sunk costs; CBRE reported European prime retail vacancy near 5–7% in 2024, so post-pandemic softness modestly improves tenant leverage but scarcity of top sites sustains landlord pricing power.

- Long leases: 10–20 years

- Fit-out sunk costs: high

- Prime vacancy (2024): ~5–7% (CBRE)

- Kinepolis response: selective expansion, lease renegotiations

Content windowing and distribution rules

National regulations and distributor policies continue to define theatrical windows and exclusivity, and shorter windows in recent years have increased studio leverage over exhibitor economics, squeezing margins for chains like Kinepolis. Event cinema and alternative content now reduce reliance on major studio schedules, and Kinepolis has broadened content types (live events, esports, opera) to rebalance negotiating power.

Studios control 60–70% box office; PLF premiums 20–40% squeeze cinemas

Major studios hold strong leverage, owning ~60–70% of global box office, limiting Kinepolis programming and revenue share. PLF/tech licensors exert pressure with 20–40% ticket premiums and high switching costs. Concessions (~65% margin) and scale (92 complexes, 1,128 screens) temper supplier power despite 2024 food inflation (~7%) and 10–20 year lease dependence (prime vacancy 5–7%).

| Metric | 2024 |

|---|---|

| Major studios box office share | 60–70% |

| Kinepolis scale | 92 complexes / 1,128 screens |

| Concession margin | ~65% |

| Food inflation (EU) | ~7% |

| PLF premium | 20–40% |

| Prime vacancy | 5–7% |

| Typical lease length | 10–20 yrs |

What is included in the product

Tailored Porter’s Five Forces analysis of Kinepolis Group uncovering key drivers of rivalry, supplier and buyer power, substitutes and entry barriers, highlighting how multiplex scale, content relationships and digital alternatives shape pricing, profitability and market entry risks.

A one-sheet Porter's Five Forces for Kinepolis—quickly pinpoint competitive pressures (streaming rivals, exhibitor consolidation, supplier leverage) and relieve decision-making friction. Customizable pressure levels and copy-ready layout make it instant to drop into board decks or scenario tabs for pre/post regulation or new-entrant stress tests.

Customers Bargaining Power

Low switching costs for moviegoers

Low switching costs mean moviegoers can choose rival cinemas or stay home with minimal friction, making price and convenience decisive for quick ticket choices; Kinepolis operates over 100 cinemas across seven countries, amplifying local competition.

High price sensitivity

Demand for non-tentpole titles is highly elastic, forcing downward pressure on ticket and F&B pricing; promotions and dynamic pricing are used to smooth attendance swings and boost off-peak fill rates. Families and students heighten price sensitivity, prompting Kinepolis to deploy tailored bundles and tiered offers to capture incremental value while protecting average spend per visit.

Digital transparency and reviews

Showtimes, prices and ratings are fully visible online, enabling instant comparison; 98% of consumers consult online reviews before buying (BrightLocal 2023), so negative feedback spreads rapidly and deters visits. Service quality thus directly drives ticket choice and ancillary spend, and Kinepolis reports active tracking of CX metrics with targeted responses typically within 24 hours to mitigate reputational risk.

Corporate and group bookings

B2B clients can negotiate discounts for events and private screenings, using volume to secure scheduling and price concessions. Their bookings contributed noticeably to Kinepolis’s 2024 revenue mix while diluting per-ticket margins. Kinepolis offsets pressure via premium services, F&B upsells and tailored packages emphasized in 2024 strategy.

- High-volume leverage on pricing

- Attractive but margin-dilutive revenue

- Mitigated by premium upsells

Substitute-rich leisure wallet

- Leisure substitution increases buyer power

- Peak titles lower price sensitivity

- Off-peak demand more elastic

- Event programming strengthens retention

Low switching costs boost customer leverage; operator uses dynamic pricing across 100+ cinemas

Low switching costs and wide online visibility give customers strong leverage; Kinepolis operates 100+ cinemas in seven countries and uses dynamic pricing, bundles and event cinema to defend yield. 98% consult reviews (BrightLocal 2023) and Kinepolis targets CX responses within 24 hours. B2B bookings were a noticeable part of 2024 revenue mix, offset by premium upsells.

| Metric | Value |

|---|---|

| Cinemas | 100+ |

| Countries | 7 |

| Review consult rate | 98% (BrightLocal 2023) |

| CX response | within 24h |

Preview Before You Purchase

Kinepolis Group Porter's Five Forces Analysis

This preview is the exact Kinepolis Group Porter's Five Forces Analysis you'll receive—fully formatted and ready for immediate download after purchase. The report covers competitive rivalry, supplier and buyer power, threat of entry and substitutes, and strategic implications. No samples or placeholders—what you see is what you get.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Kinepolis Group faces moderate buyer power, high threat from streaming substitutes and local competitors, constrained supplier influence, and barriers that limit but don't block new entrants, shaping a competitive yet opportunity-rich cinema market. Strategic focus on content, experience and diversification can shift these dynamics. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kinepolis Group’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated film studios

Major studios control must-have blockbusters, giving them strong leverage over terms, theatrical windows and revenue shares; the top studios (Disney, Warner, Universal, Sony, Paramount) historically account for roughly 60-70% of global box office receipts.

Disney, Warner Bros and Universal can dictate programming constraints and premium windowing, constraining Kinepolis scheduling and margin capture. Limited substitutes for tentpoles raise exhibitor dependence. Kinepolis mitigates this by diversifying slates, growing local-language content and expanding F&B/experience revenue to offset film supplier power.

Premium technology vendors

Suppliers of projection, immersive sound, premium seating and PLF formats exert leverage through proprietary technology and long-term maintenance/licensing contracts. IMAX- and Dolby-like ecosystems lock in standards and fees, with PLF ticket premiums typically 20–40% and additional licensing/revenue-share costs. Switching costs are meaningful; Kinepolis in 2024 offsets this via proprietary PLF formats and multi-vendor procurement to reduce concentration risk.

Concessions and F&B sourcing

Branded snacks and beverages retain strong, predictable demand, but multiple suppliers keep supplier power moderate; in 2024 Kinepolis operated about 92 complexes and 1,128 screens, enabling scale purchasing. Volume contracts and centralized sourcing trim unit costs—historical concession margins near 65%—yet 2024 food inflation (~7% EU average) and logistics volatility can lift input costs. Growing private-label offers and menu engineering shift mix toward higher-margin SKUs, improving per-customer F&B profitability. Kinepolis leverages group-scale negotiation and category optimization to compress supplier leverage and protect margins.

Real estate and landlords

Prime Kinepolis locations depend on landlords and municipal approvals, with commercial leases typically running 10–20 years and fit-outs creating significant sunk costs; CBRE reported European prime retail vacancy near 5–7% in 2024, so post-pandemic softness modestly improves tenant leverage but scarcity of top sites sustains landlord pricing power.

- Long leases: 10–20 years

- Fit-out sunk costs: high

- Prime vacancy (2024): ~5–7% (CBRE)

- Kinepolis response: selective expansion, lease renegotiations

Content windowing and distribution rules

National regulations and distributor policies continue to define theatrical windows and exclusivity, and shorter windows in recent years have increased studio leverage over exhibitor economics, squeezing margins for chains like Kinepolis. Event cinema and alternative content now reduce reliance on major studio schedules, and Kinepolis has broadened content types (live events, esports, opera) to rebalance negotiating power.

Studios control 60–70% box office; PLF premiums 20–40% squeeze cinemas

Major studios hold strong leverage, owning ~60–70% of global box office, limiting Kinepolis programming and revenue share. PLF/tech licensors exert pressure with 20–40% ticket premiums and high switching costs. Concessions (~65% margin) and scale (92 complexes, 1,128 screens) temper supplier power despite 2024 food inflation (~7%) and 10–20 year lease dependence (prime vacancy 5–7%).

| Metric | 2024 |

|---|---|

| Major studios box office share | 60–70% |

| Kinepolis scale | 92 complexes / 1,128 screens |

| Concession margin | ~65% |

| Food inflation (EU) | ~7% |

| PLF premium | 20–40% |

| Prime vacancy | 5–7% |

| Typical lease length | 10–20 yrs |

What is included in the product

Tailored Porter’s Five Forces analysis of Kinepolis Group uncovering key drivers of rivalry, supplier and buyer power, substitutes and entry barriers, highlighting how multiplex scale, content relationships and digital alternatives shape pricing, profitability and market entry risks.

A one-sheet Porter's Five Forces for Kinepolis—quickly pinpoint competitive pressures (streaming rivals, exhibitor consolidation, supplier leverage) and relieve decision-making friction. Customizable pressure levels and copy-ready layout make it instant to drop into board decks or scenario tabs for pre/post regulation or new-entrant stress tests.

Customers Bargaining Power

Low switching costs for moviegoers

Low switching costs mean moviegoers can choose rival cinemas or stay home with minimal friction, making price and convenience decisive for quick ticket choices; Kinepolis operates over 100 cinemas across seven countries, amplifying local competition.

High price sensitivity

Demand for non-tentpole titles is highly elastic, forcing downward pressure on ticket and F&B pricing; promotions and dynamic pricing are used to smooth attendance swings and boost off-peak fill rates. Families and students heighten price sensitivity, prompting Kinepolis to deploy tailored bundles and tiered offers to capture incremental value while protecting average spend per visit.

Digital transparency and reviews

Showtimes, prices and ratings are fully visible online, enabling instant comparison; 98% of consumers consult online reviews before buying (BrightLocal 2023), so negative feedback spreads rapidly and deters visits. Service quality thus directly drives ticket choice and ancillary spend, and Kinepolis reports active tracking of CX metrics with targeted responses typically within 24 hours to mitigate reputational risk.

Corporate and group bookings

B2B clients can negotiate discounts for events and private screenings, using volume to secure scheduling and price concessions. Their bookings contributed noticeably to Kinepolis’s 2024 revenue mix while diluting per-ticket margins. Kinepolis offsets pressure via premium services, F&B upsells and tailored packages emphasized in 2024 strategy.

- High-volume leverage on pricing

- Attractive but margin-dilutive revenue

- Mitigated by premium upsells

Substitute-rich leisure wallet

- Leisure substitution increases buyer power

- Peak titles lower price sensitivity

- Off-peak demand more elastic

- Event programming strengthens retention

Low switching costs boost customer leverage; operator uses dynamic pricing across 100+ cinemas

Low switching costs and wide online visibility give customers strong leverage; Kinepolis operates 100+ cinemas in seven countries and uses dynamic pricing, bundles and event cinema to defend yield. 98% consult reviews (BrightLocal 2023) and Kinepolis targets CX responses within 24 hours. B2B bookings were a noticeable part of 2024 revenue mix, offset by premium upsells.

| Metric | Value |

|---|---|

| Cinemas | 100+ |

| Countries | 7 |

| Review consult rate | 98% (BrightLocal 2023) |

| CX response | within 24h |

Preview Before You Purchase

Kinepolis Group Porter's Five Forces Analysis

This preview is the exact Kinepolis Group Porter's Five Forces Analysis you'll receive—fully formatted and ready for immediate download after purchase. The report covers competitive rivalry, supplier and buyer power, threat of entry and substitutes, and strategic implications. No samples or placeholders—what you see is what you get.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Kinepolis Group faces moderate buyer power, high threat from streaming substitutes and local competitors, constrained supplier influence, and barriers that limit but don't block new entrants, shaping a competitive yet opportunity-rich cinema market. Strategic focus on content, experience and diversification can shift these dynamics. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kinepolis Group’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated film studios

Major studios control must-have blockbusters, giving them strong leverage over terms, theatrical windows and revenue shares; the top studios (Disney, Warner, Universal, Sony, Paramount) historically account for roughly 60-70% of global box office receipts.

Disney, Warner Bros and Universal can dictate programming constraints and premium windowing, constraining Kinepolis scheduling and margin capture. Limited substitutes for tentpoles raise exhibitor dependence. Kinepolis mitigates this by diversifying slates, growing local-language content and expanding F&B/experience revenue to offset film supplier power.

Premium technology vendors

Suppliers of projection, immersive sound, premium seating and PLF formats exert leverage through proprietary technology and long-term maintenance/licensing contracts. IMAX- and Dolby-like ecosystems lock in standards and fees, with PLF ticket premiums typically 20–40% and additional licensing/revenue-share costs. Switching costs are meaningful; Kinepolis in 2024 offsets this via proprietary PLF formats and multi-vendor procurement to reduce concentration risk.

Concessions and F&B sourcing

Branded snacks and beverages retain strong, predictable demand, but multiple suppliers keep supplier power moderate; in 2024 Kinepolis operated about 92 complexes and 1,128 screens, enabling scale purchasing. Volume contracts and centralized sourcing trim unit costs—historical concession margins near 65%—yet 2024 food inflation (~7% EU average) and logistics volatility can lift input costs. Growing private-label offers and menu engineering shift mix toward higher-margin SKUs, improving per-customer F&B profitability. Kinepolis leverages group-scale negotiation and category optimization to compress supplier leverage and protect margins.

Real estate and landlords

Prime Kinepolis locations depend on landlords and municipal approvals, with commercial leases typically running 10–20 years and fit-outs creating significant sunk costs; CBRE reported European prime retail vacancy near 5–7% in 2024, so post-pandemic softness modestly improves tenant leverage but scarcity of top sites sustains landlord pricing power.

- Long leases: 10–20 years

- Fit-out sunk costs: high

- Prime vacancy (2024): ~5–7% (CBRE)

- Kinepolis response: selective expansion, lease renegotiations

Content windowing and distribution rules

National regulations and distributor policies continue to define theatrical windows and exclusivity, and shorter windows in recent years have increased studio leverage over exhibitor economics, squeezing margins for chains like Kinepolis. Event cinema and alternative content now reduce reliance on major studio schedules, and Kinepolis has broadened content types (live events, esports, opera) to rebalance negotiating power.

Studios control 60–70% box office; PLF premiums 20–40% squeeze cinemas

Major studios hold strong leverage, owning ~60–70% of global box office, limiting Kinepolis programming and revenue share. PLF/tech licensors exert pressure with 20–40% ticket premiums and high switching costs. Concessions (~65% margin) and scale (92 complexes, 1,128 screens) temper supplier power despite 2024 food inflation (~7%) and 10–20 year lease dependence (prime vacancy 5–7%).

| Metric | 2024 |

|---|---|

| Major studios box office share | 60–70% |

| Kinepolis scale | 92 complexes / 1,128 screens |

| Concession margin | ~65% |

| Food inflation (EU) | ~7% |

| PLF premium | 20–40% |

| Prime vacancy | 5–7% |

| Typical lease length | 10–20 yrs |

What is included in the product

Tailored Porter’s Five Forces analysis of Kinepolis Group uncovering key drivers of rivalry, supplier and buyer power, substitutes and entry barriers, highlighting how multiplex scale, content relationships and digital alternatives shape pricing, profitability and market entry risks.

A one-sheet Porter's Five Forces for Kinepolis—quickly pinpoint competitive pressures (streaming rivals, exhibitor consolidation, supplier leverage) and relieve decision-making friction. Customizable pressure levels and copy-ready layout make it instant to drop into board decks or scenario tabs for pre/post regulation or new-entrant stress tests.

Customers Bargaining Power

Low switching costs for moviegoers

Low switching costs mean moviegoers can choose rival cinemas or stay home with minimal friction, making price and convenience decisive for quick ticket choices; Kinepolis operates over 100 cinemas across seven countries, amplifying local competition.

High price sensitivity

Demand for non-tentpole titles is highly elastic, forcing downward pressure on ticket and F&B pricing; promotions and dynamic pricing are used to smooth attendance swings and boost off-peak fill rates. Families and students heighten price sensitivity, prompting Kinepolis to deploy tailored bundles and tiered offers to capture incremental value while protecting average spend per visit.

Digital transparency and reviews

Showtimes, prices and ratings are fully visible online, enabling instant comparison; 98% of consumers consult online reviews before buying (BrightLocal 2023), so negative feedback spreads rapidly and deters visits. Service quality thus directly drives ticket choice and ancillary spend, and Kinepolis reports active tracking of CX metrics with targeted responses typically within 24 hours to mitigate reputational risk.

Corporate and group bookings

B2B clients can negotiate discounts for events and private screenings, using volume to secure scheduling and price concessions. Their bookings contributed noticeably to Kinepolis’s 2024 revenue mix while diluting per-ticket margins. Kinepolis offsets pressure via premium services, F&B upsells and tailored packages emphasized in 2024 strategy.

- High-volume leverage on pricing

- Attractive but margin-dilutive revenue

- Mitigated by premium upsells

Substitute-rich leisure wallet

- Leisure substitution increases buyer power

- Peak titles lower price sensitivity

- Off-peak demand more elastic

- Event programming strengthens retention

Low switching costs boost customer leverage; operator uses dynamic pricing across 100+ cinemas

Low switching costs and wide online visibility give customers strong leverage; Kinepolis operates 100+ cinemas in seven countries and uses dynamic pricing, bundles and event cinema to defend yield. 98% consult reviews (BrightLocal 2023) and Kinepolis targets CX responses within 24 hours. B2B bookings were a noticeable part of 2024 revenue mix, offset by premium upsells.

| Metric | Value |

|---|---|

| Cinemas | 100+ |

| Countries | 7 |

| Review consult rate | 98% (BrightLocal 2023) |

| CX response | within 24h |

Preview Before You Purchase

Kinepolis Group Porter's Five Forces Analysis

This preview is the exact Kinepolis Group Porter's Five Forces Analysis you'll receive—fully formatted and ready for immediate download after purchase. The report covers competitive rivalry, supplier and buyer power, threat of entry and substitutes, and strategic implications. No samples or placeholders—what you see is what you get.