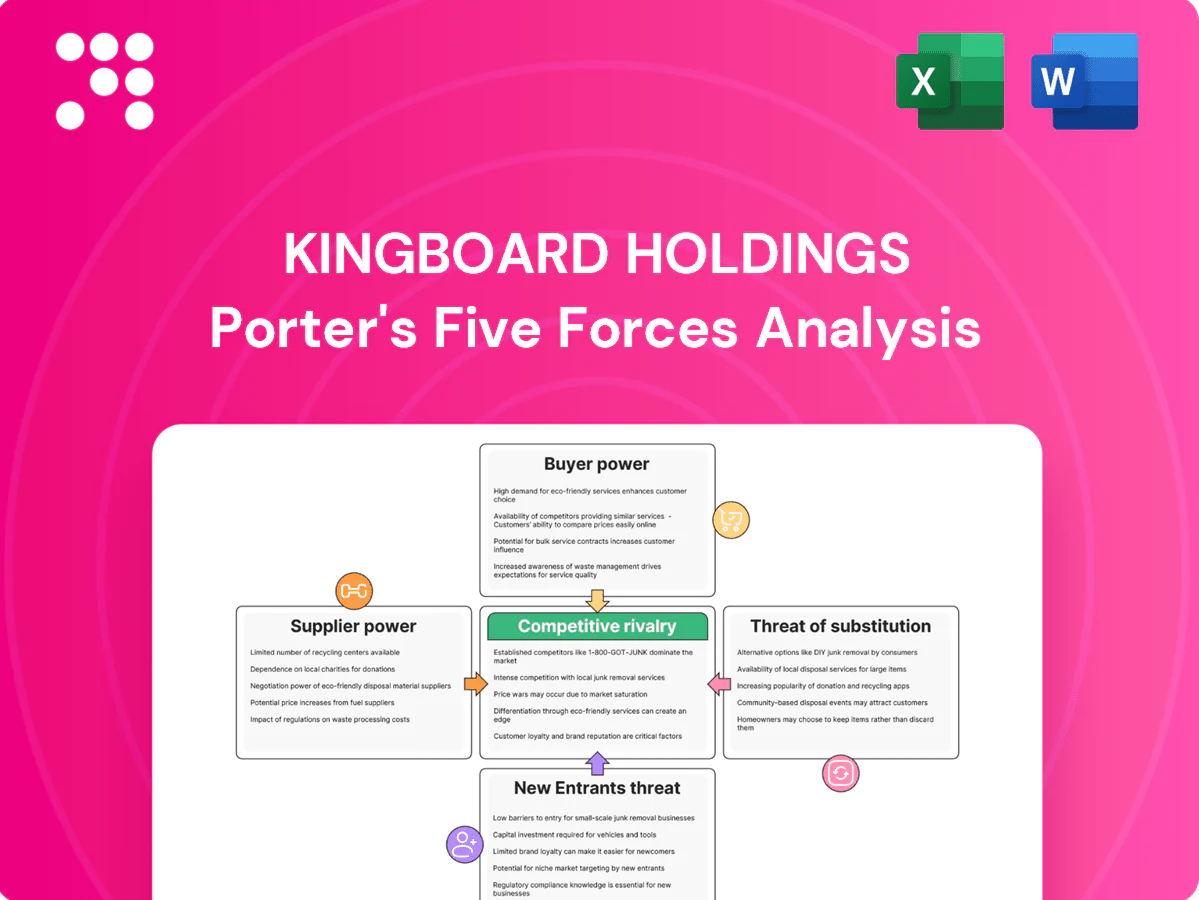

Kingboard Holdings Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Kingboard Holdings faces intense supplier and buyer dynamics, moderate threat from substitutes, and high industry rivalry driven by scale and cyclicality. This snapshot highlights strategic strengths but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for a consultant-grade breakdown of competitive intensity, risks, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Vertical integration dampens input leverage

Kingboard produces copper foil and glass fabric in-house, reducing dependence on external suppliers and dampening input leverage. This backward integration lowers price pressure and supply risk on critical laminate inputs and strengthens its bargaining position with remaining vendors. The group nevertheless relies on third-party resins, specialty chemicals and utilities for some process needs, keeping residual supplier exposure.

Commodity price volatility persists

Copper, epoxy resins, phenol and energy are globally traded commodities with volatile cycles—LME copper averaged about $9,500/tonne in 2024, Brent crude near $85/bbl and epoxy resin contract prices swung roughly ±30% YoY, letting suppliers pass spikes through and squeezing margins even at scale. Hedging and multiyear supply agreements at Kingboard mitigate but do not eliminate cost swings. Maintaining pricing discipline during up-cycles is therefore critical.

Specialized equipment vendor influence

PCB and laminate lines rely on precision presses, drills, imaging and plating tools supplied by a concentrated set of OEMs, giving those vendors measurable leverage over pricing and delivery. Service contracts and proprietary spare parts create switching frictions that raise effective replacement costs for Kingboard. Multivendor sourcing and aggregated volume purchasing are used to improve negotiation leverage and mitigate supplier concentration risk.

Environmental and utility constraints

Water, power and emissions compliance are controlled by regulated utilities and authorities, raising treatment and waste costs as standards tighten and permitting delays boost supplier leverage over capacity additions. Kingboard reduced exposure in 2024 through targeted energy-efficiency upgrades and ESG investments that lower operational and regulatory risk.

- Regulated utilities: leverage via permits

- Stricter standards: higher treatment/waste costs

- Permitting timelines: constrain capacity additions

- Efficiency & ESG (2024): lower exposure

Logistics and material lead-time sensitivity

Glass yarn, specialty chemicals and copper throughput in 2024 remained lead-time sensitive, with LME copper averaging about $9,000/ton, elevating inventory value and risk; port congestion and hazardous-material handling rules increase supplier coordination power and delay raw-material inflows. Nearshoring and multi-warehouse footprints materially lower disruption exposure, while digital planning and real-time visibility strengthen Kingboard Holdings bargaining stance with suppliers.

- High-value inventory: copper ≈ $9,000/ton (2024)

- Logistics risk: port/hazard rules raise supplier power

- Mitigation: nearshoring + multi-warehouse

- Advantage: digital planning boosts visibility & negotiation

Backward integration cuts leverage; 30% epoxy swings squeeze margins

Backward integration in copper foil and glass fabric lowers supplier leverage, but reliance on resins, specialty chemicals and utilities leaves residual exposure. Commodities volatility (LME copper ≈ $9,500/t; Brent ≈ $85/bbl; epoxy ±30% YoY) lets suppliers pass costs, pressuring margins despite hedges. OEM concentration for PCB equipment and regulated utilities raise switching costs and permit-driven delivery risk.

| Metric | 2024 Value | Impact |

|---|---|---|

| LME copper | $9,500/ton | High input cost/ inventory risk |

| Brent | $85/bbl | Energy cost pressure |

| Epoxy price swing | ±30% YoY | Margin volatility |

What is included in the product

Tailored Porter’s Five Forces analysis for Kingboard Holdings that uncovers competitive intensity, supplier and buyer power, substitutes and entrant threats, and identifies disruptive forces and market dynamics shaping its pricing, margins and strategic defenses.

A concise one-sheet Porter's Five Forces for Kingboard Holdings that highlights supplier/customer bargaining, rival intensity, entry threats and substitutes—ready to drop into decks; customize pressure levels and duplicate scenarios to test regulatory or market shifts without coding.

Customers Bargaining Power

Consolidated OEM/EMS customers negotiate hard

Large electronics OEMs, ODMs and EMS customers increasingly pool volumes to extract concessions, using frame agreements and e-auctions to drive down laminate and PCB prices.

Their sheer scale and dual-sourcing policies magnify negotiating leverage, compressing margins for suppliers despite Kingboard’s diversified product scope and global footprint.

Qualification creates switching frictions

Laminates and PCBs require stringent certifications (IPC, UL) and extended reliability testing, with supplier qualification commonly taking six months or longer. Once qualified, customers incur time and technical risk costs to switch, raising effective switching frictions and reducing buyer power in high-spec segments. Consistent yield performance and dedicated technical support further embed supplier relationships and lock in procurement decisions.

Spec mix drives sensitivity

Standard FR-4 buyers remain highly price sensitive with abundant alternatives, compressing margins; spot FR-4 prices fell ~15% in 2023–24 amid excess capacity. High-frequency, halogen-free, HDI and automotive grades prioritize performance and yield, typically commanding 20–40% premiums and representing the faster-growing share of demand in 2024. These premium segments dilute overall buyer leverage and make application engineering a key negotiating differentiator.

Demand cyclicality shifts leverage

In downturns buyers push for price cuts and extended terms amid excess capacity; Kingboard faced margin pressure as industry demand softened in 2024 while the global PCB and laminate market was roughly USD 60 billion, shifting leverage toward customers.

In up-cycles tight supply reverses leverage to producers; balanced contracts, allocation policies and vendor-managed inventory programs help smooth extremes and align incentives.

- Buyer leverage: price cuts, extended terms

- Producer leverage: tight supply in up-cycles

- Mitigants: balanced contracts, allocation policies

- Alignment: inventory programs, VMI

Service, lead time, and reliability matter

In 2024 short lead times, stable quality and technical co-development with OEMs shifted buyers away from pure price focus, as continuity on critical programs became a higher priority; vendor-managed inventory and local engineering support raised practical switching costs, and end-to-end integration strengthened Kingboard’s bargaining position.

- Less price pressure

- Higher switching costs

- Continuity valued

- Integration advantage

FR-4 -15%; HDI/auto +20–40% raise supplier leverage

Large OEMs/EMS exert strong price pressure—spot FR-4 prices fell ~15% in 2023–24, shifting leverage toward buyers despite a ~USD 60bn PCB/laminate market in 2024.

High-spec grades (HDI, automotive, halogen-free) grew in 2024 and command 20–40% premiums, raising switching costs and diluting buyer power.

Supplier qualification (>6 months), VMI and local engineering limit switching, partially restoring Kingboard’s negotiating leverage.

| Metric | 2024 | Impact |

|---|---|---|

| Market size | USD 60bn | Scale = buyer consolidation |

| FR-4 price change | -15% | Buyer leverage |

| Premium grades | +20–40% price | Supplier leverage |

| Qualification time | >6 months | Higher switching cost |

Same Document Delivered

Kingboard Holdings Porter's Five Forces Analysis

This preview shows the exact Kingboard Holdings Porter’s Five Forces analysis you’ll receive immediately after purchase—no mockups, no placeholders. The file is fully formatted, professionally written and ready for use in decision-making or reporting. Once paid, you get instant access to this same document for download and application.

From Overview to Strategy Blueprint

Kingboard Holdings faces intense supplier and buyer dynamics, moderate threat from substitutes, and high industry rivalry driven by scale and cyclicality. This snapshot highlights strategic strengths but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for a consultant-grade breakdown of competitive intensity, risks, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Vertical integration dampens input leverage

Kingboard produces copper foil and glass fabric in-house, reducing dependence on external suppliers and dampening input leverage. This backward integration lowers price pressure and supply risk on critical laminate inputs and strengthens its bargaining position with remaining vendors. The group nevertheless relies on third-party resins, specialty chemicals and utilities for some process needs, keeping residual supplier exposure.

Commodity price volatility persists

Copper, epoxy resins, phenol and energy are globally traded commodities with volatile cycles—LME copper averaged about $9,500/tonne in 2024, Brent crude near $85/bbl and epoxy resin contract prices swung roughly ±30% YoY, letting suppliers pass spikes through and squeezing margins even at scale. Hedging and multiyear supply agreements at Kingboard mitigate but do not eliminate cost swings. Maintaining pricing discipline during up-cycles is therefore critical.

Specialized equipment vendor influence

PCB and laminate lines rely on precision presses, drills, imaging and plating tools supplied by a concentrated set of OEMs, giving those vendors measurable leverage over pricing and delivery. Service contracts and proprietary spare parts create switching frictions that raise effective replacement costs for Kingboard. Multivendor sourcing and aggregated volume purchasing are used to improve negotiation leverage and mitigate supplier concentration risk.

Environmental and utility constraints

Water, power and emissions compliance are controlled by regulated utilities and authorities, raising treatment and waste costs as standards tighten and permitting delays boost supplier leverage over capacity additions. Kingboard reduced exposure in 2024 through targeted energy-efficiency upgrades and ESG investments that lower operational and regulatory risk.

- Regulated utilities: leverage via permits

- Stricter standards: higher treatment/waste costs

- Permitting timelines: constrain capacity additions

- Efficiency & ESG (2024): lower exposure

Logistics and material lead-time sensitivity

Glass yarn, specialty chemicals and copper throughput in 2024 remained lead-time sensitive, with LME copper averaging about $9,000/ton, elevating inventory value and risk; port congestion and hazardous-material handling rules increase supplier coordination power and delay raw-material inflows. Nearshoring and multi-warehouse footprints materially lower disruption exposure, while digital planning and real-time visibility strengthen Kingboard Holdings bargaining stance with suppliers.

- High-value inventory: copper ≈ $9,000/ton (2024)

- Logistics risk: port/hazard rules raise supplier power

- Mitigation: nearshoring + multi-warehouse

- Advantage: digital planning boosts visibility & negotiation

Backward integration cuts leverage; 30% epoxy swings squeeze margins

Backward integration in copper foil and glass fabric lowers supplier leverage, but reliance on resins, specialty chemicals and utilities leaves residual exposure. Commodities volatility (LME copper ≈ $9,500/t; Brent ≈ $85/bbl; epoxy ±30% YoY) lets suppliers pass costs, pressuring margins despite hedges. OEM concentration for PCB equipment and regulated utilities raise switching costs and permit-driven delivery risk.

| Metric | 2024 Value | Impact |

|---|---|---|

| LME copper | $9,500/ton | High input cost/ inventory risk |

| Brent | $85/bbl | Energy cost pressure |

| Epoxy price swing | ±30% YoY | Margin volatility |

What is included in the product

Tailored Porter’s Five Forces analysis for Kingboard Holdings that uncovers competitive intensity, supplier and buyer power, substitutes and entrant threats, and identifies disruptive forces and market dynamics shaping its pricing, margins and strategic defenses.

A concise one-sheet Porter's Five Forces for Kingboard Holdings that highlights supplier/customer bargaining, rival intensity, entry threats and substitutes—ready to drop into decks; customize pressure levels and duplicate scenarios to test regulatory or market shifts without coding.

Customers Bargaining Power

Consolidated OEM/EMS customers negotiate hard

Large electronics OEMs, ODMs and EMS customers increasingly pool volumes to extract concessions, using frame agreements and e-auctions to drive down laminate and PCB prices.

Their sheer scale and dual-sourcing policies magnify negotiating leverage, compressing margins for suppliers despite Kingboard’s diversified product scope and global footprint.

Qualification creates switching frictions

Laminates and PCBs require stringent certifications (IPC, UL) and extended reliability testing, with supplier qualification commonly taking six months or longer. Once qualified, customers incur time and technical risk costs to switch, raising effective switching frictions and reducing buyer power in high-spec segments. Consistent yield performance and dedicated technical support further embed supplier relationships and lock in procurement decisions.

Spec mix drives sensitivity

Standard FR-4 buyers remain highly price sensitive with abundant alternatives, compressing margins; spot FR-4 prices fell ~15% in 2023–24 amid excess capacity. High-frequency, halogen-free, HDI and automotive grades prioritize performance and yield, typically commanding 20–40% premiums and representing the faster-growing share of demand in 2024. These premium segments dilute overall buyer leverage and make application engineering a key negotiating differentiator.

Demand cyclicality shifts leverage

In downturns buyers push for price cuts and extended terms amid excess capacity; Kingboard faced margin pressure as industry demand softened in 2024 while the global PCB and laminate market was roughly USD 60 billion, shifting leverage toward customers.

In up-cycles tight supply reverses leverage to producers; balanced contracts, allocation policies and vendor-managed inventory programs help smooth extremes and align incentives.

- Buyer leverage: price cuts, extended terms

- Producer leverage: tight supply in up-cycles

- Mitigants: balanced contracts, allocation policies

- Alignment: inventory programs, VMI

Service, lead time, and reliability matter

In 2024 short lead times, stable quality and technical co-development with OEMs shifted buyers away from pure price focus, as continuity on critical programs became a higher priority; vendor-managed inventory and local engineering support raised practical switching costs, and end-to-end integration strengthened Kingboard’s bargaining position.

- Less price pressure

- Higher switching costs

- Continuity valued

- Integration advantage

FR-4 -15%; HDI/auto +20–40% raise supplier leverage

Large OEMs/EMS exert strong price pressure—spot FR-4 prices fell ~15% in 2023–24, shifting leverage toward buyers despite a ~USD 60bn PCB/laminate market in 2024.

High-spec grades (HDI, automotive, halogen-free) grew in 2024 and command 20–40% premiums, raising switching costs and diluting buyer power.

Supplier qualification (>6 months), VMI and local engineering limit switching, partially restoring Kingboard’s negotiating leverage.

| Metric | 2024 | Impact |

|---|---|---|

| Market size | USD 60bn | Scale = buyer consolidation |

| FR-4 price change | -15% | Buyer leverage |

| Premium grades | +20–40% price | Supplier leverage |

| Qualification time | >6 months | Higher switching cost |

Same Document Delivered

Kingboard Holdings Porter's Five Forces Analysis

This preview shows the exact Kingboard Holdings Porter’s Five Forces analysis you’ll receive immediately after purchase—no mockups, no placeholders. The file is fully formatted, professionally written and ready for use in decision-making or reporting. Once paid, you get instant access to this same document for download and application.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Kingboard Holdings faces intense supplier and buyer dynamics, moderate threat from substitutes, and high industry rivalry driven by scale and cyclicality. This snapshot highlights strategic strengths but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for a consultant-grade breakdown of competitive intensity, risks, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Vertical integration dampens input leverage

Kingboard produces copper foil and glass fabric in-house, reducing dependence on external suppliers and dampening input leverage. This backward integration lowers price pressure and supply risk on critical laminate inputs and strengthens its bargaining position with remaining vendors. The group nevertheless relies on third-party resins, specialty chemicals and utilities for some process needs, keeping residual supplier exposure.

Commodity price volatility persists

Copper, epoxy resins, phenol and energy are globally traded commodities with volatile cycles—LME copper averaged about $9,500/tonne in 2024, Brent crude near $85/bbl and epoxy resin contract prices swung roughly ±30% YoY, letting suppliers pass spikes through and squeezing margins even at scale. Hedging and multiyear supply agreements at Kingboard mitigate but do not eliminate cost swings. Maintaining pricing discipline during up-cycles is therefore critical.

Specialized equipment vendor influence

PCB and laminate lines rely on precision presses, drills, imaging and plating tools supplied by a concentrated set of OEMs, giving those vendors measurable leverage over pricing and delivery. Service contracts and proprietary spare parts create switching frictions that raise effective replacement costs for Kingboard. Multivendor sourcing and aggregated volume purchasing are used to improve negotiation leverage and mitigate supplier concentration risk.

Environmental and utility constraints

Water, power and emissions compliance are controlled by regulated utilities and authorities, raising treatment and waste costs as standards tighten and permitting delays boost supplier leverage over capacity additions. Kingboard reduced exposure in 2024 through targeted energy-efficiency upgrades and ESG investments that lower operational and regulatory risk.

- Regulated utilities: leverage via permits

- Stricter standards: higher treatment/waste costs

- Permitting timelines: constrain capacity additions

- Efficiency & ESG (2024): lower exposure

Logistics and material lead-time sensitivity

Glass yarn, specialty chemicals and copper throughput in 2024 remained lead-time sensitive, with LME copper averaging about $9,000/ton, elevating inventory value and risk; port congestion and hazardous-material handling rules increase supplier coordination power and delay raw-material inflows. Nearshoring and multi-warehouse footprints materially lower disruption exposure, while digital planning and real-time visibility strengthen Kingboard Holdings bargaining stance with suppliers.

- High-value inventory: copper ≈ $9,000/ton (2024)

- Logistics risk: port/hazard rules raise supplier power

- Mitigation: nearshoring + multi-warehouse

- Advantage: digital planning boosts visibility & negotiation

Backward integration cuts leverage; 30% epoxy swings squeeze margins

Backward integration in copper foil and glass fabric lowers supplier leverage, but reliance on resins, specialty chemicals and utilities leaves residual exposure. Commodities volatility (LME copper ≈ $9,500/t; Brent ≈ $85/bbl; epoxy ±30% YoY) lets suppliers pass costs, pressuring margins despite hedges. OEM concentration for PCB equipment and regulated utilities raise switching costs and permit-driven delivery risk.

| Metric | 2024 Value | Impact |

|---|---|---|

| LME copper | $9,500/ton | High input cost/ inventory risk |

| Brent | $85/bbl | Energy cost pressure |

| Epoxy price swing | ±30% YoY | Margin volatility |

What is included in the product

Tailored Porter’s Five Forces analysis for Kingboard Holdings that uncovers competitive intensity, supplier and buyer power, substitutes and entrant threats, and identifies disruptive forces and market dynamics shaping its pricing, margins and strategic defenses.

A concise one-sheet Porter's Five Forces for Kingboard Holdings that highlights supplier/customer bargaining, rival intensity, entry threats and substitutes—ready to drop into decks; customize pressure levels and duplicate scenarios to test regulatory or market shifts without coding.

Customers Bargaining Power

Consolidated OEM/EMS customers negotiate hard

Large electronics OEMs, ODMs and EMS customers increasingly pool volumes to extract concessions, using frame agreements and e-auctions to drive down laminate and PCB prices.

Their sheer scale and dual-sourcing policies magnify negotiating leverage, compressing margins for suppliers despite Kingboard’s diversified product scope and global footprint.

Qualification creates switching frictions

Laminates and PCBs require stringent certifications (IPC, UL) and extended reliability testing, with supplier qualification commonly taking six months or longer. Once qualified, customers incur time and technical risk costs to switch, raising effective switching frictions and reducing buyer power in high-spec segments. Consistent yield performance and dedicated technical support further embed supplier relationships and lock in procurement decisions.

Spec mix drives sensitivity

Standard FR-4 buyers remain highly price sensitive with abundant alternatives, compressing margins; spot FR-4 prices fell ~15% in 2023–24 amid excess capacity. High-frequency, halogen-free, HDI and automotive grades prioritize performance and yield, typically commanding 20–40% premiums and representing the faster-growing share of demand in 2024. These premium segments dilute overall buyer leverage and make application engineering a key negotiating differentiator.

Demand cyclicality shifts leverage

In downturns buyers push for price cuts and extended terms amid excess capacity; Kingboard faced margin pressure as industry demand softened in 2024 while the global PCB and laminate market was roughly USD 60 billion, shifting leverage toward customers.

In up-cycles tight supply reverses leverage to producers; balanced contracts, allocation policies and vendor-managed inventory programs help smooth extremes and align incentives.

- Buyer leverage: price cuts, extended terms

- Producer leverage: tight supply in up-cycles

- Mitigants: balanced contracts, allocation policies

- Alignment: inventory programs, VMI

Service, lead time, and reliability matter

In 2024 short lead times, stable quality and technical co-development with OEMs shifted buyers away from pure price focus, as continuity on critical programs became a higher priority; vendor-managed inventory and local engineering support raised practical switching costs, and end-to-end integration strengthened Kingboard’s bargaining position.

- Less price pressure

- Higher switching costs

- Continuity valued

- Integration advantage

FR-4 -15%; HDI/auto +20–40% raise supplier leverage

Large OEMs/EMS exert strong price pressure—spot FR-4 prices fell ~15% in 2023–24, shifting leverage toward buyers despite a ~USD 60bn PCB/laminate market in 2024.

High-spec grades (HDI, automotive, halogen-free) grew in 2024 and command 20–40% premiums, raising switching costs and diluting buyer power.

Supplier qualification (>6 months), VMI and local engineering limit switching, partially restoring Kingboard’s negotiating leverage.

| Metric | 2024 | Impact |

|---|---|---|

| Market size | USD 60bn | Scale = buyer consolidation |

| FR-4 price change | -15% | Buyer leverage |

| Premium grades | +20–40% price | Supplier leverage |

| Qualification time | >6 months | Higher switching cost |

Same Document Delivered

Kingboard Holdings Porter's Five Forces Analysis

This preview shows the exact Kingboard Holdings Porter’s Five Forces analysis you’ll receive immediately after purchase—no mockups, no placeholders. The file is fully formatted, professionally written and ready for use in decision-making or reporting. Once paid, you get instant access to this same document for download and application.