Kingfisher Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

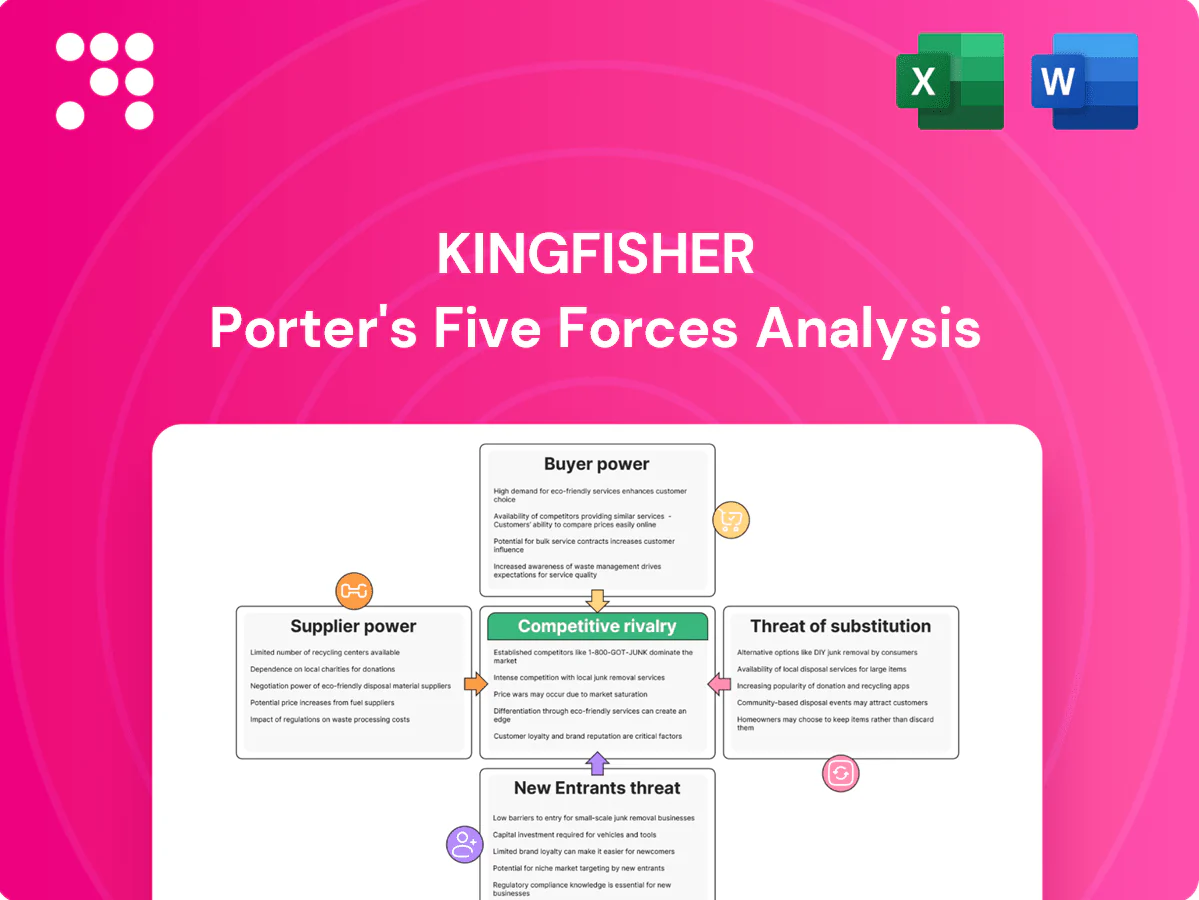

Kingfisher faces varied pressures—from concentrated suppliers and savvy buyers to digitization-driven substitutes and moderate entry barriers—shaping margins and expansion choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kingfisher’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scale leverage and OEB

Kingfisher’s pan‑European scale (presence in 10 countries and c.1,200 stores in 2024) plus Own Exclusive Brands like GoodHome and Erbauer reduce dependence on national brands and improve negotiating leverage. Private label penetration lets Kingfisher substitute branded SKUs, disciplining vendor pricing and protecting gross margins. Centralized sourcing and consolidated buys drive volume discounts, while sustaining OEB quality demands robust supplier development and QA processes.

Supplier fragmentation vs branded concentration

Building materials and fittings remain highly fragmented, limiting individual supplier leverage, while power tools and paint show strong brand concentration—Bosch, Makita, SBD and Dulux dominate category listings. Kingfisher (FY24 sales £12.8bn) uses range rationalization and dual‑sourcing plus exclusive ranges and long‑term agreements to balance brand pull with retailer control.

Logistics integration and vendor terms

In 2024 Kingfisher’s owned distribution centres, drop‑ship options and aligned replenishment broaden supplier switching and standardise contract terms, while vendors accept tighter trading margins for pan‑EU throughput; VMI and shared sales data secure faster lead times and higher fill rates, though persistent freight and commodity price volatility in 2024 continues to force periodic renegotiation.

Compliance and sustainability requirements

Compliance and sustainability requirements — ESG standards, timber legality and product stewardship — have narrowed Kingfisher’s approved supplier pool, raising compliance costs for vendors; Kingfisher reported 96% of timber from more sustainable sources in FY24, strengthening its leverage to set specs and audits. Suppliers with eco‑labels gain shelf access and volume, while smaller vendors face higher relative burden, reducing their bargaining power.

- ESG-driven supplier narrowing

- 96% sustainable timber (FY24)

- Eco-labels = shelf access/volume

- Higher relative costs for smaller vendors

Innovation and exclusivity dynamics

Suppliers with patent-backed innovation retain pricing power, but Kingfisher’s push for retailer-exclusive SKUs and co-development shifts margin leverage toward the channel; Kingfisher reported FY 2024 revenue ~£11.6bn, underscoring scale in negotiating supplier terms. OEB fast-following compresses vendor life cycles and margins; the balance depends on speed to market and category captaincy.

- Patent power: supplier leverage

- Retailer-exclusive: redirects margins

- OEB fast-follow: shortens vendor windows

- Key hinge: speed to market & category captain

Scale, centralized sourcing and £12.8bn sales boost supplier leverage

Kingfisher scale (c.1,200 stores in 10 countries; FY24 sales £12.8bn) and Own Exclusive Brands reduce supplier dependence. Centralized sourcing, DCs and VMI raise leverage; 96% sustainable timber (FY24) strengthens compliance-led bargaining. Strong branded suppliers (Bosch, Makita, Dulux) retain pricing power where patents/brand equity exist.

| Metric | 2024 |

|---|---|

| Stores (approx) | 1,200 |

| FY24 sales | £12.8bn |

| Sustainable timber | 96% |

What is included in the product

Concise Porter’s Five Forces analysis for Kingfisher, uncovering competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and strategic levers to protect margins.

One-sheet Kingfisher Porter’s Five Forces summary that instantly maps competitive pressure with a customizable spider chart—no macros, easy to edit for board decks or scenario comparisons.

Customers Bargaining Power

Price transparency and low switching

DIY and trade buyers can compare prices across banners and online in seconds, increasing price sensitivity for Kingfisher, which operates c.1,300 stores (2024). Low switching costs across most categories and frequent promotions anchor expectations and shorten purchase cycles. Price‑match policies blunt defection but compress margins and limit pricing power.

Trade customers’ volume clout

Trade customers like Screwfix’s trade accounts—Screwfix operating c.800+ outlets and serving ~2m trade customers in 2024—drive repeat bulk purchases and extract better margin and credit terms; delivery windows and jobsite logistics are clear levers of bargaining power. Losing a trade account can swing local volumes significantly; reliability and tailored service often beat small price concessions in retaining trade buyers.

Omnichannel expectations

Buyers demand real‑time inventory visibility, rapid click‑and‑collect and flexible returns, and Kingfisher’s digital push (digital sales around 25% of group sales in 2024) reflects that pressure. Service lapses prompt immediate switching to rivals or marketplaces—surveys show a single poor experience drives many DIY shoppers away. Strong app/site UX lowers perceived switching friction, while tight delivery SLAs and paid installation services can neutralize buyer power.

Product knowledge asymmetry

Complex install projects at Kingfisher create advice dependency enabling solution selling and basket expansion; in 2024 in‑store project consultations and calculators increased attach rates in multiple formats, while content and specialist staff raise customer stickiness even as online reviews and how‑to videos (used by a large majority of shoppers) narrow the knowledge gap. Transparent specs and curated bundles help preserve margin without resorting to pure price cuts.

- advice dependency

- solution selling

- stickiness via content

- reviews narrow gap

- transparent bundles preserve value

Sustainability and quality preferences

Customers increasingly value eco-credentials and durable products, shifting competition from lowest price to lifecycle value; in 2024 surveys ~68% of shoppers said sustainability influences purchase decisions, boosting demand for certified ranges and energy-saving solutions that can command 10-25% premiums in home improvement categories.

- Reduced bargaining via clear labels and guarantees

- Premiums for certified/energy-saving lines

- Lifecycle value over upfront price

Price-sensitive shoppers, low switching costs; digital sales ~25%

Customers wield high price sensitivity with low switching costs across c.1,300 Kingfisher stores (2024), while digital sales ~25% of group sales (2024) raise service expectations. Trade buyers (Screwfix c.800+ outlets; ~2m trade customers in 2024) extract better terms; sustainability now shapes choices (~68% influenced in 2024).

| Metric | 2024 value |

|---|---|

| Kingfisher stores | c.1,300 |

| Digital sales | ~25% group sales |

| Screwfix outlets | c.800+ |

| Trade customers | ~2m |

| Sustainability influence | ~68% |

Preview Before You Purchase

Kingfisher Porter's Five Forces Analysis

This Kingfisher Porter's Five Forces Analysis preview is the exact document you’ll receive after purchase—no placeholders, no mockups. It delivers a thorough assessment of competitive rivalry, supplier and buyer power, threats of substitutes, and entry barriers. The file is fully formatted, actionable, and ready to download the moment you buy.

Go Beyond the Preview—Access the Full Strategic Report

Kingfisher faces varied pressures—from concentrated suppliers and savvy buyers to digitization-driven substitutes and moderate entry barriers—shaping margins and expansion choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kingfisher’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scale leverage and OEB

Kingfisher’s pan‑European scale (presence in 10 countries and c.1,200 stores in 2024) plus Own Exclusive Brands like GoodHome and Erbauer reduce dependence on national brands and improve negotiating leverage. Private label penetration lets Kingfisher substitute branded SKUs, disciplining vendor pricing and protecting gross margins. Centralized sourcing and consolidated buys drive volume discounts, while sustaining OEB quality demands robust supplier development and QA processes.

Supplier fragmentation vs branded concentration

Building materials and fittings remain highly fragmented, limiting individual supplier leverage, while power tools and paint show strong brand concentration—Bosch, Makita, SBD and Dulux dominate category listings. Kingfisher (FY24 sales £12.8bn) uses range rationalization and dual‑sourcing plus exclusive ranges and long‑term agreements to balance brand pull with retailer control.

Logistics integration and vendor terms

In 2024 Kingfisher’s owned distribution centres, drop‑ship options and aligned replenishment broaden supplier switching and standardise contract terms, while vendors accept tighter trading margins for pan‑EU throughput; VMI and shared sales data secure faster lead times and higher fill rates, though persistent freight and commodity price volatility in 2024 continues to force periodic renegotiation.

Compliance and sustainability requirements

Compliance and sustainability requirements — ESG standards, timber legality and product stewardship — have narrowed Kingfisher’s approved supplier pool, raising compliance costs for vendors; Kingfisher reported 96% of timber from more sustainable sources in FY24, strengthening its leverage to set specs and audits. Suppliers with eco‑labels gain shelf access and volume, while smaller vendors face higher relative burden, reducing their bargaining power.

- ESG-driven supplier narrowing

- 96% sustainable timber (FY24)

- Eco-labels = shelf access/volume

- Higher relative costs for smaller vendors

Innovation and exclusivity dynamics

Suppliers with patent-backed innovation retain pricing power, but Kingfisher’s push for retailer-exclusive SKUs and co-development shifts margin leverage toward the channel; Kingfisher reported FY 2024 revenue ~£11.6bn, underscoring scale in negotiating supplier terms. OEB fast-following compresses vendor life cycles and margins; the balance depends on speed to market and category captaincy.

- Patent power: supplier leverage

- Retailer-exclusive: redirects margins

- OEB fast-follow: shortens vendor windows

- Key hinge: speed to market & category captain

Scale, centralized sourcing and £12.8bn sales boost supplier leverage

Kingfisher scale (c.1,200 stores in 10 countries; FY24 sales £12.8bn) and Own Exclusive Brands reduce supplier dependence. Centralized sourcing, DCs and VMI raise leverage; 96% sustainable timber (FY24) strengthens compliance-led bargaining. Strong branded suppliers (Bosch, Makita, Dulux) retain pricing power where patents/brand equity exist.

| Metric | 2024 |

|---|---|

| Stores (approx) | 1,200 |

| FY24 sales | £12.8bn |

| Sustainable timber | 96% |

What is included in the product

Concise Porter’s Five Forces analysis for Kingfisher, uncovering competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and strategic levers to protect margins.

One-sheet Kingfisher Porter’s Five Forces summary that instantly maps competitive pressure with a customizable spider chart—no macros, easy to edit for board decks or scenario comparisons.

Customers Bargaining Power

Price transparency and low switching

DIY and trade buyers can compare prices across banners and online in seconds, increasing price sensitivity for Kingfisher, which operates c.1,300 stores (2024). Low switching costs across most categories and frequent promotions anchor expectations and shorten purchase cycles. Price‑match policies blunt defection but compress margins and limit pricing power.

Trade customers’ volume clout

Trade customers like Screwfix’s trade accounts—Screwfix operating c.800+ outlets and serving ~2m trade customers in 2024—drive repeat bulk purchases and extract better margin and credit terms; delivery windows and jobsite logistics are clear levers of bargaining power. Losing a trade account can swing local volumes significantly; reliability and tailored service often beat small price concessions in retaining trade buyers.

Omnichannel expectations

Buyers demand real‑time inventory visibility, rapid click‑and‑collect and flexible returns, and Kingfisher’s digital push (digital sales around 25% of group sales in 2024) reflects that pressure. Service lapses prompt immediate switching to rivals or marketplaces—surveys show a single poor experience drives many DIY shoppers away. Strong app/site UX lowers perceived switching friction, while tight delivery SLAs and paid installation services can neutralize buyer power.

Product knowledge asymmetry

Complex install projects at Kingfisher create advice dependency enabling solution selling and basket expansion; in 2024 in‑store project consultations and calculators increased attach rates in multiple formats, while content and specialist staff raise customer stickiness even as online reviews and how‑to videos (used by a large majority of shoppers) narrow the knowledge gap. Transparent specs and curated bundles help preserve margin without resorting to pure price cuts.

- advice dependency

- solution selling

- stickiness via content

- reviews narrow gap

- transparent bundles preserve value

Sustainability and quality preferences

Customers increasingly value eco-credentials and durable products, shifting competition from lowest price to lifecycle value; in 2024 surveys ~68% of shoppers said sustainability influences purchase decisions, boosting demand for certified ranges and energy-saving solutions that can command 10-25% premiums in home improvement categories.

- Reduced bargaining via clear labels and guarantees

- Premiums for certified/energy-saving lines

- Lifecycle value over upfront price

Price-sensitive shoppers, low switching costs; digital sales ~25%

Customers wield high price sensitivity with low switching costs across c.1,300 Kingfisher stores (2024), while digital sales ~25% of group sales (2024) raise service expectations. Trade buyers (Screwfix c.800+ outlets; ~2m trade customers in 2024) extract better terms; sustainability now shapes choices (~68% influenced in 2024).

| Metric | 2024 value |

|---|---|

| Kingfisher stores | c.1,300 |

| Digital sales | ~25% group sales |

| Screwfix outlets | c.800+ |

| Trade customers | ~2m |

| Sustainability influence | ~68% |

Preview Before You Purchase

Kingfisher Porter's Five Forces Analysis

This Kingfisher Porter's Five Forces Analysis preview is the exact document you’ll receive after purchase—no placeholders, no mockups. It delivers a thorough assessment of competitive rivalry, supplier and buyer power, threats of substitutes, and entry barriers. The file is fully formatted, actionable, and ready to download the moment you buy.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Kingfisher faces varied pressures—from concentrated suppliers and savvy buyers to digitization-driven substitutes and moderate entry barriers—shaping margins and expansion choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kingfisher’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scale leverage and OEB

Kingfisher’s pan‑European scale (presence in 10 countries and c.1,200 stores in 2024) plus Own Exclusive Brands like GoodHome and Erbauer reduce dependence on national brands and improve negotiating leverage. Private label penetration lets Kingfisher substitute branded SKUs, disciplining vendor pricing and protecting gross margins. Centralized sourcing and consolidated buys drive volume discounts, while sustaining OEB quality demands robust supplier development and QA processes.

Supplier fragmentation vs branded concentration

Building materials and fittings remain highly fragmented, limiting individual supplier leverage, while power tools and paint show strong brand concentration—Bosch, Makita, SBD and Dulux dominate category listings. Kingfisher (FY24 sales £12.8bn) uses range rationalization and dual‑sourcing plus exclusive ranges and long‑term agreements to balance brand pull with retailer control.

Logistics integration and vendor terms

In 2024 Kingfisher’s owned distribution centres, drop‑ship options and aligned replenishment broaden supplier switching and standardise contract terms, while vendors accept tighter trading margins for pan‑EU throughput; VMI and shared sales data secure faster lead times and higher fill rates, though persistent freight and commodity price volatility in 2024 continues to force periodic renegotiation.

Compliance and sustainability requirements

Compliance and sustainability requirements — ESG standards, timber legality and product stewardship — have narrowed Kingfisher’s approved supplier pool, raising compliance costs for vendors; Kingfisher reported 96% of timber from more sustainable sources in FY24, strengthening its leverage to set specs and audits. Suppliers with eco‑labels gain shelf access and volume, while smaller vendors face higher relative burden, reducing their bargaining power.

- ESG-driven supplier narrowing

- 96% sustainable timber (FY24)

- Eco-labels = shelf access/volume

- Higher relative costs for smaller vendors

Innovation and exclusivity dynamics

Suppliers with patent-backed innovation retain pricing power, but Kingfisher’s push for retailer-exclusive SKUs and co-development shifts margin leverage toward the channel; Kingfisher reported FY 2024 revenue ~£11.6bn, underscoring scale in negotiating supplier terms. OEB fast-following compresses vendor life cycles and margins; the balance depends on speed to market and category captaincy.

- Patent power: supplier leverage

- Retailer-exclusive: redirects margins

- OEB fast-follow: shortens vendor windows

- Key hinge: speed to market & category captain

Scale, centralized sourcing and £12.8bn sales boost supplier leverage

Kingfisher scale (c.1,200 stores in 10 countries; FY24 sales £12.8bn) and Own Exclusive Brands reduce supplier dependence. Centralized sourcing, DCs and VMI raise leverage; 96% sustainable timber (FY24) strengthens compliance-led bargaining. Strong branded suppliers (Bosch, Makita, Dulux) retain pricing power where patents/brand equity exist.

| Metric | 2024 |

|---|---|

| Stores (approx) | 1,200 |

| FY24 sales | £12.8bn |

| Sustainable timber | 96% |

What is included in the product

Concise Porter’s Five Forces analysis for Kingfisher, uncovering competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and strategic levers to protect margins.

One-sheet Kingfisher Porter’s Five Forces summary that instantly maps competitive pressure with a customizable spider chart—no macros, easy to edit for board decks or scenario comparisons.

Customers Bargaining Power

Price transparency and low switching

DIY and trade buyers can compare prices across banners and online in seconds, increasing price sensitivity for Kingfisher, which operates c.1,300 stores (2024). Low switching costs across most categories and frequent promotions anchor expectations and shorten purchase cycles. Price‑match policies blunt defection but compress margins and limit pricing power.

Trade customers’ volume clout

Trade customers like Screwfix’s trade accounts—Screwfix operating c.800+ outlets and serving ~2m trade customers in 2024—drive repeat bulk purchases and extract better margin and credit terms; delivery windows and jobsite logistics are clear levers of bargaining power. Losing a trade account can swing local volumes significantly; reliability and tailored service often beat small price concessions in retaining trade buyers.

Omnichannel expectations

Buyers demand real‑time inventory visibility, rapid click‑and‑collect and flexible returns, and Kingfisher’s digital push (digital sales around 25% of group sales in 2024) reflects that pressure. Service lapses prompt immediate switching to rivals or marketplaces—surveys show a single poor experience drives many DIY shoppers away. Strong app/site UX lowers perceived switching friction, while tight delivery SLAs and paid installation services can neutralize buyer power.

Product knowledge asymmetry

Complex install projects at Kingfisher create advice dependency enabling solution selling and basket expansion; in 2024 in‑store project consultations and calculators increased attach rates in multiple formats, while content and specialist staff raise customer stickiness even as online reviews and how‑to videos (used by a large majority of shoppers) narrow the knowledge gap. Transparent specs and curated bundles help preserve margin without resorting to pure price cuts.

- advice dependency

- solution selling

- stickiness via content

- reviews narrow gap

- transparent bundles preserve value

Sustainability and quality preferences

Customers increasingly value eco-credentials and durable products, shifting competition from lowest price to lifecycle value; in 2024 surveys ~68% of shoppers said sustainability influences purchase decisions, boosting demand for certified ranges and energy-saving solutions that can command 10-25% premiums in home improvement categories.

- Reduced bargaining via clear labels and guarantees

- Premiums for certified/energy-saving lines

- Lifecycle value over upfront price

Price-sensitive shoppers, low switching costs; digital sales ~25%

Customers wield high price sensitivity with low switching costs across c.1,300 Kingfisher stores (2024), while digital sales ~25% of group sales (2024) raise service expectations. Trade buyers (Screwfix c.800+ outlets; ~2m trade customers in 2024) extract better terms; sustainability now shapes choices (~68% influenced in 2024).

| Metric | 2024 value |

|---|---|

| Kingfisher stores | c.1,300 |

| Digital sales | ~25% group sales |

| Screwfix outlets | c.800+ |

| Trade customers | ~2m |

| Sustainability influence | ~68% |

Preview Before You Purchase

Kingfisher Porter's Five Forces Analysis

This Kingfisher Porter's Five Forces Analysis preview is the exact document you’ll receive after purchase—no placeholders, no mockups. It delivers a thorough assessment of competitive rivalry, supplier and buyer power, threats of substitutes, and entry barriers. The file is fully formatted, actionable, and ready to download the moment you buy.