Kingsway Financial Services Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Kingsway Financial Services faces moderate buyer power, concentrated supplier channels, and evolving substitute threats that shape its margins and growth outlook. This snapshot highlights key competitive pressures and strategic levers. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to Kingsway’s market position.

Suppliers Bargaining Power

Concentrated reinsurance partners

Concentrated reinsurance partners give reinsurers outsized leverage; in 2024 the top five global reinsurers supplied roughly 50% of market capacity, allowing them to set pricing, collateral demands and exclusions, especially in niche, high-volatility lines. Tight capacity and mid-teens to low‑twenties percent rate increases in many specialty renewals elevated Kingsway’s cost of risk transfer and constrained flexibility. Renewal cycles therefore amplify earnings volatility, while long-standing relationships and multi-year treaties partially mitigate but do not eliminate reinsurer bargaining power.

Dependence on data, telematics, and credit bureaus

Accurate pricing for non-standard auto and warranties depends heavily on third-party data, telematics and the three major credit bureaus (Equifax, Experian, TransUnion) in 2024. Proprietary scoring models, custom API integrations and switching costs give these suppliers significant leverage. Sudden price hikes or access limits can materially reduce underwriting precision and margins. Ongoing vendor consolidation further amplifies supplier bargaining power.

Claims supply chain and repair networks

Auto body shops, parts suppliers and service centers drive indemnity and loss-adjustment expenses; parts inflation (~8% in 2024) and tight labor markets (technician vacancy rates near 7–9%) pushed repair severity higher, raising carrier costs. Preferred networks lower pricing dispersion but cannot remove dependence on local capacity. Warranty fulfillment partners likewise directly impact cost-of-goods sold for service contracts.

Technology platforms and administrators

Technology platforms and administrators—policy admin systems, TPAs, and warranty administrators—are critical to Kingsway Financial Services operations, with 2024 industry surveys showing 56% of insurers prioritizing admin modernization; heavy custom configurations create strong lock-in and slow migration to alternatives. Per-policy fees and frequent change-order charges create ongoing cost pressure, and outages or underperformance directly harm service levels and customer satisfaction.

- Critical suppliers: policy admin vendors, TPAs, warranty admin

- Lock-in: custom configs slow switching

- Cost drivers: per-policy fees, change orders

- Risk: outages → direct service and satisfaction impact

Capital providers and rating agencies

Equity, debt and fronting providers set covenants, pricing and collateral requirements that directly constrain Kingsway’s strategic flexibility; in 2024 rising reinsurance and fronting costs (reinsurance pricing up ~15% year-over-year) and wider IG spreads (~50 bps) increased funding costs. Rating agencies act as suppliers of credibility, shaping distribution access and reinsurance terms; downgrades or tighter capital markets raise Kingsway’s costs and elevate supplier power in stressed cycles.

Top 5 reinsurers ≈50%; pricing +15%, parts +8%

Concentrated reinsurers (top 5 ≈50% capacity in 2024) plus ~+15% reinsurance pricing raised Kingsway’s transfer costs and limited flexibility. Third-party data vendors and admin platforms (56% insurers prioritizing modernization in 2024) create strong lock-in and switching costs. Parts inflation (~8% in 2024) and technician vacancies (7–9%) increased loss severity and LAE.

| Supplier | 2024 metric |

|---|---|

| Top reinsurers | Top 5 ≈50% capacity |

| Reinsurance pricing | +15% YoY |

| Admin modernization | 56% insurers |

| Parts inflation | ~8% |

| Technician vacancy | 7–9% |

What is included in the product

Tailored Porter’s Five Forces analysis for Kingsway Financial Services that uncovers key drivers of competition, buyer/supplier power, substitutes and disruptive threats, and assesses market entry barriers and profitability impact.

A clear, one-sheet summary of Kingsway Financial Services' five forces—enabling rapid assessment of competitive pressures and fast, board-ready strategic decisions.

Customers Bargaining Power

Price-sensitive non-standard auto policyholders

Price-sensitive non-standard auto policyholders shop frequently and churn—industry data show ~30% annual churn in non-standard books in 2024—pressuring rates and fees. Aggregators and digital quote tools, used by roughly 52% of shoppers in 2024, increase transparency. Limited disposable income amplifies elasticity, forcing carriers to balance competitive pricing with strict risk selection to avoid adverse selection.

Auto dealers as extended-warranty channels

Dealers control point-of-sale access for Kingsway service contracts and commonly demand 20–35% F&I commissions; they can switch administrators if economics or claims experience worsen. In 2024 large dealer groups (top 5–10) concentrate roughly 15–25% of retail volume, giving outsized leverage. Co-marketing and white-label arrangements partly align incentives but do not eliminate dealer bargaining power.

Commercial clients in business services

Commercial clients evaluate providers primarily on cost, turnaround time, and compliance; in 2024, 58% of enterprises used formal RFPs and SLA clauses to drive terms, boosting buyer leverage. Contractual SLAs and standardized RFP processes raise bargaining power by creating measurable performance levers and exit triggers. Widespread multi-sourcing—used by roughly half of firms—lowers switching barriers, while clear ROI and analytics can soften price pressure by shifting negotiations toward value-based fees.

Regulated coverage minimums but flexible carriers

State-mandated minimums sustain baseline demand for Kingsway products, but abundant carriers and program options give buyers leverage; monthly billing and statutory cancellation rights make switching simpler, while discounts and endorsements are common negotiation levers, and service quality plus claims handling remain key retention drivers.

- Regulatory baseline demand

- High carrier/program choice

- Monthly billing eases switching

- Discounts/endorsements as leverage

- Claims/service drive retention

Reputation and claims outcomes drive leverage

Reputation and claims outcomes drive leverage: negative claims experiences accelerate shopping and increase churn, with a 2024 Accenture survey reporting 67% of policyholders say claims handling is their top retention factor; social reviews and complaint ratios increasingly inform buyer choices, while faster, fairer settlements reduce perceived need to bargain and poor service amplifies buyer power immediately.

- 67% 2024 Accenture: claims handling = top retention factor

- Higher complaint ratios correlate with immediate quote-shopping

- Faster settlements lower bargaining leverage

High churn and aggregators (30%, 52%) squeeze margins; dealer F&I (20-35%) and claims (67%)

Customers wield strong bargaining power: retail non-standard churn ~30% (2024) and 52% use aggregators, forcing price pressure and tight risk selection. Dealers demand 20–35% F&I and top groups control 15–25% volume, raising switching risk. Commercial buyers use RFPs/SLA (58%) and claims handling drives retention (67% cite claims as top factor).

| Metric | 2024 Value |

|---|---|

| Non-standard churn | ~30% |

| Aggregator use | 52% |

| Dealer F&I commission | 20–35% |

| Top dealer group share | 15–25% |

| Enterprises using RFPs/SLA | 58% |

| Claims = top retention factor | 67% |

What You See Is What You Get

Kingsway Financial Services Porter's Five Forces Analysis

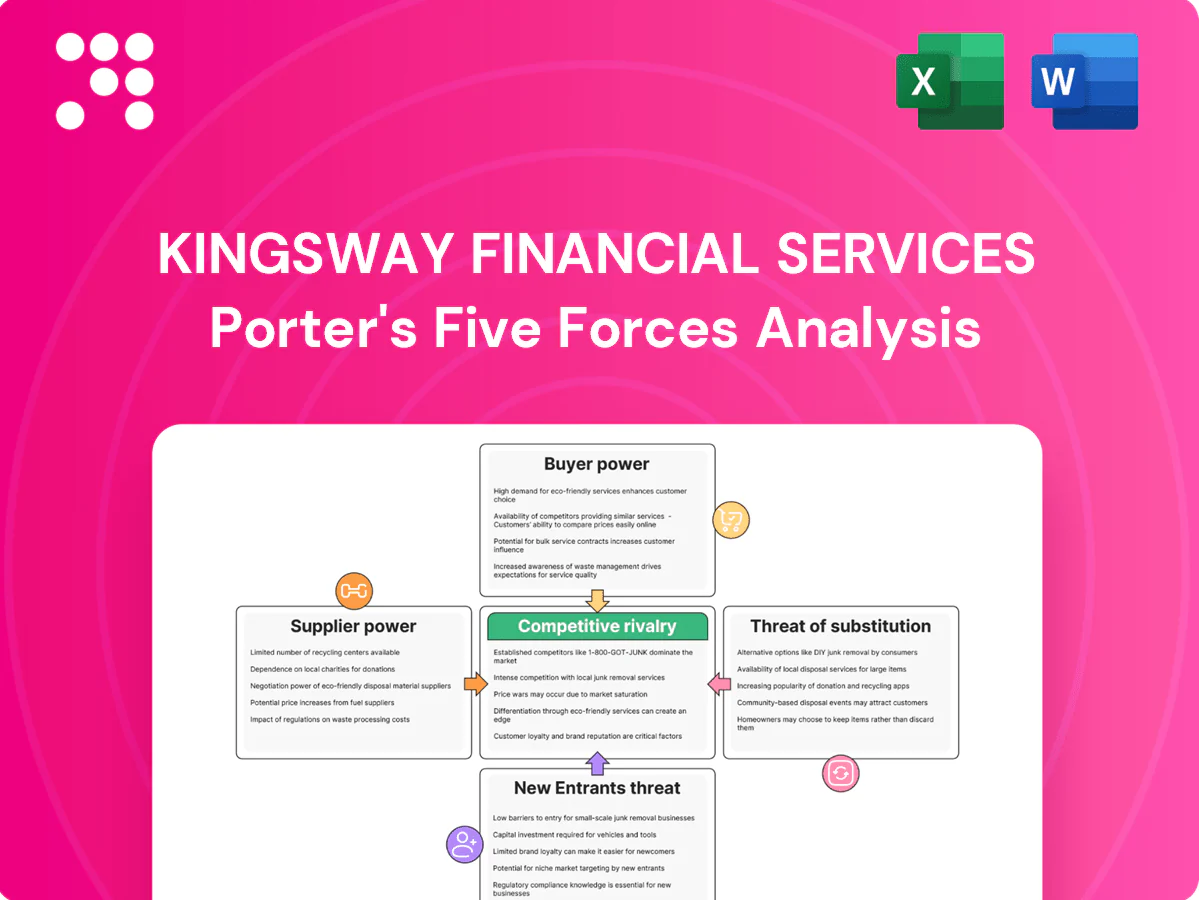

This preview shows the exact Porter's Five Forces analysis of Kingsway Financial Services you'll receive immediately after purchase—no placeholders. It assesses competitive rivalry, supplier and buyer power, and threats of entry and substitutes with actionable insights. The document is fully formatted and ready for instant download and use.

Don't Miss the Bigger Picture

Kingsway Financial Services faces moderate buyer power, concentrated supplier channels, and evolving substitute threats that shape its margins and growth outlook. This snapshot highlights key competitive pressures and strategic levers. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to Kingsway’s market position.

Suppliers Bargaining Power

Concentrated reinsurance partners

Concentrated reinsurance partners give reinsurers outsized leverage; in 2024 the top five global reinsurers supplied roughly 50% of market capacity, allowing them to set pricing, collateral demands and exclusions, especially in niche, high-volatility lines. Tight capacity and mid-teens to low‑twenties percent rate increases in many specialty renewals elevated Kingsway’s cost of risk transfer and constrained flexibility. Renewal cycles therefore amplify earnings volatility, while long-standing relationships and multi-year treaties partially mitigate but do not eliminate reinsurer bargaining power.

Dependence on data, telematics, and credit bureaus

Accurate pricing for non-standard auto and warranties depends heavily on third-party data, telematics and the three major credit bureaus (Equifax, Experian, TransUnion) in 2024. Proprietary scoring models, custom API integrations and switching costs give these suppliers significant leverage. Sudden price hikes or access limits can materially reduce underwriting precision and margins. Ongoing vendor consolidation further amplifies supplier bargaining power.

Claims supply chain and repair networks

Auto body shops, parts suppliers and service centers drive indemnity and loss-adjustment expenses; parts inflation (~8% in 2024) and tight labor markets (technician vacancy rates near 7–9%) pushed repair severity higher, raising carrier costs. Preferred networks lower pricing dispersion but cannot remove dependence on local capacity. Warranty fulfillment partners likewise directly impact cost-of-goods sold for service contracts.

Technology platforms and administrators

Technology platforms and administrators—policy admin systems, TPAs, and warranty administrators—are critical to Kingsway Financial Services operations, with 2024 industry surveys showing 56% of insurers prioritizing admin modernization; heavy custom configurations create strong lock-in and slow migration to alternatives. Per-policy fees and frequent change-order charges create ongoing cost pressure, and outages or underperformance directly harm service levels and customer satisfaction.

- Critical suppliers: policy admin vendors, TPAs, warranty admin

- Lock-in: custom configs slow switching

- Cost drivers: per-policy fees, change orders

- Risk: outages → direct service and satisfaction impact

Capital providers and rating agencies

Equity, debt and fronting providers set covenants, pricing and collateral requirements that directly constrain Kingsway’s strategic flexibility; in 2024 rising reinsurance and fronting costs (reinsurance pricing up ~15% year-over-year) and wider IG spreads (~50 bps) increased funding costs. Rating agencies act as suppliers of credibility, shaping distribution access and reinsurance terms; downgrades or tighter capital markets raise Kingsway’s costs and elevate supplier power in stressed cycles.

Top 5 reinsurers ≈50%; pricing +15%, parts +8%

Concentrated reinsurers (top 5 ≈50% capacity in 2024) plus ~+15% reinsurance pricing raised Kingsway’s transfer costs and limited flexibility. Third-party data vendors and admin platforms (56% insurers prioritizing modernization in 2024) create strong lock-in and switching costs. Parts inflation (~8% in 2024) and technician vacancies (7–9%) increased loss severity and LAE.

| Supplier | 2024 metric |

|---|---|

| Top reinsurers | Top 5 ≈50% capacity |

| Reinsurance pricing | +15% YoY |

| Admin modernization | 56% insurers |

| Parts inflation | ~8% |

| Technician vacancy | 7–9% |

What is included in the product

Tailored Porter’s Five Forces analysis for Kingsway Financial Services that uncovers key drivers of competition, buyer/supplier power, substitutes and disruptive threats, and assesses market entry barriers and profitability impact.

A clear, one-sheet summary of Kingsway Financial Services' five forces—enabling rapid assessment of competitive pressures and fast, board-ready strategic decisions.

Customers Bargaining Power

Price-sensitive non-standard auto policyholders

Price-sensitive non-standard auto policyholders shop frequently and churn—industry data show ~30% annual churn in non-standard books in 2024—pressuring rates and fees. Aggregators and digital quote tools, used by roughly 52% of shoppers in 2024, increase transparency. Limited disposable income amplifies elasticity, forcing carriers to balance competitive pricing with strict risk selection to avoid adverse selection.

Auto dealers as extended-warranty channels

Dealers control point-of-sale access for Kingsway service contracts and commonly demand 20–35% F&I commissions; they can switch administrators if economics or claims experience worsen. In 2024 large dealer groups (top 5–10) concentrate roughly 15–25% of retail volume, giving outsized leverage. Co-marketing and white-label arrangements partly align incentives but do not eliminate dealer bargaining power.

Commercial clients in business services

Commercial clients evaluate providers primarily on cost, turnaround time, and compliance; in 2024, 58% of enterprises used formal RFPs and SLA clauses to drive terms, boosting buyer leverage. Contractual SLAs and standardized RFP processes raise bargaining power by creating measurable performance levers and exit triggers. Widespread multi-sourcing—used by roughly half of firms—lowers switching barriers, while clear ROI and analytics can soften price pressure by shifting negotiations toward value-based fees.

Regulated coverage minimums but flexible carriers

State-mandated minimums sustain baseline demand for Kingsway products, but abundant carriers and program options give buyers leverage; monthly billing and statutory cancellation rights make switching simpler, while discounts and endorsements are common negotiation levers, and service quality plus claims handling remain key retention drivers.

- Regulatory baseline demand

- High carrier/program choice

- Monthly billing eases switching

- Discounts/endorsements as leverage

- Claims/service drive retention

Reputation and claims outcomes drive leverage

Reputation and claims outcomes drive leverage: negative claims experiences accelerate shopping and increase churn, with a 2024 Accenture survey reporting 67% of policyholders say claims handling is their top retention factor; social reviews and complaint ratios increasingly inform buyer choices, while faster, fairer settlements reduce perceived need to bargain and poor service amplifies buyer power immediately.

- 67% 2024 Accenture: claims handling = top retention factor

- Higher complaint ratios correlate with immediate quote-shopping

- Faster settlements lower bargaining leverage

High churn and aggregators (30%, 52%) squeeze margins; dealer F&I (20-35%) and claims (67%)

Customers wield strong bargaining power: retail non-standard churn ~30% (2024) and 52% use aggregators, forcing price pressure and tight risk selection. Dealers demand 20–35% F&I and top groups control 15–25% volume, raising switching risk. Commercial buyers use RFPs/SLA (58%) and claims handling drives retention (67% cite claims as top factor).

| Metric | 2024 Value |

|---|---|

| Non-standard churn | ~30% |

| Aggregator use | 52% |

| Dealer F&I commission | 20–35% |

| Top dealer group share | 15–25% |

| Enterprises using RFPs/SLA | 58% |

| Claims = top retention factor | 67% |

What You See Is What You Get

Kingsway Financial Services Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Kingsway Financial Services you'll receive immediately after purchase—no placeholders. It assesses competitive rivalry, supplier and buyer power, and threats of entry and substitutes with actionable insights. The document is fully formatted and ready for instant download and use.

Description

Don't Miss the Bigger Picture

Kingsway Financial Services faces moderate buyer power, concentrated supplier channels, and evolving substitute threats that shape its margins and growth outlook. This snapshot highlights key competitive pressures and strategic levers. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to Kingsway’s market position.

Suppliers Bargaining Power

Concentrated reinsurance partners

Concentrated reinsurance partners give reinsurers outsized leverage; in 2024 the top five global reinsurers supplied roughly 50% of market capacity, allowing them to set pricing, collateral demands and exclusions, especially in niche, high-volatility lines. Tight capacity and mid-teens to low‑twenties percent rate increases in many specialty renewals elevated Kingsway’s cost of risk transfer and constrained flexibility. Renewal cycles therefore amplify earnings volatility, while long-standing relationships and multi-year treaties partially mitigate but do not eliminate reinsurer bargaining power.

Dependence on data, telematics, and credit bureaus

Accurate pricing for non-standard auto and warranties depends heavily on third-party data, telematics and the three major credit bureaus (Equifax, Experian, TransUnion) in 2024. Proprietary scoring models, custom API integrations and switching costs give these suppliers significant leverage. Sudden price hikes or access limits can materially reduce underwriting precision and margins. Ongoing vendor consolidation further amplifies supplier bargaining power.

Claims supply chain and repair networks

Auto body shops, parts suppliers and service centers drive indemnity and loss-adjustment expenses; parts inflation (~8% in 2024) and tight labor markets (technician vacancy rates near 7–9%) pushed repair severity higher, raising carrier costs. Preferred networks lower pricing dispersion but cannot remove dependence on local capacity. Warranty fulfillment partners likewise directly impact cost-of-goods sold for service contracts.

Technology platforms and administrators

Technology platforms and administrators—policy admin systems, TPAs, and warranty administrators—are critical to Kingsway Financial Services operations, with 2024 industry surveys showing 56% of insurers prioritizing admin modernization; heavy custom configurations create strong lock-in and slow migration to alternatives. Per-policy fees and frequent change-order charges create ongoing cost pressure, and outages or underperformance directly harm service levels and customer satisfaction.

- Critical suppliers: policy admin vendors, TPAs, warranty admin

- Lock-in: custom configs slow switching

- Cost drivers: per-policy fees, change orders

- Risk: outages → direct service and satisfaction impact

Capital providers and rating agencies

Equity, debt and fronting providers set covenants, pricing and collateral requirements that directly constrain Kingsway’s strategic flexibility; in 2024 rising reinsurance and fronting costs (reinsurance pricing up ~15% year-over-year) and wider IG spreads (~50 bps) increased funding costs. Rating agencies act as suppliers of credibility, shaping distribution access and reinsurance terms; downgrades or tighter capital markets raise Kingsway’s costs and elevate supplier power in stressed cycles.

Top 5 reinsurers ≈50%; pricing +15%, parts +8%

Concentrated reinsurers (top 5 ≈50% capacity in 2024) plus ~+15% reinsurance pricing raised Kingsway’s transfer costs and limited flexibility. Third-party data vendors and admin platforms (56% insurers prioritizing modernization in 2024) create strong lock-in and switching costs. Parts inflation (~8% in 2024) and technician vacancies (7–9%) increased loss severity and LAE.

| Supplier | 2024 metric |

|---|---|

| Top reinsurers | Top 5 ≈50% capacity |

| Reinsurance pricing | +15% YoY |

| Admin modernization | 56% insurers |

| Parts inflation | ~8% |

| Technician vacancy | 7–9% |

What is included in the product

Tailored Porter’s Five Forces analysis for Kingsway Financial Services that uncovers key drivers of competition, buyer/supplier power, substitutes and disruptive threats, and assesses market entry barriers and profitability impact.

A clear, one-sheet summary of Kingsway Financial Services' five forces—enabling rapid assessment of competitive pressures and fast, board-ready strategic decisions.

Customers Bargaining Power

Price-sensitive non-standard auto policyholders

Price-sensitive non-standard auto policyholders shop frequently and churn—industry data show ~30% annual churn in non-standard books in 2024—pressuring rates and fees. Aggregators and digital quote tools, used by roughly 52% of shoppers in 2024, increase transparency. Limited disposable income amplifies elasticity, forcing carriers to balance competitive pricing with strict risk selection to avoid adverse selection.

Auto dealers as extended-warranty channels

Dealers control point-of-sale access for Kingsway service contracts and commonly demand 20–35% F&I commissions; they can switch administrators if economics or claims experience worsen. In 2024 large dealer groups (top 5–10) concentrate roughly 15–25% of retail volume, giving outsized leverage. Co-marketing and white-label arrangements partly align incentives but do not eliminate dealer bargaining power.

Commercial clients in business services

Commercial clients evaluate providers primarily on cost, turnaround time, and compliance; in 2024, 58% of enterprises used formal RFPs and SLA clauses to drive terms, boosting buyer leverage. Contractual SLAs and standardized RFP processes raise bargaining power by creating measurable performance levers and exit triggers. Widespread multi-sourcing—used by roughly half of firms—lowers switching barriers, while clear ROI and analytics can soften price pressure by shifting negotiations toward value-based fees.

Regulated coverage minimums but flexible carriers

State-mandated minimums sustain baseline demand for Kingsway products, but abundant carriers and program options give buyers leverage; monthly billing and statutory cancellation rights make switching simpler, while discounts and endorsements are common negotiation levers, and service quality plus claims handling remain key retention drivers.

- Regulatory baseline demand

- High carrier/program choice

- Monthly billing eases switching

- Discounts/endorsements as leverage

- Claims/service drive retention

Reputation and claims outcomes drive leverage

Reputation and claims outcomes drive leverage: negative claims experiences accelerate shopping and increase churn, with a 2024 Accenture survey reporting 67% of policyholders say claims handling is their top retention factor; social reviews and complaint ratios increasingly inform buyer choices, while faster, fairer settlements reduce perceived need to bargain and poor service amplifies buyer power immediately.

- 67% 2024 Accenture: claims handling = top retention factor

- Higher complaint ratios correlate with immediate quote-shopping

- Faster settlements lower bargaining leverage

High churn and aggregators (30%, 52%) squeeze margins; dealer F&I (20-35%) and claims (67%)

Customers wield strong bargaining power: retail non-standard churn ~30% (2024) and 52% use aggregators, forcing price pressure and tight risk selection. Dealers demand 20–35% F&I and top groups control 15–25% volume, raising switching risk. Commercial buyers use RFPs/SLA (58%) and claims handling drives retention (67% cite claims as top factor).

| Metric | 2024 Value |

|---|---|

| Non-standard churn | ~30% |

| Aggregator use | 52% |

| Dealer F&I commission | 20–35% |

| Top dealer group share | 15–25% |

| Enterprises using RFPs/SLA | 58% |

| Claims = top retention factor | 67% |

What You See Is What You Get

Kingsway Financial Services Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Kingsway Financial Services you'll receive immediately after purchase—no placeholders. It assesses competitive rivalry, supplier and buyer power, and threats of entry and substitutes with actionable insights. The document is fully formatted and ready for instant download and use.