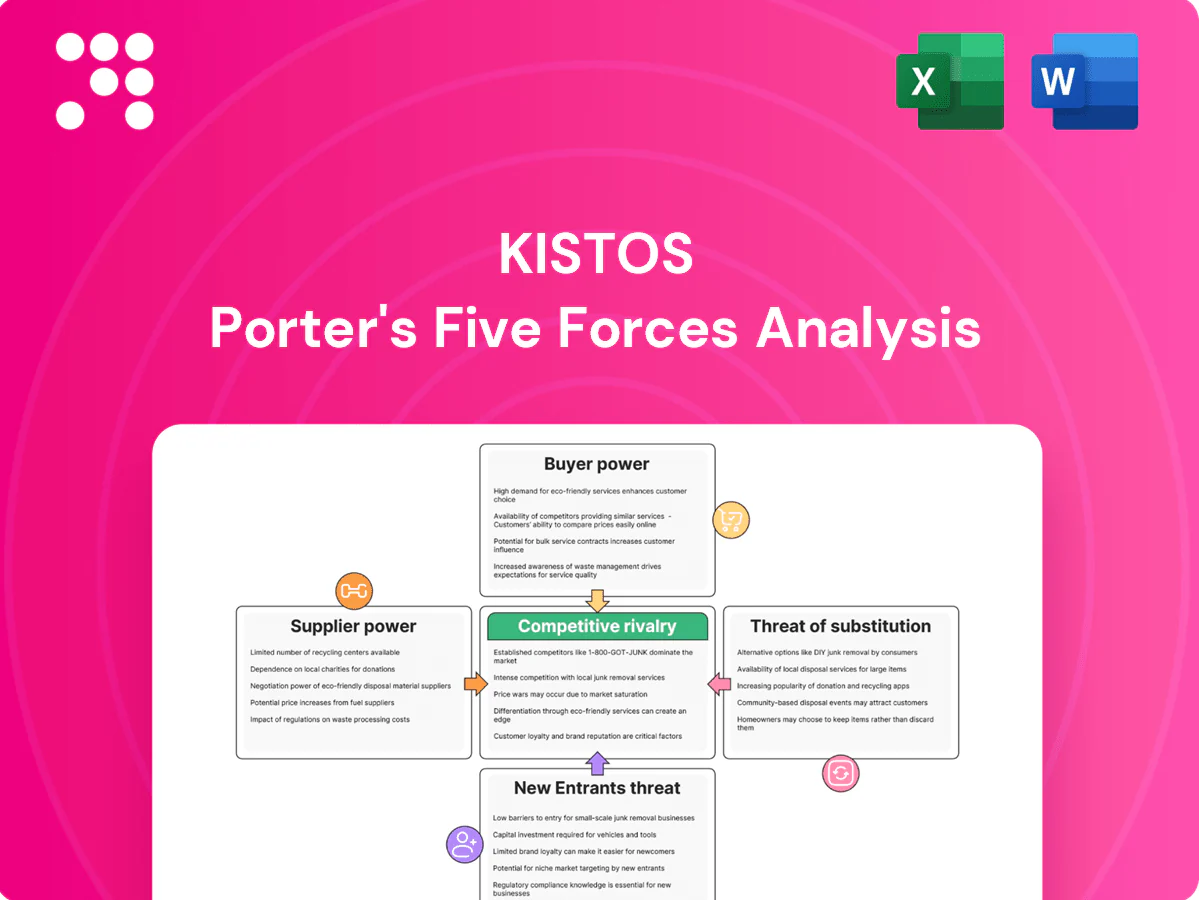

Kistos Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Kistos faces moderated supplier power and evolving buyer bargaining amid energy transition, while new entrants and substitutes pose emerging threats; competitive rivalry hinges on scale and project pipeline. This snapshot only scratches the surface — unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategic insights.

Suppliers Bargaining Power

Specialized OFS dependence

Upstream operations depend on a concentrated set of oilfield service firms and OEMs for drilling, subsea and compression, giving suppliers strong leverage over day rates and critical equipment availability. Limited qualified vendors in the North Sea can push input costs higher and create premium pricing during capacity tightness. Kistos mitigates this via multi-year frame agreements and equipment standardization to lock rates and improve sourcing flexibility. Schedule risk persists if key suppliers face bottlenecks or fleet constraints.

Rig and vessel scarcity

Harsh‑environment rigs and intervention vessels are highly cyclical and capacity‑constrained; North Sea rig utilization exceeded 85% in 2024, tightening supply and lifting dayrates by roughly 40% year‑on‑year. Forward booking and flexible scopes mitigate risk, but small operators lack scale to secure prime slots. Limited weather windows further amplify supplier leverage.

Infrastructure access fees

Processing plants and pipelines are often third‑party owned with tariff structures, and access negotiations plus tie‑in timing give midstream owners bargaining power, especially where few alternatives exist.

Regulatory third‑party access frameworks (EU/UK TPA regimes, updated post‑2019) can limit excess pricing but do not secure scheduling or priority for tie‑ins.

Kistos’ brownfield tie‑backs can still face take‑or‑pay exposure and commercial sequencing risks when capacity is constrained.

Low‑carbon tech providers

Specialized electrification, leak‑detection and emissions‑abatement technologies give suppliers moderate bargaining power as vendor pools and certification schemes remain concentrated; adoption supports Kistos’ lower‑carbon positioning and access to 2024 incentives (eg investment tax credits). Limited competition can raise prices, while co‑development deals trade margin for speed, credibility and faster deployment.

- Concentrated vendors → higher pricing pressure

- Adoption unlocks incentives and market differentiation

- Co‑development: margin sacrifice for speed/credibility

Skilled labor tightness

- Skilled scarcity: 2024 industry reports indicate tight labor pools

- Cost pressure: rising wages and retention premiums

- Constraint: training/local content reduce flexibility

- Mitigation: collaborative HSE and predictable campaigns lower talent costs

Supply squeeze: rigs >85% util, dayrates +~40% YoY

Suppliers hold elevated leverage: North Sea rig utilization >85% in 2024 and dayrates rose ~40% YoY, tightening access and lifting input costs. Concentrated OEMs, midstream tolling and scarce skilled crews amplify pricing and scheduling risk; Kistos uses multi‑year frames and standardisation to lock rates and improve flexibility. Electrification vendors remain concentrated but unlock 2024 incentives and differentiation.

| Metric | 2024 |

|---|---|

| Rig utilization | >85% |

| Dayrate change | +~40% YoY |

| Skilled labour | Reported tight pools (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Kistos, uncovering competitive intensity, supplier and buyer power, entry barriers, and substitute threats to its offshore energy services position. Detailed, strategic insights identify disruptive forces, pricing pressures, and protective dynamics to inform investor presentations and internal strategy.

A one-sheet Porter's Five Forces for Kistos that quantifies competitive pressure, lets you tweak inputs for scenarios, and exports clean visuals for decks—removing analysis bottlenecks and speeding strategic decisions.

Customers Bargaining Power

Commodity price‑takers

Natural gas is a standardized commodity so utilities, traders and industrials can switch sources readily, leaving Kistos as a price-taker; TTF and NBP remained the anchoring hubs in 2024. Buyers exert power via short‑term contracts and volume optionality, compressing Kistos’ ability to add premiums. Transparent hub pricing (TTF/NBP) limits realised spreads, though hedging and structured offtake in 2024 partially stabilized revenues.

Portfolio buyers with scale

Portfolio buyers such as large utilities and commodity traders aggregate demand across regions and use their scale to press for stricter quality specs, tighter balancing and tougher credit terms. Kistos’ negotiating leverage rises with consistent, flexible delivery and demonstrated operational reliability. Dealing with investment-grade counterparties (S&P BBB- or higher) lowers receivable risk but typically compresses realized margins. Concentrated buyer power therefore squeezes pricing flexibility for sellers.

Security‑of‑supply trade‑off

In tight 2024 markets buyers prioritized reliability over price, weakening their bargaining leverage and enabling suppliers like Kistos to command longer tenors; domestic lower‑emission production increasingly gained preferred status. Kistos’ operational efficiency and improving ESG metrics support contract length and price resilience, but as markets loosen buyer power can re‑intensify rapidly.

Regulatory pass‑through

Regulatory pass‑through: price caps and consumer protections in 2024 squeezed downstream margins, driving buyers to press upstream for concessions when regulated returns narrowed; Kistos mitigates this via indexed contracts linked to Brent and TTF hubs, reducing exposure to unilateral adjustments; political interventions can still shift negotiating leverage suddenly.

- 2024: increased buyer push when regulated returns fell

- Indexed contracts: Brent and TTF linkage

- Political risk: sudden shifts in negotiating dynamics

Balancing and flexibility fees

Balancing and flexibility fees erode Kistos netbacks as imbalance penalties and paid flexibility services shift value away from producers; in 2024 market reports showed elevated balancing costs during tight winter months. Sophisticated buyers leverage strict delivery windows to push costs upstream, increasing short-term cashflow variability. Investing in storage, swing capacity and improved forecasting in 2024 materially reduced buyer leverage and captured pricing premiums at peak demand.

- Imbalance penalties reduce realized netbacks

- Buyers use strict windows to transfer costs upstream

- Storage and swing lower customer bargaining power

- Operational flexibility earns premiums in peak periods

TTF/NBP anchoring keeps buyers powerful; reliability and storage enable longer-tenor premiums

Buyers hold strong leverage as gas is a standardized commodity with TTF and NBP anchoring 2024 pricing, enabling easy switching and limiting Kistos to hub-driven spreads. Large utilities and traders compress premiums via volume/credit terms while reliability and ESG gains let Kistos capture longer tenors in tight periods. Indexed contracts and balancing fees shifted margin pressure upstream but storage/swing reduced buyer power.

| Metric | 2024 Impact |

|---|---|

| Hub anchoring | TTF/NBP govern pricing |

| Contracting | Indexed to Brent/TTF |

| Flexibility | Storage/swing lowers buyer leverage |

Preview Before You Purchase

Kistos Porter's Five Forces Analysis

This preview displays the exact Kistos Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, ready for download and use the moment you buy. What you see here is the final, complete deliverable.

A Must-Have Tool for Decision-Makers

Kistos faces moderated supplier power and evolving buyer bargaining amid energy transition, while new entrants and substitutes pose emerging threats; competitive rivalry hinges on scale and project pipeline. This snapshot only scratches the surface — unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategic insights.

Suppliers Bargaining Power

Specialized OFS dependence

Upstream operations depend on a concentrated set of oilfield service firms and OEMs for drilling, subsea and compression, giving suppliers strong leverage over day rates and critical equipment availability. Limited qualified vendors in the North Sea can push input costs higher and create premium pricing during capacity tightness. Kistos mitigates this via multi-year frame agreements and equipment standardization to lock rates and improve sourcing flexibility. Schedule risk persists if key suppliers face bottlenecks or fleet constraints.

Rig and vessel scarcity

Harsh‑environment rigs and intervention vessels are highly cyclical and capacity‑constrained; North Sea rig utilization exceeded 85% in 2024, tightening supply and lifting dayrates by roughly 40% year‑on‑year. Forward booking and flexible scopes mitigate risk, but small operators lack scale to secure prime slots. Limited weather windows further amplify supplier leverage.

Infrastructure access fees

Processing plants and pipelines are often third‑party owned with tariff structures, and access negotiations plus tie‑in timing give midstream owners bargaining power, especially where few alternatives exist.

Regulatory third‑party access frameworks (EU/UK TPA regimes, updated post‑2019) can limit excess pricing but do not secure scheduling or priority for tie‑ins.

Kistos’ brownfield tie‑backs can still face take‑or‑pay exposure and commercial sequencing risks when capacity is constrained.

Low‑carbon tech providers

Specialized electrification, leak‑detection and emissions‑abatement technologies give suppliers moderate bargaining power as vendor pools and certification schemes remain concentrated; adoption supports Kistos’ lower‑carbon positioning and access to 2024 incentives (eg investment tax credits). Limited competition can raise prices, while co‑development deals trade margin for speed, credibility and faster deployment.

- Concentrated vendors → higher pricing pressure

- Adoption unlocks incentives and market differentiation

- Co‑development: margin sacrifice for speed/credibility

Skilled labor tightness

- Skilled scarcity: 2024 industry reports indicate tight labor pools

- Cost pressure: rising wages and retention premiums

- Constraint: training/local content reduce flexibility

- Mitigation: collaborative HSE and predictable campaigns lower talent costs

Supply squeeze: rigs >85% util, dayrates +~40% YoY

Suppliers hold elevated leverage: North Sea rig utilization >85% in 2024 and dayrates rose ~40% YoY, tightening access and lifting input costs. Concentrated OEMs, midstream tolling and scarce skilled crews amplify pricing and scheduling risk; Kistos uses multi‑year frames and standardisation to lock rates and improve flexibility. Electrification vendors remain concentrated but unlock 2024 incentives and differentiation.

| Metric | 2024 |

|---|---|

| Rig utilization | >85% |

| Dayrate change | +~40% YoY |

| Skilled labour | Reported tight pools (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Kistos, uncovering competitive intensity, supplier and buyer power, entry barriers, and substitute threats to its offshore energy services position. Detailed, strategic insights identify disruptive forces, pricing pressures, and protective dynamics to inform investor presentations and internal strategy.

A one-sheet Porter's Five Forces for Kistos that quantifies competitive pressure, lets you tweak inputs for scenarios, and exports clean visuals for decks—removing analysis bottlenecks and speeding strategic decisions.

Customers Bargaining Power

Commodity price‑takers

Natural gas is a standardized commodity so utilities, traders and industrials can switch sources readily, leaving Kistos as a price-taker; TTF and NBP remained the anchoring hubs in 2024. Buyers exert power via short‑term contracts and volume optionality, compressing Kistos’ ability to add premiums. Transparent hub pricing (TTF/NBP) limits realised spreads, though hedging and structured offtake in 2024 partially stabilized revenues.

Portfolio buyers with scale

Portfolio buyers such as large utilities and commodity traders aggregate demand across regions and use their scale to press for stricter quality specs, tighter balancing and tougher credit terms. Kistos’ negotiating leverage rises with consistent, flexible delivery and demonstrated operational reliability. Dealing with investment-grade counterparties (S&P BBB- or higher) lowers receivable risk but typically compresses realized margins. Concentrated buyer power therefore squeezes pricing flexibility for sellers.

Security‑of‑supply trade‑off

In tight 2024 markets buyers prioritized reliability over price, weakening their bargaining leverage and enabling suppliers like Kistos to command longer tenors; domestic lower‑emission production increasingly gained preferred status. Kistos’ operational efficiency and improving ESG metrics support contract length and price resilience, but as markets loosen buyer power can re‑intensify rapidly.

Regulatory pass‑through

Regulatory pass‑through: price caps and consumer protections in 2024 squeezed downstream margins, driving buyers to press upstream for concessions when regulated returns narrowed; Kistos mitigates this via indexed contracts linked to Brent and TTF hubs, reducing exposure to unilateral adjustments; political interventions can still shift negotiating leverage suddenly.

- 2024: increased buyer push when regulated returns fell

- Indexed contracts: Brent and TTF linkage

- Political risk: sudden shifts in negotiating dynamics

Balancing and flexibility fees

Balancing and flexibility fees erode Kistos netbacks as imbalance penalties and paid flexibility services shift value away from producers; in 2024 market reports showed elevated balancing costs during tight winter months. Sophisticated buyers leverage strict delivery windows to push costs upstream, increasing short-term cashflow variability. Investing in storage, swing capacity and improved forecasting in 2024 materially reduced buyer leverage and captured pricing premiums at peak demand.

- Imbalance penalties reduce realized netbacks

- Buyers use strict windows to transfer costs upstream

- Storage and swing lower customer bargaining power

- Operational flexibility earns premiums in peak periods

TTF/NBP anchoring keeps buyers powerful; reliability and storage enable longer-tenor premiums

Buyers hold strong leverage as gas is a standardized commodity with TTF and NBP anchoring 2024 pricing, enabling easy switching and limiting Kistos to hub-driven spreads. Large utilities and traders compress premiums via volume/credit terms while reliability and ESG gains let Kistos capture longer tenors in tight periods. Indexed contracts and balancing fees shifted margin pressure upstream but storage/swing reduced buyer power.

| Metric | 2024 Impact |

|---|---|

| Hub anchoring | TTF/NBP govern pricing |

| Contracting | Indexed to Brent/TTF |

| Flexibility | Storage/swing lowers buyer leverage |

Preview Before You Purchase

Kistos Porter's Five Forces Analysis

This preview displays the exact Kistos Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, ready for download and use the moment you buy. What you see here is the final, complete deliverable.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Kistos faces moderated supplier power and evolving buyer bargaining amid energy transition, while new entrants and substitutes pose emerging threats; competitive rivalry hinges on scale and project pipeline. This snapshot only scratches the surface — unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategic insights.

Suppliers Bargaining Power

Specialized OFS dependence

Upstream operations depend on a concentrated set of oilfield service firms and OEMs for drilling, subsea and compression, giving suppliers strong leverage over day rates and critical equipment availability. Limited qualified vendors in the North Sea can push input costs higher and create premium pricing during capacity tightness. Kistos mitigates this via multi-year frame agreements and equipment standardization to lock rates and improve sourcing flexibility. Schedule risk persists if key suppliers face bottlenecks or fleet constraints.

Rig and vessel scarcity

Harsh‑environment rigs and intervention vessels are highly cyclical and capacity‑constrained; North Sea rig utilization exceeded 85% in 2024, tightening supply and lifting dayrates by roughly 40% year‑on‑year. Forward booking and flexible scopes mitigate risk, but small operators lack scale to secure prime slots. Limited weather windows further amplify supplier leverage.

Infrastructure access fees

Processing plants and pipelines are often third‑party owned with tariff structures, and access negotiations plus tie‑in timing give midstream owners bargaining power, especially where few alternatives exist.

Regulatory third‑party access frameworks (EU/UK TPA regimes, updated post‑2019) can limit excess pricing but do not secure scheduling or priority for tie‑ins.

Kistos’ brownfield tie‑backs can still face take‑or‑pay exposure and commercial sequencing risks when capacity is constrained.

Low‑carbon tech providers

Specialized electrification, leak‑detection and emissions‑abatement technologies give suppliers moderate bargaining power as vendor pools and certification schemes remain concentrated; adoption supports Kistos’ lower‑carbon positioning and access to 2024 incentives (eg investment tax credits). Limited competition can raise prices, while co‑development deals trade margin for speed, credibility and faster deployment.

- Concentrated vendors → higher pricing pressure

- Adoption unlocks incentives and market differentiation

- Co‑development: margin sacrifice for speed/credibility

Skilled labor tightness

- Skilled scarcity: 2024 industry reports indicate tight labor pools

- Cost pressure: rising wages and retention premiums

- Constraint: training/local content reduce flexibility

- Mitigation: collaborative HSE and predictable campaigns lower talent costs

Supply squeeze: rigs >85% util, dayrates +~40% YoY

Suppliers hold elevated leverage: North Sea rig utilization >85% in 2024 and dayrates rose ~40% YoY, tightening access and lifting input costs. Concentrated OEMs, midstream tolling and scarce skilled crews amplify pricing and scheduling risk; Kistos uses multi‑year frames and standardisation to lock rates and improve flexibility. Electrification vendors remain concentrated but unlock 2024 incentives and differentiation.

| Metric | 2024 |

|---|---|

| Rig utilization | >85% |

| Dayrate change | +~40% YoY |

| Skilled labour | Reported tight pools (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Kistos, uncovering competitive intensity, supplier and buyer power, entry barriers, and substitute threats to its offshore energy services position. Detailed, strategic insights identify disruptive forces, pricing pressures, and protective dynamics to inform investor presentations and internal strategy.

A one-sheet Porter's Five Forces for Kistos that quantifies competitive pressure, lets you tweak inputs for scenarios, and exports clean visuals for decks—removing analysis bottlenecks and speeding strategic decisions.

Customers Bargaining Power

Commodity price‑takers

Natural gas is a standardized commodity so utilities, traders and industrials can switch sources readily, leaving Kistos as a price-taker; TTF and NBP remained the anchoring hubs in 2024. Buyers exert power via short‑term contracts and volume optionality, compressing Kistos’ ability to add premiums. Transparent hub pricing (TTF/NBP) limits realised spreads, though hedging and structured offtake in 2024 partially stabilized revenues.

Portfolio buyers with scale

Portfolio buyers such as large utilities and commodity traders aggregate demand across regions and use their scale to press for stricter quality specs, tighter balancing and tougher credit terms. Kistos’ negotiating leverage rises with consistent, flexible delivery and demonstrated operational reliability. Dealing with investment-grade counterparties (S&P BBB- or higher) lowers receivable risk but typically compresses realized margins. Concentrated buyer power therefore squeezes pricing flexibility for sellers.

Security‑of‑supply trade‑off

In tight 2024 markets buyers prioritized reliability over price, weakening their bargaining leverage and enabling suppliers like Kistos to command longer tenors; domestic lower‑emission production increasingly gained preferred status. Kistos’ operational efficiency and improving ESG metrics support contract length and price resilience, but as markets loosen buyer power can re‑intensify rapidly.

Regulatory pass‑through

Regulatory pass‑through: price caps and consumer protections in 2024 squeezed downstream margins, driving buyers to press upstream for concessions when regulated returns narrowed; Kistos mitigates this via indexed contracts linked to Brent and TTF hubs, reducing exposure to unilateral adjustments; political interventions can still shift negotiating leverage suddenly.

- 2024: increased buyer push when regulated returns fell

- Indexed contracts: Brent and TTF linkage

- Political risk: sudden shifts in negotiating dynamics

Balancing and flexibility fees

Balancing and flexibility fees erode Kistos netbacks as imbalance penalties and paid flexibility services shift value away from producers; in 2024 market reports showed elevated balancing costs during tight winter months. Sophisticated buyers leverage strict delivery windows to push costs upstream, increasing short-term cashflow variability. Investing in storage, swing capacity and improved forecasting in 2024 materially reduced buyer leverage and captured pricing premiums at peak demand.

- Imbalance penalties reduce realized netbacks

- Buyers use strict windows to transfer costs upstream

- Storage and swing lower customer bargaining power

- Operational flexibility earns premiums in peak periods

TTF/NBP anchoring keeps buyers powerful; reliability and storage enable longer-tenor premiums

Buyers hold strong leverage as gas is a standardized commodity with TTF and NBP anchoring 2024 pricing, enabling easy switching and limiting Kistos to hub-driven spreads. Large utilities and traders compress premiums via volume/credit terms while reliability and ESG gains let Kistos capture longer tenors in tight periods. Indexed contracts and balancing fees shifted margin pressure upstream but storage/swing reduced buyer power.

| Metric | 2024 Impact |

|---|---|

| Hub anchoring | TTF/NBP govern pricing |

| Contracting | Indexed to Brent/TTF |

| Flexibility | Storage/swing lowers buyer leverage |

Preview Before You Purchase

Kistos Porter's Five Forces Analysis

This preview displays the exact Kistos Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, ready for download and use the moment you buy. What you see here is the final, complete deliverable.