KITZ Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

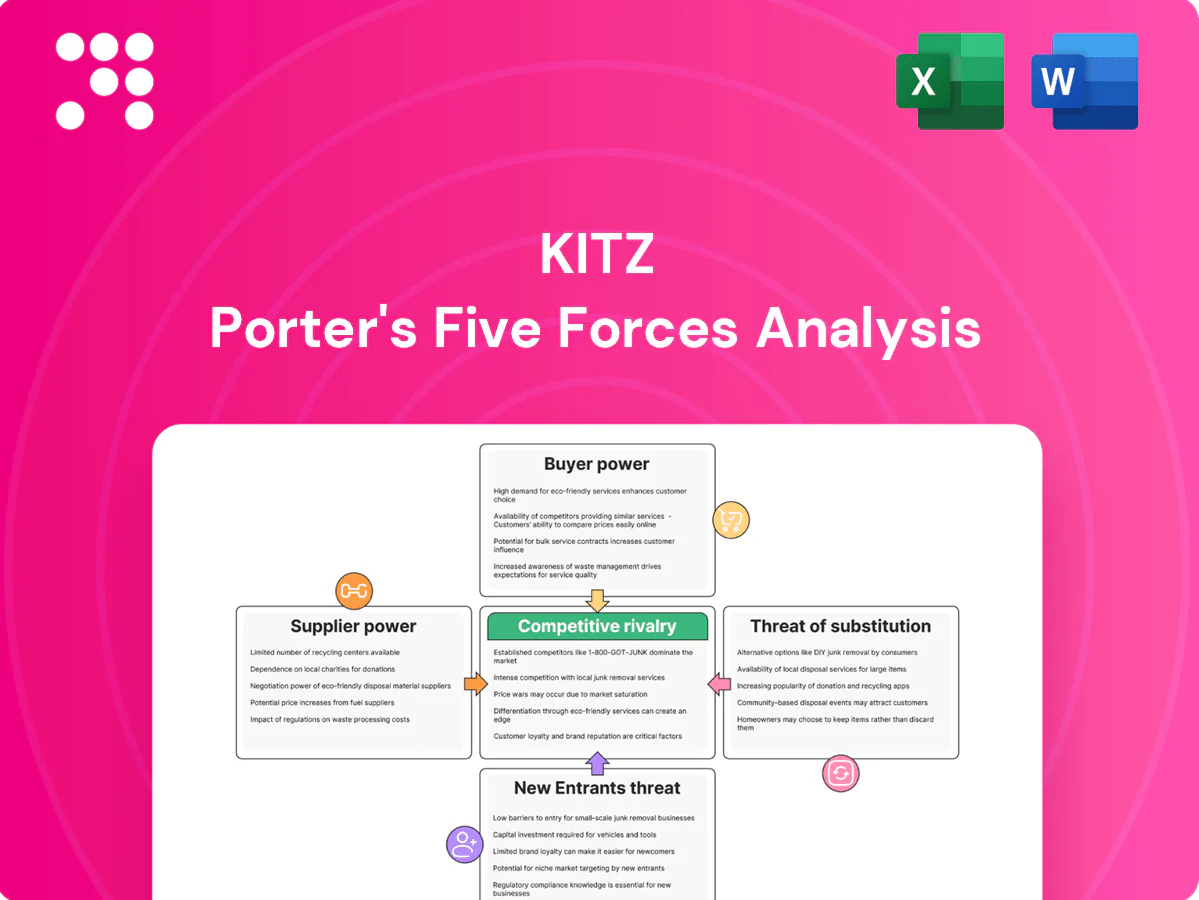

This snapshot highlights KITZ’s competitive pressures across suppliers, buyers, substitutes and entry threats. It teases strategic implications but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for a data-driven, consultant-grade breakdown tailored to KITZ.

Suppliers Bargaining Power

Critical metals and alloys

Valves depend on stainless steel, brass, specialty alloys and high‑grade castings; nickel supply is dominated by Indonesia and the Philippines while copper is led by Chile, concentrating leverage among select mills. 2024 market volatility in nickel, copper and molybdenum—often a copper byproduct—raised input-cost pressure and can squeeze KITZ margins if pass‑through is limited. Long‑term contracts and hedging practices partially mitigate this exposure.

Specialty components and seals

Seats, seals and elastomers for severe-service or ultrapure applications come from niche suppliers, with qualification cycles typically taking 6–12 months and tight performance specs limiting easy switching. This gives certified component makers moderate bargaining power, often reflected in premium pricing of 10–25% versus commodity parts. Dual-sourcing reduces supplier risk but commonly extends lead times by 2–6 weeks.

Logistics and geopolitical risk

Global supply chains expose KITZ to freight, tariff and geopolitical disruptions, highlighted by lingering US-China tariffs on roughly $360 billion of imports that raise input uncertainty and duty risk. Suppliers in concentrated regions gain leverage during bottlenecks, driving lead-time spikes and price pass-through. Buffer stocks and regionalized sourcing reduce disruption risk but typically raise inventory and sourcing costs by about 5-8%. Customers still demand ~98% on-time delivery, compressing KITZs operational flexibility.

Partial backward integration

Partial backward integration via in-house casting, machining and testing reduces supplier leverage, secures critical quality and shortens lead times; 2024 industry practice shows this is a key resilience move for industrial manufacturers. Not all alloys/parts are captive, so external vendor dependence persists and capital intensity can erode ROI if scaled indiscriminately.

- Reduce supplier spend: lower variability

- Protect quality: critical path control

- Residual dependence: specialty alloys

- Capex trade-off: ROI vs flexibility

Specification-driven inputs

Industry certifications dictate material grades and traceability, constraining sourcing in KITZ’s supply chain; API, JIS, ISO and UHP specs increasingly form procurement must-haves. Suppliers with these approvals capture measurable premiums and priority allocation in regulated end-markets. ISO 9001 had roughly 1.3 million certificates globally in 2023–24, underscoring widespread certification-driven sourcing.

- API/JIS/ISO/UHP: premium pricing

- Traceability rules: reduce switchability

- Regulated markets: higher supplier power

Metal volatility squeezes margins; niche seals, hedging and integration mitigate risk

KITZ faces concentrated metal suppliers (nickel, copper) and 2024 volatility that can compress margins; long‑term contracts/hedging partially offset risk. Niche seals/elastomers yield 10–25% premiums and 6–12 month qualification, limiting switchability. Partial backward integration cuts lead times but raises capex; inventory/regionalization add ~5–8% cost while customers demand ~98% on‑time delivery.

| Metric | Value |

|---|---|

| Nickel/copper volatility 2024 | High |

| Premiums (seals) | 10–25% |

| Qualification time | 6–12 months |

| Inventory cost uplift | 5–8% |

| On‑time delivery target | ~98% |

What is included in the product

Comprehensive Porter's Five Forces assessment of KITZ, revealing competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and strategic levers to protect margins and sustain market share.

KITZ Porter's Five Forces gives a single, clean one-sheet summary with customizable pressure levels and an instant spider/radar chart to visualize strategic threats—easy to copy into decks, adapt to scenarios, and integrate into existing reports without macros or advanced skills.

Customers Bargaining Power

Large EPCs and industrial majors

Large oil & gas, chemical, water and building EPCs buy valves and fittings in bundled contracts and negotiate aggressively, with bundled orders in 2024 frequently exceeding $50 million and driving single-supplier awards. Their purchasing scale forces price concessions and tighter service terms, and preferred-vendor lists concentrate over half of contract awards in major projects. KITZ must compete on total cost of ownership—price, delivery, reliability and aftermarket—to defend margin.

Qualification and switching costs

Application approval, documentation and compliance create meaningful switching frictions; as of 2024 requalification timelines for severe-service and semiconductor UHP parts typically run 6–12 months and often incur six-figure costs, tempering buyer leverage once parts are specified. In commoditized lines switching remains quicker and price-driven, so customer power is materially higher.

Product standardization vs customization

Standard ball, gate, globe, check, and butterfly valves remain highly comparable, giving buyers leverage on catalog SKUs; 2024 industry data shows commoditized valves drive price competition. Custom materials, specialty coatings, and integrated actuation lower comparability and can command premium pricing. KITZ can shift its sales mix toward configured and ETO solutions to reduce buyer power and protect margins.

Aftermarket and lifecycle value

Aftermarket spares, maintenance, and reliability shift buying decisions from upfront price to lifecycle value; 2024 industry benchmarks show service revenues often exceed 30% of total lifecycle value, increasing supplier margins and reducing buyer leverage.

Installed base lock-in and multi-year service-level agreements (SLAs) create stickiness—industry surveys in 2024 report 68% of buyers accept higher unit prices to avoid downtime—and unplanned downtime costs commonly outweigh marginal price differences.

- Spares-driven margins

- Installed-base lock-in

- SLA stickiness

- Downtime > price delta

Demand cyclicality and project timing

Project-driven demand at KITZ creates bidding intensity: peaks see multiple bidders, troughs enable buyers to exploit slack capacity and push prices down; industry estimates put the 2024 global industrial valve market around USD 79.2 billion, amplifying cyclical volume swings. Expedited schedules increase buyer leverage on delivery terms, while collaborative forecasting can rebalance negotiating power and reduce late-order premiums.

>$50M EPC bundles concentrate awards; 68% pay premium to avoid downtime

Large EPC bundled buys (often >$50m in 2024) concentrate awards and force price concessions; severe/UHP switching incurs 6–12 month requalification and six‑figure costs. Commoditized SKUs increase buyer leverage, while configured/aftermarket sales (service >30% lifecycle value) and installed‑base lock‑in reduce it; 68% pay premiums to avoid downtime.

| Metric | 2024 |

|---|---|

| Market size | USD 79.2B |

| Bundled order size | >$50M |

| Requalification | 6–12 months |

| Service % lifecycle | >30% |

| Buyers accept premium | 68% |

What You See Is What You Get

KITZ Porter's Five Forces Analysis

This preview shows the exact KITZ Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The full, professionally formatted document is ready for instant download and use the moment you buy. What you see here is the complete, final analysis file you'll get.

Go Beyond the Preview—Access the Full Strategic Report

This snapshot highlights KITZ’s competitive pressures across suppliers, buyers, substitutes and entry threats. It teases strategic implications but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for a data-driven, consultant-grade breakdown tailored to KITZ.

Suppliers Bargaining Power

Critical metals and alloys

Valves depend on stainless steel, brass, specialty alloys and high‑grade castings; nickel supply is dominated by Indonesia and the Philippines while copper is led by Chile, concentrating leverage among select mills. 2024 market volatility in nickel, copper and molybdenum—often a copper byproduct—raised input-cost pressure and can squeeze KITZ margins if pass‑through is limited. Long‑term contracts and hedging practices partially mitigate this exposure.

Specialty components and seals

Seats, seals and elastomers for severe-service or ultrapure applications come from niche suppliers, with qualification cycles typically taking 6–12 months and tight performance specs limiting easy switching. This gives certified component makers moderate bargaining power, often reflected in premium pricing of 10–25% versus commodity parts. Dual-sourcing reduces supplier risk but commonly extends lead times by 2–6 weeks.

Logistics and geopolitical risk

Global supply chains expose KITZ to freight, tariff and geopolitical disruptions, highlighted by lingering US-China tariffs on roughly $360 billion of imports that raise input uncertainty and duty risk. Suppliers in concentrated regions gain leverage during bottlenecks, driving lead-time spikes and price pass-through. Buffer stocks and regionalized sourcing reduce disruption risk but typically raise inventory and sourcing costs by about 5-8%. Customers still demand ~98% on-time delivery, compressing KITZs operational flexibility.

Partial backward integration

Partial backward integration via in-house casting, machining and testing reduces supplier leverage, secures critical quality and shortens lead times; 2024 industry practice shows this is a key resilience move for industrial manufacturers. Not all alloys/parts are captive, so external vendor dependence persists and capital intensity can erode ROI if scaled indiscriminately.

- Reduce supplier spend: lower variability

- Protect quality: critical path control

- Residual dependence: specialty alloys

- Capex trade-off: ROI vs flexibility

Specification-driven inputs

Industry certifications dictate material grades and traceability, constraining sourcing in KITZ’s supply chain; API, JIS, ISO and UHP specs increasingly form procurement must-haves. Suppliers with these approvals capture measurable premiums and priority allocation in regulated end-markets. ISO 9001 had roughly 1.3 million certificates globally in 2023–24, underscoring widespread certification-driven sourcing.

- API/JIS/ISO/UHP: premium pricing

- Traceability rules: reduce switchability

- Regulated markets: higher supplier power

Metal volatility squeezes margins; niche seals, hedging and integration mitigate risk

KITZ faces concentrated metal suppliers (nickel, copper) and 2024 volatility that can compress margins; long‑term contracts/hedging partially offset risk. Niche seals/elastomers yield 10–25% premiums and 6–12 month qualification, limiting switchability. Partial backward integration cuts lead times but raises capex; inventory/regionalization add ~5–8% cost while customers demand ~98% on‑time delivery.

| Metric | Value |

|---|---|

| Nickel/copper volatility 2024 | High |

| Premiums (seals) | 10–25% |

| Qualification time | 6–12 months |

| Inventory cost uplift | 5–8% |

| On‑time delivery target | ~98% |

What is included in the product

Comprehensive Porter's Five Forces assessment of KITZ, revealing competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and strategic levers to protect margins and sustain market share.

KITZ Porter's Five Forces gives a single, clean one-sheet summary with customizable pressure levels and an instant spider/radar chart to visualize strategic threats—easy to copy into decks, adapt to scenarios, and integrate into existing reports without macros or advanced skills.

Customers Bargaining Power

Large EPCs and industrial majors

Large oil & gas, chemical, water and building EPCs buy valves and fittings in bundled contracts and negotiate aggressively, with bundled orders in 2024 frequently exceeding $50 million and driving single-supplier awards. Their purchasing scale forces price concessions and tighter service terms, and preferred-vendor lists concentrate over half of contract awards in major projects. KITZ must compete on total cost of ownership—price, delivery, reliability and aftermarket—to defend margin.

Qualification and switching costs

Application approval, documentation and compliance create meaningful switching frictions; as of 2024 requalification timelines for severe-service and semiconductor UHP parts typically run 6–12 months and often incur six-figure costs, tempering buyer leverage once parts are specified. In commoditized lines switching remains quicker and price-driven, so customer power is materially higher.

Product standardization vs customization

Standard ball, gate, globe, check, and butterfly valves remain highly comparable, giving buyers leverage on catalog SKUs; 2024 industry data shows commoditized valves drive price competition. Custom materials, specialty coatings, and integrated actuation lower comparability and can command premium pricing. KITZ can shift its sales mix toward configured and ETO solutions to reduce buyer power and protect margins.

Aftermarket and lifecycle value

Aftermarket spares, maintenance, and reliability shift buying decisions from upfront price to lifecycle value; 2024 industry benchmarks show service revenues often exceed 30% of total lifecycle value, increasing supplier margins and reducing buyer leverage.

Installed base lock-in and multi-year service-level agreements (SLAs) create stickiness—industry surveys in 2024 report 68% of buyers accept higher unit prices to avoid downtime—and unplanned downtime costs commonly outweigh marginal price differences.

- Spares-driven margins

- Installed-base lock-in

- SLA stickiness

- Downtime > price delta

Demand cyclicality and project timing

Project-driven demand at KITZ creates bidding intensity: peaks see multiple bidders, troughs enable buyers to exploit slack capacity and push prices down; industry estimates put the 2024 global industrial valve market around USD 79.2 billion, amplifying cyclical volume swings. Expedited schedules increase buyer leverage on delivery terms, while collaborative forecasting can rebalance negotiating power and reduce late-order premiums.

>$50M EPC bundles concentrate awards; 68% pay premium to avoid downtime

Large EPC bundled buys (often >$50m in 2024) concentrate awards and force price concessions; severe/UHP switching incurs 6–12 month requalification and six‑figure costs. Commoditized SKUs increase buyer leverage, while configured/aftermarket sales (service >30% lifecycle value) and installed‑base lock‑in reduce it; 68% pay premiums to avoid downtime.

| Metric | 2024 |

|---|---|

| Market size | USD 79.2B |

| Bundled order size | >$50M |

| Requalification | 6–12 months |

| Service % lifecycle | >30% |

| Buyers accept premium | 68% |

What You See Is What You Get

KITZ Porter's Five Forces Analysis

This preview shows the exact KITZ Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The full, professionally formatted document is ready for instant download and use the moment you buy. What you see here is the complete, final analysis file you'll get.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

This snapshot highlights KITZ’s competitive pressures across suppliers, buyers, substitutes and entry threats. It teases strategic implications but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for a data-driven, consultant-grade breakdown tailored to KITZ.

Suppliers Bargaining Power

Critical metals and alloys

Valves depend on stainless steel, brass, specialty alloys and high‑grade castings; nickel supply is dominated by Indonesia and the Philippines while copper is led by Chile, concentrating leverage among select mills. 2024 market volatility in nickel, copper and molybdenum—often a copper byproduct—raised input-cost pressure and can squeeze KITZ margins if pass‑through is limited. Long‑term contracts and hedging practices partially mitigate this exposure.

Specialty components and seals

Seats, seals and elastomers for severe-service or ultrapure applications come from niche suppliers, with qualification cycles typically taking 6–12 months and tight performance specs limiting easy switching. This gives certified component makers moderate bargaining power, often reflected in premium pricing of 10–25% versus commodity parts. Dual-sourcing reduces supplier risk but commonly extends lead times by 2–6 weeks.

Logistics and geopolitical risk

Global supply chains expose KITZ to freight, tariff and geopolitical disruptions, highlighted by lingering US-China tariffs on roughly $360 billion of imports that raise input uncertainty and duty risk. Suppliers in concentrated regions gain leverage during bottlenecks, driving lead-time spikes and price pass-through. Buffer stocks and regionalized sourcing reduce disruption risk but typically raise inventory and sourcing costs by about 5-8%. Customers still demand ~98% on-time delivery, compressing KITZs operational flexibility.

Partial backward integration

Partial backward integration via in-house casting, machining and testing reduces supplier leverage, secures critical quality and shortens lead times; 2024 industry practice shows this is a key resilience move for industrial manufacturers. Not all alloys/parts are captive, so external vendor dependence persists and capital intensity can erode ROI if scaled indiscriminately.

- Reduce supplier spend: lower variability

- Protect quality: critical path control

- Residual dependence: specialty alloys

- Capex trade-off: ROI vs flexibility

Specification-driven inputs

Industry certifications dictate material grades and traceability, constraining sourcing in KITZ’s supply chain; API, JIS, ISO and UHP specs increasingly form procurement must-haves. Suppliers with these approvals capture measurable premiums and priority allocation in regulated end-markets. ISO 9001 had roughly 1.3 million certificates globally in 2023–24, underscoring widespread certification-driven sourcing.

- API/JIS/ISO/UHP: premium pricing

- Traceability rules: reduce switchability

- Regulated markets: higher supplier power

Metal volatility squeezes margins; niche seals, hedging and integration mitigate risk

KITZ faces concentrated metal suppliers (nickel, copper) and 2024 volatility that can compress margins; long‑term contracts/hedging partially offset risk. Niche seals/elastomers yield 10–25% premiums and 6–12 month qualification, limiting switchability. Partial backward integration cuts lead times but raises capex; inventory/regionalization add ~5–8% cost while customers demand ~98% on‑time delivery.

| Metric | Value |

|---|---|

| Nickel/copper volatility 2024 | High |

| Premiums (seals) | 10–25% |

| Qualification time | 6–12 months |

| Inventory cost uplift | 5–8% |

| On‑time delivery target | ~98% |

What is included in the product

Comprehensive Porter's Five Forces assessment of KITZ, revealing competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and strategic levers to protect margins and sustain market share.

KITZ Porter's Five Forces gives a single, clean one-sheet summary with customizable pressure levels and an instant spider/radar chart to visualize strategic threats—easy to copy into decks, adapt to scenarios, and integrate into existing reports without macros or advanced skills.

Customers Bargaining Power

Large EPCs and industrial majors

Large oil & gas, chemical, water and building EPCs buy valves and fittings in bundled contracts and negotiate aggressively, with bundled orders in 2024 frequently exceeding $50 million and driving single-supplier awards. Their purchasing scale forces price concessions and tighter service terms, and preferred-vendor lists concentrate over half of contract awards in major projects. KITZ must compete on total cost of ownership—price, delivery, reliability and aftermarket—to defend margin.

Qualification and switching costs

Application approval, documentation and compliance create meaningful switching frictions; as of 2024 requalification timelines for severe-service and semiconductor UHP parts typically run 6–12 months and often incur six-figure costs, tempering buyer leverage once parts are specified. In commoditized lines switching remains quicker and price-driven, so customer power is materially higher.

Product standardization vs customization

Standard ball, gate, globe, check, and butterfly valves remain highly comparable, giving buyers leverage on catalog SKUs; 2024 industry data shows commoditized valves drive price competition. Custom materials, specialty coatings, and integrated actuation lower comparability and can command premium pricing. KITZ can shift its sales mix toward configured and ETO solutions to reduce buyer power and protect margins.

Aftermarket and lifecycle value

Aftermarket spares, maintenance, and reliability shift buying decisions from upfront price to lifecycle value; 2024 industry benchmarks show service revenues often exceed 30% of total lifecycle value, increasing supplier margins and reducing buyer leverage.

Installed base lock-in and multi-year service-level agreements (SLAs) create stickiness—industry surveys in 2024 report 68% of buyers accept higher unit prices to avoid downtime—and unplanned downtime costs commonly outweigh marginal price differences.

- Spares-driven margins

- Installed-base lock-in

- SLA stickiness

- Downtime > price delta

Demand cyclicality and project timing

Project-driven demand at KITZ creates bidding intensity: peaks see multiple bidders, troughs enable buyers to exploit slack capacity and push prices down; industry estimates put the 2024 global industrial valve market around USD 79.2 billion, amplifying cyclical volume swings. Expedited schedules increase buyer leverage on delivery terms, while collaborative forecasting can rebalance negotiating power and reduce late-order premiums.

>$50M EPC bundles concentrate awards; 68% pay premium to avoid downtime

Large EPC bundled buys (often >$50m in 2024) concentrate awards and force price concessions; severe/UHP switching incurs 6–12 month requalification and six‑figure costs. Commoditized SKUs increase buyer leverage, while configured/aftermarket sales (service >30% lifecycle value) and installed‑base lock‑in reduce it; 68% pay premiums to avoid downtime.

| Metric | 2024 |

|---|---|

| Market size | USD 79.2B |

| Bundled order size | >$50M |

| Requalification | 6–12 months |

| Service % lifecycle | >30% |

| Buyers accept premium | 68% |

What You See Is What You Get

KITZ Porter's Five Forces Analysis

This preview shows the exact KITZ Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The full, professionally formatted document is ready for instant download and use the moment you buy. What you see here is the complete, final analysis file you'll get.