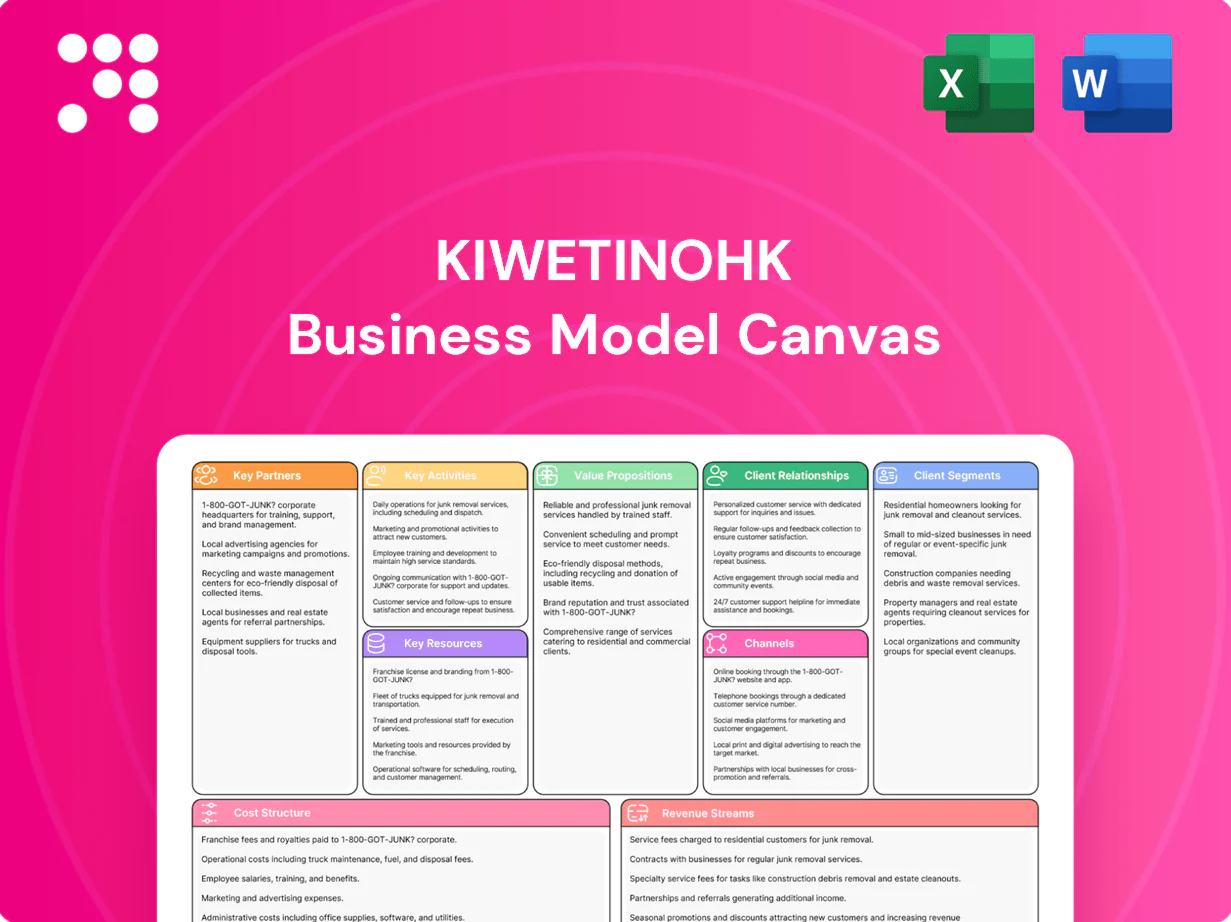

Kiwetinohk Business Model Canvas

Download the Business Model Canvas to map value, customers, partnerships and revenue

Unlock the full strategic blueprint behind Kiwetinohk with our Business Model Canvas—three to five clear sentences won't capture the depth: this downloadable file maps value propositions, customer segments, revenue streams and key partnerships so you can benchmark, plan, and pitch with confidence. Purchase the full Canvas in Word and Excel to access actionable insights and start applying proven strategies today.

Partnerships

Midstream and pipeline operators

Partnerships with gas gathering, processing and pipeline firms — notably NGTL (≈16 Bcf/d regional takeaway) — secure takeaway capacity and efficient liquids handling, reducing bottlenecks and narrowing AECO basis differentials by roughly US$0.50/Mcf in 2023–24. Long-term transportation agreements (typically 5–15 years) stabilize costs and market access. Collaboration also enables routing CO2 into regional transport corridors supporting CCS projects with capacities in the 1–3 Mtpa range.

Technology and CCS solution providers

Alliances with capture technology vendors, subsurface modeling experts and CO2 MMV firms accelerate Kiwetinohk deployment, leveraging an industry with over 40 MtCO2/yr operational capture capacity (2024). Joint pilots de-risk capture efficiency and storage integrity and shorten typical 5–10 year project development timelines. Shared IP and service agreements lower implementation time and cost, and help qualify projects for tax credits such as US 45Q (up to about $85/ton) and low-carbon certifications.

Power equipment OEMs and EPC contractors

OEMs supply turbines, balance-of-plant and renewables while EPCs deliver turnkey execution; 10-year LTSAs and performance guarantees target >95% availability and cap O&M costs, improving bankability. Coordinated delivery aligns gas supply contracts with commissioning to avoid delay penalties; partners also conduct grid-code compliance and interconnection studies (typical 12–24 month lead times in 2024).

Indigenous communities and local stakeholders

Engagement agreements secure land access, workforce participation and shared benefits through formal impact and revenue-sharing arrangements, while collaborative monitoring programs enhance environmental stewardship and bolster social license to operate. Co-development with Indigenous partners can streamline permitting and reduce timelines by aligning project design with Indigenous knowledge. Transparent governance structures build long-term trust and project resilience.

- Engagement agreements: land access, jobs, revenue

- Monitoring: joint environmental stewardship

- Co-development: improved permitting timelines

- Governance: transparency → trust, resilience

Financial institutions and offtakers

Lenders, infrastructure funds and corporate offtakers underpin Kiwetinohk project finance, with infrastructure dry powder ~$1.2trn in 2024 supporting deal liquidity. Long‑term PPAs and gas supply contracts (typical tenors 10–15 years) provide bankable cash flows. Hedging counterparties manage commodity and power price risk; EU carbon prices traded ~€80–100/t in 2024. Structured finance ties CCS incentives and carbon markets to improve debt sizing.

- Lenders: project debt capacity, covenant structures

- Infrastructure funds: ~$1.2trn dry powder (2024)

- Offtakers: PPAs 10–15y for bankability

- Hedging: counterparties for power/commodity risk

- Structured finance: aligns CCS incentives and carbon market revenue (~€80–100/t 2024)

Partnerships secure ~16 Bcf/d takeaway, CO2 corridors 1-3 Mtpa, AECO ≈ $0.50/Mcf

Partnerships secure NGTL takeaway (~16 Bcf/d), long-term transport (5–15y) and CO2 corridors (1–3 Mtpa), narrowing AECO basis ≈$0.50/Mcf (2023–24). Alliances with capture vendors leverage ~40 MtCO2/yr capacity (2024) and incentives (US 45Q ≈$85/t). Lenders and offtakers tap ~$1.2trn infra dry powder (2024) for project finance.

| Partner | Role | Key metric (2024) |

|---|---|---|

| NGTL | Takeaway | ≈16 Bcf/d |

| CCS vendors | Capture & storage | ≈40 MtCO2/yr |

| Finance | Project capital | $1.2trn dry powder |

| Markets | Carbon price | €80–100/t |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Kiwetinohk that maps all nine BMC blocks with clear value propositions, customer segments, channels and revenue logic; includes competitive advantages, linked SWOT insights and polished narratives ideal for investor presentations and strategic decision-making.

High-level view of Kiwetinohk’s business model with editable cells to quickly surface and relieve operational pain points; perfect for team collaboration, executive briefs, or fast comparison against alternative models.

Activities

Natural gas and NGL development

Plan, drill, complete and produce wells across the Western Canadian Sedimentary Basin targeting scalable gas output within Canada’s ~16.6 Bcf/d basin; optimize pad design, frac intensity and artificial lift to boost per-well recovery and NGL yields (targeting +20–35% NGL uplift on mixed gas streams). Manage gathering and processing to maximize NGL capture and revenue, integrate emissions tracking with methane-intensity goals around 0.2% and deploy abatement across operations.

Power project development and operations

Originate, permit, finance and build gas-fired and renewable assets, following typical interconnection study and market registration timelines of 12–24 months; combined-cycle units target heat rates around 6,000–7,000 Btu/kWh while simple-cycle units run 9,000–11,000 Btu/kWh. Operate plants to meet availability targets above 90% and optimize dispatch against market signals and fuel-price dynamics in real-time markets.

CCS integration and emissions management

Design and deploy capture systems with CO2 compression, transport and storage solutions aligned to industry capture costs of roughly 40–120 USD/t and global CCS capacity ~40 MtCO2/yr (2023), targeting geologic sinks within the >2,000 GtCO2 global storage resource.

Conduct reservoir characterization and MMV planning using seismic and well data to de-risk storage and meet regulatory MRV standards.

Pursue credits, grants and compliance pathways—leveraging Canada’s federal carbon framework (federal price 65 USD/t in 2023)—to monetize reductions.

Continuously lower lifecycle carbon intensity through process optimization and electrification, tracking CI metrics per barrel and per MWh.

Commercial contracting and risk management

Kiwetinohk negotiates PPAs, gas sales, transportation and tolling agreements to secure supply, price certainty and operational flexibility for industrial and utility customers. Hedging programs manage basis, heat-rate, spark-spread and carbon exposure, with Canada’s federal carbon price at C$80/tonne in 2024 materially affecting contract economics. Contracts include flexible dispatch/tolling terms and strict counterparty oversight, credit limits and collateral management to protect cashflow.

- Negotiate PPAs, gas, transport, tolling

- Hedge basis, heat-rate, spark-spread, carbon

- Flexible terms for industrials & utilities

- Counterparty risk, credit limits, collateral

Regulatory, ESG, and stakeholder engagement

Secure permits, licenses and environmental approvals for projects while aligning ESG disclosures to TCFD, SASB and the ISSB standards effective 2024; maintain emissions reporting compatible with national inventories and GHG protocols. Proactively engage communities, Indigenous partners and policymakers through formal agreements and benefit-sharing; enforce HSE excellence with continuous compliance audits and corrective action tracking.

- Permits & approvals: legal risk mitigation

- ESG reporting: TCFD/SASB/ISSB-aligned

- Stakeholder engagement: Indigenous & community agreements

- HSE & audits: continuous compliance

Optimize WCSB pads to lift NGLs +20–35% and target methane ~0.2%

Plan, drill and produce scalable gas wells in the WCSB optimizing pad design, frac and lift to lift NGLs +20–35% and target methane intensity ~0.2%. Develop gas-fired and renewables (plant availability >90%) and CCS (capture cost $40–120/t). Negotiate PPAs, hedges and permits; align ESG to TCFD/SASB/ISSB and use C$80/t carbon price (2024).

| Metric | Value |

|---|---|

| NGL uplift | +20–35% |

| Methane intensity | ~0.2% |

| Carbon price (2024) | C$80/t |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual Kiwetinohk Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this exact file with all sections included, ready to edit and present. Files are delivered in Word and Excel formats for immediate use and customization.

Download the Business Model Canvas to map value, customers, partnerships and revenue

Unlock the full strategic blueprint behind Kiwetinohk with our Business Model Canvas—three to five clear sentences won't capture the depth: this downloadable file maps value propositions, customer segments, revenue streams and key partnerships so you can benchmark, plan, and pitch with confidence. Purchase the full Canvas in Word and Excel to access actionable insights and start applying proven strategies today.

Partnerships

Midstream and pipeline operators

Partnerships with gas gathering, processing and pipeline firms — notably NGTL (≈16 Bcf/d regional takeaway) — secure takeaway capacity and efficient liquids handling, reducing bottlenecks and narrowing AECO basis differentials by roughly US$0.50/Mcf in 2023–24. Long-term transportation agreements (typically 5–15 years) stabilize costs and market access. Collaboration also enables routing CO2 into regional transport corridors supporting CCS projects with capacities in the 1–3 Mtpa range.

Technology and CCS solution providers

Alliances with capture technology vendors, subsurface modeling experts and CO2 MMV firms accelerate Kiwetinohk deployment, leveraging an industry with over 40 MtCO2/yr operational capture capacity (2024). Joint pilots de-risk capture efficiency and storage integrity and shorten typical 5–10 year project development timelines. Shared IP and service agreements lower implementation time and cost, and help qualify projects for tax credits such as US 45Q (up to about $85/ton) and low-carbon certifications.

Power equipment OEMs and EPC contractors

OEMs supply turbines, balance-of-plant and renewables while EPCs deliver turnkey execution; 10-year LTSAs and performance guarantees target >95% availability and cap O&M costs, improving bankability. Coordinated delivery aligns gas supply contracts with commissioning to avoid delay penalties; partners also conduct grid-code compliance and interconnection studies (typical 12–24 month lead times in 2024).

Indigenous communities and local stakeholders

Engagement agreements secure land access, workforce participation and shared benefits through formal impact and revenue-sharing arrangements, while collaborative monitoring programs enhance environmental stewardship and bolster social license to operate. Co-development with Indigenous partners can streamline permitting and reduce timelines by aligning project design with Indigenous knowledge. Transparent governance structures build long-term trust and project resilience.

- Engagement agreements: land access, jobs, revenue

- Monitoring: joint environmental stewardship

- Co-development: improved permitting timelines

- Governance: transparency → trust, resilience

Financial institutions and offtakers

Lenders, infrastructure funds and corporate offtakers underpin Kiwetinohk project finance, with infrastructure dry powder ~$1.2trn in 2024 supporting deal liquidity. Long‑term PPAs and gas supply contracts (typical tenors 10–15 years) provide bankable cash flows. Hedging counterparties manage commodity and power price risk; EU carbon prices traded ~€80–100/t in 2024. Structured finance ties CCS incentives and carbon markets to improve debt sizing.

- Lenders: project debt capacity, covenant structures

- Infrastructure funds: ~$1.2trn dry powder (2024)

- Offtakers: PPAs 10–15y for bankability

- Hedging: counterparties for power/commodity risk

- Structured finance: aligns CCS incentives and carbon market revenue (~€80–100/t 2024)

Partnerships secure ~16 Bcf/d takeaway, CO2 corridors 1-3 Mtpa, AECO ≈ $0.50/Mcf

Partnerships secure NGTL takeaway (~16 Bcf/d), long-term transport (5–15y) and CO2 corridors (1–3 Mtpa), narrowing AECO basis ≈$0.50/Mcf (2023–24). Alliances with capture vendors leverage ~40 MtCO2/yr capacity (2024) and incentives (US 45Q ≈$85/t). Lenders and offtakers tap ~$1.2trn infra dry powder (2024) for project finance.

| Partner | Role | Key metric (2024) |

|---|---|---|

| NGTL | Takeaway | ≈16 Bcf/d |

| CCS vendors | Capture & storage | ≈40 MtCO2/yr |

| Finance | Project capital | $1.2trn dry powder |

| Markets | Carbon price | €80–100/t |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Kiwetinohk that maps all nine BMC blocks with clear value propositions, customer segments, channels and revenue logic; includes competitive advantages, linked SWOT insights and polished narratives ideal for investor presentations and strategic decision-making.

High-level view of Kiwetinohk’s business model with editable cells to quickly surface and relieve operational pain points; perfect for team collaboration, executive briefs, or fast comparison against alternative models.

Activities

Natural gas and NGL development

Plan, drill, complete and produce wells across the Western Canadian Sedimentary Basin targeting scalable gas output within Canada’s ~16.6 Bcf/d basin; optimize pad design, frac intensity and artificial lift to boost per-well recovery and NGL yields (targeting +20–35% NGL uplift on mixed gas streams). Manage gathering and processing to maximize NGL capture and revenue, integrate emissions tracking with methane-intensity goals around 0.2% and deploy abatement across operations.

Power project development and operations

Originate, permit, finance and build gas-fired and renewable assets, following typical interconnection study and market registration timelines of 12–24 months; combined-cycle units target heat rates around 6,000–7,000 Btu/kWh while simple-cycle units run 9,000–11,000 Btu/kWh. Operate plants to meet availability targets above 90% and optimize dispatch against market signals and fuel-price dynamics in real-time markets.

CCS integration and emissions management

Design and deploy capture systems with CO2 compression, transport and storage solutions aligned to industry capture costs of roughly 40–120 USD/t and global CCS capacity ~40 MtCO2/yr (2023), targeting geologic sinks within the >2,000 GtCO2 global storage resource.

Conduct reservoir characterization and MMV planning using seismic and well data to de-risk storage and meet regulatory MRV standards.

Pursue credits, grants and compliance pathways—leveraging Canada’s federal carbon framework (federal price 65 USD/t in 2023)—to monetize reductions.

Continuously lower lifecycle carbon intensity through process optimization and electrification, tracking CI metrics per barrel and per MWh.

Commercial contracting and risk management

Kiwetinohk negotiates PPAs, gas sales, transportation and tolling agreements to secure supply, price certainty and operational flexibility for industrial and utility customers. Hedging programs manage basis, heat-rate, spark-spread and carbon exposure, with Canada’s federal carbon price at C$80/tonne in 2024 materially affecting contract economics. Contracts include flexible dispatch/tolling terms and strict counterparty oversight, credit limits and collateral management to protect cashflow.

- Negotiate PPAs, gas, transport, tolling

- Hedge basis, heat-rate, spark-spread, carbon

- Flexible terms for industrials & utilities

- Counterparty risk, credit limits, collateral

Regulatory, ESG, and stakeholder engagement

Secure permits, licenses and environmental approvals for projects while aligning ESG disclosures to TCFD, SASB and the ISSB standards effective 2024; maintain emissions reporting compatible with national inventories and GHG protocols. Proactively engage communities, Indigenous partners and policymakers through formal agreements and benefit-sharing; enforce HSE excellence with continuous compliance audits and corrective action tracking.

- Permits & approvals: legal risk mitigation

- ESG reporting: TCFD/SASB/ISSB-aligned

- Stakeholder engagement: Indigenous & community agreements

- HSE & audits: continuous compliance

Optimize WCSB pads to lift NGLs +20–35% and target methane ~0.2%

Plan, drill and produce scalable gas wells in the WCSB optimizing pad design, frac and lift to lift NGLs +20–35% and target methane intensity ~0.2%. Develop gas-fired and renewables (plant availability >90%) and CCS (capture cost $40–120/t). Negotiate PPAs, hedges and permits; align ESG to TCFD/SASB/ISSB and use C$80/t carbon price (2024).

| Metric | Value |

|---|---|

| NGL uplift | +20–35% |

| Methane intensity | ~0.2% |

| Carbon price (2024) | C$80/t |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual Kiwetinohk Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this exact file with all sections included, ready to edit and present. Files are delivered in Word and Excel formats for immediate use and customization.

Original: $10.00

-65%$10.00

$3.50Description

Download the Business Model Canvas to map value, customers, partnerships and revenue

Unlock the full strategic blueprint behind Kiwetinohk with our Business Model Canvas—three to five clear sentences won't capture the depth: this downloadable file maps value propositions, customer segments, revenue streams and key partnerships so you can benchmark, plan, and pitch with confidence. Purchase the full Canvas in Word and Excel to access actionable insights and start applying proven strategies today.

Partnerships

Midstream and pipeline operators

Partnerships with gas gathering, processing and pipeline firms — notably NGTL (≈16 Bcf/d regional takeaway) — secure takeaway capacity and efficient liquids handling, reducing bottlenecks and narrowing AECO basis differentials by roughly US$0.50/Mcf in 2023–24. Long-term transportation agreements (typically 5–15 years) stabilize costs and market access. Collaboration also enables routing CO2 into regional transport corridors supporting CCS projects with capacities in the 1–3 Mtpa range.

Technology and CCS solution providers

Alliances with capture technology vendors, subsurface modeling experts and CO2 MMV firms accelerate Kiwetinohk deployment, leveraging an industry with over 40 MtCO2/yr operational capture capacity (2024). Joint pilots de-risk capture efficiency and storage integrity and shorten typical 5–10 year project development timelines. Shared IP and service agreements lower implementation time and cost, and help qualify projects for tax credits such as US 45Q (up to about $85/ton) and low-carbon certifications.

Power equipment OEMs and EPC contractors

OEMs supply turbines, balance-of-plant and renewables while EPCs deliver turnkey execution; 10-year LTSAs and performance guarantees target >95% availability and cap O&M costs, improving bankability. Coordinated delivery aligns gas supply contracts with commissioning to avoid delay penalties; partners also conduct grid-code compliance and interconnection studies (typical 12–24 month lead times in 2024).

Indigenous communities and local stakeholders

Engagement agreements secure land access, workforce participation and shared benefits through formal impact and revenue-sharing arrangements, while collaborative monitoring programs enhance environmental stewardship and bolster social license to operate. Co-development with Indigenous partners can streamline permitting and reduce timelines by aligning project design with Indigenous knowledge. Transparent governance structures build long-term trust and project resilience.

- Engagement agreements: land access, jobs, revenue

- Monitoring: joint environmental stewardship

- Co-development: improved permitting timelines

- Governance: transparency → trust, resilience

Financial institutions and offtakers

Lenders, infrastructure funds and corporate offtakers underpin Kiwetinohk project finance, with infrastructure dry powder ~$1.2trn in 2024 supporting deal liquidity. Long‑term PPAs and gas supply contracts (typical tenors 10–15 years) provide bankable cash flows. Hedging counterparties manage commodity and power price risk; EU carbon prices traded ~€80–100/t in 2024. Structured finance ties CCS incentives and carbon markets to improve debt sizing.

- Lenders: project debt capacity, covenant structures

- Infrastructure funds: ~$1.2trn dry powder (2024)

- Offtakers: PPAs 10–15y for bankability

- Hedging: counterparties for power/commodity risk

- Structured finance: aligns CCS incentives and carbon market revenue (~€80–100/t 2024)

Partnerships secure ~16 Bcf/d takeaway, CO2 corridors 1-3 Mtpa, AECO ≈ $0.50/Mcf

Partnerships secure NGTL takeaway (~16 Bcf/d), long-term transport (5–15y) and CO2 corridors (1–3 Mtpa), narrowing AECO basis ≈$0.50/Mcf (2023–24). Alliances with capture vendors leverage ~40 MtCO2/yr capacity (2024) and incentives (US 45Q ≈$85/t). Lenders and offtakers tap ~$1.2trn infra dry powder (2024) for project finance.

| Partner | Role | Key metric (2024) |

|---|---|---|

| NGTL | Takeaway | ≈16 Bcf/d |

| CCS vendors | Capture & storage | ≈40 MtCO2/yr |

| Finance | Project capital | $1.2trn dry powder |

| Markets | Carbon price | €80–100/t |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Kiwetinohk that maps all nine BMC blocks with clear value propositions, customer segments, channels and revenue logic; includes competitive advantages, linked SWOT insights and polished narratives ideal for investor presentations and strategic decision-making.

High-level view of Kiwetinohk’s business model with editable cells to quickly surface and relieve operational pain points; perfect for team collaboration, executive briefs, or fast comparison against alternative models.

Activities

Natural gas and NGL development

Plan, drill, complete and produce wells across the Western Canadian Sedimentary Basin targeting scalable gas output within Canada’s ~16.6 Bcf/d basin; optimize pad design, frac intensity and artificial lift to boost per-well recovery and NGL yields (targeting +20–35% NGL uplift on mixed gas streams). Manage gathering and processing to maximize NGL capture and revenue, integrate emissions tracking with methane-intensity goals around 0.2% and deploy abatement across operations.

Power project development and operations

Originate, permit, finance and build gas-fired and renewable assets, following typical interconnection study and market registration timelines of 12–24 months; combined-cycle units target heat rates around 6,000–7,000 Btu/kWh while simple-cycle units run 9,000–11,000 Btu/kWh. Operate plants to meet availability targets above 90% and optimize dispatch against market signals and fuel-price dynamics in real-time markets.

CCS integration and emissions management

Design and deploy capture systems with CO2 compression, transport and storage solutions aligned to industry capture costs of roughly 40–120 USD/t and global CCS capacity ~40 MtCO2/yr (2023), targeting geologic sinks within the >2,000 GtCO2 global storage resource.

Conduct reservoir characterization and MMV planning using seismic and well data to de-risk storage and meet regulatory MRV standards.

Pursue credits, grants and compliance pathways—leveraging Canada’s federal carbon framework (federal price 65 USD/t in 2023)—to monetize reductions.

Continuously lower lifecycle carbon intensity through process optimization and electrification, tracking CI metrics per barrel and per MWh.

Commercial contracting and risk management

Kiwetinohk negotiates PPAs, gas sales, transportation and tolling agreements to secure supply, price certainty and operational flexibility for industrial and utility customers. Hedging programs manage basis, heat-rate, spark-spread and carbon exposure, with Canada’s federal carbon price at C$80/tonne in 2024 materially affecting contract economics. Contracts include flexible dispatch/tolling terms and strict counterparty oversight, credit limits and collateral management to protect cashflow.

- Negotiate PPAs, gas, transport, tolling

- Hedge basis, heat-rate, spark-spread, carbon

- Flexible terms for industrials & utilities

- Counterparty risk, credit limits, collateral

Regulatory, ESG, and stakeholder engagement

Secure permits, licenses and environmental approvals for projects while aligning ESG disclosures to TCFD, SASB and the ISSB standards effective 2024; maintain emissions reporting compatible with national inventories and GHG protocols. Proactively engage communities, Indigenous partners and policymakers through formal agreements and benefit-sharing; enforce HSE excellence with continuous compliance audits and corrective action tracking.

- Permits & approvals: legal risk mitigation

- ESG reporting: TCFD/SASB/ISSB-aligned

- Stakeholder engagement: Indigenous & community agreements

- HSE & audits: continuous compliance

Optimize WCSB pads to lift NGLs +20–35% and target methane ~0.2%

Plan, drill and produce scalable gas wells in the WCSB optimizing pad design, frac and lift to lift NGLs +20–35% and target methane intensity ~0.2%. Develop gas-fired and renewables (plant availability >90%) and CCS (capture cost $40–120/t). Negotiate PPAs, hedges and permits; align ESG to TCFD/SASB/ISSB and use C$80/t carbon price (2024).

| Metric | Value |

|---|---|

| NGL uplift | +20–35% |

| Methane intensity | ~0.2% |

| Carbon price (2024) | C$80/t |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual Kiwetinohk Business Model Canvas, not a mockup or sample. When you purchase, you’ll receive this exact file with all sections included, ready to edit and present. Files are delivered in Word and Excel formats for immediate use and customization.