Kawasaki Kisen Kaisha Porter's Five Forces Analysis

Don't Miss the Bigger Picture

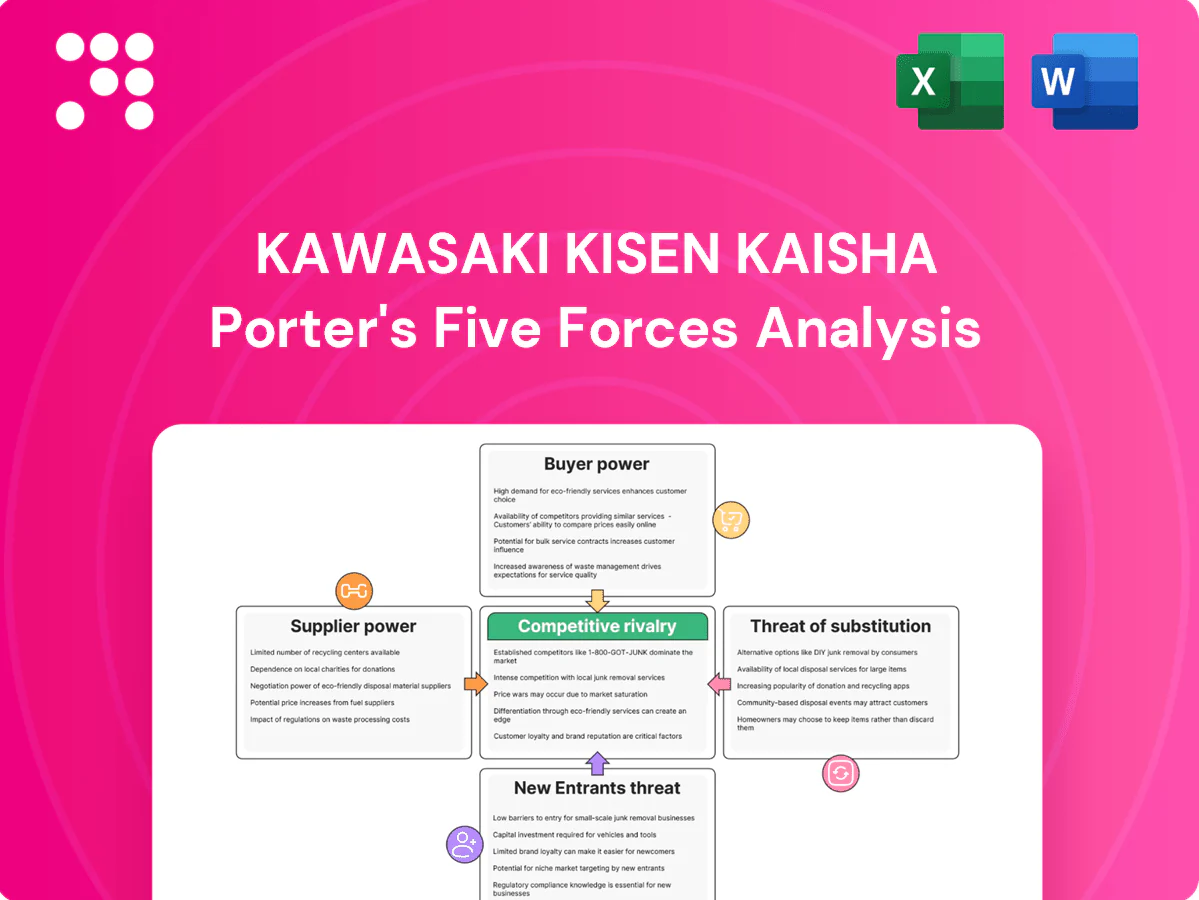

Kawasaki Kisen Kaisha faces intense rivalry, evolving buyer power, and supply-chain pressures that shape its freight and logistics margins; regulatory and technological shifts add strategic urgency. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kawasaki Kisen Kaisha’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated shipbuilders and engine makers

Global shipbuilding capacity is highly concentrated: in 2024 China ~42% of GT, Korea ~33% and Japan ~10%, giving major yards leverage on pricing and delivery slots; top marine engine makers (MAN Energy, WinGD, Wartsila) supply a majority of large two‑stroke engines (~60%+). For K LINE, switching core vessel/engine suppliers is slow and costly, often adding months and higher capex, while newbuild lead times of 18–36 months and engine lead times of 12–24 months can squeeze retrofit and delivery schedules.

Fuel and bunker suppliers’ pricing power

Marine fuel markets remain highly volatile, driven by OPEC+ production moves, geopolitics and refining capacity constraints; benchmark-led bunker prices can spike sharply during supply disruptions despite a competitive supplier base at major hubs. The shift to compliance fuels (VLSFO, MGO) and growing LNG bunkering increases sourcing complexity and premium risk. K LINE’s scale supports competitive tenders and hedging programs, but does not fully insulate it from sudden price shocks.

Specialized equipment and digital systems

Ballast water treatment units, exhaust scrubbers, LNG fuel systems and voyage-optimization software are sourced from specialized vendors, with BWTS retrofit typically $0.5–1.5M, scrubbers $2–5M and LNG premiums often $10–20M, while software runs ~$10k–50k/vessel/year (2024 industry ranges). Certification and complex integration raise switching costs; vendors leverage power through maintenance contracts and update cycles that capture recurring revenue. K LINE reduces supplier leverage via fleet standardization and multi-sourcing where feasible.

Crewing and technical services constraints

Qualified seafarers, especially for LNG and advanced ships, remain scarce; BIMCO/ICS 2024 projects an officer shortfall of about 147,500 by 2025. Training, safety and STCW compliance heighten dependence on manning and technical managers, while wage inflation and rising compliance costs push crew-related operating expenses up. K LINE’s in-house crewing units and long-term technical partnerships mitigate but do not eliminate supplier risk.

- 147,500 officer shortfall (BIMCO/ICS 2024)

- Higher crew cost share due to wage inflation and compliance

- K LINE in-house crewing + long-term partners reduce exposure

Port terminals and pilotage services

Supplier power surges - China 42%, engines >60%, 147,500 officer gap

Supplier power is high: 2024 shipbuilding share China 42%, Korea 33%, Japan 10% and top engine makers supply >60% of large two‑stroke engines, raising lead‑time and cost leverage. Ports/pilotage act as local monopolies; crew shortage (BIMCO/ICS 147,500 officers by 2025) and expensive compliance boost supplier influence. K LINE mitigation: fleet standardization, in‑house crewing, terminal stakes.

| Metric | 2024 |

|---|---|

| China shipbuilding GT | ~42% |

| Engine market (top) | >60% |

| Officer shortfall | 147,500 |

What is included in the product

Tailored Porter’s Five Forces analysis for Kawasaki Kisen Kaisha, assessing industry rivalry, buyer and supplier power, threat of new entrants and substitutes, and identifying disruptive trends and strategic levers affecting profitability.

A concise one-sheet Porter's Five Forces for Kawasaki Kisen Kaisha highlighting carrier rivalry, charterer and supplier bargaining, threat of new logistics models and regulation-driven pressures—instantly revealing operational pain points so executives can prioritize pricing, capacity and regulatory responses.

Customers Bargaining Power

Large, concentrated cargo owners

Automakers, commodity majors and global forwarders lock multi-year contracts with K LINE, using concentrated volumes to extract pricing and service concessions.

Their scale gives strong negotiating leverage, forcing demands for reliability, real-time visibility and demonstrable ESG performance.

K LINE must compete on total value—integrated logistics, carbon reporting and uptime—not on rate alone.

Price transparency and tendering

Spot indices such as the SCFI (down ~65% from the 2021 peak to 2024) and the FBX (avg ~US$1,200/FEU in 2024) raise rate transparency across trades, empowering shippers in negotiations. Annual tenders force carriers into head-to-head pricing, squeezing margins, while buyers routinely split volumes across 2–4 carriers to optimize cost and reliability. K LINE reported group revenue of about ¥1.1 trillion (FY2023), and its diversified segments partly buffer spot volatility.

Switching costs are moderate

For containers and dry bulk buyers can reallocate volumes relatively quickly, keeping switching costs moderate; K LINE's global fleet exceeds 300 vessels in 2024, enabling flexible redeployment. Specialized car carriers and LNG trades require tailored specs and charters, though alternatives remain competitive. Service differentiation and network fit raise customer stickiness. K LINE leverages schedule reliability and technical expertise to retain accounts.

Service-level and ESG requirements

Buyers demand lower emissions, digital tracking and just-in-time deliveries, raising compliance costs and operational complexity for carriers; missed KPIs can trigger penalties or lost volumes. K Line has a net-zero by 2050 commitment and published a decarbonization roadmap, which helps defend pricing power by signaling capability to meet ESG and service-level demands.

Forwarders as sophisticated intermediaries

Global 3PLs aggregate demand across shippers—the 3PL market was about $1.2 trillion in 2024—and manage multi‑carrier capacity, using advanced analytics that sharpen negotiation power and yield better rates. These intermediaries can reallocate bookings quickly in response to spot rates and disruptions, forcing carriers to bid for allocations. K LINE must offer competitive contract terms plus transparent performance data to secure volume and slot priority.

- 3PL market size: $1.2 trillion (2024)

- Top 10 3PLs: ~40% market share

- Rapid rebooking capability: leverages multi‑carrier pools

- K LINE responses: competitive contracts and performance reporting

Shippers gain bargaining power as spot rates fall; carriers focus on decarbonized logistics

Large automakers, commodity majors and global forwarders leverage concentrated volumes and annual tenders to extract pricing and service concessions from K LINE.

Spot index transparency (SCFI down ~65% from 2021 peak to 2024; FBX ~US$1,200/FEU in 2024) and 3PL analytics amplify buyer negotiation power.

K LINE (group revenue ~¥1.1 trillion FY2023; fleet >300 vessels in 2024) competes on integrated logistics, reliability and decarbonization (net‑zero by 2050), not rate alone.

| Metric | 2024 / Latest |

|---|---|

| SCFI change | -65% vs 2021 peak |

| FBX avg | ~US$1,200/FEU |

| 3PL market | ~US$1.2T |

| K LINE revenue | ¥1.1T (FY2023) |

| Fleet size | >300 vessels |

Same Document Delivered

Kawasaki Kisen Kaisha Porter's Five Forces Analysis

This Porter's Five Forces analysis of Kawasaki Kisen Kaisha assesses industry rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to inform strategic decisions. The document you see is the same professionally written analysis you'll receive—fully formatted and ready to use. Purchase grants instant access to this exact file.

Don't Miss the Bigger Picture

Kawasaki Kisen Kaisha faces intense rivalry, evolving buyer power, and supply-chain pressures that shape its freight and logistics margins; regulatory and technological shifts add strategic urgency. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kawasaki Kisen Kaisha’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated shipbuilders and engine makers

Global shipbuilding capacity is highly concentrated: in 2024 China ~42% of GT, Korea ~33% and Japan ~10%, giving major yards leverage on pricing and delivery slots; top marine engine makers (MAN Energy, WinGD, Wartsila) supply a majority of large two‑stroke engines (~60%+). For K LINE, switching core vessel/engine suppliers is slow and costly, often adding months and higher capex, while newbuild lead times of 18–36 months and engine lead times of 12–24 months can squeeze retrofit and delivery schedules.

Fuel and bunker suppliers’ pricing power

Marine fuel markets remain highly volatile, driven by OPEC+ production moves, geopolitics and refining capacity constraints; benchmark-led bunker prices can spike sharply during supply disruptions despite a competitive supplier base at major hubs. The shift to compliance fuels (VLSFO, MGO) and growing LNG bunkering increases sourcing complexity and premium risk. K LINE’s scale supports competitive tenders and hedging programs, but does not fully insulate it from sudden price shocks.

Specialized equipment and digital systems

Ballast water treatment units, exhaust scrubbers, LNG fuel systems and voyage-optimization software are sourced from specialized vendors, with BWTS retrofit typically $0.5–1.5M, scrubbers $2–5M and LNG premiums often $10–20M, while software runs ~$10k–50k/vessel/year (2024 industry ranges). Certification and complex integration raise switching costs; vendors leverage power through maintenance contracts and update cycles that capture recurring revenue. K LINE reduces supplier leverage via fleet standardization and multi-sourcing where feasible.

Crewing and technical services constraints

Qualified seafarers, especially for LNG and advanced ships, remain scarce; BIMCO/ICS 2024 projects an officer shortfall of about 147,500 by 2025. Training, safety and STCW compliance heighten dependence on manning and technical managers, while wage inflation and rising compliance costs push crew-related operating expenses up. K LINE’s in-house crewing units and long-term technical partnerships mitigate but do not eliminate supplier risk.

- 147,500 officer shortfall (BIMCO/ICS 2024)

- Higher crew cost share due to wage inflation and compliance

- K LINE in-house crewing + long-term partners reduce exposure

Port terminals and pilotage services

Supplier power surges - China 42%, engines >60%, 147,500 officer gap

Supplier power is high: 2024 shipbuilding share China 42%, Korea 33%, Japan 10% and top engine makers supply >60% of large two‑stroke engines, raising lead‑time and cost leverage. Ports/pilotage act as local monopolies; crew shortage (BIMCO/ICS 147,500 officers by 2025) and expensive compliance boost supplier influence. K LINE mitigation: fleet standardization, in‑house crewing, terminal stakes.

| Metric | 2024 |

|---|---|

| China shipbuilding GT | ~42% |

| Engine market (top) | >60% |

| Officer shortfall | 147,500 |

What is included in the product

Tailored Porter’s Five Forces analysis for Kawasaki Kisen Kaisha, assessing industry rivalry, buyer and supplier power, threat of new entrants and substitutes, and identifying disruptive trends and strategic levers affecting profitability.

A concise one-sheet Porter's Five Forces for Kawasaki Kisen Kaisha highlighting carrier rivalry, charterer and supplier bargaining, threat of new logistics models and regulation-driven pressures—instantly revealing operational pain points so executives can prioritize pricing, capacity and regulatory responses.

Customers Bargaining Power

Large, concentrated cargo owners

Automakers, commodity majors and global forwarders lock multi-year contracts with K LINE, using concentrated volumes to extract pricing and service concessions.

Their scale gives strong negotiating leverage, forcing demands for reliability, real-time visibility and demonstrable ESG performance.

K LINE must compete on total value—integrated logistics, carbon reporting and uptime—not on rate alone.

Price transparency and tendering

Spot indices such as the SCFI (down ~65% from the 2021 peak to 2024) and the FBX (avg ~US$1,200/FEU in 2024) raise rate transparency across trades, empowering shippers in negotiations. Annual tenders force carriers into head-to-head pricing, squeezing margins, while buyers routinely split volumes across 2–4 carriers to optimize cost and reliability. K LINE reported group revenue of about ¥1.1 trillion (FY2023), and its diversified segments partly buffer spot volatility.

Switching costs are moderate

For containers and dry bulk buyers can reallocate volumes relatively quickly, keeping switching costs moderate; K LINE's global fleet exceeds 300 vessels in 2024, enabling flexible redeployment. Specialized car carriers and LNG trades require tailored specs and charters, though alternatives remain competitive. Service differentiation and network fit raise customer stickiness. K LINE leverages schedule reliability and technical expertise to retain accounts.

Service-level and ESG requirements

Buyers demand lower emissions, digital tracking and just-in-time deliveries, raising compliance costs and operational complexity for carriers; missed KPIs can trigger penalties or lost volumes. K Line has a net-zero by 2050 commitment and published a decarbonization roadmap, which helps defend pricing power by signaling capability to meet ESG and service-level demands.

Forwarders as sophisticated intermediaries

Global 3PLs aggregate demand across shippers—the 3PL market was about $1.2 trillion in 2024—and manage multi‑carrier capacity, using advanced analytics that sharpen negotiation power and yield better rates. These intermediaries can reallocate bookings quickly in response to spot rates and disruptions, forcing carriers to bid for allocations. K LINE must offer competitive contract terms plus transparent performance data to secure volume and slot priority.

- 3PL market size: $1.2 trillion (2024)

- Top 10 3PLs: ~40% market share

- Rapid rebooking capability: leverages multi‑carrier pools

- K LINE responses: competitive contracts and performance reporting

Shippers gain bargaining power as spot rates fall; carriers focus on decarbonized logistics

Large automakers, commodity majors and global forwarders leverage concentrated volumes and annual tenders to extract pricing and service concessions from K LINE.

Spot index transparency (SCFI down ~65% from 2021 peak to 2024; FBX ~US$1,200/FEU in 2024) and 3PL analytics amplify buyer negotiation power.

K LINE (group revenue ~¥1.1 trillion FY2023; fleet >300 vessels in 2024) competes on integrated logistics, reliability and decarbonization (net‑zero by 2050), not rate alone.

| Metric | 2024 / Latest |

|---|---|

| SCFI change | -65% vs 2021 peak |

| FBX avg | ~US$1,200/FEU |

| 3PL market | ~US$1.2T |

| K LINE revenue | ¥1.1T (FY2023) |

| Fleet size | >300 vessels |

Same Document Delivered

Kawasaki Kisen Kaisha Porter's Five Forces Analysis

This Porter's Five Forces analysis of Kawasaki Kisen Kaisha assesses industry rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to inform strategic decisions. The document you see is the same professionally written analysis you'll receive—fully formatted and ready to use. Purchase grants instant access to this exact file.

Description

Don't Miss the Bigger Picture

Kawasaki Kisen Kaisha faces intense rivalry, evolving buyer power, and supply-chain pressures that shape its freight and logistics margins; regulatory and technological shifts add strategic urgency. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Kawasaki Kisen Kaisha’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated shipbuilders and engine makers

Global shipbuilding capacity is highly concentrated: in 2024 China ~42% of GT, Korea ~33% and Japan ~10%, giving major yards leverage on pricing and delivery slots; top marine engine makers (MAN Energy, WinGD, Wartsila) supply a majority of large two‑stroke engines (~60%+). For K LINE, switching core vessel/engine suppliers is slow and costly, often adding months and higher capex, while newbuild lead times of 18–36 months and engine lead times of 12–24 months can squeeze retrofit and delivery schedules.

Fuel and bunker suppliers’ pricing power

Marine fuel markets remain highly volatile, driven by OPEC+ production moves, geopolitics and refining capacity constraints; benchmark-led bunker prices can spike sharply during supply disruptions despite a competitive supplier base at major hubs. The shift to compliance fuels (VLSFO, MGO) and growing LNG bunkering increases sourcing complexity and premium risk. K LINE’s scale supports competitive tenders and hedging programs, but does not fully insulate it from sudden price shocks.

Specialized equipment and digital systems

Ballast water treatment units, exhaust scrubbers, LNG fuel systems and voyage-optimization software are sourced from specialized vendors, with BWTS retrofit typically $0.5–1.5M, scrubbers $2–5M and LNG premiums often $10–20M, while software runs ~$10k–50k/vessel/year (2024 industry ranges). Certification and complex integration raise switching costs; vendors leverage power through maintenance contracts and update cycles that capture recurring revenue. K LINE reduces supplier leverage via fleet standardization and multi-sourcing where feasible.

Crewing and technical services constraints

Qualified seafarers, especially for LNG and advanced ships, remain scarce; BIMCO/ICS 2024 projects an officer shortfall of about 147,500 by 2025. Training, safety and STCW compliance heighten dependence on manning and technical managers, while wage inflation and rising compliance costs push crew-related operating expenses up. K LINE’s in-house crewing units and long-term technical partnerships mitigate but do not eliminate supplier risk.

- 147,500 officer shortfall (BIMCO/ICS 2024)

- Higher crew cost share due to wage inflation and compliance

- K LINE in-house crewing + long-term partners reduce exposure

Port terminals and pilotage services

Supplier power surges - China 42%, engines >60%, 147,500 officer gap

Supplier power is high: 2024 shipbuilding share China 42%, Korea 33%, Japan 10% and top engine makers supply >60% of large two‑stroke engines, raising lead‑time and cost leverage. Ports/pilotage act as local monopolies; crew shortage (BIMCO/ICS 147,500 officers by 2025) and expensive compliance boost supplier influence. K LINE mitigation: fleet standardization, in‑house crewing, terminal stakes.

| Metric | 2024 |

|---|---|

| China shipbuilding GT | ~42% |

| Engine market (top) | >60% |

| Officer shortfall | 147,500 |

What is included in the product

Tailored Porter’s Five Forces analysis for Kawasaki Kisen Kaisha, assessing industry rivalry, buyer and supplier power, threat of new entrants and substitutes, and identifying disruptive trends and strategic levers affecting profitability.

A concise one-sheet Porter's Five Forces for Kawasaki Kisen Kaisha highlighting carrier rivalry, charterer and supplier bargaining, threat of new logistics models and regulation-driven pressures—instantly revealing operational pain points so executives can prioritize pricing, capacity and regulatory responses.

Customers Bargaining Power

Large, concentrated cargo owners

Automakers, commodity majors and global forwarders lock multi-year contracts with K LINE, using concentrated volumes to extract pricing and service concessions.

Their scale gives strong negotiating leverage, forcing demands for reliability, real-time visibility and demonstrable ESG performance.

K LINE must compete on total value—integrated logistics, carbon reporting and uptime—not on rate alone.

Price transparency and tendering

Spot indices such as the SCFI (down ~65% from the 2021 peak to 2024) and the FBX (avg ~US$1,200/FEU in 2024) raise rate transparency across trades, empowering shippers in negotiations. Annual tenders force carriers into head-to-head pricing, squeezing margins, while buyers routinely split volumes across 2–4 carriers to optimize cost and reliability. K LINE reported group revenue of about ¥1.1 trillion (FY2023), and its diversified segments partly buffer spot volatility.

Switching costs are moderate

For containers and dry bulk buyers can reallocate volumes relatively quickly, keeping switching costs moderate; K LINE's global fleet exceeds 300 vessels in 2024, enabling flexible redeployment. Specialized car carriers and LNG trades require tailored specs and charters, though alternatives remain competitive. Service differentiation and network fit raise customer stickiness. K LINE leverages schedule reliability and technical expertise to retain accounts.

Service-level and ESG requirements

Buyers demand lower emissions, digital tracking and just-in-time deliveries, raising compliance costs and operational complexity for carriers; missed KPIs can trigger penalties or lost volumes. K Line has a net-zero by 2050 commitment and published a decarbonization roadmap, which helps defend pricing power by signaling capability to meet ESG and service-level demands.

Forwarders as sophisticated intermediaries

Global 3PLs aggregate demand across shippers—the 3PL market was about $1.2 trillion in 2024—and manage multi‑carrier capacity, using advanced analytics that sharpen negotiation power and yield better rates. These intermediaries can reallocate bookings quickly in response to spot rates and disruptions, forcing carriers to bid for allocations. K LINE must offer competitive contract terms plus transparent performance data to secure volume and slot priority.

- 3PL market size: $1.2 trillion (2024)

- Top 10 3PLs: ~40% market share

- Rapid rebooking capability: leverages multi‑carrier pools

- K LINE responses: competitive contracts and performance reporting

Shippers gain bargaining power as spot rates fall; carriers focus on decarbonized logistics

Large automakers, commodity majors and global forwarders leverage concentrated volumes and annual tenders to extract pricing and service concessions from K LINE.

Spot index transparency (SCFI down ~65% from 2021 peak to 2024; FBX ~US$1,200/FEU in 2024) and 3PL analytics amplify buyer negotiation power.

K LINE (group revenue ~¥1.1 trillion FY2023; fleet >300 vessels in 2024) competes on integrated logistics, reliability and decarbonization (net‑zero by 2050), not rate alone.

| Metric | 2024 / Latest |

|---|---|

| SCFI change | -65% vs 2021 peak |

| FBX avg | ~US$1,200/FEU |

| 3PL market | ~US$1.2T |

| K LINE revenue | ¥1.1T (FY2023) |

| Fleet size | >300 vessels |

Same Document Delivered

Kawasaki Kisen Kaisha Porter's Five Forces Analysis

This Porter's Five Forces analysis of Kawasaki Kisen Kaisha assesses industry rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to inform strategic decisions. The document you see is the same professionally written analysis you'll receive—fully formatted and ready to use. Purchase grants instant access to this exact file.