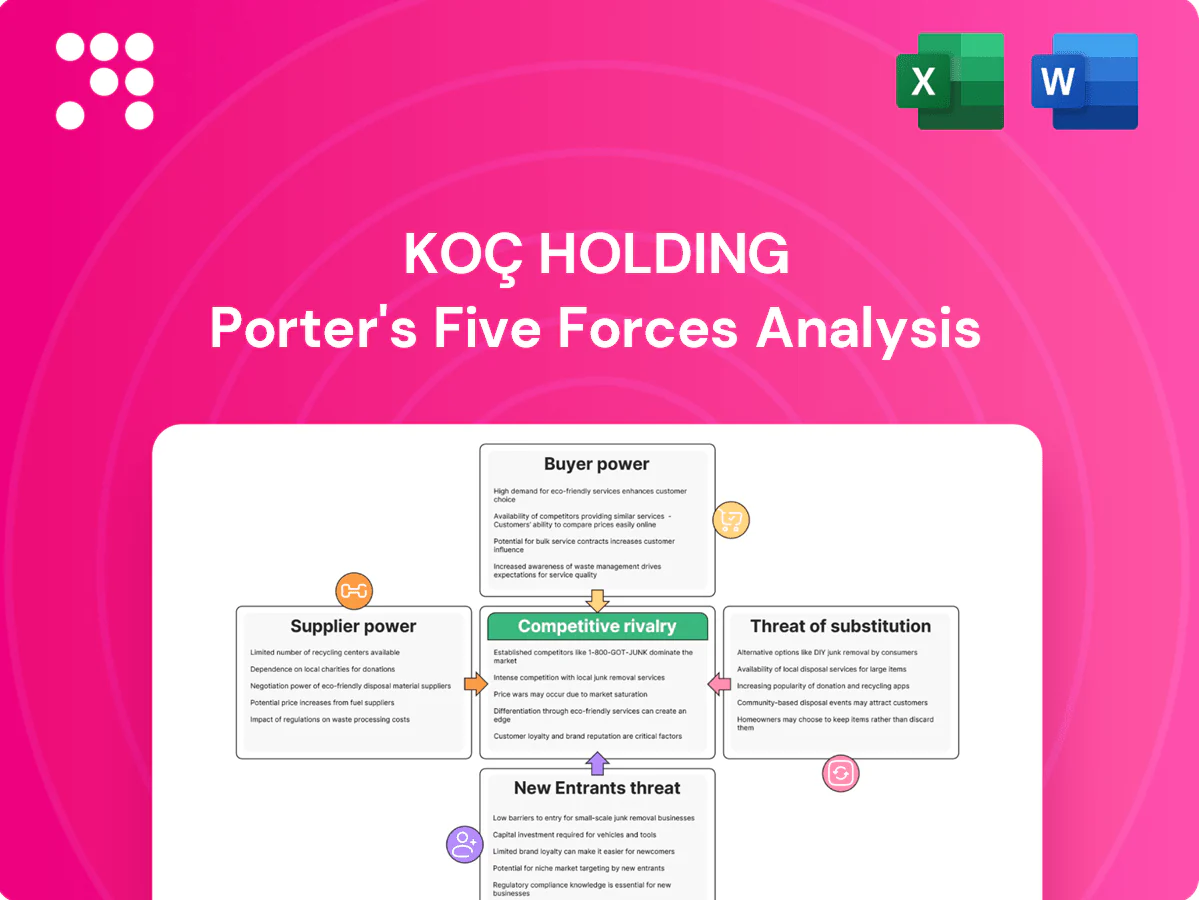

Koç Holding Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Koç Holding faces moderate supplier power, diverse buyer segments, and significant rivalry across energy, automotive and consumer sectors, while barriers to entry and substitutes vary by division; macroeconomic sensitivity and regulatory shifts shape strategic risk. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Critical inputs concentration

Koç’s energy and automotive units depend on concentrated suppliers for crude, petrochemicals and semiconductors, where TSMC and Samsung together held ~70% of global foundry capacity in 2023–24, raising switching costs and delivery timelines; major oil exporters/OPEC+ supplied roughly 40% of global crude, giving upstream players pricing leverage. Koç reduces risk through multi-sourcing and JV-backed procurement scale.

Scale-driven bargaining

As Turkey’s largest conglomerate with over 200 subsidiaries and roughly 100,000 employees, Koç aggregates demand to secure volume discounts and long-term contracts, reducing supplier bargaining power.

Vendor-managed inventory and category management, plus global sourcing hubs, improve price discovery and cost control.

Scale offsets much supplier leverage but niche technology vendors retain premium pricing power.

Technology and IP dependency

Automotive platforms, white goods components and energy equipment commonly embed supplier IP, creating design lock-ins and certification hurdles that raise switching costs for Koç Holding's business units. Firmware, software and proprietary tooling further extend supplier influence beyond physical parts. To dilute dependency Koç scales in-house R&D and pursues co-development partnerships across its automotive, durable goods and energy affiliates.

Regulatory and geopolitical exposure

Sustainability and compliance demands

Rising ESG standards—notably EU CSRD implementation from 2024 expanding Scope 3 and traceability demands—shrink compliant supplier pools, letting certified inputs command price premiums and stricter contract terms. Suppliers with verified green credentials gain measurable negotiating leverage, while Koç Holding uses supplier development and capacity-building programs to broaden the compliant base.

- Impact: narrower supplier pool

- Driver: CSRD 2024 expands Scope 3 reporting

- Response: Koç supplier development

Concentrated chip and oil suppliers boost pricing power; Turkey sees energy import and FX pressure

Concentrated suppliers in semiconductors (TSMC+Samsung ~70% foundry 2023–24) and oil (OPEC+ ~40% crude) raise switching costs and pricing leverage; Koç offsets via multi-sourcing, JVs and in‑house R&D. Turkey’s ~75% energy import dependence (2023) and TRY ~40% depreciation (2021–2023) amplify input cost risk. ESG rules (CSRD 2024) narrow compliant supplier pools, prompting supplier development programs.

| Metric | Value |

|---|---|

| Foundry share (TSMC+Samsung) | ~70% (2023–24) |

| OPEC+ crude share | ~40% |

| Turkey energy imports | ~75% (2023) |

| TRY depreciation | ~40% (2021–2023) |

What is included in the product

Tailored Porter's Five Forces analysis for Koç Holding revealing competitive intensity, supplier and buyer power, entry barriers, and substitute threats, plus strategic insights on disruptive forces and market vulnerabilities.

A concise one-sheet Porter’s Five Forces for Koç Holding—customizable pressure levels and a radar chart for instant strategic clarity, ready to drop into decks.

Customers Bargaining Power

Diverse customer mix

Koç serves retail consumers, fleets, industrials and financial clients, diluting single-segment buyer power while exposing the group to varied negotiation dynamics in 2024. Large B2B accounts and dealer networks retain leverage to secure price and service concessions, especially in automotive and commercial sales. Consumer durables and fuel retail remain highly price-sensitive at the end-user level. Portfolio diversity buffers cyclical bargaining swings across sectors.

Price transparency and switching

In fuels and durables, frequent price comparisons intensify buyer leverage as omnichannel retailing and e-commerce improve discoverability of cheaper alternatives. Switching costs remain moderate across many categories, rising only where service networks and warranties are critical. Koç mitigates pressure through strong brands, loyalty programs and bundled services that raise effective retention.

Institutional buyers in autos

Institutional buyers—fleets and government tenders—consolidate demand and bid aggressively, squeezing OEM margins as fleet purchases drove roughly 15% of Turkey’s new vehicle registrations in 2024; specification-based procurement further compresses price leverage by rewarding exact compliance. After-sales packages and TCO propositions shift negotiations from upfront price to lifecycle value, while multi-year maintenance contracts lock in revenue streams and increase customer switching costs.

Financial services sophistication

Corporate and affluent clients demand bespoke rates, fees and advanced digital features, increasing negotiating leverage; competition from fintechs and challenger banks intensifies price and service pressure on Koç Holding’s finance affiliates. Cross-selling within Koç’s ecosystem raises switching costs, while data-driven pricing and risk models help preserve spreads and mitigate margin erosion.

- Customer sophistication: tailored pricing

- Competitive pressure: fintechs + banks

- Ecosystem: higher switching costs

- Protection: data-driven pricing & risk models

ESG and quality expectations

Buyers increasingly demand energy efficiency, low emissions and responsible sourcing, shifting negotiation power toward firms that can demonstrate ESG credentials.

Failure to meet standards risks customer churn and discount pressure; the EU carbon border adjustment mechanism scheduled for full application from 2026 raises compliance costs for suppliers.

Superior ESG performance can secure premiums and loyalty; Koç is a constituent of the BIST Sustainability Index and has a net-zero by 2050 target, allowing its sustainability investments to tilt buyer power in its favor.

- Buyers: demand energy efficiency, low emissions, responsible sourcing

- Risk: EU CBAM 2026 increases penalty for non-compliance

- Koç: BIST Sustainability Index constituent; net-zero by 2050

Moderate-to-high buyer power; data pricing and ESG protect margins (fleet 15%, net-zero 2050)

Koç faces moderate-to-high buyer power: large B2B fleets and dealers negotiate hard while retail customers remain price-sensitive across fuels and durables. Ecosystem cross-selling, brands and data-driven pricing raise switching costs and protect margins. ESG credentials and net-zero commitments shift leverage toward compliant suppliers and can secure premiums.

| Metric | Value |

|---|---|

| Fleet share 2024 | 15% |

| BIST Sustain. Index | Constituent |

| Net-zero target | 2050 |

What You See Is What You Get

Koç Holding Porter's Five Forces Analysis

This Porter's Five Forces analysis of Koç Holding is the exact document you'll receive after purchase—fully formatted and ready to use. It evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights tailored to Koç Holding's diversified conglomerate structure.

Don't Miss the Bigger Picture

Koç Holding faces moderate supplier power, diverse buyer segments, and significant rivalry across energy, automotive and consumer sectors, while barriers to entry and substitutes vary by division; macroeconomic sensitivity and regulatory shifts shape strategic risk. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Critical inputs concentration

Koç’s energy and automotive units depend on concentrated suppliers for crude, petrochemicals and semiconductors, where TSMC and Samsung together held ~70% of global foundry capacity in 2023–24, raising switching costs and delivery timelines; major oil exporters/OPEC+ supplied roughly 40% of global crude, giving upstream players pricing leverage. Koç reduces risk through multi-sourcing and JV-backed procurement scale.

Scale-driven bargaining

As Turkey’s largest conglomerate with over 200 subsidiaries and roughly 100,000 employees, Koç aggregates demand to secure volume discounts and long-term contracts, reducing supplier bargaining power.

Vendor-managed inventory and category management, plus global sourcing hubs, improve price discovery and cost control.

Scale offsets much supplier leverage but niche technology vendors retain premium pricing power.

Technology and IP dependency

Automotive platforms, white goods components and energy equipment commonly embed supplier IP, creating design lock-ins and certification hurdles that raise switching costs for Koç Holding's business units. Firmware, software and proprietary tooling further extend supplier influence beyond physical parts. To dilute dependency Koç scales in-house R&D and pursues co-development partnerships across its automotive, durable goods and energy affiliates.

Regulatory and geopolitical exposure

Sustainability and compliance demands

Rising ESG standards—notably EU CSRD implementation from 2024 expanding Scope 3 and traceability demands—shrink compliant supplier pools, letting certified inputs command price premiums and stricter contract terms. Suppliers with verified green credentials gain measurable negotiating leverage, while Koç Holding uses supplier development and capacity-building programs to broaden the compliant base.

- Impact: narrower supplier pool

- Driver: CSRD 2024 expands Scope 3 reporting

- Response: Koç supplier development

Concentrated chip and oil suppliers boost pricing power; Turkey sees energy import and FX pressure

Concentrated suppliers in semiconductors (TSMC+Samsung ~70% foundry 2023–24) and oil (OPEC+ ~40% crude) raise switching costs and pricing leverage; Koç offsets via multi-sourcing, JVs and in‑house R&D. Turkey’s ~75% energy import dependence (2023) and TRY ~40% depreciation (2021–2023) amplify input cost risk. ESG rules (CSRD 2024) narrow compliant supplier pools, prompting supplier development programs.

| Metric | Value |

|---|---|

| Foundry share (TSMC+Samsung) | ~70% (2023–24) |

| OPEC+ crude share | ~40% |

| Turkey energy imports | ~75% (2023) |

| TRY depreciation | ~40% (2021–2023) |

What is included in the product

Tailored Porter's Five Forces analysis for Koç Holding revealing competitive intensity, supplier and buyer power, entry barriers, and substitute threats, plus strategic insights on disruptive forces and market vulnerabilities.

A concise one-sheet Porter’s Five Forces for Koç Holding—customizable pressure levels and a radar chart for instant strategic clarity, ready to drop into decks.

Customers Bargaining Power

Diverse customer mix

Koç serves retail consumers, fleets, industrials and financial clients, diluting single-segment buyer power while exposing the group to varied negotiation dynamics in 2024. Large B2B accounts and dealer networks retain leverage to secure price and service concessions, especially in automotive and commercial sales. Consumer durables and fuel retail remain highly price-sensitive at the end-user level. Portfolio diversity buffers cyclical bargaining swings across sectors.

Price transparency and switching

In fuels and durables, frequent price comparisons intensify buyer leverage as omnichannel retailing and e-commerce improve discoverability of cheaper alternatives. Switching costs remain moderate across many categories, rising only where service networks and warranties are critical. Koç mitigates pressure through strong brands, loyalty programs and bundled services that raise effective retention.

Institutional buyers in autos

Institutional buyers—fleets and government tenders—consolidate demand and bid aggressively, squeezing OEM margins as fleet purchases drove roughly 15% of Turkey’s new vehicle registrations in 2024; specification-based procurement further compresses price leverage by rewarding exact compliance. After-sales packages and TCO propositions shift negotiations from upfront price to lifecycle value, while multi-year maintenance contracts lock in revenue streams and increase customer switching costs.

Financial services sophistication

Corporate and affluent clients demand bespoke rates, fees and advanced digital features, increasing negotiating leverage; competition from fintechs and challenger banks intensifies price and service pressure on Koç Holding’s finance affiliates. Cross-selling within Koç’s ecosystem raises switching costs, while data-driven pricing and risk models help preserve spreads and mitigate margin erosion.

- Customer sophistication: tailored pricing

- Competitive pressure: fintechs + banks

- Ecosystem: higher switching costs

- Protection: data-driven pricing & risk models

ESG and quality expectations

Buyers increasingly demand energy efficiency, low emissions and responsible sourcing, shifting negotiation power toward firms that can demonstrate ESG credentials.

Failure to meet standards risks customer churn and discount pressure; the EU carbon border adjustment mechanism scheduled for full application from 2026 raises compliance costs for suppliers.

Superior ESG performance can secure premiums and loyalty; Koç is a constituent of the BIST Sustainability Index and has a net-zero by 2050 target, allowing its sustainability investments to tilt buyer power in its favor.

- Buyers: demand energy efficiency, low emissions, responsible sourcing

- Risk: EU CBAM 2026 increases penalty for non-compliance

- Koç: BIST Sustainability Index constituent; net-zero by 2050

Moderate-to-high buyer power; data pricing and ESG protect margins (fleet 15%, net-zero 2050)

Koç faces moderate-to-high buyer power: large B2B fleets and dealers negotiate hard while retail customers remain price-sensitive across fuels and durables. Ecosystem cross-selling, brands and data-driven pricing raise switching costs and protect margins. ESG credentials and net-zero commitments shift leverage toward compliant suppliers and can secure premiums.

| Metric | Value |

|---|---|

| Fleet share 2024 | 15% |

| BIST Sustain. Index | Constituent |

| Net-zero target | 2050 |

What You See Is What You Get

Koç Holding Porter's Five Forces Analysis

This Porter's Five Forces analysis of Koç Holding is the exact document you'll receive after purchase—fully formatted and ready to use. It evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights tailored to Koç Holding's diversified conglomerate structure.

Description

Don't Miss the Bigger Picture

Koç Holding faces moderate supplier power, diverse buyer segments, and significant rivalry across energy, automotive and consumer sectors, while barriers to entry and substitutes vary by division; macroeconomic sensitivity and regulatory shifts shape strategic risk. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Critical inputs concentration

Koç’s energy and automotive units depend on concentrated suppliers for crude, petrochemicals and semiconductors, where TSMC and Samsung together held ~70% of global foundry capacity in 2023–24, raising switching costs and delivery timelines; major oil exporters/OPEC+ supplied roughly 40% of global crude, giving upstream players pricing leverage. Koç reduces risk through multi-sourcing and JV-backed procurement scale.

Scale-driven bargaining

As Turkey’s largest conglomerate with over 200 subsidiaries and roughly 100,000 employees, Koç aggregates demand to secure volume discounts and long-term contracts, reducing supplier bargaining power.

Vendor-managed inventory and category management, plus global sourcing hubs, improve price discovery and cost control.

Scale offsets much supplier leverage but niche technology vendors retain premium pricing power.

Technology and IP dependency

Automotive platforms, white goods components and energy equipment commonly embed supplier IP, creating design lock-ins and certification hurdles that raise switching costs for Koç Holding's business units. Firmware, software and proprietary tooling further extend supplier influence beyond physical parts. To dilute dependency Koç scales in-house R&D and pursues co-development partnerships across its automotive, durable goods and energy affiliates.

Regulatory and geopolitical exposure

Sustainability and compliance demands

Rising ESG standards—notably EU CSRD implementation from 2024 expanding Scope 3 and traceability demands—shrink compliant supplier pools, letting certified inputs command price premiums and stricter contract terms. Suppliers with verified green credentials gain measurable negotiating leverage, while Koç Holding uses supplier development and capacity-building programs to broaden the compliant base.

- Impact: narrower supplier pool

- Driver: CSRD 2024 expands Scope 3 reporting

- Response: Koç supplier development

Concentrated chip and oil suppliers boost pricing power; Turkey sees energy import and FX pressure

Concentrated suppliers in semiconductors (TSMC+Samsung ~70% foundry 2023–24) and oil (OPEC+ ~40% crude) raise switching costs and pricing leverage; Koç offsets via multi-sourcing, JVs and in‑house R&D. Turkey’s ~75% energy import dependence (2023) and TRY ~40% depreciation (2021–2023) amplify input cost risk. ESG rules (CSRD 2024) narrow compliant supplier pools, prompting supplier development programs.

| Metric | Value |

|---|---|

| Foundry share (TSMC+Samsung) | ~70% (2023–24) |

| OPEC+ crude share | ~40% |

| Turkey energy imports | ~75% (2023) |

| TRY depreciation | ~40% (2021–2023) |

What is included in the product

Tailored Porter's Five Forces analysis for Koç Holding revealing competitive intensity, supplier and buyer power, entry barriers, and substitute threats, plus strategic insights on disruptive forces and market vulnerabilities.

A concise one-sheet Porter’s Five Forces for Koç Holding—customizable pressure levels and a radar chart for instant strategic clarity, ready to drop into decks.

Customers Bargaining Power

Diverse customer mix

Koç serves retail consumers, fleets, industrials and financial clients, diluting single-segment buyer power while exposing the group to varied negotiation dynamics in 2024. Large B2B accounts and dealer networks retain leverage to secure price and service concessions, especially in automotive and commercial sales. Consumer durables and fuel retail remain highly price-sensitive at the end-user level. Portfolio diversity buffers cyclical bargaining swings across sectors.

Price transparency and switching

In fuels and durables, frequent price comparisons intensify buyer leverage as omnichannel retailing and e-commerce improve discoverability of cheaper alternatives. Switching costs remain moderate across many categories, rising only where service networks and warranties are critical. Koç mitigates pressure through strong brands, loyalty programs and bundled services that raise effective retention.

Institutional buyers in autos

Institutional buyers—fleets and government tenders—consolidate demand and bid aggressively, squeezing OEM margins as fleet purchases drove roughly 15% of Turkey’s new vehicle registrations in 2024; specification-based procurement further compresses price leverage by rewarding exact compliance. After-sales packages and TCO propositions shift negotiations from upfront price to lifecycle value, while multi-year maintenance contracts lock in revenue streams and increase customer switching costs.

Financial services sophistication

Corporate and affluent clients demand bespoke rates, fees and advanced digital features, increasing negotiating leverage; competition from fintechs and challenger banks intensifies price and service pressure on Koç Holding’s finance affiliates. Cross-selling within Koç’s ecosystem raises switching costs, while data-driven pricing and risk models help preserve spreads and mitigate margin erosion.

- Customer sophistication: tailored pricing

- Competitive pressure: fintechs + banks

- Ecosystem: higher switching costs

- Protection: data-driven pricing & risk models

ESG and quality expectations

Buyers increasingly demand energy efficiency, low emissions and responsible sourcing, shifting negotiation power toward firms that can demonstrate ESG credentials.

Failure to meet standards risks customer churn and discount pressure; the EU carbon border adjustment mechanism scheduled for full application from 2026 raises compliance costs for suppliers.

Superior ESG performance can secure premiums and loyalty; Koç is a constituent of the BIST Sustainability Index and has a net-zero by 2050 target, allowing its sustainability investments to tilt buyer power in its favor.

- Buyers: demand energy efficiency, low emissions, responsible sourcing

- Risk: EU CBAM 2026 increases penalty for non-compliance

- Koç: BIST Sustainability Index constituent; net-zero by 2050

Moderate-to-high buyer power; data pricing and ESG protect margins (fleet 15%, net-zero 2050)

Koç faces moderate-to-high buyer power: large B2B fleets and dealers negotiate hard while retail customers remain price-sensitive across fuels and durables. Ecosystem cross-selling, brands and data-driven pricing raise switching costs and protect margins. ESG credentials and net-zero commitments shift leverage toward compliant suppliers and can secure premiums.

| Metric | Value |

|---|---|

| Fleet share 2024 | 15% |

| BIST Sustain. Index | Constituent |

| Net-zero target | 2050 |

What You See Is What You Get

Koç Holding Porter's Five Forces Analysis

This Porter's Five Forces analysis of Koç Holding is the exact document you'll receive after purchase—fully formatted and ready to use. It evaluates competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights tailored to Koç Holding's diversified conglomerate structure.