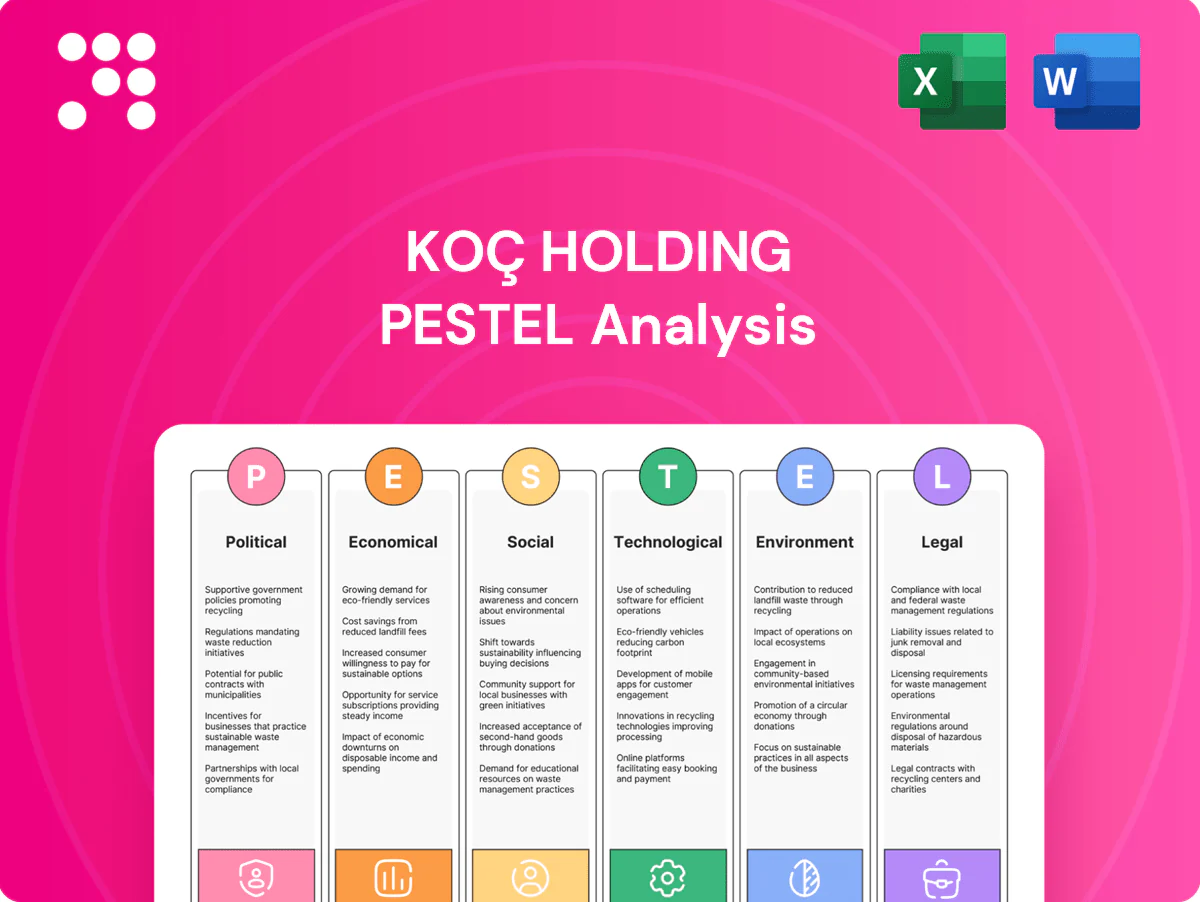

Koç Holding PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological change are reshaping Koç Holding’s strategic landscape in our concise PESTLE snapshot. This analysis highlights key external risks and growth levers to inform investment and strategy decisions. Buy the full PESTLE for an actionable, fully editable deep-dive you can use immediately.

Political factors

Regulatory volatility in Turkey

Frequent shifts in energy pricing, taxation and FX rules materially affect Koç’s margins across automotive, energy and finance businesses; Turkey imports nearly all natural gas, amplifying exposure to global price swings. State influence in strategic sectors raises compliance costs and planning complexity for Koç’s ~100,000-strong group. Scenario planning and active policy engagement are essential. Regional geopolitics and EU ties (EU ~40% of Turkish exports) affect trade and supply chains.

Government incentives and SOE dynamics

Government incentives—tax exemptions, VAT refunds and subsidized loans—can unlock capex for Koç’s automotive, appliances and energy units, supporting projects as Türkiye’s renewables capacity exceeded 60 GW by 2024.

Competition or cooperation with SOEs shapes market access, notably in energy and large-scale tenders where partnerships with state firms often determine contract wins.

Aligning with industrial policy on localization and R&D secures subsidies and tenders; close monitoring of eligibility and reporting mitigates incentive clawback risks.

EU accession framework and customs union

Turkey’s Customs Union with the EU (in force since 1995) governs tariffs, standards and market access for Koç’s industrial exports, with the EU taking about 36% of Turkish exports in 2023. Convergence with EU regulations raises compliance and certification costs but enables scale benefits across Koç’s automotive and white goods units. Any renegotiation of the union would directly affect competitiveness in automotive and white goods export markets. Diplomatic swings can quickly pressure export volumes and certifications.

Sanctions and trade restrictions

Global sanctions regimes constrain energy sourcing, banking flows and cross-border JVs, forcing Koç to tighten due diligence across treasury, procurement and M&A teams. Robust screening and transaction monitoring are essential to avoid fines and reputational damage. Rapid supply-chain rerouting is required when new restrictions emerge, while diversified markets cushion exposure but increase compliance complexity.

- Sanctions impact energy, banking, JVs

- Mandatory robust screening

- Need for rapid supply-chain rerouting

- Diversification reduces risk but raises compliance burden

Public procurement and PPP exposure

Energy, infrastructure and defense-adjacent Koç subsidiaries depend on politically overseen tenders, where public procurement pipelines can drive rapid topline growth yet concentrate political-cycle risk after elections like those held in Türkiye in 2023.

Stronger transparent governance and compliance improve bid credibility and access to PPPs, while diversified private-sector contracts smooth revenue cyclicality tied to changing administrations.

- tender dependence: accelerates growth, raises political risk

- governance: transparency boosts bid success

- diversification: private exposure reduces election cyclicality

Political shocks threaten margins: FX, gas dependence and EU export exposure

Political risks: FX, tax and energy policy swings hit margins across Koç’s ~100,000-strong group; Türkiye imports ≈98% of natural gas, amplifying exposure as renewables reached >60 GW in 2024. EU took ~36% of exports in 2023, so Customs Union dynamics and 2023 elections drive trade and tender cycles; sanctions and state influence raise compliance and procurement complexity.

| Metric | Value | Immediate Impact |

|---|---|---|

| Employees | ~100,000 | scale/HR risk |

| Natural gas import | ≈98% | price exposure |

| Renewables (2024) | >60 GW | capex opportunity |

| Exports to EU (2023) | ~36% | trade sensitivity |

What is included in the product

Explores how macro-environmental factors uniquely affect Koç Holding across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities; formatted for executives, consultants and investors to insert directly into plans, decks or reports.

A concise, visually segmented PESTLE summary for Koç Holding that simplifies external risk analysis and market positioning, making it easy to drop into presentations or share across teams for faster strategic alignment.

Economic factors

Inflation and interest rate swings

High inflation in Turkey (consumer inflation remained above 50% in 2024) and large policy-rate swings compress Koç Holding’s costs, working capital needs and damp real consumer demand. Pricing power in branded durables and fuels mitigates pass-through but lags can squeeze margins. FX-linked debt and imported input costs require active hedging amid lira volatility. Tight credit conditions have already slowed auto and appliance sales.

Currency depreciation risk

TRY depreciation—about 30% vs USD from 2022–24—inflates imported inputs and capex, squeezing manufacturing margins across Koç Holding. Export revenues in hard currency, which represent roughly 40% of group sales, provide a partial natural hedge. Volatile FX pressures asset quality and capital adequacy in its financial-services units, with loan‑to‑deposit and CAR metrics under stress. Centralized treasury and active hedging remain critical risk mitigants.

Global demand cycles

Koç’s automotive and consumer durables businesses closely track external cycles, with EU new car registrations around 10.5 million units in 2024 and MENA appliance demand growing roughly 4% y/y, exposing revenues to regional swings.

Energy throughput correlates with mobility and industrial activity—global oil product demand rose about 1.5% in 2024, affecting downstream margins.

Geographic diversification across EU, Turkey and MENA smooths shocks but raises coordination and logistics costs for Koç’s multi-business portfolio.

Improved inventory buffers and production flexibility—shorter lead times, scalable plants—have measurably reduced sales volatility for similar peers by ~20%.

Commodity and energy price volatility

- Brent ~ $88/bbl (2024) — >30% oil/gas/metals swings

- Mitigants: vertical integration, long-term contracts, dynamic pricing

- Risk focus: basis vs liquidity and counterparty concentration

Household income and credit availability

- Auto sales ~800,000 units (2024)

- Consumer loans +18% y/y (2024)

- BNPL ~5% e‑commerce share (2024)

- Segmentation increases market breadth

Political shocks threaten margins: FX, gas dependence and EU export exposure

High inflation (>50% in 2024), TRY ~-30% vs USD (2022–24) and Brent ~$88/bbl (2024) raise imported input and hedging costs, squeezing margins. Exports ~40% of group sales and centralized treasury partly hedge FX; auto sales ~800k (2024) and consumer loans +18% y/y support demand. BNPL ~5% e‑commerce share raises credit provisioning needs.

| Metric | 2024 |

|---|---|

| Inflation | >50% |

| TRY vs USD (2022–24) | -30% |

| Brent | $88/bbl |

| Exports share | ~40% |

| Auto sales | ~800k |

| Consumer loans | +18% y/y |

| BNPL | ~5% |

Same Document Delivered

Koç Holding PESTLE Analysis

This Koç Holding PESTLE Analysis provides a concise, structured review of political, economic, social, technological, legal and environmental factors affecting the group. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or surprises; you’ll download the final file immediately after payment.

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological change are reshaping Koç Holding’s strategic landscape in our concise PESTLE snapshot. This analysis highlights key external risks and growth levers to inform investment and strategy decisions. Buy the full PESTLE for an actionable, fully editable deep-dive you can use immediately.

Political factors

Regulatory volatility in Turkey

Frequent shifts in energy pricing, taxation and FX rules materially affect Koç’s margins across automotive, energy and finance businesses; Turkey imports nearly all natural gas, amplifying exposure to global price swings. State influence in strategic sectors raises compliance costs and planning complexity for Koç’s ~100,000-strong group. Scenario planning and active policy engagement are essential. Regional geopolitics and EU ties (EU ~40% of Turkish exports) affect trade and supply chains.

Government incentives and SOE dynamics

Government incentives—tax exemptions, VAT refunds and subsidized loans—can unlock capex for Koç’s automotive, appliances and energy units, supporting projects as Türkiye’s renewables capacity exceeded 60 GW by 2024.

Competition or cooperation with SOEs shapes market access, notably in energy and large-scale tenders where partnerships with state firms often determine contract wins.

Aligning with industrial policy on localization and R&D secures subsidies and tenders; close monitoring of eligibility and reporting mitigates incentive clawback risks.

EU accession framework and customs union

Turkey’s Customs Union with the EU (in force since 1995) governs tariffs, standards and market access for Koç’s industrial exports, with the EU taking about 36% of Turkish exports in 2023. Convergence with EU regulations raises compliance and certification costs but enables scale benefits across Koç’s automotive and white goods units. Any renegotiation of the union would directly affect competitiveness in automotive and white goods export markets. Diplomatic swings can quickly pressure export volumes and certifications.

Sanctions and trade restrictions

Global sanctions regimes constrain energy sourcing, banking flows and cross-border JVs, forcing Koç to tighten due diligence across treasury, procurement and M&A teams. Robust screening and transaction monitoring are essential to avoid fines and reputational damage. Rapid supply-chain rerouting is required when new restrictions emerge, while diversified markets cushion exposure but increase compliance complexity.

- Sanctions impact energy, banking, JVs

- Mandatory robust screening

- Need for rapid supply-chain rerouting

- Diversification reduces risk but raises compliance burden

Public procurement and PPP exposure

Energy, infrastructure and defense-adjacent Koç subsidiaries depend on politically overseen tenders, where public procurement pipelines can drive rapid topline growth yet concentrate political-cycle risk after elections like those held in Türkiye in 2023.

Stronger transparent governance and compliance improve bid credibility and access to PPPs, while diversified private-sector contracts smooth revenue cyclicality tied to changing administrations.

- tender dependence: accelerates growth, raises political risk

- governance: transparency boosts bid success

- diversification: private exposure reduces election cyclicality

Political shocks threaten margins: FX, gas dependence and EU export exposure

Political risks: FX, tax and energy policy swings hit margins across Koç’s ~100,000-strong group; Türkiye imports ≈98% of natural gas, amplifying exposure as renewables reached >60 GW in 2024. EU took ~36% of exports in 2023, so Customs Union dynamics and 2023 elections drive trade and tender cycles; sanctions and state influence raise compliance and procurement complexity.

| Metric | Value | Immediate Impact |

|---|---|---|

| Employees | ~100,000 | scale/HR risk |

| Natural gas import | ≈98% | price exposure |

| Renewables (2024) | >60 GW | capex opportunity |

| Exports to EU (2023) | ~36% | trade sensitivity |

What is included in the product

Explores how macro-environmental factors uniquely affect Koç Holding across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities; formatted for executives, consultants and investors to insert directly into plans, decks or reports.

A concise, visually segmented PESTLE summary for Koç Holding that simplifies external risk analysis and market positioning, making it easy to drop into presentations or share across teams for faster strategic alignment.

Economic factors

Inflation and interest rate swings

High inflation in Turkey (consumer inflation remained above 50% in 2024) and large policy-rate swings compress Koç Holding’s costs, working capital needs and damp real consumer demand. Pricing power in branded durables and fuels mitigates pass-through but lags can squeeze margins. FX-linked debt and imported input costs require active hedging amid lira volatility. Tight credit conditions have already slowed auto and appliance sales.

Currency depreciation risk

TRY depreciation—about 30% vs USD from 2022–24—inflates imported inputs and capex, squeezing manufacturing margins across Koç Holding. Export revenues in hard currency, which represent roughly 40% of group sales, provide a partial natural hedge. Volatile FX pressures asset quality and capital adequacy in its financial-services units, with loan‑to‑deposit and CAR metrics under stress. Centralized treasury and active hedging remain critical risk mitigants.

Global demand cycles

Koç’s automotive and consumer durables businesses closely track external cycles, with EU new car registrations around 10.5 million units in 2024 and MENA appliance demand growing roughly 4% y/y, exposing revenues to regional swings.

Energy throughput correlates with mobility and industrial activity—global oil product demand rose about 1.5% in 2024, affecting downstream margins.

Geographic diversification across EU, Turkey and MENA smooths shocks but raises coordination and logistics costs for Koç’s multi-business portfolio.

Improved inventory buffers and production flexibility—shorter lead times, scalable plants—have measurably reduced sales volatility for similar peers by ~20%.

Commodity and energy price volatility

- Brent ~ $88/bbl (2024) — >30% oil/gas/metals swings

- Mitigants: vertical integration, long-term contracts, dynamic pricing

- Risk focus: basis vs liquidity and counterparty concentration

Household income and credit availability

- Auto sales ~800,000 units (2024)

- Consumer loans +18% y/y (2024)

- BNPL ~5% e‑commerce share (2024)

- Segmentation increases market breadth

Political shocks threaten margins: FX, gas dependence and EU export exposure

High inflation (>50% in 2024), TRY ~-30% vs USD (2022–24) and Brent ~$88/bbl (2024) raise imported input and hedging costs, squeezing margins. Exports ~40% of group sales and centralized treasury partly hedge FX; auto sales ~800k (2024) and consumer loans +18% y/y support demand. BNPL ~5% e‑commerce share raises credit provisioning needs.

| Metric | 2024 |

|---|---|

| Inflation | >50% |

| TRY vs USD (2022–24) | -30% |

| Brent | $88/bbl |

| Exports share | ~40% |

| Auto sales | ~800k |

| Consumer loans | +18% y/y |

| BNPL | ~5% |

Same Document Delivered

Koç Holding PESTLE Analysis

This Koç Holding PESTLE Analysis provides a concise, structured review of political, economic, social, technological, legal and environmental factors affecting the group. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or surprises; you’ll download the final file immediately after payment.

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological change are reshaping Koç Holding’s strategic landscape in our concise PESTLE snapshot. This analysis highlights key external risks and growth levers to inform investment and strategy decisions. Buy the full PESTLE for an actionable, fully editable deep-dive you can use immediately.

Political factors

Regulatory volatility in Turkey

Frequent shifts in energy pricing, taxation and FX rules materially affect Koç’s margins across automotive, energy and finance businesses; Turkey imports nearly all natural gas, amplifying exposure to global price swings. State influence in strategic sectors raises compliance costs and planning complexity for Koç’s ~100,000-strong group. Scenario planning and active policy engagement are essential. Regional geopolitics and EU ties (EU ~40% of Turkish exports) affect trade and supply chains.

Government incentives and SOE dynamics

Government incentives—tax exemptions, VAT refunds and subsidized loans—can unlock capex for Koç’s automotive, appliances and energy units, supporting projects as Türkiye’s renewables capacity exceeded 60 GW by 2024.

Competition or cooperation with SOEs shapes market access, notably in energy and large-scale tenders where partnerships with state firms often determine contract wins.

Aligning with industrial policy on localization and R&D secures subsidies and tenders; close monitoring of eligibility and reporting mitigates incentive clawback risks.

EU accession framework and customs union

Turkey’s Customs Union with the EU (in force since 1995) governs tariffs, standards and market access for Koç’s industrial exports, with the EU taking about 36% of Turkish exports in 2023. Convergence with EU regulations raises compliance and certification costs but enables scale benefits across Koç’s automotive and white goods units. Any renegotiation of the union would directly affect competitiveness in automotive and white goods export markets. Diplomatic swings can quickly pressure export volumes and certifications.

Sanctions and trade restrictions

Global sanctions regimes constrain energy sourcing, banking flows and cross-border JVs, forcing Koç to tighten due diligence across treasury, procurement and M&A teams. Robust screening and transaction monitoring are essential to avoid fines and reputational damage. Rapid supply-chain rerouting is required when new restrictions emerge, while diversified markets cushion exposure but increase compliance complexity.

- Sanctions impact energy, banking, JVs

- Mandatory robust screening

- Need for rapid supply-chain rerouting

- Diversification reduces risk but raises compliance burden

Public procurement and PPP exposure

Energy, infrastructure and defense-adjacent Koç subsidiaries depend on politically overseen tenders, where public procurement pipelines can drive rapid topline growth yet concentrate political-cycle risk after elections like those held in Türkiye in 2023.

Stronger transparent governance and compliance improve bid credibility and access to PPPs, while diversified private-sector contracts smooth revenue cyclicality tied to changing administrations.

- tender dependence: accelerates growth, raises political risk

- governance: transparency boosts bid success

- diversification: private exposure reduces election cyclicality

Political shocks threaten margins: FX, gas dependence and EU export exposure

Political risks: FX, tax and energy policy swings hit margins across Koç’s ~100,000-strong group; Türkiye imports ≈98% of natural gas, amplifying exposure as renewables reached >60 GW in 2024. EU took ~36% of exports in 2023, so Customs Union dynamics and 2023 elections drive trade and tender cycles; sanctions and state influence raise compliance and procurement complexity.

| Metric | Value | Immediate Impact |

|---|---|---|

| Employees | ~100,000 | scale/HR risk |

| Natural gas import | ≈98% | price exposure |

| Renewables (2024) | >60 GW | capex opportunity |

| Exports to EU (2023) | ~36% | trade sensitivity |

What is included in the product

Explores how macro-environmental factors uniquely affect Koç Holding across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to identify threats and opportunities; formatted for executives, consultants and investors to insert directly into plans, decks or reports.

A concise, visually segmented PESTLE summary for Koç Holding that simplifies external risk analysis and market positioning, making it easy to drop into presentations or share across teams for faster strategic alignment.

Economic factors

Inflation and interest rate swings

High inflation in Turkey (consumer inflation remained above 50% in 2024) and large policy-rate swings compress Koç Holding’s costs, working capital needs and damp real consumer demand. Pricing power in branded durables and fuels mitigates pass-through but lags can squeeze margins. FX-linked debt and imported input costs require active hedging amid lira volatility. Tight credit conditions have already slowed auto and appliance sales.

Currency depreciation risk

TRY depreciation—about 30% vs USD from 2022–24—inflates imported inputs and capex, squeezing manufacturing margins across Koç Holding. Export revenues in hard currency, which represent roughly 40% of group sales, provide a partial natural hedge. Volatile FX pressures asset quality and capital adequacy in its financial-services units, with loan‑to‑deposit and CAR metrics under stress. Centralized treasury and active hedging remain critical risk mitigants.

Global demand cycles

Koç’s automotive and consumer durables businesses closely track external cycles, with EU new car registrations around 10.5 million units in 2024 and MENA appliance demand growing roughly 4% y/y, exposing revenues to regional swings.

Energy throughput correlates with mobility and industrial activity—global oil product demand rose about 1.5% in 2024, affecting downstream margins.

Geographic diversification across EU, Turkey and MENA smooths shocks but raises coordination and logistics costs for Koç’s multi-business portfolio.

Improved inventory buffers and production flexibility—shorter lead times, scalable plants—have measurably reduced sales volatility for similar peers by ~20%.

Commodity and energy price volatility

- Brent ~ $88/bbl (2024) — >30% oil/gas/metals swings

- Mitigants: vertical integration, long-term contracts, dynamic pricing

- Risk focus: basis vs liquidity and counterparty concentration

Household income and credit availability

- Auto sales ~800,000 units (2024)

- Consumer loans +18% y/y (2024)

- BNPL ~5% e‑commerce share (2024)

- Segmentation increases market breadth

Political shocks threaten margins: FX, gas dependence and EU export exposure

High inflation (>50% in 2024), TRY ~-30% vs USD (2022–24) and Brent ~$88/bbl (2024) raise imported input and hedging costs, squeezing margins. Exports ~40% of group sales and centralized treasury partly hedge FX; auto sales ~800k (2024) and consumer loans +18% y/y support demand. BNPL ~5% e‑commerce share raises credit provisioning needs.

| Metric | 2024 |

|---|---|

| Inflation | >50% |

| TRY vs USD (2022–24) | -30% |

| Brent | $88/bbl |

| Exports share | ~40% |

| Auto sales | ~800k |

| Consumer loans | +18% y/y |

| BNPL | ~5% |

Same Document Delivered

Koç Holding PESTLE Analysis

This Koç Holding PESTLE Analysis provides a concise, structured review of political, economic, social, technological, legal and environmental factors affecting the group. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or surprises; you’ll download the final file immediately after payment.