KORE Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

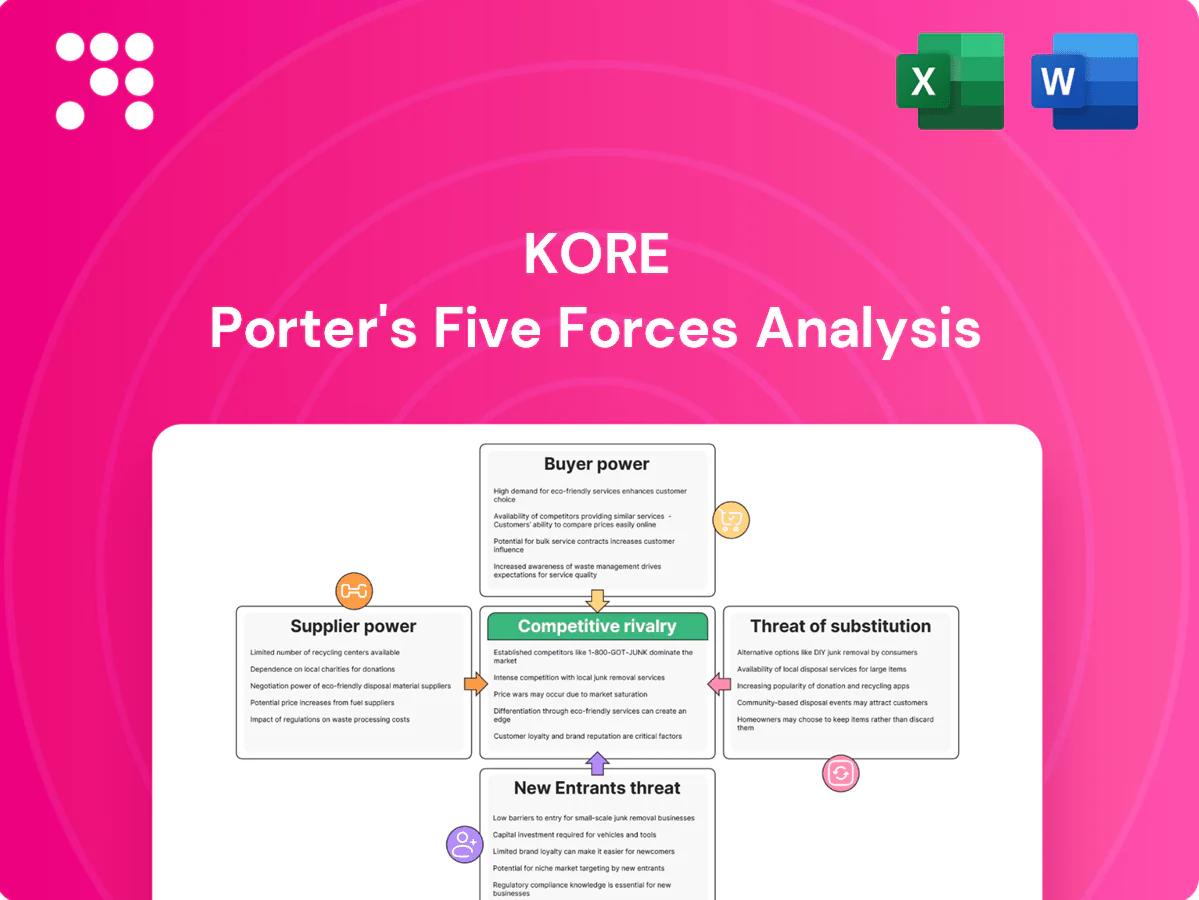

KORE’s Porter's Five Forces snapshot highlights supplier leverage, buyer power, rivalry intensity, threat of entrants, and substitutes, revealing pockets of competitive advantage and vulnerability. This brief overview points to strategic levers and market risks. Unlock the full report for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Concentrated carrier dependencies

Mobile network operators own spectrum and core connectivity, giving them leverage over MVNOs like KORE; as of 2024 fewer than 10 carriers offer true global Tier-1 coverage, limiting substitution options. Long-term roaming and wholesale contracts typically span 3–5 years, creating pricing floors and margin pressure. KORE mitigates this with multi-carrier eSIM and diversified carrier agreements, but carrier power remains materially constraining.

Specialized hardware and module vendors

IoT modules, eSIMs and certified devices are sourced from a concentrated set of OEMs, and long certification cycles plus periodic supply constraints shift bargaining power toward these vendors. Large-volume commitments let KORE negotiate better pricing and lead times, but design lock-in and proprietary stacks raise switching costs for customers. KORE’s multi-vendor catalog mitigates single-supplier risk yet cannot fully eliminate vendor influence.

Cloud and platform infrastructure reliance

Dependence on hyperscalers (AWS ~32%, Azure ~23%, GCP ~11% in 2024) gives suppliers pricing and architecture leverage, driving lock-in risks. Egress charges and proprietary services can materially raise TCO—customers report data egress and managed service premiums that effectively add double-digit percent costs. Enterprise agreements and volume discounts (often 10–30%) mitigate but scale dictates terms. Maintaining portability is an effective hedge yet adds ongoing engineering costs.

Satellite and LPWAN partnerships

Specialized coverage for satellite and LPWAN (LoRaWAN, private LTE/5G) is concentrated among a handful of suppliers—notably Iridium, Globalstar, Inmarsat and Swarm—giving suppliers leverage when customers need ubiquitous or remote coverage. Niche capabilities raise switching costs and can pressure margins when vendors bundle connectivity, device management and services. Diversifying access technologies (terrestrial LPWAN, private cellular and multiple satellite links) balances negotiation dynamics and reduces single‑supplier dependence.

- Supplier concentration: Iridium, Globalstar, Inmarsat, Swarm

- Risk: higher leverage when ubiquitous/remote coverage required

- Margin pressure: bundled connectivity + services

- Mitigation: diversify LPWAN, private LTE/5G, multi‑satellite partners

Standards, SIM, and certification ecosystems

GSMA eSIM standards, device certifications and security compliance act as a gatekeeping layer for KORE, with suppliers controlling tooling and certification slots who can directly raise timelines and costs; delays then ripple into revenue and go-to-market timing. KORE’s certification experience shortens cycles but cannot fully neutralize standards bottlenecks.

- GSMA eSIM & security compliance: gatekeeping

- Tooling/certification control: timeline/cost leverage

- KORE shortens but cannot eliminate delays

Carrier+hyperscaler concentration boosts IoT TCO; 32% signals lock-in

Mobile operators (fewer than 10 Tier‑1 global carriers in 2024) and concentrated IoT OEMs give suppliers strong leverage, with 3–5 year contracts creating pricing floors. Hyperscaler dependence (AWS 32%, Azure 23%, GCP 11% in 2024) raises TCO via egress and proprietary services. Satellite/LPWAN providers (Iridium, Globalstar, Inmarsat, Swarm) further constrain pricing for remote coverage.

| Supplier | 2024 share/notes | Impact |

|---|---|---|

| Carriers | Fewer than 10 global Tier‑1 | High pricing power, limited substitution |

| Hyperscalers | AWS 32%/Azure 23%/GCP 11% | Egress + proprietary lock‑in |

| Sat/LPWAN | Iridium, Globalstar, Inmarsat, Swarm | Premium for remote ubiquity |

| OEMs | Concentrated, long cert cycles | Switching costs, lead‑time risk |

What is included in the product

Tailored Porter's Five Forces for KORE: uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and emerging threats with strategic commentary and editable insights for reports.

KORE Porter's Five Forces delivers a clean one-sheet summary and interactive radar visualization so teams quickly spot strategic pressure; duplicate tabs for scenarios and swap in your data—no macros, easy to share in decks or dashboards.

Customers Bargaining Power

Large enterprises with scale

Global IoT deployments—GSMA projects cellular IoT connections to exceed 5 billion by 2025—drive high SIM counts and multi‑year contracts, boosting buyer leverage. Enterprises run formal RFPs demanding volume discounts and stringent SLAs, and churn risk can force mid‑single‑digit to low‑double‑digit price concessions. KORE must offset pressure with differentiated coverage, vertical solutions, and superior service quality to preserve margins.

Price transparency and commoditization

Per-SIM pricing transparency in 2024 drove visible margin compression, with average IoT SIM tariffs declining an estimated 15% year-over-year in key markets; aggressive MVNO/MNO offers, freemium tiers and flat-fee models intensified bargaining power. Buyers now benchmark rates across 50+ regions in minutes, forcing commoditization. KORE defends ARPU via bundled value, vertical outcomes-based pricing and managed services that preserve higher-yield revenues.

Switching costs versus integration lock-in

Platform integrations, device credentials and bespoke workflows create real switching friction for KORE customers, increasing lock-in as deployments scale; KORE reported lifecycle services contributed to higher retention trends in 2024. Standards-based APIs and rising eUICC adoption—eUICC deployments grew roughly 28% in 2024—make multi-sourcing more feasible, and about 40% of sophisticated buyers dual-source to preserve flexibility. KORE’s lifecycle and orchestration services aim to raise stickiness beyond pure connectivity by embedding device management and billing into client ecosystems.

Demand for compliance and security

Buyers demand certifications, data residency, and sector-specific compliance, increasing solution complexity and giving customers leverage to impose custom contract terms; non-compliance can cost deals. With global cybersecurity spending near $200B in 2024, KORE’s managed security and regulatory know-how can convert compliance demands into premium, higher-margin services.

- Certifications required

- Data residency clauses

- Sector-specific controls

- Non-compliance = lost deals

- KORE can monetize compliance

Vertical solution expectations

Customers now demand end-to-end vertical solutions across fleet, healthcare, and industrial IoT, pressing vendors to bundle devices, connectivity, analytics, and 24/7 support; Scope creep is cited by industry reports as a chief margin pressure, with some providers reporting gross margin erosion of 5–10 percentage points on unmanaged projects in 2024.

- Bundled demand: devices+connectivity+analytics+support

- Margin risk: scope creep → 5–10% gross margin erosion (2024)

- Mitigation: clear packaging and SLAs to protect profitability

IoT buyers force -15% SIM tariffs; eUICC +28%, ≈40% dual-sourcing

Customers hold elevated bargaining power: large-scale IoT deployments and formal RFPs force volume discounts and SLAs, driving ~15% YoY SIM tariff declines in 2024. Platform lock-in limits churn but rising eUICC (+28% in 2024) and 40% dual-sourcing by sophisticated buyers increase switching options. Compliance and cybersecurity demand (global spend ≈ $200B in 2024) lets KORE upsell managed services.

| Metric | 2024 |

|---|---|

| Avg SIM tariff change | -15% YoY |

| eUICC growth | +28% |

| Dual-sourcing buyers | ≈40% |

| Cybersecurity spend | ≈$200B |

Same Document Delivered

KORE Porter's Five Forces Analysis

This preview shows the exact KORE Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted and ready for use the moment you buy. You're looking at the actual deliverable; upon payment you’ll get instant access to this exact file.

Go Beyond the Preview—Access the Full Strategic Report

KORE’s Porter's Five Forces snapshot highlights supplier leverage, buyer power, rivalry intensity, threat of entrants, and substitutes, revealing pockets of competitive advantage and vulnerability. This brief overview points to strategic levers and market risks. Unlock the full report for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Concentrated carrier dependencies

Mobile network operators own spectrum and core connectivity, giving them leverage over MVNOs like KORE; as of 2024 fewer than 10 carriers offer true global Tier-1 coverage, limiting substitution options. Long-term roaming and wholesale contracts typically span 3–5 years, creating pricing floors and margin pressure. KORE mitigates this with multi-carrier eSIM and diversified carrier agreements, but carrier power remains materially constraining.

Specialized hardware and module vendors

IoT modules, eSIMs and certified devices are sourced from a concentrated set of OEMs, and long certification cycles plus periodic supply constraints shift bargaining power toward these vendors. Large-volume commitments let KORE negotiate better pricing and lead times, but design lock-in and proprietary stacks raise switching costs for customers. KORE’s multi-vendor catalog mitigates single-supplier risk yet cannot fully eliminate vendor influence.

Cloud and platform infrastructure reliance

Dependence on hyperscalers (AWS ~32%, Azure ~23%, GCP ~11% in 2024) gives suppliers pricing and architecture leverage, driving lock-in risks. Egress charges and proprietary services can materially raise TCO—customers report data egress and managed service premiums that effectively add double-digit percent costs. Enterprise agreements and volume discounts (often 10–30%) mitigate but scale dictates terms. Maintaining portability is an effective hedge yet adds ongoing engineering costs.

Satellite and LPWAN partnerships

Specialized coverage for satellite and LPWAN (LoRaWAN, private LTE/5G) is concentrated among a handful of suppliers—notably Iridium, Globalstar, Inmarsat and Swarm—giving suppliers leverage when customers need ubiquitous or remote coverage. Niche capabilities raise switching costs and can pressure margins when vendors bundle connectivity, device management and services. Diversifying access technologies (terrestrial LPWAN, private cellular and multiple satellite links) balances negotiation dynamics and reduces single‑supplier dependence.

- Supplier concentration: Iridium, Globalstar, Inmarsat, Swarm

- Risk: higher leverage when ubiquitous/remote coverage required

- Margin pressure: bundled connectivity + services

- Mitigation: diversify LPWAN, private LTE/5G, multi‑satellite partners

Standards, SIM, and certification ecosystems

GSMA eSIM standards, device certifications and security compliance act as a gatekeeping layer for KORE, with suppliers controlling tooling and certification slots who can directly raise timelines and costs; delays then ripple into revenue and go-to-market timing. KORE’s certification experience shortens cycles but cannot fully neutralize standards bottlenecks.

- GSMA eSIM & security compliance: gatekeeping

- Tooling/certification control: timeline/cost leverage

- KORE shortens but cannot eliminate delays

Carrier+hyperscaler concentration boosts IoT TCO; 32% signals lock-in

Mobile operators (fewer than 10 Tier‑1 global carriers in 2024) and concentrated IoT OEMs give suppliers strong leverage, with 3–5 year contracts creating pricing floors. Hyperscaler dependence (AWS 32%, Azure 23%, GCP 11% in 2024) raises TCO via egress and proprietary services. Satellite/LPWAN providers (Iridium, Globalstar, Inmarsat, Swarm) further constrain pricing for remote coverage.

| Supplier | 2024 share/notes | Impact |

|---|---|---|

| Carriers | Fewer than 10 global Tier‑1 | High pricing power, limited substitution |

| Hyperscalers | AWS 32%/Azure 23%/GCP 11% | Egress + proprietary lock‑in |

| Sat/LPWAN | Iridium, Globalstar, Inmarsat, Swarm | Premium for remote ubiquity |

| OEMs | Concentrated, long cert cycles | Switching costs, lead‑time risk |

What is included in the product

Tailored Porter's Five Forces for KORE: uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and emerging threats with strategic commentary and editable insights for reports.

KORE Porter's Five Forces delivers a clean one-sheet summary and interactive radar visualization so teams quickly spot strategic pressure; duplicate tabs for scenarios and swap in your data—no macros, easy to share in decks or dashboards.

Customers Bargaining Power

Large enterprises with scale

Global IoT deployments—GSMA projects cellular IoT connections to exceed 5 billion by 2025—drive high SIM counts and multi‑year contracts, boosting buyer leverage. Enterprises run formal RFPs demanding volume discounts and stringent SLAs, and churn risk can force mid‑single‑digit to low‑double‑digit price concessions. KORE must offset pressure with differentiated coverage, vertical solutions, and superior service quality to preserve margins.

Price transparency and commoditization

Per-SIM pricing transparency in 2024 drove visible margin compression, with average IoT SIM tariffs declining an estimated 15% year-over-year in key markets; aggressive MVNO/MNO offers, freemium tiers and flat-fee models intensified bargaining power. Buyers now benchmark rates across 50+ regions in minutes, forcing commoditization. KORE defends ARPU via bundled value, vertical outcomes-based pricing and managed services that preserve higher-yield revenues.

Switching costs versus integration lock-in

Platform integrations, device credentials and bespoke workflows create real switching friction for KORE customers, increasing lock-in as deployments scale; KORE reported lifecycle services contributed to higher retention trends in 2024. Standards-based APIs and rising eUICC adoption—eUICC deployments grew roughly 28% in 2024—make multi-sourcing more feasible, and about 40% of sophisticated buyers dual-source to preserve flexibility. KORE’s lifecycle and orchestration services aim to raise stickiness beyond pure connectivity by embedding device management and billing into client ecosystems.

Demand for compliance and security

Buyers demand certifications, data residency, and sector-specific compliance, increasing solution complexity and giving customers leverage to impose custom contract terms; non-compliance can cost deals. With global cybersecurity spending near $200B in 2024, KORE’s managed security and regulatory know-how can convert compliance demands into premium, higher-margin services.

- Certifications required

- Data residency clauses

- Sector-specific controls

- Non-compliance = lost deals

- KORE can monetize compliance

Vertical solution expectations

Customers now demand end-to-end vertical solutions across fleet, healthcare, and industrial IoT, pressing vendors to bundle devices, connectivity, analytics, and 24/7 support; Scope creep is cited by industry reports as a chief margin pressure, with some providers reporting gross margin erosion of 5–10 percentage points on unmanaged projects in 2024.

- Bundled demand: devices+connectivity+analytics+support

- Margin risk: scope creep → 5–10% gross margin erosion (2024)

- Mitigation: clear packaging and SLAs to protect profitability

IoT buyers force -15% SIM tariffs; eUICC +28%, ≈40% dual-sourcing

Customers hold elevated bargaining power: large-scale IoT deployments and formal RFPs force volume discounts and SLAs, driving ~15% YoY SIM tariff declines in 2024. Platform lock-in limits churn but rising eUICC (+28% in 2024) and 40% dual-sourcing by sophisticated buyers increase switching options. Compliance and cybersecurity demand (global spend ≈ $200B in 2024) lets KORE upsell managed services.

| Metric | 2024 |

|---|---|

| Avg SIM tariff change | -15% YoY |

| eUICC growth | +28% |

| Dual-sourcing buyers | ≈40% |

| Cybersecurity spend | ≈$200B |

Same Document Delivered

KORE Porter's Five Forces Analysis

This preview shows the exact KORE Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted and ready for use the moment you buy. You're looking at the actual deliverable; upon payment you’ll get instant access to this exact file.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

KORE’s Porter's Five Forces snapshot highlights supplier leverage, buyer power, rivalry intensity, threat of entrants, and substitutes, revealing pockets of competitive advantage and vulnerability. This brief overview points to strategic levers and market risks. Unlock the full report for force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Concentrated carrier dependencies

Mobile network operators own spectrum and core connectivity, giving them leverage over MVNOs like KORE; as of 2024 fewer than 10 carriers offer true global Tier-1 coverage, limiting substitution options. Long-term roaming and wholesale contracts typically span 3–5 years, creating pricing floors and margin pressure. KORE mitigates this with multi-carrier eSIM and diversified carrier agreements, but carrier power remains materially constraining.

Specialized hardware and module vendors

IoT modules, eSIMs and certified devices are sourced from a concentrated set of OEMs, and long certification cycles plus periodic supply constraints shift bargaining power toward these vendors. Large-volume commitments let KORE negotiate better pricing and lead times, but design lock-in and proprietary stacks raise switching costs for customers. KORE’s multi-vendor catalog mitigates single-supplier risk yet cannot fully eliminate vendor influence.

Cloud and platform infrastructure reliance

Dependence on hyperscalers (AWS ~32%, Azure ~23%, GCP ~11% in 2024) gives suppliers pricing and architecture leverage, driving lock-in risks. Egress charges and proprietary services can materially raise TCO—customers report data egress and managed service premiums that effectively add double-digit percent costs. Enterprise agreements and volume discounts (often 10–30%) mitigate but scale dictates terms. Maintaining portability is an effective hedge yet adds ongoing engineering costs.

Satellite and LPWAN partnerships

Specialized coverage for satellite and LPWAN (LoRaWAN, private LTE/5G) is concentrated among a handful of suppliers—notably Iridium, Globalstar, Inmarsat and Swarm—giving suppliers leverage when customers need ubiquitous or remote coverage. Niche capabilities raise switching costs and can pressure margins when vendors bundle connectivity, device management and services. Diversifying access technologies (terrestrial LPWAN, private cellular and multiple satellite links) balances negotiation dynamics and reduces single‑supplier dependence.

- Supplier concentration: Iridium, Globalstar, Inmarsat, Swarm

- Risk: higher leverage when ubiquitous/remote coverage required

- Margin pressure: bundled connectivity + services

- Mitigation: diversify LPWAN, private LTE/5G, multi‑satellite partners

Standards, SIM, and certification ecosystems

GSMA eSIM standards, device certifications and security compliance act as a gatekeeping layer for KORE, with suppliers controlling tooling and certification slots who can directly raise timelines and costs; delays then ripple into revenue and go-to-market timing. KORE’s certification experience shortens cycles but cannot fully neutralize standards bottlenecks.

- GSMA eSIM & security compliance: gatekeeping

- Tooling/certification control: timeline/cost leverage

- KORE shortens but cannot eliminate delays

Carrier+hyperscaler concentration boosts IoT TCO; 32% signals lock-in

Mobile operators (fewer than 10 Tier‑1 global carriers in 2024) and concentrated IoT OEMs give suppliers strong leverage, with 3–5 year contracts creating pricing floors. Hyperscaler dependence (AWS 32%, Azure 23%, GCP 11% in 2024) raises TCO via egress and proprietary services. Satellite/LPWAN providers (Iridium, Globalstar, Inmarsat, Swarm) further constrain pricing for remote coverage.

| Supplier | 2024 share/notes | Impact |

|---|---|---|

| Carriers | Fewer than 10 global Tier‑1 | High pricing power, limited substitution |

| Hyperscalers | AWS 32%/Azure 23%/GCP 11% | Egress + proprietary lock‑in |

| Sat/LPWAN | Iridium, Globalstar, Inmarsat, Swarm | Premium for remote ubiquity |

| OEMs | Concentrated, long cert cycles | Switching costs, lead‑time risk |

What is included in the product

Tailored Porter's Five Forces for KORE: uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and emerging threats with strategic commentary and editable insights for reports.

KORE Porter's Five Forces delivers a clean one-sheet summary and interactive radar visualization so teams quickly spot strategic pressure; duplicate tabs for scenarios and swap in your data—no macros, easy to share in decks or dashboards.

Customers Bargaining Power

Large enterprises with scale

Global IoT deployments—GSMA projects cellular IoT connections to exceed 5 billion by 2025—drive high SIM counts and multi‑year contracts, boosting buyer leverage. Enterprises run formal RFPs demanding volume discounts and stringent SLAs, and churn risk can force mid‑single‑digit to low‑double‑digit price concessions. KORE must offset pressure with differentiated coverage, vertical solutions, and superior service quality to preserve margins.

Price transparency and commoditization

Per-SIM pricing transparency in 2024 drove visible margin compression, with average IoT SIM tariffs declining an estimated 15% year-over-year in key markets; aggressive MVNO/MNO offers, freemium tiers and flat-fee models intensified bargaining power. Buyers now benchmark rates across 50+ regions in minutes, forcing commoditization. KORE defends ARPU via bundled value, vertical outcomes-based pricing and managed services that preserve higher-yield revenues.

Switching costs versus integration lock-in

Platform integrations, device credentials and bespoke workflows create real switching friction for KORE customers, increasing lock-in as deployments scale; KORE reported lifecycle services contributed to higher retention trends in 2024. Standards-based APIs and rising eUICC adoption—eUICC deployments grew roughly 28% in 2024—make multi-sourcing more feasible, and about 40% of sophisticated buyers dual-source to preserve flexibility. KORE’s lifecycle and orchestration services aim to raise stickiness beyond pure connectivity by embedding device management and billing into client ecosystems.

Demand for compliance and security

Buyers demand certifications, data residency, and sector-specific compliance, increasing solution complexity and giving customers leverage to impose custom contract terms; non-compliance can cost deals. With global cybersecurity spending near $200B in 2024, KORE’s managed security and regulatory know-how can convert compliance demands into premium, higher-margin services.

- Certifications required

- Data residency clauses

- Sector-specific controls

- Non-compliance = lost deals

- KORE can monetize compliance

Vertical solution expectations

Customers now demand end-to-end vertical solutions across fleet, healthcare, and industrial IoT, pressing vendors to bundle devices, connectivity, analytics, and 24/7 support; Scope creep is cited by industry reports as a chief margin pressure, with some providers reporting gross margin erosion of 5–10 percentage points on unmanaged projects in 2024.

- Bundled demand: devices+connectivity+analytics+support

- Margin risk: scope creep → 5–10% gross margin erosion (2024)

- Mitigation: clear packaging and SLAs to protect profitability

IoT buyers force -15% SIM tariffs; eUICC +28%, ≈40% dual-sourcing

Customers hold elevated bargaining power: large-scale IoT deployments and formal RFPs force volume discounts and SLAs, driving ~15% YoY SIM tariff declines in 2024. Platform lock-in limits churn but rising eUICC (+28% in 2024) and 40% dual-sourcing by sophisticated buyers increase switching options. Compliance and cybersecurity demand (global spend ≈ $200B in 2024) lets KORE upsell managed services.

| Metric | 2024 |

|---|---|

| Avg SIM tariff change | -15% YoY |

| eUICC growth | +28% |

| Dual-sourcing buyers | ≈40% |

| Cybersecurity spend | ≈$200B |

Same Document Delivered

KORE Porter's Five Forces Analysis

This preview shows the exact KORE Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted and ready for use the moment you buy. You're looking at the actual deliverable; upon payment you’ll get instant access to this exact file.