Kotak Mahindra Bank Boston Consulting Group Matrix

See the Bigger Picture

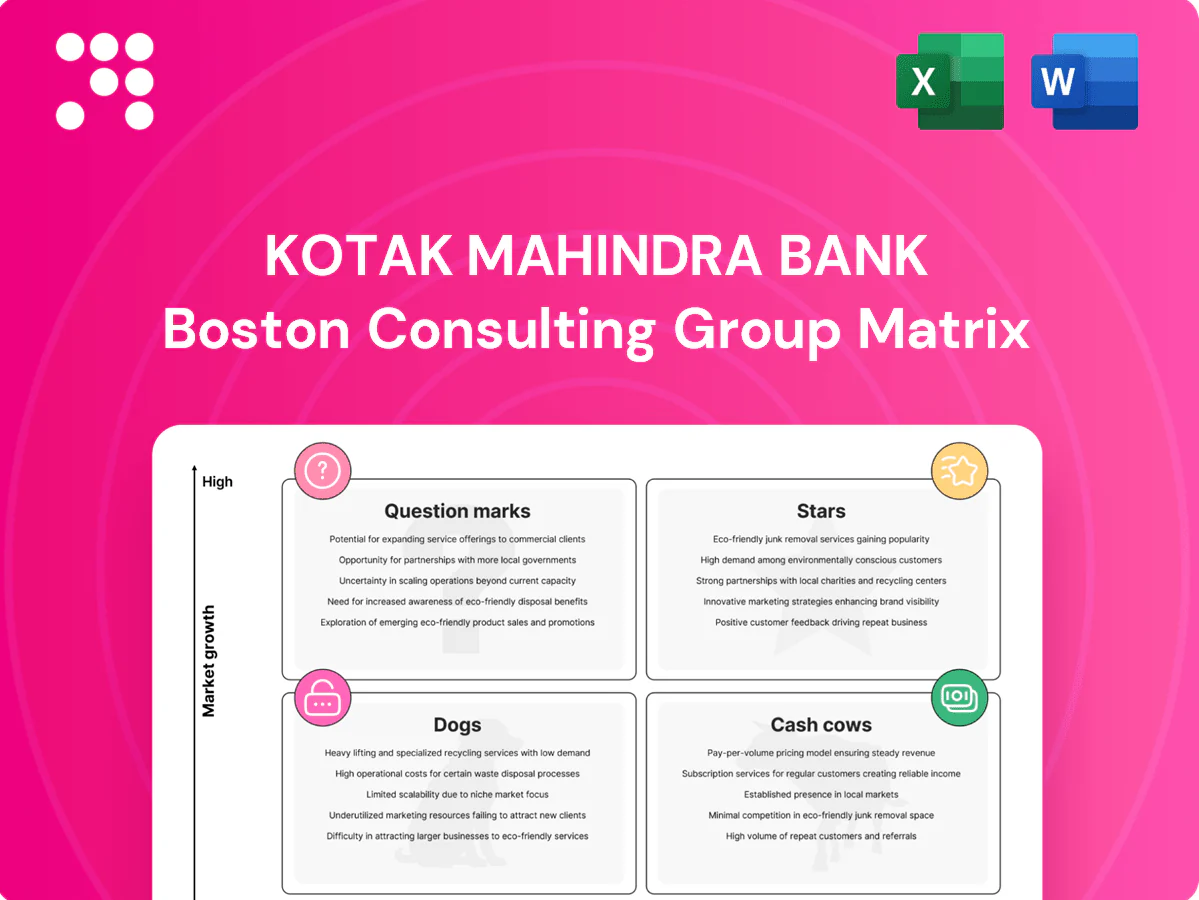

Kotak Mahindra Bank’s BCG Matrix snapshot shows where its retail, corporate, and digital offerings land—who’s fueling growth, who’s funding it, and which units need a rethink. This quick view teases strategic patterns; the full BCG Matrix gives you quadrant-by-quadrant placements, data-driven recommendations, and clear next steps. Buy the complete report for a ready-to-use Word briefing plus an Excel summary—cut the analysis time and start making smarter allocation and product decisions today.

Stars

Digital retail banking & mobile app

Digital retail banking through Kotak’s mobile app sits in Stars: strong digital adoption continues to accelerate and the app’s UX and feature set consistently pull users into higher engagement and transaction frequency, showing sticky daily usage patterns. Continued investment in UX, security and cloud scale is required to sustain growth and protect share. If maintained, it can transition into a compounding cash engine.

Affluent/Private banking & wealth management

Kotak Mahindra Bank’s affluent/private banking unit projects leader vibes in India’s fast-expanding wealth market, with Kotak Wealth reporting AUM of about Rs 2.1 lakh crore in 2024 and high wallet share among HNI/ultra-HNI clients.

Strong advisory and execution capabilities, deep product breadth and brand-led trust underpin its position, but sustaining the lead requires top-tier talent and continuous product investment.

Keep investing to defend market share as competition from private banks, boutiques and family offices intensifies across advisory, custody and discretionary mandates.

Corporate & Investment Banking (ECM/DCM/M&A)

Deal flow in India remains buoyant and Kotak’s corporate & investment banking franchise is well placed, with visible league-table presence, repeat mandates and strong syndication capabilities. Capital-hungry growth sectors require heavy relationship and balance-sheet support, leveraging Kotak’s consolidated assets of about INR 6.2 trillion (March 2024). With current momentum it can convert mandates into recurring Cash Cow fee streams over time.

Credit cards & affluent unsecured lending

Credit cards and affluent unsecured lending are Stars for Kotak Mahindra Bank: premium yields and cross-sell drive a fast-growing profit pool, with India credit-card spends up about 20% YoY in 2024 supporting scale. Scaling acquisitions via partnerships and digital funnels is working, but success needs marketing spend, advanced risk analytics and loyalty economics to click; the right mix creates a durable flywheel.

- Premium yields

- Cross-sell leverage

- Partnerships + digital funnels

- Marketing, risk analytics, loyalty required

- Flywheel potential

Transaction banking for mid–large corporates

Transaction banking for mid–large corporates is a Stars quadrant win: cash management, APIs and trade flows scale with economic activity and, once embedded, create high switching costs that lock in share; sustaining this requires continual platform upgrades and dedicated RM coverage to monetize compounding volumes.

- Cash management scale

- API-led stickiness

- Trade flow compounding

- Needs tech + RM investment

Digital retail & affluent banking: AUM Rs 2.1 lakh crore, cards +20%

Kotak’s digital retail app, affluent/private banking (AUM ~Rs 2.1 lakh crore in 2024) and cards/unsecured lending (India card spends +20% YoY in 2024) sit in Stars—high growth, strong engagement and premium yields. Transaction banking and CIB show scaling fee potential supported by consolidated assets ~Rs 6.2 trillion (Mar 2024). Continued UX, cloud, risk analytics and RM investment required to lock in flywheels.

| Business | 2024 Metric | Implication |

|---|---|---|

| Affluent/Wealth | AUM Rs 2.1 lakh crore | High growth, wallet share |

| Cards & unsecured | Card spends +20% YoY | Premium yields, scale |

| Group assets | Rs 6.2 trillion (Mar 2024) | Balance-sheet support |

What is included in the product

Concise BCG Matrix for Kotak Mahindra Bank: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold or divest recommendations.

One-page BCG matrix placing Kotak Mahindra business units in quadrants—clean, export-ready for C-suite sharing.

Cash Cows

CASA deposits franchise

Large, sticky low-cost CASA deposits fund Kotak Mahindra Bank’s whole engine. Mature market still offers productivity gains; CASA ratio was about 46% with CASA deposits near Rs 3.1 lakh crore as of March 2024. Low promo intensity once the base is built, providing margin stability and liquidity optionality.

Home loans (prime mortgages)

Home loans (prime mortgages) deliver defensive yields with low credit losses and steady demand, forming a large, predictable volume base for Kotak Mahindra Bank. Growth is moderate while origination volumes are stable, minimizing promotional spend beyond deep distribution. Focus on optimizing sourcing cost and streamlining processing can meaningfully widen spreads and net interest margins.

Vehicle finance (secured retail)

Vehicle finance (secured retail) is a well-understood book for Kotak Mahindra Bank, offering stable risk and scale advantages; retail secured loans helped keep consolidated GNPA around 1.3% in FY2024 while lending remained steady. Market growth is steady rather than explosive, supporting predictable cash generation. Strong cross-sell and disciplined collections drive cash; incremental process tech lifts ROE without heavy incremental spend.

Fee income from distribution (MFs, insurance, bonds)

Fee income from distribution is a recurring, capital-light revenue stream for Kotak, drawing from a wide customer base; Indian mutual fund AUM reached about INR 47 lakh crore by Dec 2024, underlining scale in the market. Metros are mature so growth is incremental, but low capex and strong margins help smooth earnings; product-shelf focus and strict compliance remain critical.

- Recurring, capital-light fees

- Metros mature; incremental expansion

- Low capex, high margins — earnings stability

- Keep product shelves sharp

- Tight compliance

Trade services & FX for established clients

Trade services and FX for established Kotak clients deliver high-repeat, fee-led revenues backed by entrenched corporate and HNI relationships; market growth is modest while Kotak’s share remains durable. The business needs incremental system upgrades rather than large strategic bets and provides steady cash to fund higher-growth initiatives.

- High-repeat fees

- Durable market share

- Modest growth

- Requires incremental tech spend

- Reliable cash generation

Capital-light growth: 46% CASA, Rs 3.1L cr, 1.3% GNPA

Kotak’s cash cows—CASA, home loans, vehicle finance, distribution and trade—produce stable, capital-light cash flow funding growth initiatives. CASA ratio ~46% with CASA deposits ~Rs 3.1 lakh crore (Mar 2024); consolidated GNPA ~1.3% (FY2024). Distribution benefits from large market AUM ~Rs 47 lakh crore (Dec 2024) and low incremental capex needs.

| Segment | Metric | 2024 |

|---|---|---|

| CASA | Ratio / Deposits | 46% / Rs 3.1L cr |

| Home loans | Risk / Demand | Low loss / Stable |

| Vehicle finance | GNPA | Consol GNPA 1.3% |

| Distribution | Market AUM | Rs 47L cr |

What You’re Viewing Is Included

Kotak Mahindra Bank BCG Matrix

The file you're previewing here is the exact Kotak Mahindra Bank BCG Matrix you'll receive after purchase. No watermarks, no placeholder slides—just the fully formatted, analysis-ready report built for strategic clarity. After buying you get the same editable, print-ready document delivered immediately to your inbox, ready for presentations or planning. What you see is what you’ll use—no surprises, no edits required.

See the Bigger Picture

Kotak Mahindra Bank’s BCG Matrix snapshot shows where its retail, corporate, and digital offerings land—who’s fueling growth, who’s funding it, and which units need a rethink. This quick view teases strategic patterns; the full BCG Matrix gives you quadrant-by-quadrant placements, data-driven recommendations, and clear next steps. Buy the complete report for a ready-to-use Word briefing plus an Excel summary—cut the analysis time and start making smarter allocation and product decisions today.

Stars

Digital retail banking & mobile app

Digital retail banking through Kotak’s mobile app sits in Stars: strong digital adoption continues to accelerate and the app’s UX and feature set consistently pull users into higher engagement and transaction frequency, showing sticky daily usage patterns. Continued investment in UX, security and cloud scale is required to sustain growth and protect share. If maintained, it can transition into a compounding cash engine.

Affluent/Private banking & wealth management

Kotak Mahindra Bank’s affluent/private banking unit projects leader vibes in India’s fast-expanding wealth market, with Kotak Wealth reporting AUM of about Rs 2.1 lakh crore in 2024 and high wallet share among HNI/ultra-HNI clients.

Strong advisory and execution capabilities, deep product breadth and brand-led trust underpin its position, but sustaining the lead requires top-tier talent and continuous product investment.

Keep investing to defend market share as competition from private banks, boutiques and family offices intensifies across advisory, custody and discretionary mandates.

Corporate & Investment Banking (ECM/DCM/M&A)

Deal flow in India remains buoyant and Kotak’s corporate & investment banking franchise is well placed, with visible league-table presence, repeat mandates and strong syndication capabilities. Capital-hungry growth sectors require heavy relationship and balance-sheet support, leveraging Kotak’s consolidated assets of about INR 6.2 trillion (March 2024). With current momentum it can convert mandates into recurring Cash Cow fee streams over time.

Credit cards & affluent unsecured lending

Credit cards and affluent unsecured lending are Stars for Kotak Mahindra Bank: premium yields and cross-sell drive a fast-growing profit pool, with India credit-card spends up about 20% YoY in 2024 supporting scale. Scaling acquisitions via partnerships and digital funnels is working, but success needs marketing spend, advanced risk analytics and loyalty economics to click; the right mix creates a durable flywheel.

- Premium yields

- Cross-sell leverage

- Partnerships + digital funnels

- Marketing, risk analytics, loyalty required

- Flywheel potential

Transaction banking for mid–large corporates

Transaction banking for mid–large corporates is a Stars quadrant win: cash management, APIs and trade flows scale with economic activity and, once embedded, create high switching costs that lock in share; sustaining this requires continual platform upgrades and dedicated RM coverage to monetize compounding volumes.

- Cash management scale

- API-led stickiness

- Trade flow compounding

- Needs tech + RM investment

Digital retail & affluent banking: AUM Rs 2.1 lakh crore, cards +20%

Kotak’s digital retail app, affluent/private banking (AUM ~Rs 2.1 lakh crore in 2024) and cards/unsecured lending (India card spends +20% YoY in 2024) sit in Stars—high growth, strong engagement and premium yields. Transaction banking and CIB show scaling fee potential supported by consolidated assets ~Rs 6.2 trillion (Mar 2024). Continued UX, cloud, risk analytics and RM investment required to lock in flywheels.

| Business | 2024 Metric | Implication |

|---|---|---|

| Affluent/Wealth | AUM Rs 2.1 lakh crore | High growth, wallet share |

| Cards & unsecured | Card spends +20% YoY | Premium yields, scale |

| Group assets | Rs 6.2 trillion (Mar 2024) | Balance-sheet support |

What is included in the product

Concise BCG Matrix for Kotak Mahindra Bank: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold or divest recommendations.

One-page BCG matrix placing Kotak Mahindra business units in quadrants—clean, export-ready for C-suite sharing.

Cash Cows

CASA deposits franchise

Large, sticky low-cost CASA deposits fund Kotak Mahindra Bank’s whole engine. Mature market still offers productivity gains; CASA ratio was about 46% with CASA deposits near Rs 3.1 lakh crore as of March 2024. Low promo intensity once the base is built, providing margin stability and liquidity optionality.

Home loans (prime mortgages)

Home loans (prime mortgages) deliver defensive yields with low credit losses and steady demand, forming a large, predictable volume base for Kotak Mahindra Bank. Growth is moderate while origination volumes are stable, minimizing promotional spend beyond deep distribution. Focus on optimizing sourcing cost and streamlining processing can meaningfully widen spreads and net interest margins.

Vehicle finance (secured retail)

Vehicle finance (secured retail) is a well-understood book for Kotak Mahindra Bank, offering stable risk and scale advantages; retail secured loans helped keep consolidated GNPA around 1.3% in FY2024 while lending remained steady. Market growth is steady rather than explosive, supporting predictable cash generation. Strong cross-sell and disciplined collections drive cash; incremental process tech lifts ROE without heavy incremental spend.

Fee income from distribution (MFs, insurance, bonds)

Fee income from distribution is a recurring, capital-light revenue stream for Kotak, drawing from a wide customer base; Indian mutual fund AUM reached about INR 47 lakh crore by Dec 2024, underlining scale in the market. Metros are mature so growth is incremental, but low capex and strong margins help smooth earnings; product-shelf focus and strict compliance remain critical.

- Recurring, capital-light fees

- Metros mature; incremental expansion

- Low capex, high margins — earnings stability

- Keep product shelves sharp

- Tight compliance

Trade services & FX for established clients

Trade services and FX for established Kotak clients deliver high-repeat, fee-led revenues backed by entrenched corporate and HNI relationships; market growth is modest while Kotak’s share remains durable. The business needs incremental system upgrades rather than large strategic bets and provides steady cash to fund higher-growth initiatives.

- High-repeat fees

- Durable market share

- Modest growth

- Requires incremental tech spend

- Reliable cash generation

Capital-light growth: 46% CASA, Rs 3.1L cr, 1.3% GNPA

Kotak’s cash cows—CASA, home loans, vehicle finance, distribution and trade—produce stable, capital-light cash flow funding growth initiatives. CASA ratio ~46% with CASA deposits ~Rs 3.1 lakh crore (Mar 2024); consolidated GNPA ~1.3% (FY2024). Distribution benefits from large market AUM ~Rs 47 lakh crore (Dec 2024) and low incremental capex needs.

| Segment | Metric | 2024 |

|---|---|---|

| CASA | Ratio / Deposits | 46% / Rs 3.1L cr |

| Home loans | Risk / Demand | Low loss / Stable |

| Vehicle finance | GNPA | Consol GNPA 1.3% |

| Distribution | Market AUM | Rs 47L cr |

What You’re Viewing Is Included

Kotak Mahindra Bank BCG Matrix

The file you're previewing here is the exact Kotak Mahindra Bank BCG Matrix you'll receive after purchase. No watermarks, no placeholder slides—just the fully formatted, analysis-ready report built for strategic clarity. After buying you get the same editable, print-ready document delivered immediately to your inbox, ready for presentations or planning. What you see is what you’ll use—no surprises, no edits required.

Original: $10.00

-65%$10.00

$3.50Description

See the Bigger Picture

Kotak Mahindra Bank’s BCG Matrix snapshot shows where its retail, corporate, and digital offerings land—who’s fueling growth, who’s funding it, and which units need a rethink. This quick view teases strategic patterns; the full BCG Matrix gives you quadrant-by-quadrant placements, data-driven recommendations, and clear next steps. Buy the complete report for a ready-to-use Word briefing plus an Excel summary—cut the analysis time and start making smarter allocation and product decisions today.

Stars

Digital retail banking & mobile app

Digital retail banking through Kotak’s mobile app sits in Stars: strong digital adoption continues to accelerate and the app’s UX and feature set consistently pull users into higher engagement and transaction frequency, showing sticky daily usage patterns. Continued investment in UX, security and cloud scale is required to sustain growth and protect share. If maintained, it can transition into a compounding cash engine.

Affluent/Private banking & wealth management

Kotak Mahindra Bank’s affluent/private banking unit projects leader vibes in India’s fast-expanding wealth market, with Kotak Wealth reporting AUM of about Rs 2.1 lakh crore in 2024 and high wallet share among HNI/ultra-HNI clients.

Strong advisory and execution capabilities, deep product breadth and brand-led trust underpin its position, but sustaining the lead requires top-tier talent and continuous product investment.

Keep investing to defend market share as competition from private banks, boutiques and family offices intensifies across advisory, custody and discretionary mandates.

Corporate & Investment Banking (ECM/DCM/M&A)

Deal flow in India remains buoyant and Kotak’s corporate & investment banking franchise is well placed, with visible league-table presence, repeat mandates and strong syndication capabilities. Capital-hungry growth sectors require heavy relationship and balance-sheet support, leveraging Kotak’s consolidated assets of about INR 6.2 trillion (March 2024). With current momentum it can convert mandates into recurring Cash Cow fee streams over time.

Credit cards & affluent unsecured lending

Credit cards and affluent unsecured lending are Stars for Kotak Mahindra Bank: premium yields and cross-sell drive a fast-growing profit pool, with India credit-card spends up about 20% YoY in 2024 supporting scale. Scaling acquisitions via partnerships and digital funnels is working, but success needs marketing spend, advanced risk analytics and loyalty economics to click; the right mix creates a durable flywheel.

- Premium yields

- Cross-sell leverage

- Partnerships + digital funnels

- Marketing, risk analytics, loyalty required

- Flywheel potential

Transaction banking for mid–large corporates

Transaction banking for mid–large corporates is a Stars quadrant win: cash management, APIs and trade flows scale with economic activity and, once embedded, create high switching costs that lock in share; sustaining this requires continual platform upgrades and dedicated RM coverage to monetize compounding volumes.

- Cash management scale

- API-led stickiness

- Trade flow compounding

- Needs tech + RM investment

Digital retail & affluent banking: AUM Rs 2.1 lakh crore, cards +20%

Kotak’s digital retail app, affluent/private banking (AUM ~Rs 2.1 lakh crore in 2024) and cards/unsecured lending (India card spends +20% YoY in 2024) sit in Stars—high growth, strong engagement and premium yields. Transaction banking and CIB show scaling fee potential supported by consolidated assets ~Rs 6.2 trillion (Mar 2024). Continued UX, cloud, risk analytics and RM investment required to lock in flywheels.

| Business | 2024 Metric | Implication |

|---|---|---|

| Affluent/Wealth | AUM Rs 2.1 lakh crore | High growth, wallet share |

| Cards & unsecured | Card spends +20% YoY | Premium yields, scale |

| Group assets | Rs 6.2 trillion (Mar 2024) | Balance-sheet support |

What is included in the product

Concise BCG Matrix for Kotak Mahindra Bank: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold or divest recommendations.

One-page BCG matrix placing Kotak Mahindra business units in quadrants—clean, export-ready for C-suite sharing.

Cash Cows

CASA deposits franchise

Large, sticky low-cost CASA deposits fund Kotak Mahindra Bank’s whole engine. Mature market still offers productivity gains; CASA ratio was about 46% with CASA deposits near Rs 3.1 lakh crore as of March 2024. Low promo intensity once the base is built, providing margin stability and liquidity optionality.

Home loans (prime mortgages)

Home loans (prime mortgages) deliver defensive yields with low credit losses and steady demand, forming a large, predictable volume base for Kotak Mahindra Bank. Growth is moderate while origination volumes are stable, minimizing promotional spend beyond deep distribution. Focus on optimizing sourcing cost and streamlining processing can meaningfully widen spreads and net interest margins.

Vehicle finance (secured retail)

Vehicle finance (secured retail) is a well-understood book for Kotak Mahindra Bank, offering stable risk and scale advantages; retail secured loans helped keep consolidated GNPA around 1.3% in FY2024 while lending remained steady. Market growth is steady rather than explosive, supporting predictable cash generation. Strong cross-sell and disciplined collections drive cash; incremental process tech lifts ROE without heavy incremental spend.

Fee income from distribution (MFs, insurance, bonds)

Fee income from distribution is a recurring, capital-light revenue stream for Kotak, drawing from a wide customer base; Indian mutual fund AUM reached about INR 47 lakh crore by Dec 2024, underlining scale in the market. Metros are mature so growth is incremental, but low capex and strong margins help smooth earnings; product-shelf focus and strict compliance remain critical.

- Recurring, capital-light fees

- Metros mature; incremental expansion

- Low capex, high margins — earnings stability

- Keep product shelves sharp

- Tight compliance

Trade services & FX for established clients

Trade services and FX for established Kotak clients deliver high-repeat, fee-led revenues backed by entrenched corporate and HNI relationships; market growth is modest while Kotak’s share remains durable. The business needs incremental system upgrades rather than large strategic bets and provides steady cash to fund higher-growth initiatives.

- High-repeat fees

- Durable market share

- Modest growth

- Requires incremental tech spend

- Reliable cash generation

Capital-light growth: 46% CASA, Rs 3.1L cr, 1.3% GNPA

Kotak’s cash cows—CASA, home loans, vehicle finance, distribution and trade—produce stable, capital-light cash flow funding growth initiatives. CASA ratio ~46% with CASA deposits ~Rs 3.1 lakh crore (Mar 2024); consolidated GNPA ~1.3% (FY2024). Distribution benefits from large market AUM ~Rs 47 lakh crore (Dec 2024) and low incremental capex needs.

| Segment | Metric | 2024 |

|---|---|---|

| CASA | Ratio / Deposits | 46% / Rs 3.1L cr |

| Home loans | Risk / Demand | Low loss / Stable |

| Vehicle finance | GNPA | Consol GNPA 1.3% |

| Distribution | Market AUM | Rs 47L cr |

What You’re Viewing Is Included

Kotak Mahindra Bank BCG Matrix

The file you're previewing here is the exact Kotak Mahindra Bank BCG Matrix you'll receive after purchase. No watermarks, no placeholder slides—just the fully formatted, analysis-ready report built for strategic clarity. After buying you get the same editable, print-ready document delivered immediately to your inbox, ready for presentations or planning. What you see is what you’ll use—no surprises, no edits required.